Insurers are feeling the pinch of climate change.

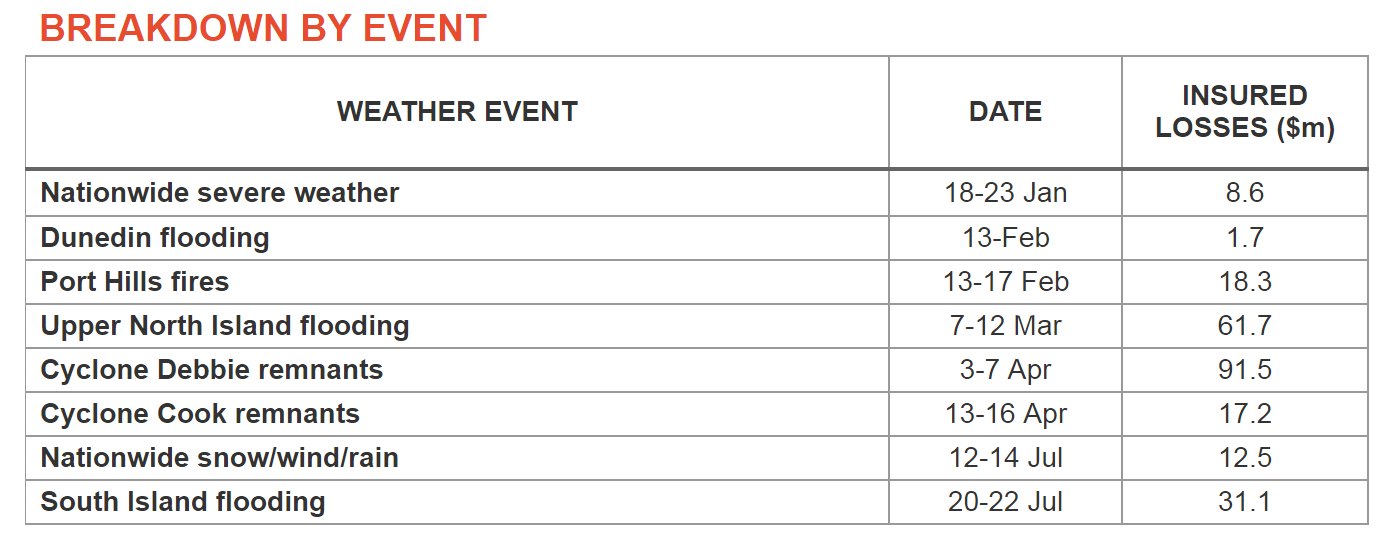

The Insurance Council (ICNZ) says 2017 has been the most expensive year on record for weather-related losses in New Zealand.

Totalling more than $242 million, the industry body’s CEO, Tim Grafton, says this is a “clear sign” of the impact of climate change.

“As time goes on, we expect to see more of these sorts of extreme weather events occurring,” he says.

The most expensive event of the year was the remnants of Cyclone Debbie, which struck in early April. That event resulted in 5,470 claims totalling $91.5 million in insured losses.

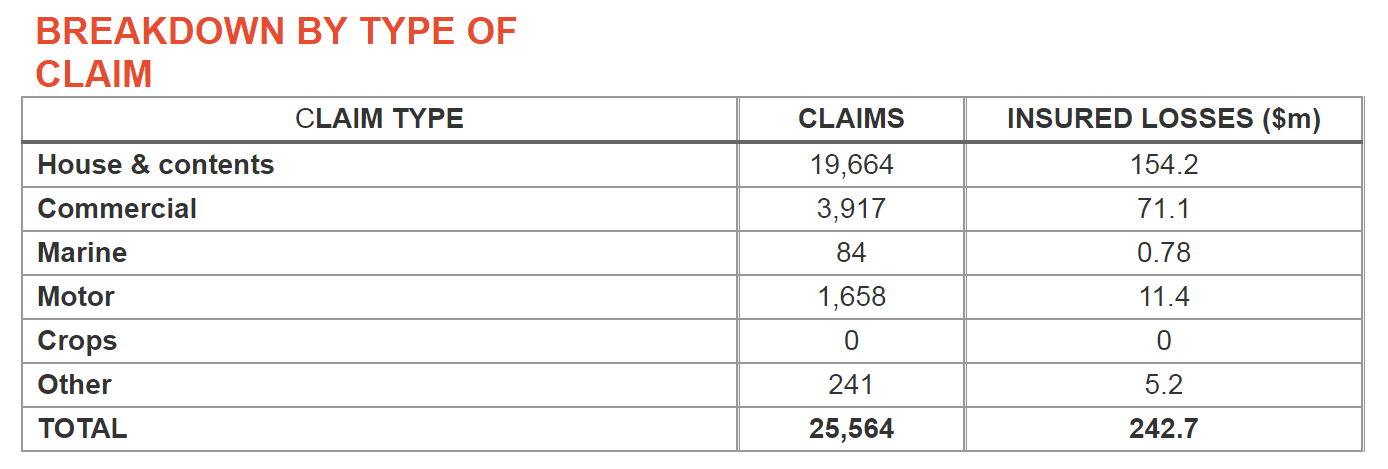

House and contents claims made up over half of all insured losses for the year, with a total cost of $154.2 million paid out by insurers.

Insurers hiking premiums to counter higher claims costs

Insurers recognise these weather-related events have impacted their profit margins.

IAG’s New Zealand division produced an insurance profit of A$125 million in 2017 financial year - an 8% drop from the previous year. Meanwhile Suncorp’s New Zealand general insurance division reduced its profit (before tax) by 63% to A$63 million.

However both insurers have flagged premium increases to counter rising claims costs.

In fact, three quarters of IAG’s consumer division gross written premium growth (of 5.5%) came from it charging higher premiums in the past year.

Recent weather events around the world might impact reinsurers’ pricing as well

As for the impact climate change is having on New Zealand’s risk profile from a reinsurer’s perspective, the Reserve Bank says insurers continue to be well supported by reinsurers.

In its latest biannual Financial Stability Report it says: “A series of extreme events, including hurricanes in the Caribbean and the United States and earthquakes in Mexico, has significantly impacted the profits of international reinsurers.

“At an aggregate level, recent events have the potential to impact reinsurance pricing and the scope of cover.

“For New Zealand, a more immediate issue for general insurers is likely to be the need to review levels of reinsurance in light of updates to catastrophe risk models following the Canterbury earthquakes.

“General insurers are required to hold catastrophe protection for a 1 in 1000 year event, and insurers will be reviewing their catastrophe cover to ensure they continue to meet this requirement.”

How insurers are handling higher risk properties

Jan Wright, during her time as Environment Commissioner, expressed concerns about rising seas making some coastal properties uninsurable.

While Grafton in July told interest.co.nz this was a possibility, he said insurers hadn’t made any drastic moves.

Vero executive manager for underwriting & portfolio management Don Smith said: “Climate change is something we’re continually looking at, but we haven’t yet made any changes similar to the blanket exclusions for damage by the sea in Australia. Vero is a subsidiary of Suncorp.

“It’s more likely that we’ll adopt a case by case approach where customers may be underwritten so they have no cover for certain types of damage.”

Meanwhile IAG’s Brendan McGillicuddy said: “We have not made any arbitrary decisions to refuse insurance cover in any locations in New Zealand based on flood risk or anticipated sea level rise, and the terms we apply to “at risk” properties are no harsher than they would have been five years ago.

“In regards to rising sea levels, this is not something that occurs suddenly and this means we do not expect to see people surprised by a sudden change to their insurance coverage.

“Councils have advanced a fair amount in mapping their territory to identify which properties are at risk from natural hazards such as flooding, and in particular, some councils have acknowledged that sea level rise has a material change in the risk profile of their territory.

“In response to this acknowledgement, the flood modelling that had been carried out previously might have been amended to account for an increase in the level of underground, river, lake and coastal water.

“This in turn is likely to have changed the classification the council puts on individual properties… so if more properties are identified as being “at risk” or if the level of risk is higher than previously believed, then we are likely to apply a higher premium and/or excess based on that revised classification.”

18 Comments

[ Cheap-shot smear removed. Ed ]

nothing

Fundamentally this is driven by a flawed model which insurance has grown into, and why Buffet bought into it, that rips of their clientele in the name of profit rather than genuinely insuring against risk.

Insurance premium models calculate the odds of any particular event from minor to catastrophic occurring in any one year, and a premium is made up of a price of each of those accountings. The problem is that for years the risk of major weather (or seismic) related events has been considered small, and the component of the premium that covers these has been equally small. What hasn't been paid out in claims in any one year is then taken as profit.

It should've been salted away as a growing investment to pay for the big one (think Cullen Fund), which the longer we go without, looms ever nearer and bigger. This is why so many insurance companies played hardball over the Christchurch earthquake claims. they blithely assumed a big one wouldn't happen on their watch, and when it did, were not resourced to pay the full cost of the claims. They see it as cheaper to wear litigants down with big lawyers than having integrity and paying out in good faith, and on principle.

It is past time to expose insurance companies for what they are, profiteering leeches, and regulate them to make sure they do their job properly or get out!

Exactly. No mention or allowance is made for the good years preceding this one. As evidenced by ChCh, they make exstensive us of time as a means of demonising the direct costs. The failing there is the massive hike in building costs offsetting the money gained by delaying.

Might suggest that non-profit societies (a la Southern Cross) are a better option for insurance than for-profit schemes.

a) If they were truly leeches with a rentier ability we'd see their profits rising, this doesnt seem to be the case.

b) Yes their model is now broken. Historically the model was perfectly sound so a 1 in 100 year event was factored in fine. However what the insurance companies have been seeing for the last few decades is an increase in both events and an intensification of top end events (given the water is warmer and hence more evaporation and heat ie basic physics hardly surprising). So in effect their 1 in 100 year event which they worked on can now be 1 in 20 or even 1 in 5. This means a huge increase in rates is looming and some areas wont be insurable.

c) Chch, actually this was considered a lower risk area and hence their under-priced the premiums. If you look at AMI its modeling seemed pretty sound and adequate, sadly an extreme event occured that was out of the playing area.

What worries me is the Govn was, is? considering being an insurer that means us the tax payer has to cover the risk. Now as someone who bought a house with care, comfortably above sea level in effect I could be called upon to cover others who bought on the beach stupidity, I object to that.

"Historically the model was perfectly sound so a 1 in 100 year event was factored in fine. However what the insurance companies have been seeing for the last few decades is an increase in both events and an intensification of top end events (given the water is warmer and hence more evaporation and heat ie basic physics hardly surprising)."

Personally I just don't see the evidence supporting this. What records are they using?

Some of the "major" earthquakes in NZ https://www.gns.cri.nz/gns/Home/Learning/Science-Topics/Earthquakes/New-Zealand-Earthquakes/Where-were-NZs-largest-earthquakes

Based on the above we have a "major" earthquake every 5-10 years. 1/100 is wishful thinking at best.

As for the weather, http://www.newshub.co.nz/home/new-zealand/2017/04/a-history-of-new-zealand-s-most-extreme-weather.html

You can see some more in-depth stats here https://hwe.niwa.co.nz/

Again, it appears that throughout reliable history, there have been a lot more events than the insurance modelling seems to be taking into account.

My (low-level) understanding is that it is part of the mandate of local bodies to notify the at-risk zones, which will impact on insurance premiums & resale. However the (usually wealthy & well-connected) residents issue a legal challenge & the zoning classification gets overturned.

So the "mapping" that this article refers to usually doesn't actually happen at all.

What's the consequence of this? Does the average premium-payer in a safe part of town then subsidise those by the sea shore or on cliff tops?

Insurers create their own risk maps. They use data from various sources that is common to some TA mapping but a TA risk designation on property being overturned by a well resourced litigant, wouldn't necessarily change the insurers flood calculations for that property, unless new hard data emerged from the case. Insurers know, usually down to specific addresses, which properties they wish to avoid insuring.

Grafton cites 'climate change' as the cause of a recent spike in reinsurers catastrophe events but offers no supporting evidence for his claim. These events could just as easily be a random spike. But it's more effective to use a populist justification as a softener because that's going to generate less kickback,

The 'softy, softly, no one's getting a dear John letter' approach from the insurers is because the insurers know increased sea levels from climate change is a long game. First phase out acceptance of new cover for houses in flood zones. Then observe existing policies and thus exposure numbers gradually diminish - houses are sold regularly and a proportion of new owners don't renew with the existing insurer, insurance lapses through non payment, banks become reluctant to lend in flood areas etc. Lastly, progressively increase 'disaster perils' claims excesses and apply inundation exclusions for the policies you have left on your books. Death by a thousand cuts, we'll hardly know it is happening.

There is and has been evidence for quite a while that CC events are increasing. The first I recall was from "munich" but there have been others since.

Some articles to take a look at,

http://www.rmmagazine.com/2015/02/03/climate-change-and-its-impact-on-t…

munich

http://evanmills.lbl.gov/pubs/pdf/climate-action-insurance.pdf

profound impact.

The chairman of Lloyd’s

of London has said that climate change is the number-

one issue for that massive insurance group. And Europe’s

largest insurer, Allianz, stated that climate change

stands to increase insured losses from extreme events

in an average year by 37 per cent within just a decade

http://www.smithsonianmag.com/science-nature/how-the-insurance-industry…

in recent years, the industry researchers who attempt to determine the annual odds of catastrophic weather-related disasters—including floods and wind storms—say they’re seeing something new.

This pronounced shift can be seen in extreme rainfall events, heat waves and wind storm.

https://www.genevaassociation.org/media/616661/ga2013-warming_of_the_oc…

You are correct I think.

Kapiti? tried to do just this and that got challenged by the "well off" in court. The trouble is/was Kapiti's model was overly simplistic and probably in-adequate the result was the court upheld the challenge. The council at that point gave up as they could not afford the cost of millions to develop models to do this.

The last I heard my understanding is the Councils are looking to central Government to provide guidance and leadership and even legislation and of course we have had National for 9 years who did not do a damn thing about it.

"So the "mapping" that this article refers to usually doesn't actually happen at all."

Correct.

"Does the average premium-payer in a safe part of town then subsidise those by the sea shore or on cliff tops?"

Yes and its peeing me off as in effect I cover the "rich" climate deniers, back to privitise the profits and socialise the losses again.

What's worse is Labour did consider (still do?) providing govn insurance scheme to cover as a challenge to private insurers. So this means PAYErs are facing an even bigger risk and cost covering property speculators who will pay no or little tax.

Its nuts frankly, but no one cares, they are quite prepared to gamble the call wont be made.

Meanwhile insurance companies will probably start to walk away,

"As these things become more certain, our appetite to offer insurance reduces. We insure people against risks – not certainties."

So once a claim is made I suspect the company will take a look at the property and then decline to re-insure.

https://www.stuff.co.nz/business/property/98797867/insurers-warn-climat…

I agree and without the ability to insure ones own home, then that home becomes virtually worthless. We would all be better off owning portable tiny homes that can be moved to areas less risky if our insurers start refusing to insure in areas that are prone to flooding and earthquakes for example.

We had the best Summer & Fall weather on the east coast

A better summer than I can remember with 31C temps common

Sad about Florida & Texas & USVirgin Is & PRico

In Auckland volcano land Rangitoto is long overdue to blow and when it does they’re projecting ash clouds 5 Kilometres radius

I’d make sure insurance was up to date

Our insurance companies would be bankrupt and out of money with todays current Auckland prices and most owners will be under-insured anyway. The money pool is a finite resource.

$242,700,000 expenses on 2,000,000,000 revenue sounds pretty good to me.

Insurance marketing speak. The “clear sign” the IPCC can’t find.

“Working Group II AR5:

“Economic growth, including greater concentrations of people and wealth in periled areas and rising insurance penetration, is the most important driver of increasing losses.” (AR5 10.7.3)

“Apart from detection, loss trends have not been conclusively attributed to anthropogenic climate change; most such claims are not based on scientific attribution methods.” (AR5 10.7.3)

“…increased probabilities of upward shifted accumulated loss [from tropical cyclones] might be detectable by 2025 at earliest, whereas a significant loss trend might emerge much later (Emanuel, 2011); (Crompton et al., 2011).” (AR5 10.7.3)

“The observed rise in US normalized insured flood losses (Barthel and Neumayer, 2012) may partly correspond to very likely increased heavy precipitation events in central North America (WG1-2.6.2.1), while the evidence for climate driven changes in river floods is not compelling (WG1-2.6.2.2)” (AR5 10.7.3)”

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.