Economists at the country's largest bank now believe the Reserve Bank will be forced to increase the Official Cash Rate from as soon as next February following the stunning 1.6% rise in March quarter GDP.

ANZ chief economist Sharon Zollner and senior economist Miles Workman said the first quarter GDP figures confirm NZ’s economic recovery "has been spectacular relative to early-pandemic expectations".

"...The core drivers of domestic demand, alongside lingering supply disruptions and biting capacity constraints, mean inflation pressures are lifting strongly," they said.

"That’s consistent with OCR hikes being needed, and a year from now feels too far away. However, a February hike is highly conditional, in light of the Reserve Bank’s “least regrets” approach. In particular, the evolution of inflation, inflation expectations and the labour market are key."

The March quarter figures released by Statistics New Zealand on Thursday simply blew all forecasts and expectations out of the water, following as they did a -1.0% fall in the December 2020 quarter.

The Reserve Bank had been forecasting a -0.6% drop for the March quarter. The market expectation had been for a 0.5% rise - although expectations had been sharply rising in recent days after the release of positive data in the run-up to the GDP release. Retail sales figures in particular had fared much better than expected.

It was inevitable the news of the actual outcome for the March quarter would turn talk to the prospect of interest rates rising.

The RBNZ is forecasting the first rise in the Official Cash Rate (from the current 0.25%) in the second half of next year, but economists had already suggested before the release of the GDP figures that the first rise may come earlier than this.

The GDP detail

"After an easing of economic activity in the December quarter, we’ve seen broad-based growth in the first quarter of 2021," Stats NZ's national accounts manager Paul Pascoe said.

"This is despite Auckland being in alert level 3 lockdown for 10 days, and continued border restrictions."

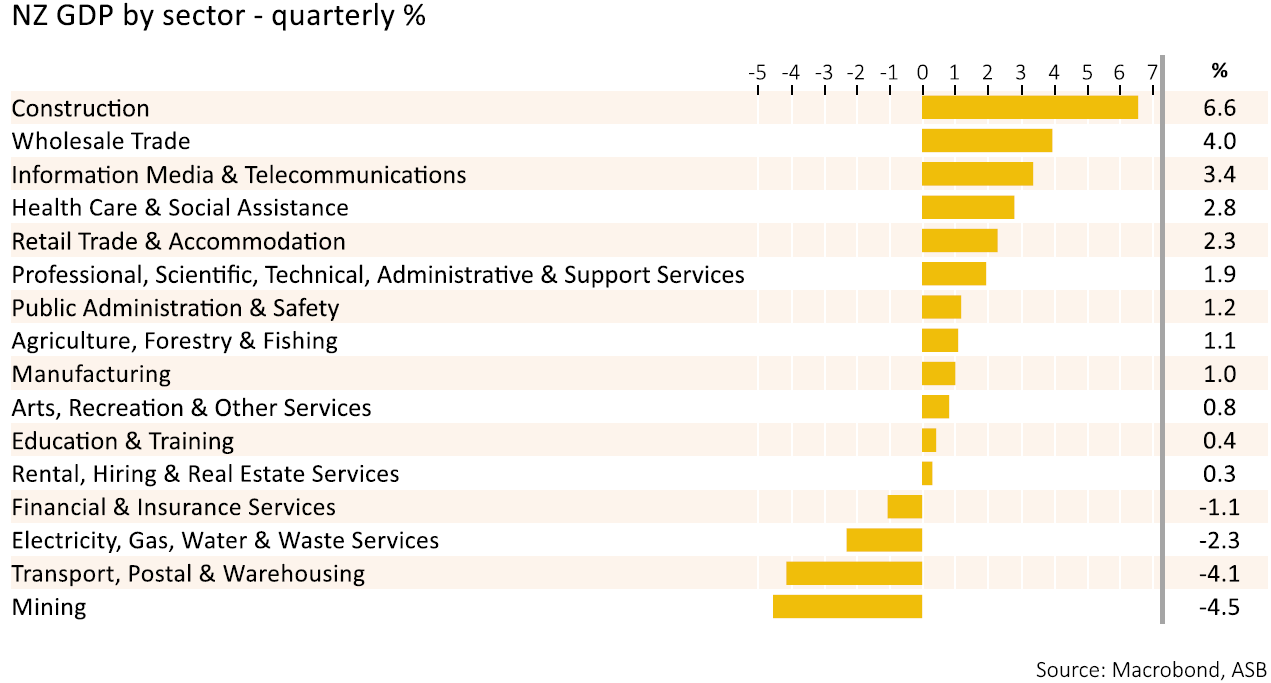

The services industries, which represent about two thirds of New Zealand's economy, made the largest contribution to the result.

"Households spent more on accommodation, eating out, and purchasing big ticket items such as furniture, audio visual equipment, and motor vehicles. This helped support the growth in retail trade and accommodation industry and wholesale trade industry," Pascoe said.

Household consumption spending rose 5.5% in the quarter.

The construction sector rebounded 6.6% after a fall of -8.4% in the December 2020 quarter.

'Remarkable'

Kiwibank chief economist Jarrod Kerr said the overall 1.6% March quarter gain was "remarkable".

"You’d be forgiven for thinking that was the annual rate. Nope. The annual rate was 2.4% - compared to consensus expectations of 0.9%. The report was stronger than expected – pretty much across the board. And the economy has confidently returned to pre-Covid levels.

"...We’ve more than dodged a double dip recession. We’ve outrun it. A solid rebound in construction activity and strong domestic spending have more than offset the loss of international tourism typical over the summer period."

Kerr noted that the "whopping" 1.6% bounceback came in well in excess of the Reserve Bank’s forecast of another quarterly dip (-0.6%).

"As the markets digest today’s strong report, we should see expectations shift toward an earlier lift-off in the OCR than the Reserve Bank has schedule. Our forecast May ’22 start date for RBNZ rate hikes looks increasingly likely."

ASB chief economist Nick Tuffley and senior economist Jane Turner said the time for the RBNZ to normalise interest rates "is fast approaching".

"We currently expect the RBNZ to start lifting the OCR in May next year but the risks are now skewed to an earlier move.

"Borrowers should brace for the end of record-low interest rates."

Economic growth

Select chart tabs

78 Comments

Pretty incredible really. I think central banks are globally going to have to move sooner. The RBNZ might even do one rate hike by Christmas year if data continues to surprise on the upside by this much. The Fed saying 2023 and AU RBNZ saying 2024 are still in absolute dreamland so despite what we all think of Orr at least he's being quite a bit less delusional compared to the other central banks. I sincerely hope with these existing and worsening capacity constraints - businesses continue invest far more in Machinery and automation to drive productivity.

ANZ now forecasting a February hike, but then again they didn't call this forecast.

https://twitter.com/economics/status/1405318883712569349

I don't. A rise in the OCR even to 1.5% will crash house prices. The RBNZ & govt won't let this happen. Unless the integrity of our currency is threatened they won't raise interest rates.

Agree. The NZ economy = house price appreciation. Sooner or later the party must end, but later is my pick.

It's more like they don't want that happen, but it doesn't mean they wont. When we get there, they will have no choice but to increase the rate. Crash house prices is better than crash the whole economy and use endless years to recover it. Also Orr and RBNZ keep saying the house price in not in the mandate, this means that housing price going down or up is not in consideration when they make decision towards OCR. So I don't think it's smart to your property booming hope in them.

House prices are the whole economy.

Then the crash is inevitable. I haven't seen a country has a functional economy by just exporting houses.

We don't export houses in this country but we do import tenants. When not at home, you can find those people working in our farms, driving Ubers or cooking our takeaway meals.

Yes. We are importing tenants, because they are used to renting. When the Brain Drain 2.0 hits, add or young people realise that house prices are insane, immigration will increase a lot to bring in needed skills that will head overseas.

Sounds like a conspiracy theory to me. The government doesn't get a say in what the independent RBNZ does. If the RBNZ does see real inflation coming it will raise rates, it has no choice.

Once US and rest of world start lifting rates NZ will have to comply or NZD will tank.looks like it’s going to be a rush to sell before shit hits the fan

The wolf is coming, The wolf is coming.

Won’t happen until this whole covid situation is over and global travel reopens again, until then…all just talk.

We are in the covid era.

this coupled with the FED's announcement, bye bye cheap rates!!!!

Banks started to lower short term rates in anticipation of a recession announcement.. they will be scrambling now!!!!

Second sentence re banks I think is a bit off. Banks lowered short end rates because they have access to FLP and LSAP is still suppressing the short end of swap curve. Curve has steepened after Fed & GDP not a parallel shift. They saw the steepening hence the 1yr mortgage rates down but 3yr-5yr up. Suck those customers into another short term tenor (1yr) so in June 2022 they're faced with a much higher rate card.

Recent article on interest.co.nz indicated that banks have barely used FLP funding, instead it seems they've just been using the growing On Call/Cheque balances for funding, which are effectively free (pay 0% interest), since most people aren't bothering with term deposits anymore.

Yes indeed. A move from term deposits to transactional/call deposits has provided well for bank margins. The mere existence of the FLP facility and the assumption it will be fully utilised before it ends is all that's needed to effect rates. LSAP likely having a bigger effect. RBNZ has been paying through mids to buy shorter tenor govt bonds lately. My original point being that banks lowering 1yr but increasing 3yr - 5yr mortgage rates is a curve steepening play rather than expectations of a double recession. Back of the envelope example (very rough), $750k mortgage you can currently fix for 3yrs at 2.99% or 1yr at 2.19% (saving $6k), suppose in a years time the bank anticipates the 2yr rate to be 3.99% so they get you to fix at that rate then for those two years you pay $7.5k more (vs the original 2.99% fixer), so the bank makes more by getting you to fix short term now and hope to roll you onto a higher rate in the future. The steeper the curve gets the more they set to make.

"suppose in a years time the bank anticipates the 2yr rate to be 3.99% (very conservative given that's only 44bps higher from today)"

Current 2 year rates are more like 2.55% so 3.99% would be 144bps higher. I'd be surprised to see 2 years 3.99% rates 1 year from now. At 2.99% (more likely), you'd be better off taking the 1 year 2.19% rate now.

Yes, my error I missed the 1 in front of 44bps. "I'd be surprised to see 2yr at 3.99%" I'm not so doubtful. Last time average 2yr was 3.99% was April 2019 when the 2yr swap was 1.68%. Remember the RBNZ had 150bp of hikes in their May MPS OCR track by end of 2024. Data since then has been very strong. After GDP the market (OIS) has brought forward the first OCR hike to May 2022. Most banks calling May 2022 hike too and even Feb 2022. So in June 2022 we could have an OCR 25bps higher at 0.50% and be looking 2yrs ahead to June 2024 (2yr swap) and it's actually quite probable that the 2yr swap will be around 1.70% and therefore very real chance of 2yr retail mortgage rate of 3.99%.

I see that the RBNZ is consulting with various parties , over morning tea, whether Bozo the Clown is to hand over the darts to the Chimp.

So we don't really need tourism....?

If we can keep kiwis spending their travel money at home, it's not too bad. If they all start going back to raro and oz instead of Qtown, though...

yes, it would appear tourism is a net loss to the country. We spend more overseas, than the overseas people spend here. Trap that local spending here and boom.

...and get two ticks on our emissions (inbound and outbound)

Plus we no longer need to bring in tens of thousands of low wage migrants into the country.

A researcher at AUT, as part of his PhD findings, stated in 2017 that wages in NZ's tourism sector have fallen 21-22 percent in real terms since the mid-1970s.

International tourism has clearly been a drag on economic productivity and wellbeing.

And how much of that money actually stays in NZ? Picture Bus loads of Chinese tourists. Everything paid for back in China and arranged with NZ resident Chinese providers and all services negotiated to the bone. PRC tourists are all handed the maximum allowable $10K dollars before arrival and hand it back when through the boarder. They are bused around and what they see and do is constrained to minimum cost to the operators. Services are largely provided by low cost temporary immigrant labor. Who is making the money here? What is in it for NZ?

Anyone else try to book tickets for a Great Walk this week? All the dates around holidays and long week weekends were sold in minutes, and the Milford is sold out for the whole season already - in record time. DOCs website crashed this morning under the pressure of it all.

Kiwis are making the most of the opportunity to explore our own country. Long may it continue.

Yep! I was lucky to score a milford and a routeburn booking. Usually that time and money I'd be spending overseas. Australia or Thailand usually.

Feels like the blast zone effect from rocket launched house prices.

Todays M10 data will provide confirmation.

Mitre10?

Think all suppliers are getting pricey on the building materials front.

Genuine question: why would this prompt a rise in rates, unless it's accompanied by a big CPI increase? Can't the RB just say it's evidence that 'stimulus' is indeed stimulating? There's no immediate pressure nor political incentive to 'normalise' rates that I can see.

Interest rates aren't just used to control inflation - they are used whenever there is a sign of the economy overheating. A jump like this in GDP- particularly consumer spending at 5.5% increase indicates there is a lot of demand in the economy and business in particular are reaching high levels of service and goods production. However too much over production can result in supply constraints of commodities and labour - this is known as the economy overheating - cheap debt means companies can buy more commodities and labour (or if they are supply constrained they pay more for the smaller pool of resources- resulting in inflation).

Interest rates are lifted then

1. To cool the amount of debt for businesses and the amount they can pay for the supply constrained resources

2. Households have higher house payments so they then have less disposable income to spend on goods and services- cooling the demand for these.

3. Non mortgage households save more (as they get a return on investment) and spend less on goods and services.

Inflation then eases and the supply /demand for the resources rebalances.

If you don't lift interest rates then you get a situation where some businesses can no longer operate and run out of resources and go broke (basically they end up with cashflow issues) - this results in a recession - and a concept called stagflation - prices are rising , the economy starts to stall, unemployment starts to rise. It creates a very ugly recession.

Exactly - if Orr does not urgently raises rates, NOW, this will be a serious breach of his mandate, and a big mistake that he will come to regret later on.

Just further to this - one of the problems with inflation is its a lag indicator- most governments and central banks wait to see 2 or 3 qtrs of data before making calls on interest rates and often the horse has bolted by the time they make the calls (this occurred in 07 + 08) so interest rates then need to be lifted y 0.5% of in consecutive months to have an effect.

To counter this most economies such as Australia, UK, EU and America look at data on a monthly basis - in the case of the US they look at unemployment figures weekly - so they get a sense of trends sooner.

NZ however is notoriously slow- all our data ie unemployment, GDP, CPI, PPI and RBNZ decisions are all quarterly so this will make us vulnerable to making decisions too late and having to lift rates quicker and higher or worse still overheating the economy without realizing there is a problem.

The inflation rate data will be very, very interesting. We saw Q1 PPI surging, which is often considered a leading indicator for CPI and in conjunction with GDP higher than estimate RBNZ might have a lot of inflation they need to "look through" in the second half of this year.

The largest driver of the increase was investment in plant, machinery, and equipment, which rose 15.5 percent in the March 2021 quarter

Construction was the main contributor, to the goods-producing industries, rising 6.6 percent

A proposed building regulation reform currently being pushed through its final stages by MBIE could significantly lift construction output and boost related manufacturing activity with the help of a 'modular component manufacturer' scheme (offsite construction and prefab manufacturing).

This scheme has the potential to alleviate some of the chronic skill shortages in construction trades with the help of existing technologies in industrial automation.

"This scheme has the potential to alleviate some of the chronic skill shortage" and increase productivity.

Oh no, a failed prediction! Some people are going to have a meltdown.

I'm going to call it- If the REINZ and corelogic reports show in July and Aug a still rising housing market - then the RBNZ will lift interest rates by a quarter of a percent in August - as a shot across the bow to cool the market.

Initially I had thought with a sluggish GDP they might wait to help out business (with lower debt funding) but all excuses have now left the room.

I agree it would be the wise thing to do but I doubt the RBNZ will do it

There is no reason whatsoever for not increasing the OCR, NOW, back at least to pre-Covid levels. The OCR should be raised immediately to 1% and all forms of QE stopped right now.

Not doing so would be a breach of the RBNZ mandate. Orr has no excuses left.

Not surprising the the economy took a licking and keeps on ticking. As long as no one mess around with the interest rates, there won't be an immediate recession - I told you so!

RBNZ should focus on the 2.5% inflation target and ignore the noises from AstroTurfs.

This article does not mention debt, nor the resource-base reductions required to achieve this much-lauded number.

Is that oversight going to be addressed?

[ Irrelevant comment with dangerous link removed. Don't do it. Ed. ]

New Zealand bank economist has got to be one of the easiest jobs in the world. All you need to do is scribble down some prediction on toilet paper each time you take a dump. It doesn't matter if you are right or wrong because you'll scribble something else tommorrow.

What a waste considering for a while last year, housing became the second-most fought-over commodity in NZ after toilet paper!

Excellent article by Bernard Hickey.

Confirms that even if DTI is implimented than will not be before 2023 and is also correct that NO political wants the housing ponzi to stop and Jacinda Arden has gave personal assurance that under her the ponzi will continue.

Bad new for FHB as they have been and will keep on been screwed only posistion will change.

https://thekaka.substack.com/p/a-chorus-rbnz-gets-dti-tool?token=eyJ1c2…

Timing of mentioning DTI was only to shift attention from ever rising house price.

Why wait until next year ? Raising the OCR to pre-Covid level right now would be good

Exactly. It went down like a lead balloon, but takes years of thought to lift it a tiny amount.

The only reason Yvil is saying that is because hes cashed up and looking to buy after selling his house, and wants the rbnz to scare off other buyers so he can buy at a discount.

Yvil took a dollar bet each way and lost. That Ponsonby house has probably gone up $500k since he sold it about a year ago.

Yes indeed, with the benefit of hindsight, it was a bad decision. Luckily I own other real estate which has appreciated in value but yes, in March 2020 I thought it was better to reduce some of my Real Estate as I expected prices to level at best or go down. I was wrong

Ha ha. Crunch time approaching.

Inflation is here already.

Wolf Richter column today in USA shows fed way behind curve and they are talking about 2023 - stroll on.

Now, NZ its no extra mortgage rate cut sweeties and instead, the prospect of cost of loans RISING for first time in 7 years. Oh dear....

They will have to rise a great deal before this home owner is paying a market rent equivalent.

Depends on where you look. The rent I pay is less than the interest I would be paying if I brought the house I live in today @4% interest 20% deposit.

Sounds like your rent increase is overdue

Maximum troll level attained…..

I pay market rent. I'll move if they try charge me more.

You make it sound as if it's easy to move and there's plenty of cheap rentals available, there's not.

I've moved so many times ive got the process pretty well sorted, that it's not an issue. I don't have children or pets, I'm in a professional job and landlords always snap me up. If they dont show me loyalty by not raising my rent, I wont show them loyalty by staying. Its that simple. Plenty of rentals in Auckland, its gotten easier to find quality ones with closed borders, and rents actually seem to be going down.

Of course our good friends and Masters, P8 and Yvil will see the naughty ANZ as being overly negative or even DGM?

You should read previous comments before posting.

by Yvil | 17th Jun 21, 1:19pm 3up

Why wait until next year ? Raising the OCR to pre-Covid level right now would be good

To be fair, Yvil has been consistent about their thoughts on the OCR and the need for it to be raised.

Yes ... we are BOOMING! ... we are RICH RICH RICH i say ...

now has anyone seen the Govt credit card, i need some groceries

Your post is not even satirical. Coworker made about 500k in capital gains in the last 3 years by the virtue of owning a house (through divorce). Yet she has zero savings and struggles if the monthly wage transfer is late one day. Literally a millionaire who can't afford groceries.

In Auckland you can be a millionaire that can't afford a house.

Clown country.

The government is big on holding inquiries and making apologies for past wrongdoings that seemed ok at the time, but with hindsight seem outrageous. I wonder what year we will see an apology issued to those tortured by the runaway house prices caused by emergency ocr rates left in place for too long.

But whats the alternative - the govt itself sets the OCR? DO we really want to go down that road again

Well I would have thought the alternative is that the RBNZ sees the predicted covid collapse of the economy didn't happen and so return the ocr to an appropriate level. It's like watching a young fella driving dads car full of his mates on a metal road....way too slow to react.

I do not see how the RBNZ can be out of synch with the RBA who have stated they don’t see rises until 2024 unless they are happy to sink our exports.

why panic I thought the Banks stress tested to 7%...so only the ones that lied to the banks when they took out the large mortgage need to panic.

The bank tells you to lie on the application form so you can get a loan. Friend just brought a house and was told to put down his brothers name down as a boarder so he could get the loan.

Wow, RBNZ forecasted 0.6% drop, and there was a 1.6% increase. The incompetence of these fools knows no bounds.

They attempt to forecast the future with statistics that looks backwards. It never works.

More politics from the banks. Even less surprising it's ANZ this time. Rates are going up, and they are also going down! This Govt wants you to believe they are going up, which unknown to them, only creates more short term demand.

So much pounding, but no orgasm.

Filthy

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.