Young people dominated the high level of KiwiSaver fund switching during the height of Covid-19 market volatility last year, according to research commissioned by regulator the Financial Markets Authority.

The research, carried out by PwC, found KiwiSaver members aged 26-35 made five times more fund switches than usual, while overall fund switching was three times higher than the normal volume.

FMA Manager - Investor Capability Gillian Boyes (pictured at right) said it was "concerning" that only 9.1% of people who switched to a lower risk fund from February to April 2020 ‘boomeranged’ back to a high growth fund by August.

"This meant a large portion of those who left growth funds would now be in a low-risk fund that may not align with their savings goals, especially if they were a long way from retirement," she said.

PwC compared and analysed fund switching data of 1.5 million KiwiSaver members from seven KiwiSaver providers – representing around half all KiwiSaver accounts. Switching data from February to April 2020 was compared to the same period in 2019.

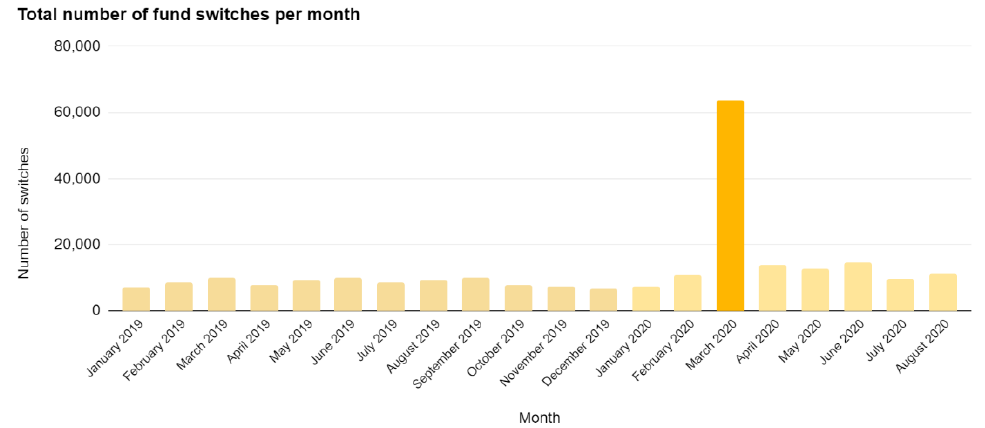

The report found 58,356 of the sample KiwiSaver members made 88,112 switches, meaning some made multiple switches. These switching members represented 3.9% of the total sample - 2.7 times higher than the same group in 2019.

Other key findings from the sample members included:

- March 2020 was the peak switching month, with seven times the 2019 average monthly volume

- On 22 March 2020 there were 6,156 switches – the equivalent of around 20 days’ worth of switches in 2019

- 70.5% of switches were to lower risk funds, 11% to equivalent risk funds and 18.5% to higher risk funds

- Members aged 26 to 35 constituted 23% of all sample members, yet made 30.8% of all lower risk fund switches

- Banks saw a disproportionate increase in switching compared to other KiwiSaver providers

The report acknowledges all participating KiwiSaver providers increased their investor communications during the COVID-19 market volatility, "however there remain important considerations for KiwiSaver managers to help members make informed decisions in future market turbulence".

The FMA said it commissioned the research to "understand the extent of and reasons for fund switching behaviour during the high level of market volatility, through a behavioural science lens".

Boyes said the report had focused predominantly on the behaviour of younger KiwiSavers because this is where the most switching occurred.

“Using behavioural science, we can observe a bias among younger people to take action when they see their balances drop. Younger people with a bank KiwiSaver provider often see their balance alongside day-to-day accounts. The research found this may be influencing younger people to see their KiwiSaver as both accessible and transactional like a bank account. This was supported with a small number of case studies we interviewed – all three said they switched funds after seeing their balance drop and they found the process straightforward,” Boyes said.

“Action bias means people felt the need to ‘do something’ to gain a sense of control over their falling balance," she said.

"Other factors provoking this activity were emotionally-charged public conversations about KiwiSaver at the time, a herd mentality, and a desire to mitigate short-term losses.

"A panic decision to switch because of shorter term events can have long term consequences."

The report contains a number of future considerations for providers, including highlighting the risks of switching funds, improving the measurement of investor communication effectiveness, utilising prompts to have members pause before completing a switch, and following up with anyone who switched to ensure they were comfortable with their decision and the consequences for the long-term.

The FMA says it will discuss the findings and implications with providers to explore potential improvements.

12 Comments

Makes sense. While some might see this past year's share market rally as a sign of return to normality, there are plenty who see it as a sign of insanity.

In reality they got spooked, not making long term crystal ball decisions.

My wifes Kiwisaver has gone up $50K in a year. That's spooky in itself. You know it ain't real.

She's cool, not switching.

We are far from out of the woods; after one of the biggest economic shocks in history on the back of the 2008 great financial crises that's been propped up by tax payer stimulus can not last indefinitely; Central Bank debasing/destroying monetary policy is almost backed into a corner with little option other than real economic fundamentals inevitably returning to sustainable levels.

Not the tax payer, but the printing press.

I changed from Growth to Cash AFTER the biggest fall, switched back to Growth in June '20 and have 38% gain since then. 15% gain from pre-Covid. I'm happy. It would be silly to have stayed in Cash fund, however some people that are more risk averse may have. I have pity over them as they have not reaped the gains myself and others have experienced.

Have it ever come across the minds of the super fund managers, from this event, that younger investors simply do not trust them to manage their money? Given a choice the same people who rather be their own super fund manager than to choose from a government dictated list.

I think there's a few things here:

1. You can bet the likes of the FMA promoted the rights of kiwisaver members having more information about their funds. This in turn has allowed them to check it everyday which we know is not somethihg you should do with longterm savings.

2. If your funds are with Simplicitiy or another index follower you know they're not going to be doing anything to reduce the drop because the can't - they follow the index down as well as up. Moving to another kiwisaver takes time so swapping funds with a current kiwisaver is members' likley only option if they don't like what they see. So this will get worse as the FMA drives more members into low cost index funds (40% of how the kiwisavers were rated when selecting the new defaults was on fees, which in turn drives index huggers).

3. Cindy and her pals are making it harder and more expensive to be a financial adviser so the same kiwisaver members are less likely to seek advice. So none of this should really be a surpirse

Stay the course

Dear Government, please put financial literacy on the national curriculum.

If you have a long term investment horizon - say 15 years at least - then shares are the ones that will be the most rewarding. Dollar cost averaging has done wonders to my overall investment performance in the last 25 years. My only regret is that I have always been a conservative investor, allocating only a relatively minor portion of my investments into shares.

Never sell when many are panicking - this is the time to seriously consider buying a little more than usual.

The big question mark for the next couple of years is the nature of the inflation now showing its first signs, and how high the main central banks will be forced to set interest rates in the near future. Rates-sensitive stocks may suffer, at least in the short term, but the potential of stocks for protection against unexpected inflation should also be considered. Interesting times ahead.

The turn of events seems not startling at all. I hope that new business owners will find it more beneficial.

jack,

@electrical works team

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.