Here's our summary of key economic events over the long holiday weekend that affect New Zealand with news Janet Yellen is calling for a global minimum tax on multinationals.

But first up today, the IMF has released a series of global economic reports, the heart of which show rising economic growth rates especially in the first world, but problems for the developing world and rising inequality. The improving American economy is drawing billions of dollars in capital from emerging markets, stirring concerns that investor flight may destabilise these countries where pandemic infections remain high and the prospect of an economic recovery seems distant. Not helping are awful local public policy positions in places like Turkey and Brazil.

The IMF is also warning about the rising nonfinancial sector leverage, which they see as a real risk to be addressed and entirely a consequence of loose monetary policies and vast pandemic stimulus. And it is pointing out the global risks from commercial real estate in the post-pandemic environment.

In China, there was a not-so-flash private sector Caixin PMI report. Like its official version, this one reports a cooling in their expansion of activity in private factories and the heat has well and truly gone out of their sharp recovery. It was the slowest 'expansion' in almost a year.

But price rises, some quite sharp, are becoming more common. For example, corn prices have risen almost +50% in a year, and there are moves to substitute it wheat and rice in animal feed. That may have future food security issues for China.

In South Korean factories remain in a solid expansion mode. Factories in Taiwan are expanding even faster.

In the US, the March non-farm payrolls report was a good, positive one, led by an accelerating pace of vaccinations and the anticipation of more stimulus. Employers added +916,000 jobs in March, up from +416,000 in February and the most since August 2020. The leisure and hospitality sector led the way, adding +280,000 jobs as Americans returned to restaurants and resorts in greater numbers. However, these gain left the pandemic deficit at an -8.4 mln jobs lost since February 2020, so they have a long way to go. Analysts say that future gains will grow from here, with the April data likely to be even better because the March data was collected before most states opened up, and before the latest stimulus payments actually arrived.

One feature we should watch; as more lower-paid jobs open up in their workforce, the strong growth in average weekly earnings is moderating, but it is still higher by +4.2% pa, just not as high as the prior +5.2% pa.

The number of initial claims for unemployment benefits actually rose marginally last week, although to be fair, the prior week's numbers were revised lower. That means the total number of these benefits is now 4.1 mln, and a level lower than a week ago.

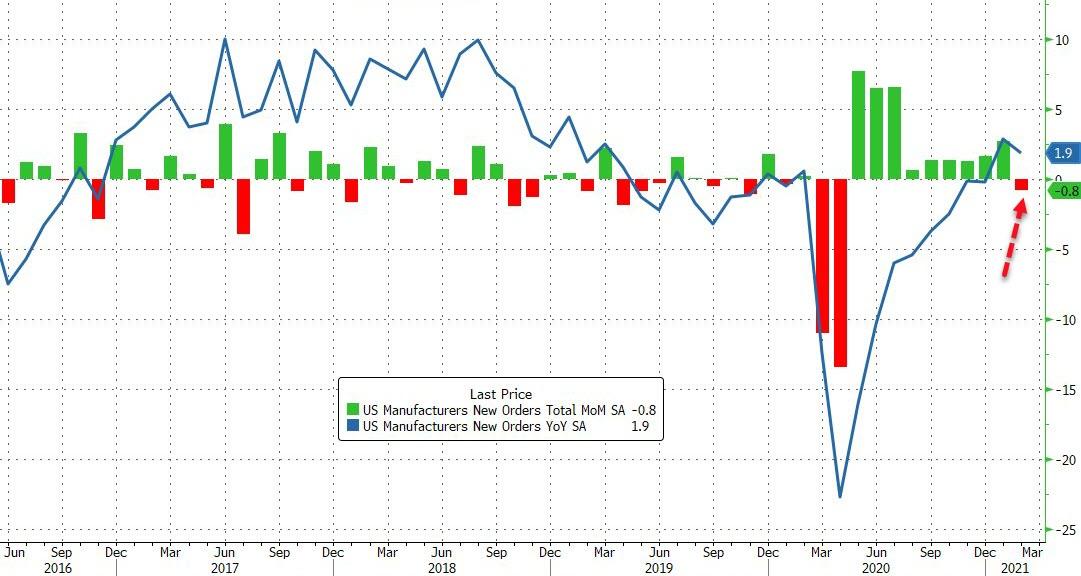

The labour market improvements are also reflected in the state of American factories. They are running at the best levels in 14 years and since before the GFC. The March results were affected by well-publicised supply-channel problems, but new order levels are high, and hiring is rising. The previously noted sharp rises in costs and prices is also a feature of these reports. The locally-watched ISM PMI reported strong conditions in the face of pandemic difficulties. The internationally benchmarked Markit PMI was equally positive, as was their services sector expansion.

American vehicle sales rose sharply in March to a rate of 17.7 mln per year, up from 15.5 mln per year in February. Still, this leaves the American car markets still well into second place behind China.

Canadian building permits rose unexpectedly strongly, in this case in February from January, with notable rises in non-residential construction permits. Building permit levels for residential construction were lower in February than January, but year-on-year they are up a very notable +25%.

In Chicago, Treasury Secretary Janet Yellen has called for a global corporate minimum tax on multinationals.

In Washington, a key consumer protection regulator is proposing some rule changes to "prevent avoidable foreclosures" as the emergency pandemic measure expire. Essentially, they are extending the time borrowers have to work through repayment stress issues.

In Europe, their factory sector is rising as well. Record increases in output, new orders, exports and purchasing activity were recorded, while unprecedented supply-chain delays drove their sharpest rise in input costs for a decade.

In Australia, their factories are expanding faster too.

While a top producer in the minerals world says it expected the iron ore price to fall -50% in 2021, in fact it is holding high, and there are reports of more supply disruptions and the immediate risk of for even higher prices. Inflation isn't getting any respite from core commodities. Further, in a few days, we will get the latest update on global food prices, and almost certainly they have risen in March.

On Wall Street, the S&P500 is up a strong +1.3% in early afternoon trade. European markets were closed overnight for Easter. Yesterday, the Shanghai and Hong Kong exchanges were closed for local holidays, but Tokyo was open and it rose +0.8%. Obviously, the ASX and NZX were closed yesterday.

The latest global compilation of COVID-19 data is here. The global tally is still rising, now 131,548,000 have been infected at some point, up +1,638,000 in two days. Global deaths reported now exceed 2,856,000 and +18,000 in two days. Vaccinations in the world are still rising fast, now up to 653 mln and in the US almost 45% of their population (163.6 mln and up +11.3 mln in 5 days) have now had this protection as they achieve a very fast rollout. The number of active cases there fell to 6,904,000 and down -38,000 since Saturday.

The UST 10yr yield is up +1 bp at 1.72%. The US 2-10 rate curve has steepened slightly to 154 bps. Their 1-5 curve is flatter at +88 bps, while their 3m-10 year curve is unchanged at +169 bps. The Australian Govt 10 year yield is up +1 bp at 1.77%. The China Govt 10 year yield is unchanged at 3.22%. And the New Zealand Govt 10 year yield is unchanged as well at 1.83%.

The price of gold starts today down -US$4 from Saturday at US$1726/oz.

Oil prices have slumped over the weekend by about -US$2.50 and are now at just under US$58.50/bbl in the US, while the international price is now just over US$62/bbl.

The Kiwi dollar opens today marginally firmer at just on 70.6 USc. Against the Australian dollar we are unchanged at 92.3AUc. Against the euro we are also virtually unchanged at 59.8 euro cents. That means our TWI-5 opens today a little higher at 73.1.

The bitcoin price will start today at US$58,977 and down -0.3% from this time Saturday. Volatility in the past 24 hours has been moderate at +/- 2.1%. The bitcoin rate is charted in the exchange rate set below.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

47 Comments

Is it bad, if house prices fall a little. Absolutely not - anyone can tell, specially when house prices have gone up from 100 to 140. If it was 100 and falls to 90 or 80 may be yes but not when from 100 to 140 and if it falls to 130 or even 120 as still 20% to 30% rise in a year.

Only fall can help calming FOMO or fight for house will continue just like toilet paper.

https://www.newstalkzb.co.nz/on-air/the-weekend-collective/the-oneroof-…

Bubble or boom? Why ultra-low interest rates mean house prices may never bust

In this era of cheap money, what once might have looked like a housing bubble might just be the new normal

“It’s like frogs in boiling water,” says Klassen. “Once mortgages were for 20 years, then 25, now 30. Soon it will be 50. Many people will never pay it back, so owning a home will become like renting – just that it’s renting from the bank.”

Yes I saw this article.

I disagree with its contention.

What happens when a financial crisis strikes? The RBNZ now has limited ammo left.

Sure they can take the OCR negative, but only so far.

Sure they can take the OCR negative, but only so far.

Yes, Curves Have Been Forced To Speak Japanese

Economists’ R*, or R-star, is a fiction. It’s one that they came up with after-the-fact to try to explain why their policies didn’t actually work the way policymakers had initially promised. While in public, officials still speak glowingly of each QE, one after another after another, in private they know it deserves absolutely no praise.

Study after study has shown basically the same thing (this pulled from a 2012 IMF research paper):

Research on the effectiveness of earlier quantitative easing has yielded mixed results, with most pointing to limited effects on economic activity. While most papers found evidence that quantitative easing helped reduce yields, its effect on economic activity and inflation was found to be small. The reasons cited included a dysfunctional banking sector, which impaired the credit channel… [emphasis added]

Helped reduce yields. That’s a very curious way to frame (in order to arrive at “mixed results”) what is its only detectable, possible contribution. In fact, even this much is debatable; ask yourself, what is it that QE is always “helping” lower rates? As I put it last week “celebrating” the undeserving theory’s unholy twentieth anniversary:

In other words, falling rates correlate with QE’s if only because rates are already falling by the time central banks get around to conducting these programs. And if yields are already dropping as things get bad enough to convince central bankers to unleash their psychology, what good are even lower interest rates than the low rates bad things have already brought up?

This is where R* supposedly comes into it. The modern central banker’s only job is to figure out a way to influence behavior; but you can’t put “behavior” into an econometric model. Thus, an imputed “natural rate” seems a plausible enough stand-in to the detached statistician with no real feel for actual economics (small “e”). To achieve success, in the regression analysis, the Fed or ECB need only drive rates below computed R* – even if the market itself is already pushing them lower.

If it seems a bit too wishy washy if not completely contradictory for what monetary policy projects for itself, that’s because it is complete nonsense. Here’s what I wrote just before the onset of Inflation Hysteria #1, back in March 2017 right at the beginning of what would shortly become that whole globally synchronized growth debacle:

R* is just the plugline or balancing factor that attempts to make sense of why neither ultra-low interest rates after the dot-com recession nor QE in the aftermath of the Great “Recession” failed to work as they “should” have. For policymakers, policy rates went low and lower but since no great recovery resulted, especially from the QE’s, it is merely asserted that R* must have been that much lower still…If “real” policy rates had been pushed down to -10%, the still lack of recovery would have left Fed officials claiming R* surely was -10.01%.

This is exactly what curves had been saying all along; not only was QE failing time and again, each time it did the market adjusted to each failure!

We are certainly victims of industrial grade financialisation. China got the jobs, we got the debt and all else that emits from the FIRE sectors.

"China Got the Jobs, we got the debt and all else that emits from the FIRE sector" True enough, but the last US Administration set out to do something about that-and did. Tarriffs gave the US Manufacturers the signal they needed to get back on their horses and expand and thus David reports today "The labour market improvements are also reflected in the state of American factories. They are running at the best levels in 14 years and since before the GFC."

What about NZ?

Difference is emphasis on Manufacturing between US & NZ are importance to the overall economy of their respective countries. In US it is the largest sector of the economy-$6 Trillion a Year. In NZ only $24 Billion. 10% versus over 30% of their respective economies.

If ultra low interest rates mean house prices may never bust - Is it not more the reason to stop Interest only loan to somewhat try and controll the speculative demand.

Low interest rate and interest only loan are perfect recipe for housing ponzi and surprisingly this Jacinda Arden government and Mr Orr are still thinking about it - Why are they playing with time ?

Evident but still resistant from Jacinda Arden and Orr is a mystery and surprising no main street media raising it.

If anyone has genuine argument in favour of interest only loan which supports speculators, please highlight other views in comment below to try and solve the mystery, if it is for reason other than vested biased interest which many are missing and only Jacinda Arden and Mr Orr knows.

Media should raise with JA and Orr, for them to respond and am sure they will come up with some redicluse excuse / theory which should expose their intent. For if they would have been serious, would not have been silent.

I think you find that behind the scenes the Aussie banks are spitting tacks...like the drunks at a party who want the dj to keep playing and the bar opened again

They will be threatening everything under the sun including sending the country broke

The RBNZ will want to have their ducks lined up in a row and a sound case

My observation of the media and lobbying is that interest deductibility on new builds was not decided until further consultation but Grant Robertson was weak and said this would still be allowed

But he knows interest only loans will be going and that will the nail in the coffin for so many speculators

Hi Stuart, am sure like you and me, many others will like to have answered why Interest Only Loan should not be stopped that is mostly used by Speculators to fund their activities.

Would be interesting if an expert - David Chaston can shed some light on it.

Sounds to me like a the call of a "permanently high plateau"of the sharemarket .... at the end of the roaring 20's. Or the "great moderation" where we had "solved" recessions ... in the late 2000's.

This idea that debt can solve all problems seems to be a mistake we are destined to repeat over and over.

Basically something being cheaper is a good thing. As something being cheaper means it is more affordable. If I go & buy a car & the car I want costs me $30,000 instead of $40,000 this is a good thing as more money goes further. The same rule applies to housing despite a popular misconception amongst older New-Zealander's that this isn't the case.

Haha. I think the fact you actually need to explain that means the cause is probably lost .

Debt is great

It was a gorgeous day here in Hawkes Bay on Easter Sunday, with the weather station nudging 30 degrees, so we invited some friends over for a bbq. As the event drew near we discovered we were short on a few items so I chanced my arm by doing a drive-by of the four closest supermarkets (public notice: sometimes Google is wrong). None were open. Oh well, no onions on the bangers tonight.

I drove a different way home (hey, sunshine!) and found just one business hard at work...a real estate agent running a very, very busy open home.

Solid priorities, NZ.

Just another article, writing what most of us know - what many choose to ignore. But one day, things will change.

"Changing the course of .... Housing Misery"

New Zealanders don't want an economy built on the misery of others. Especially when it's our childrens’, friends’, siblings' misery, Anyone who blithely argues for this economy of misery to continue is valuing the wrong things, truly... our current economy is reliant on money continuing to be extracted from housing in the way people currently do. Which is exactly why we need to change the situation.

Watching for decades people in power drive the economy further towards private unprofessional housing investment that harms people, while waiting for ‘the market’ to sort it out, does tend to limit people’s belief in things changing, including policy makers themselves. Yet things can be changed. This week people in Labour showed us a little glimpse of what shifting advantages away from problematic investments can look like.

https://www.newsroom.co.nz/changing-the-course-of-the-ship-of-housing-m…

That's a great article, very powerful how she uses 'Housing Misery' as her slogan, rather than the usual dry stuff.

The crisis deserves some sloganeering.

Yay today, bubble, bubble (toil and trouble for some?) Appears that any decision to go ahead with Australia has arisen from political pressure rather than from confidence in NZ’s ability to cope with infections appearing in the community. Probably catalysed mostly by PM Morrison debunking of our PM’s accusation that Australia was the blocker? There is undoubtedly real concern about outbreaks especially as the Australian vaccination program is lagging behind projections. Oh but then again NZ itself is still short of even 1% of population. Perhaps that too is another unannounced reason for all the hesitancy?

I don't know about that. The traditional pattern is that far more Kiwis fly to Australia to escape winter, than Australians come here to ski. The net effect will probably be a loss for NZ. We would have been better off not taking any covid risks with Australia's less secure virus management system and wait until summer when we have all been vaccinated and the balance of the tourist trade with them reverses. I would not mind betting that it was a case of once again bullying big brother Australia got grumpy and pathetic little NZ caved.

I read that normally there is a small net positive in the reciprocal travel to NZ, about $600 million in our favour.

With so many NZers residing over there I think it would be good to get it going, I dread the situation if my elderly MIL takes a turn for the worse with children and grandchildren in Australia.

$600 M - It is seasonal. In fairness however, as Australians cannot go to the rest of the world there could be a one off net gain to us. But is the risk worth it? What would a month long lock down cost us?

But is also give the airline industry some work not to mention duty free shops

Remember only economy in NZ = Housing Economy.

US Real manufacturing - factory orders - are tumbling... source Bloomberg

{kind=link}

Supply of Housing will never catch up. Can't be done as long as we continue to allow the outrageous population influx of recent years.

Someone really needs to ask the government what the planned migration levels will look like post-Covid. I can't believe we're having housing reform talk without this vital piece of information.

Or talk on climate change.

I would say immigration levels are central to 3 of the biggest issues we face:

- Housing

- Climate change

- Infrastructure

Talk on climate change, is talk, nothing much more. Case in point the Labour Government seconded by the Christchurch City Council declared, quite profoundly, a “climate emergency.” Both parties are then part owners of a project to place a wide bodied jet airport in the middle of beautiful natural landscape in Central Otago. Infrastructure 1 vs climate change nil. Yes they talk. Go figure!

Nope.

1. Population

2. Resources remaining

3. the Entropy trend.

That covers yours, en-route. :)

Here's today's challenge.

Log in to your bank account and determine how many of your dollars are actually real money and how many have been instantly conjured up on a banks keyboard and lent by them to someone else to buy a house.

Answers on a promissory note to Adrian Orr and Grant Robson.

Alchemy

Why do we allow our private banking sector to issue Bank paper or bank credit masquerading as legitimate New Zealand government currency?

To enrich the few at the expense of the many. duh.

"The improving American economy is drawing billions of dollars in capital from emerging markets,"

No David, it isn't 'improving', it's 'accelerating the draw-down of resources from a finite stock, for the gratification of one small echelon in one small period of time. And it's not 'capital' - it's a forward bet on resources and energy being future-available - which make the oil-price drop somewhat at odds with the claims.....

What is the alternative... govts supporting their peoples through handouts?

The worldwide post pandemic upswing is on the way... this is the roaring twenties!!

Post pandemic? NZ & Aussie havn't even crossed the start line yet.

Are you extremely short-sighted ... better go to specsavers

The moisture map has greened up.... keeps the grass and plants growing and sucking carbon from the ATMOS-FEAR

Slow clap

You know it's the one on the right for current conditions eh? Now compare to the one on the left (long term average). What does that tell you?

Huge Lolz

Pattern now established in economies post CV19: 6-9 month "recovery" due to extra spending by fiscal and monetary inputs, followed by flattening of growth thereafter. China now in decline phase as they were first out of Cv19. NZ ditto. EU still in mire and never had proper lift out. UK about to get its lift but Brexit costs messed it up for first quarter. USA about to get lift off and is sucking EM flows of money out into its maw. 3rd or 4th wave of CV19 evidently infection wise impacting India and Brazil primarily and deaths not caught up with infection acceleration, with world infection now above January peak but deaths near 50% only. EU recovery probably now postponed again for 6 months. Stock markets likely have another 6-8 months before they feel reality check and start falling.

You refer to 'phase'... the correct terminology is cycle as in 'growth-cycle'. Watch this carefully ;)) ... buy a bargain basement property in uk quick before it is too late

You are confusing a washing machine with a quarter-mile dragster.

I wonder what government is actually doing to monitor house prices, just sitting around like dodo birds until April results come out and someone shakes them awake? Also does anyone really know how much property is still being purchased by kiwi residents through a company with overseas shareholders, such as Apex One Limited, how much Chinese money is buying up NZ land plots to build high density housing

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.