Subscribe to our daily podcast here.

Here's our summary of key events overnight that affect New Zealand, with news of a sharp fall in American consumer credit demand.

But first, yesterday, New Zealand was the centre of interest rate news with its surprise -½% rate cut. But two other central banks also cut rates yesterday as well; India cut theirs from 5.75% to 5.40%, and Thailand's moved down -0.25% to 1.50%. The Indian move was regarded by markets as timid. The Thai move was more of a surprise but taken in the trade and currency war context because they were worried about the 'strength' of the Thai bhat.

The latest data on world trade is not encouraging.

In the US, orders for new trucks, which were running at record high level since 2018, are now reversing fast. Orders for big-rigs fell in July to their lowest level since 2010 as freight-market demand scales back quickly.

International airfreight demand is falling and the pace of the drop is picking up. The latest data for July shows it is down more than -5% from the same month a year ago, the eighth straight month of declines. In the Asia/Pacific region, this data is almost -6% lower. In North America it is down -7%.

Wall Street is -0.5% weaker today, although overnight European and Asian markets pretty much marked time. The US Administration's attacks on the Fed is being seen as cheap blame-shifting and not dealing with key economic issues they need to address. Bond investors are increasingly concerned and the closely-watched 3m-10yr yield curve is now more negative at -35 bps.

Markets are also getting to understand that the Chinese ability to depreciate their currency is a force the US can't counter. Worse, they now understand that even if the Chinese leave their currency to market forces, as the US insists, the yuan might weaken even faster. Its an own goal by Washington, and it is a tension that will be around for a long time. Markets sense that Trump's trade policy has failed and the consequences for the US won't be positive.

Not only is international trade turning lower, but US consumer credit demand is as well. Their June data has come in unexpectedly weak and a US$1 trillion lower than markets were expecting.

For months we have been reporting the rise and rise of the iron ore price. But overnight it has suddenly turned, and sharply. It is down more than -5% in one day.

In Australia, Chinese Government proxies are getting even more aggressive on campus, using undercover tactics to stifle protest.

And in a sign of the times, insurer Suncorp (Vero and AAInsurance in New Zealand) has raised its provisioning for weather-related events. Climate change costs will first be felt by households in their insurance premiums.

The UST 10yr yield is sharply lower yet again, now at 1.69%, building on the earlier weakness. Their 2-10 curve is flatter at under +10 bps while their negative 1-5 curve is wider at -28 bps. Their 3m-10yr curve is now over a negative -30 bps. The Aussie Govt 10yr is down -9 bps to just 0.94%. The China Govt 10yr is also little-changed and holding at 3.07%, as is the NZ Govt 10 yr which is now at 1.19%, a dive of -14 bps over the last 24 hours.

Gold is now up over US$1,500, in fact up +US$30 today to US$1,502. That is the highest it has been since April 2013 - and in New Zealand dollars it is an all-time new record high of NZ$2,327/oz.

US oil prices are taking another thrashing today on demand fears and are down almost -US$2.50/bbl. They are now just under US$51.50/bbl. The Brent benchmark is now under US$56.50. Both are huge moves overnight and add to recent weakness.

The Kiwi dollar starts today softer at 64.6 USc, more than a -½c drop since this time yesterday. On the cross rates we are down a whole -1c at 95.5 AUc. Against the euro we are similarly softer at 57.6 euro cents. That sets the TWI-5 down to 69.7.

Bitcoin is now at US$11,743 and virtually unchanged from this time yesterday. The bitcoin rate is charted in the exchange rate set below.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

Daily swap rates

Select chart tabs

39 Comments

Panic mode approaching as market crash season approaches

"if the Chinese leave their currency to market forces, as the US insists, the yuan might weaken even faster."

Quite so.

But let's recognise that they yuan should have had a much stronger base to launch off. It's been the decades of inaction by all and sundry that allowed China to make its currency artificially weak that caused the current US Administration to act. A decade or more of massive trade surpluses by China should have seen it's currency float to a much stronger level than it currently is.

Whose fault is all of this? Not Donald Trump's! He just inherited the problem and is setting about rectifying it in a way his several predecessors didn't.

Good points, one tires of the somewhat cheap anti-Trump rhetoric

Yes, but the Trump ideas are based on nineteenth century thinking. Trade flows are no longer the driver, capital flows are. Until the US figures out how to throttle capital flows they will just keep pissing in the wind. NZ thinking is similar, although the RBA's and RBNZ's credit throttling is a fumbling attempt in the right direction.

Washington Should Tax Capital Inflows

https://carnegieendowment.org/chinafinancialmarkets/79641?utm_source=rs…

Dp

The anti-Trump rhetoric is not overwhelmingly fuelled by his stance on China though is it? Rather his scapegoating towards minorities, attitudes towards woman, nepotistic appointment of family members who are completely unqualified for their roles, generally undiginified and unstatesmanly behaviour (including tweeting some of the biggest clangers in the history of politics), inciting violence and hate, tax evasion, lying, more lying and general demagoguery.

His stance on China really is the very least of it

I don't like Trump. But people often descend into dissing everything he does, because they don't like him. That's not particularly fair or objective. It's also petty.

We don't know what's going on behind the scenes. For all we know the US might have made exhaustive efforts to resolve this in other ways.

"Impeach Trump! They should Impeach Trump!".

"Why?"

"Uh, um, well he's a womanizer and a jerk".

The parallels between Billy Clinton and Gingers view of Trump quite striking. Though I don't recall 24/7 Billy Clinton derangement syndrome from the legacy media. Similar parallels with JLR and Labour's sex scandals.

Meh, just grab them by the P@#%#.

I resent and take offence to your comment ;)

Good to have you back Ginja

^ this.

There's a dozen or so commentators on Interest (yourself included Yvil) whose commentary and insight I value and in some cases skip most of the article body to get to. The positions often disagree but it's that earnest, respectful debate that makes it especially rich. So thank you.

At the other end of the scale we have Jacinda, she is a woman and she is always so shiny, did you know she made a baby, she's much better at her job than that gross Trump fellow. (Sarc off).

People are pretty wrapped up in interest rate cuts. For me the interest rates matter less and less each cut. So many people are taking about breaking to get lower rates. The difference between 3.99% and 3.75% isn't a lot, at least wait a few weeks. If you want to refix a lot just split your mortgage so you have portions come up for refixing on a regular basis.

I'm expecting low interest rates to last for a long time unless we hit a currency problem. There are a lot of risks with the trade and currency war. US is in a position where there is only a lose-lose outcome no matter what.

Now to sit back and watch mortgage defaults increase.

No matter how it is framed: you don't want debt during deflation.

As it increases in value, dragging down your (negative) net worth.

In Australia, Chinese Government proxies are getting even more aggressive on campus, using undercover tactics to stifle protest.

Could they be just overseas students that don't want to be identified? Calling them "Chinese Government proxies" implies they are in the pay of the CCP which we really have no idea about at this stage. It's interesting language to use and perilously close to fake news you know.

Getting sick of your fake news comments Z, you are starting to sound like Trump. Sounds like proxies to me - we have them imbedded here in NZ.

Proxies are usually unrelated to the hostile force. Like the US using Kurds to fight Syria or Iran using Hezbollah to fight Israel on their behalf. In this case they are probably just mainland students not wishing to be kicked out of Uni. Seems the simpler and less dramatic explanation.

Dear Comrade Smith.........

Plus 10 points to your social credit score Dr Smith.

You seem to need a lot of convincing that the CCP is up to no good. I spent a couple of years in China and my spidey senses tell me that these sort of stories are correct. You have a population that has been brainwashed since birth, that China is going to take its rightful place in the world as the middle kingdom, (centre of the world) most powerful country and leader of a world under the CCP. Anybody that stands in the way will be dealt to.

Probably but we expect reputed journalists to use a little more than "spidey senses" don't we?

We don't know the source of this story, why assume it is "fake news"?

I think you are coming at this from the wrong angle. Start with the fact that in the recent past the CCP has been responsible for the deaths of many millions of their own people. That they currently imprison a million minority Uyghurs and have set up a massive surveillance state to control the population and preserve power at all costs. Why do you think they wouldn't do this?

Hi Zachary Smith,

As you and everyone here can see, the mindset, vision, and views of the world are totally different between people who are only exposed to the western media and people like us who open eyes to observe both eastern and western world.

I do have hopes that the new generation NZers have much wider mindsets than the older generations.

Interesting times. It’s odd how one of the biggest benefactors of neo-liberal economics has been a communist state. The bigger picture here is whether globalisation will survive.

It won't, simple answer.

The system grew to accommodate growth, and became incapable of accommodating - or even discussing, obviously - any other possibility. But there are always limits to exponential growth, and it was always going to be between 2000 and 2050 that the peak occurred.

For those with anntennae, Robertson on Morning Report (they allowed Goldsmith to put growth and sustainable in the one sentence, unchallenged, which tells us how far off the pace MR are) said "we are entering a low-growth era". The use of era is telling.

..."we are entering a low-growth era". The use of era is telling.

Illuminati confirmed.

He definitely wasn't simply referring to cyclical growth rates, was he.

^^bingo

And yes it will survive if history is anything to go by, global trade goes through phases of flux. I think we are looking at a period of retraction from globalism for the time being. But it will return again eventually, it always does.

For instance, accordingly to Simon Jenkins (historian) the UK has joined Europe 8 times and left Europe 9 times since the Roman Empire (including the current Brexit and acknowledging that what we refer to as the UK and Europe are modern notions for ancient land masses).

Roger has highlighted a major issue with globalisation at this juncture - capital flows. Where in times prior to globalisation of ownership and pushing of profits to tax havens, companies were better participants in the societies they were located in, they now appear highly disconnected from the societies they purport to be part of. They benefit from the good things the society provides them (legal systems, infrastructure, an educated workforce) but now put their money elsewhere while global owners take that benefit. Not to say they don't benefit the societies at all, but it seems out of kilter at the moment.

Nationalism seems to be a first response, but I agree with Roger's suggestion that the issue of capital flows needs to be confronted.

It's not something I've ever studied but I seem to remember that being a company or being able to trade was a privilege bestowed by ruling monarchs with the understanding that it must benefit society (and of course the rulers who bestow it) and this privilege could be much more easily rescinded . Today seems a one way street.

I think there is a tendency to romanticism in general.

Companies and/or aristocracy have never historically operated solely for the good of citizens. The rich have pretty much always exploited the poor and disenfranchised throughout history, excluding usually very brief periods of uncharacteristic reprieve. There are so many examples or corn laws, poor laws, workhouse laws and back and forth flux between the land owning and non-land owning for rights.

During history, there have been several very notable eras of globalism. Mainly during era's of empire but taxes, inflation/deflation and interest rates have also, always been part of that picture too.

Global corporations are essentially just mini empire builders. They will continue to exploit and profit to the extent that they can, the same as every empire ever did. The East India Company behaved in exactly the same way, to name but one example.

Roger has highlighted a major issue with globalisation at this juncture - capital flows.

A better understanding of off balance sheet FX derivatives is called for :

What would balance sheets look like if the borrowing through FX swaps and forwards were recorded on-balance sheet, as the functionally equivalent repo debt is? We combine various data sources to estimate the size, distribution and use of this "missing" debt and to begin to assess its implications for financial stability. A key finding is that non-banks outside the United States owe large sums of dollars off-balance sheet through these instruments. The total is of a size similar to, and probably exceeding, the $10.7 trillion of on-balance sheet dollar debt. Even when this debt is used to hedge FX risk, it can still involve significant maturity mismatches.1

The outstanding amounts of FX swaps/forwards and currency swaps stood at $58 trillion at end-December 2016 (Graph 1, left-hand panel). For perspective, this figure approaches that of world GDP ($75 trillion), exceeds that of global portfolio stocks ($44 trillion) or international bank claims ($32 trillion), and is almost triple the value of global trade ($21 trillion).

The outstanding amount has quadrupled since the early 2000s but has grown unevenly (Graph 1, left-hand panel). After tripling in the five years to 2007, it fell back sharply during the GFC, even more than international bank credit. This most likely reflected a reduction in hedging needs, as both trade and asset prices collapsed. Link

The RBNZ:

The Committee noted that additional stimulus from central banks had underpinned growth and reduced the likelihood of a more-pronounced slowdown. However, some thought that even with support from monetary stimulus, considerable economic and policy uncertainty could see global growth continue to decline. Other members noted that the easing in global financial conditions since the beginning of the year, or a shift in political environment, could lead to a pick-up in global growth over the next year.

C'mon get real - the OCR has nearly been cut in half twice from 3.5% since April 2015 and growth "could" recover. Do us all a favour and rethink this failed moneyless monetary policy.

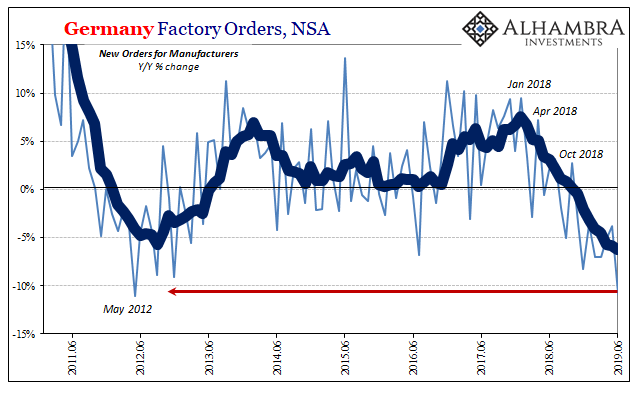

Germany is deep into negative interest rate "stimulus" and factory orders are collapsing.

{kind=link}

Our own NZ 10 year government debt yield collapsed further yesterday, confirming an extension of the dismal economic outlook without coherent solutions.

David , I think the Americans may have used a little less consumer credit in June ?

Markets are also getting to understand that the Chinese ability to depreciate their currency is a force the US can't counter.

It is more than likely the PBOC is extremely short eurodollars via off- balance sheet derivatives which habitually mature and cause ructions in the spot FX market.

Please consider the comment I posted yesterday and this older article explaining the ramifications

interesting, I have a few acquaintances or friends who in the last 2-3 months have moved out of financial service or development related roles in smaller businesses in to far more conservative (less risk exposed) roles in larger organisations, sometimes in different industries. Anecdote, I know....but

Funny how the US Fed said their recent cut was a "mid-cycle" cut. If all the news and data lately isn't screaming late-cycle, I'll eat my amassed gold ETFs.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.