Here's our summary of key events overnight that affect New Zealand, with news apprehension is building in markets and economies.

Firstly, we should report that leaders are gathering in Japan for the G20 meetings. But there is only one meeting that has any real attention - between the Chinese and US Presidents - and that is expected to happen on Friday or Saturday.

Concern there has prompted markets to go risk-off. The S&P500 is down -0.8% today. Yesterday, Shanghai dropped -0.9%. (The NZX50's +0.3% rise was one of the few anywhere in the world.)

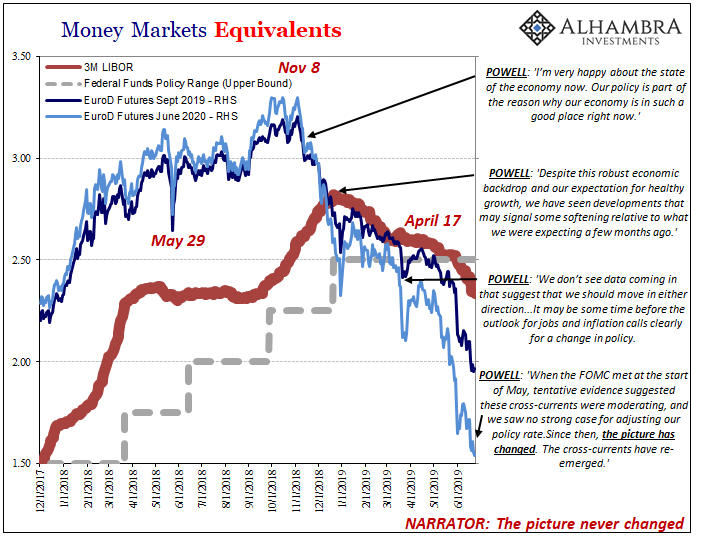

Meanwhile the US Fed boss Jay Powell repeated today that his central bank sees 'crosscurrents' in the US economy that signal weakness that may need to be responded to. These weaknesses come from "uncertainty" driven by US trade policies, a dig at his recent critic, the US President. He also pushed back by defending the Fed's policy making independence because it can prevent "damage that often arises when policy bends to short-term political interests".

Another Fed district reported on the health of its factories and this one came with a conclusion that things are little-changed. But a read of the detail shows a softening underbelly of recent data.

New home sales in the US fell sharply in May and are almost -4% lower than for the same month in 2018.

American consumer confidence dropped in June to its lowest since September 2017 as their households grew a bit more pessimistic about economic and labour market conditions. The surveyors reported the key concerns are the escalation in trade tensions between the United States and China.

And the US federal debt is on a path to reach its highest levels since World War II. Falling tax revenue and increased spending are set to worsen the US federal deficits significantly, according to a report released overnight by the Congressional Budget Office. In 2019, the debt held by the public amounted to 78% of GDP, compared to just 35% in 2007. That number is set to increase to over 90% in the next ten years, and nearly 150% in thirty years. (For comparison, the New Zealand net government debt is under 20%.)

In China, local authorities there are being urged to issue new debt and they are responding with some large offerings. June issuance is expected to be a record high, exceeding NZ$85 bln. That would take the total for the first six months of 2019 over NZ$400 bln. The goal is "to stabilize economic growth and market expectations".

In Australia, it is now becoming clear just how lucrative the Hayne Inquiry was for lawyers and consultants. Deloitte has just reported Australian revenues of AU$2.3 bln, up +13% in a year. Next year's gravy may not be as thick however.

The UST 10yr yield is falling today and now at 1.99% and weaker by -3 bps. Their 2-10 curve is now at +27 bps an their negative 1-5 curve is wider at -20 bps. The Aussie Govt 10yr is at 1.28% and a -2 bps fall from yesterday. The China Govt 10yr is unchanged at 3.27%, while the NZ Govt 10 yr is down -1 bp to 1.55%.

Gold is up again, up another +US$9 to US$1,424/oz.

US oil prices are little-changed today. Prices are now just over US$58/bbl. The Brent benchmark is now at US$65.

The Kiwi dollar is still rising and across the board, and is now at 66.5 USc. On the cross rates we are also firm at 95.5 AUc. Against the euro we are up at 58.5 euro cents. That all pushes the TWI-5 up to just over 71.

Bitcoin is up as well, now at US$11,378 and a +3% gain since this time yesterday. The bitcoin rate is charted in the exchange rate set below.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

9 Comments

"It Would Be An Earthquake" - Three Chinese Banks Tumble After US Threatens To Cut Them Off From SWIFT

https://www.zerohedge.com/news/2019-06-25/chinese-banks-tumble-after-us…

Google has your back

https://www.zerohedge.com/news/2019-06-25/msm-silent-after-google-elect…

The Sneaking Suspicion the RBNZ Could Spring a Surprise Rate Cut

Under governor Adrian Orr, New Zealand’s central bank has shown it’s not afraid of springing a surprise. That’s why some economists and traders have a sneaking suspicion it could cut interest rates tomorrow.

Yes, he could and he could also continue to cut the OCR in half forever.

The stronger NZD could trigger Orr to cut tomorrow but it would be a surprise indeed

In Canada,wholesale retailing increased for the fifth consecutive month.The 1.8 percent rise was slightly above economists expectations of a 0.2 percent rise. Although a secondary data point,another signal that their Central Bank has no urgency to cut rates. Will the RBNZ and RBA diverge in the coming week,pushing the kiwi towards parity?

I hope so, ready to change $$.

Given recent question marks around banking culture here’s an interesting panel of guests at the monetary institute. Featuring Professor Werner amongst guests.

https://youtu.be/_RWXrQqENvg?list=PLqUdGWk835zPiNJbd9svNFy3iE4eBjE1l

China now appears set to turn back all Canadian meat products currently en route, according to sources , not named for usual reasons. Usual reasons re vet inspections. I wonder what they want.

Certainly not diplomatic ties:

China Removes Its Ambassador From Canada, Decides Canucks Are Too Nuts Under Technocrat Trudeau Regime

Meanwhile the US Fed boss Jay Powell repeated today that his central bank sees 'crosscurrents' in the US economy that signal weakness that may need to be responded to.

The Fed will belatedly follow market yields down - Link

{kind=link}

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.