This article is a re-post of a report received from Fitch Solutions. The original is here.

Key View

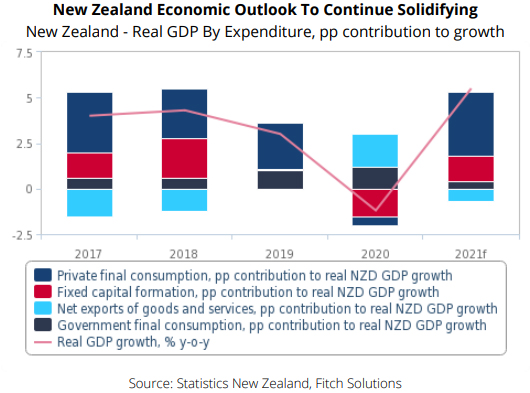

- We at Fitch Solutions have revised up our forecast for New Zealand’s economy to grow by 5.5% in 2021, from 3.6% previously.

- The upward revision reflects the better than anticipated GDP results for Q121 which showed that the economy grew 3.6% y-o-y on the back of strong domestic demand

- We expect private consumption and gross fixed capital formation to lead the economic recovery over the coming months as New Zealand’s recovery continues to firm.

We at Fitch Solutions have revised up New Zealand’s growth forecast for 2021 from 3.6% to 5.5% following a better-than-anticipated Q121 growth outturn of 3.6% y-o-y and 1.4% q-o-q. This marked an acceleration from 1.1% y-o-y and -1.5% q-o-q growth in Q420.

We expect strong growth in private consumption and gross fixed capital formation to lead the recovery over the coming months as New Zealand’s recovery continues to firm although persistent supply chain challenges do still pose downside risks to the strength of the rebound.

We expect the recovery in private consumption to be robust, and have revised up our private consumption growth forecast to 5.8% in 2021 (revised up from 3.0% previously), marking our view for a strong rebound from a 1.8% contraction in 2020. Private consumption growth over the coming quarters will be driven by minimal domestic movement restrictions to contain another resurgence in Covid-19, given New Zealand’s strong track record thus far of containing Covid-19, and a strong labour market outlook, which bodes well for incomes. Indeed, the retail trade survey in Q121 showed 2.5% y-o-y growth, versus a 2.6% contraction in the previous quarter, providing an early indication of a turnaround in retail activity.

New Zealand’s effective containment of its domestic Covid-19 outbreak leads us to believe the probability of further protracted movement restrictions being implemented is slim. Additionally, while only about 6.73% of the population is currently fully vaccinated since the country started its vaccination rollout in February, we expect vaccine deployment to the wider population slated to commencing end- July, will support consumer confidence and business activity, spurring private consumption growth.

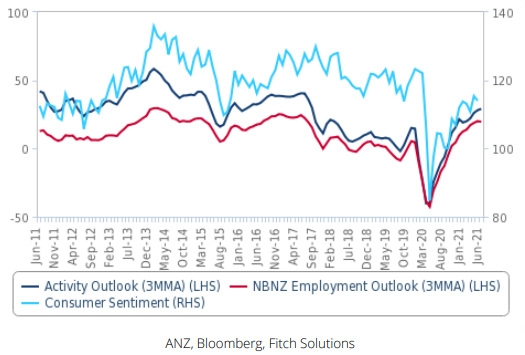

Improving Business And Employment Outlook To Support Consumer Sentiment

New Zealand – Activity Outlook Balance Index Vs Employment Outlook Balance Index, % Vs Consumer Confidence Index

An improving labour market, amid the ongoing economic recovery, will support disposable incomes and consumer spending. According to the preliminary read of the ANZ business outlook for June, employment intention remained firmly in positive territory, at levels not witnessed since 2017. Strong labour demand will likely mean a further tightening of the labour market and better prospects for wage growth. Indeed, the unemployment rate once again fell to 4.7% in Q121, down from 4.9% in the previous quarter.

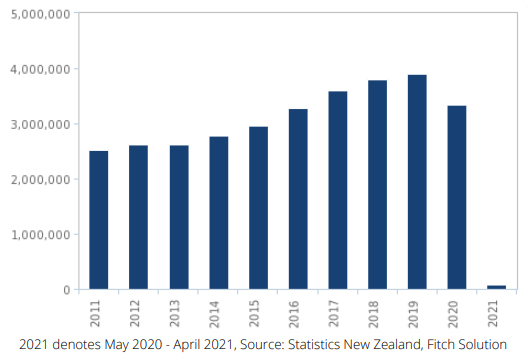

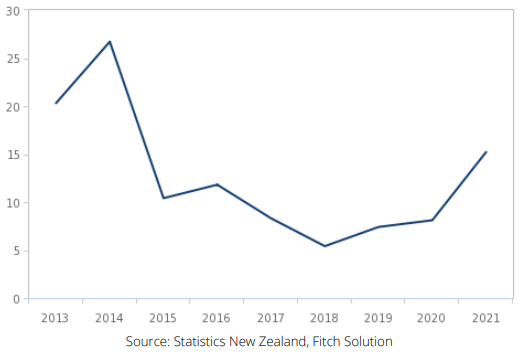

The Trans-Tasman travel bubble arrangement between New Zealand and Australia will also support private consumption to some extent and provide some respite to the ailing tourism sector. Demand for travel has risen following the bubble’s commencement. Total monthly international arrivals for April surged to 31,931, about two times greater than the total international arrivals for the first quarter of 2021. That said, total arrivals still remain very much below pre-Covid levels (see chart below) and as long as broader border closures continue, support from international arrivals will remain limited.

Tourism Continues To Perform Poorly

New Zealand – Annual Tourist Arrivals (Year Ended July)

2021 denotes May 2020 - April 2021, Source: Statistics New Zealand, Fitch Solution

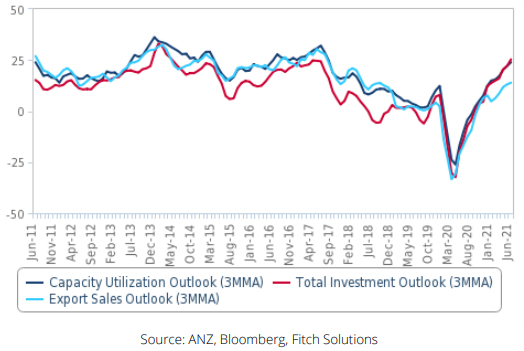

We forecast gross fixed capital formation to grow by 6.0% in 2021 (revised up from 5.0% previously), rebounding from an 11.2% contraction in 2020. A strong terms of trade position, combined with low domestic interest rates and increasing capacity pressure in some sectors of the economy, will incentivise businesses to invest. Indeed, based on the preliminary figures of the ANZ business outlook for June, total investment outlook balance index is positive, meaning that the percentage of respondents expecting an increase in investments is greater than the percentage of respondents expecting a decrease in investments. The improvement in the investment outlook is in line with the capacity utilization outlook and export sales outlook (see chart below).

GCFC To Be Boosted By Favourable Factors

New Zealand –Total Investment Outlook Balance Index Vs Capacity Utilisation Outlook Balance Index VS Export Sales Outlook Balance Index, %

Meanwhile, robust housing market activity supported by elevated residential investments will further drive fixed capital formation growth. This is reflected by the record number of annual new dwelling consents in the twelve months to April, coming in at 42848 building consents issued. representing a 15.2% y-o-y increase over the period and notching its highest level since 2014. This should provide a strong pipeline of construction activity over the coming quarters.

Robust Growth In Building Consents Issuance To Spur Housing Activity

New Zealand –Annual Building Consents Issued, % chg y-o-y

The government’s infrastructure drive will be another catalyst for growth in this component. As part of the government’s agenda to boost New Zealand’s economic recovery post-Covid-19, it has detailed NZD57.3bn worth of infrastructure investment plans over the next four years (2021-2025, given the July-June fiscal year). This is in comparison to what was already a record allocation of NZD42bn in the previous budget. Therefore, on average, we expect public investment growth to remain robust, serving as tailwinds for growth.

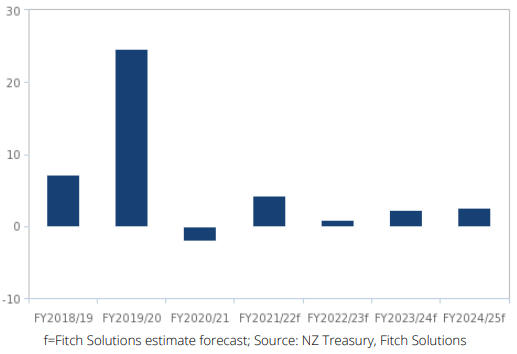

Growth In Government Consumption To Slow

New Zealand - Total Crown Expense, % chg y-o-y

We expect government consumption growth to slow to 2.0%, from 5.8% in 2020. This slowdown is due to an already significant increase in pandemic-related spending in FY2019/20 when expenditure rose by 24.7%. Additionally, as the economic recovery takes hold, the government will look to conserve fiscal space, paring back temporary pandemic-related spending. According to the data from the treasury, expenditure related to social assistance spending (which forms the bulk of expenditure in New Zealand at about 32.0%) was NZD1.2bn lower than the estimated spend in the Half Year Update for FY2020/21 (actual outturn of NZD45.0bn vs an initial estimation of NZD43.8bn). The government will instead shift its focus to long-term development projects to support the economy.

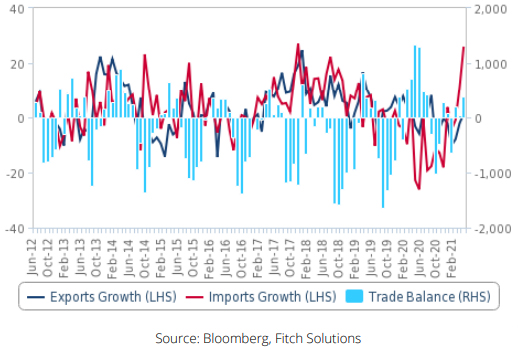

Import Growth To Outpace Export Growth

New Zealand – Exports & Imports Growth, % chg y-o-y VS Trade Balance, NZDmn

We expect net exports to drag on real GDP growth in 2021 as import growth will likely outpace exports growth in the coming quarters. Accordingly, we forecast net exports to subtract 0.8pp from real GDP growth in 2021 versus a contribution of 2.1pp in 2020. We maintain our forecast for exports to grow by 6.0% in 2021, versus -10.0% in 2020. With the global economy continuing to normalise amid more rapid vaccine rollouts, pent-up demand and the unwinding of savings will sustain strong demand for New Zealand’s exports. In particular, we expect Chinese demand for dairy products to lead the external demand recovery for New Zealand. Meanwhile, we forecast imports to grow by 8.0% (revised up 6.8% previously) compared to -16.3% in 2020. From an imports perspective, New Zealand being a net oil importer will mean that higher y-o-y oil prices will lift the import bill, while recovering domestic demand will also raise the quantity of crude oil imports. Our Oil & Gas team forecasts Brent oil prices to average USD66.00/bbl in 2021, up from USD43.20/bbl in 2020. Additionally, supply chain disruptions and the strong recovery in domestic demand will also further lift New Zealand’s import bill.

Risks to Outlook

The risks to our growth outlook are weighted to the downside. Global supply chain disruptions and surging shipping costs will put upside pressure on inflation, which could weigh slightly on private consumption growth. A lack of essential input due to persistent raw material and labour shortages could also cap growth in gross fixed capital formation.

Fitch Ratings and Fitch Solutions Country Risk & Industry Research are two separate and distinct divisions within Fitch Group. Each business produces its own independent research and commentary with different methodologies, audiences and products.

37 Comments

This is actually a good summary and let's all hope they are right. It is great if our local and central governments are starting to focus on long term delivery of infrastructure, rather than short term vanity projects. This is key for future growth in this country. However such delivery is likely highly constrained, partly by closed borders, partly from the huge amounts of social assistance we have in this country providing a disincentive to keep working (much of this around superannuation - we should find ways to encourage older people to stay in the workforce for longer as our population ages). Funnily enough I see a UBI with flat tax fixing many of the capacity constraints for infrastructure... much greater incentive to work means we can utilise latent workforce capacity both for those in later years and underutilised people who suffer from benefit abatement rate issues and those on WFF who get paid less by going back to work.

Some interesting points there, I think the UBI would indeed help. In general though the report looks through the skills shortage that this infrastructure spend requires.

Agreed on the long-term infrastructure, but your point on social assistance reducing incentive to employment is plain wrong - this is not supported by any evidence. Levels of social assistance in NZ are relatively low (https://www.oecd.org/social/soc/recipients-socr-by-country.htm) and we have 2 million jobs for 4 million working age people so I am not sure why we need more people to enter the workforce. A $15,000 per year tax credit (UBI) for all adults, with tax charged on every dollar earned, makes perfect sense though.

"we have 2 million jobs for 4 million working age people so I am not sure why we need more people to enter the workforce" - it's the missing 1 million in your equation that are a problem and a very much increasing one as our population ages while at the same time we all live longer, a double whammy for welfare. Encouraging our older workforce to stay working with some sort of incentive for doing so (like giving them a super top-up into their Kiwisaver or similar or allowing part time work while getting half their super without double tax or similar) would blunt the damage.

Our under employment rate (much like other advanced economies) is still far too high at over 12%, showing a lot of latent capacity in our workforce which could be utlilised given the right policy mix. That directly affects our GDP and long term productivity, particularly while we have labour shortages across the board, which is dumb when you think about it. Clearly we shouldn't have labour shortages alongside underutilised workforce, it shows a lack of the right incentive for people to work and a lack of skills required to fulfill the shortages.

UBI funded by bringing back LVT is the Georgist solution. Not all taxes are created equal. https://en.wikipedia.org/wiki/Progress_and_Poverty

Not quite George appears to derive all tax from LVTs. This isn't what you would do these days, instead you would tax consumption/income and assets at a similar rate. This makes it simple to administer and hard to dodge.

Currently housing is tax efficient, hence we are seeing people put so much money into it, starving the productive part of our economy of investment (i.e. the only part that creates real wealth).

My tea bag split open in my cup of tea this morning. Funnily enough the tea leaves left in the bottom said that infinite growth in a bounded system (the earth) is impossible. In the choice between tea leave reading and physical laws I know which I'd believe.

Infinite growth is possible, money supply!

Pretty much. Real GDP is calculated by dividing nominal GDP by the GDP deflator. The GDP delflator is bascially a price index similar to the CPI. We all know how much the CPI understates inflation (hedonics etc). The gdp deflator is a price index that suffers from the same flaws as the CPI. So who really knows what our real GDP is?? We live in a pretend economy.

The Stone Age did not end for lack of stone.

That is a big call. Bound to be inflationary. Can we get that growth once rates go up?

Great projections. Strong private consumption and rising incomes from labor shortages. My GDM emotive drivers are possibly way off the mark. And the wealth effect is possibly working its magic. Team of 5 million punching above its weight yet again.

There's no workers so I guess they mean 5% inflation due to supply and labour constraints

Have you ever heard of K shape economy?

The haves will experience an upward growth while the have nots will had the opposite.

This is seen in housing most certainly.

Anyone who hasn’t got property should be given a 50k cheque. Daylight robbery by NZ Government. Make property holders wealthy and get FHB to pay for it. Pretty low really.

Helicopter money would have been a much better way to inject $timulus.

How is the government robbing anyone? House prices are set by buyers not government.

Printing money and pumping it into debt markets with near zero % interest rates inflated property and shares as a way to stimulate the economy that massively favoured the rich. Essentially they solved the economic crisis by giving rich people more money to spend. When in reality poor people are far more likely to stimulate the economy with spending. As the previous person said, a broad base monetary distribution would have been far healthier for society and better for the economy. Rather than the narrow base asset inflation that they chose to go with.

You have to hand it to Yuong Ha, Geoff Bascand, Christian Hawkesby and Adrian Orr. `

Their brilliant idea to blow a housing bubble on top of a housing bubble has saved the New Zealand economy from suffering the humilation of GDP growth a couple of percent lower. And its almost a victimless crime, all those poors who are now burdened with paying hundreds of thousands more for a place to call their own should be thankful really. Trickle down economics is actually a free golden shower.

"You will own nothing and be happy" - https://www.youtube.com/watch?v=lBBxWtKKQiA

Said no-one in the real world ever. Without assets all the things you rely on are loaned to you and can be removed when they are required by the owner.

Including the programmable money they are itching to introduce.

I know it triggers certain people here to say it, but central bankers really are the greatest crooks on the face of the planet.

The stuff that makes me itch is when people talk about the Fed like it is a government organisation. Run by bankers for bankers and the most frustrating bit is that it has always been the case, it's declared in the Federal Reserve Act 1913.

I am no tin-foil milliner but if people don't think the world is run by bankers there is plenty of evidence that at a minimum the global economy is and that economic constrains control to a degree how people can live.

Agree about the Fed - the infamous meeting etc.

But the greater joust is every one of us competing for access to that resource/energy stream. Some of us are winners, some losers, and a lot of it at this stage is poker; belief and bluff. The joke is that if the system collapses - via loss of belief - most of the bankers 'wealth' goes too.

But the herald says that we are going down the gurgler because Indian restaurants can’t recruit migrant chefs. And a ski field might not open cos they can’t get a man from Sweden to operate the snow maker — they’ve only had 10 years to train up a local! Forget the stupid bridge, the stupid EV feebate, the nutty Climate Change Communard, raging house prices and the vaccine shambles. If JA and the crew can deliver 5% growth and historically low unemployment, even the return of John Key won’t save National. It’s about the economy, stupid.

The Herald also operate OneRoof. Cockroaches have a higher social status.

When I'm having a tough day I simply remember the NZ Herald has a paid subscription.. hehe makes me smile just writing it.

There is little National could do, even if they were capable, which they are not. The only head wind (and really it is only a zephyr) is the requirement for them to maintain their woke cred which is a mission impossible.

all the curry mixes are out of a can anyway

what they are saying is that they cant make a big enough profit without exploiting some migrant workers

"The risks to our growth outlook are weighted to the downside"

Richard 111, Bosworth. Insert other.....

Gotta love an infomercial.

Is this an article or paid content?

The economy is at risk of overheating, the OCR needs to be raised...

One of the big worries is rising freight costs to get anything in and out of this country at the bottom of the world. Over time this is going to become a bigger and bigger hurdle as the world is forced to become more local. Some of what we Import/Export is plain stupid and that's going to have to change. At the moment its just a pure cost in dollars calculation but that will also have to change to include the cost to the planet.

Well done the red team.

Keep the good work up

I don't know which growth our Govt. is chasing, by opening doors of mass immigration & pushing kiwi's to the brink of loosing basic necessities i.e. housing.

Public housing waitlist multiply 4 times from the day labour come into power.

https://www.stuff.co.nz/national/politics/300335849/public-housing-wait…

There is no hope now the damage is irreparable, FHB should seriously think to migrate rather than binding themselves to paying high rents or huge mortgage for rest of their life.

Fitch seems to have assumed that what the government announces is what is going to happen…well I guess their deep knowledge and understanding of the countries and companies they report on is why they get paid the big bucks.

“ while only about 6.73% of the population is currently fully vaccinated since the country started its vaccination rollout in February, we expect vaccine deployment to the wider population slated to commencing end- July, will support consumer confidence”

“ The government’s infrastructure drive will be another catalyst for growth in this component. As part of the government’s agenda to boost New Zealand’s economic recovery post-Covid-19, it has detailed NZD57.3bn worth of infrastructure investment plans over the next four years”

Interesting to see there projection has by far Private Consumption as biggest GDP ‘real’ contributor. With next exports negative, real must be funded by Debt. I guess they see low interest rate party continuing for a while yet.

The only growth is people cashing in on their house price gains and spending up creating ever more debt. This has nothing to do with the real economy . Surely an economy that was truly buzzing would be paying down that debt and still growing. Its all smoke and mirrors and full of people trying to talk it up and trying to control the outcomes using just words. At some point reality is going to set in and its not going to be pretty. Those people that locked in their mortgages at a decent 5 year rate will be breathing a sigh of relief.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.