New Zealand's current account deficit could be heading north based on what may be an emerging trend outlined in PwC's latest bi-annual Banking Perspectives report.

Covering the country's big five banks - ANZ, ASB, BNZ, Kiwibank and Westpac - Banking Perspectives provides a thorough wrap up of a half-year period for the five. The latest one covers the first-half of their 2015 financial years.

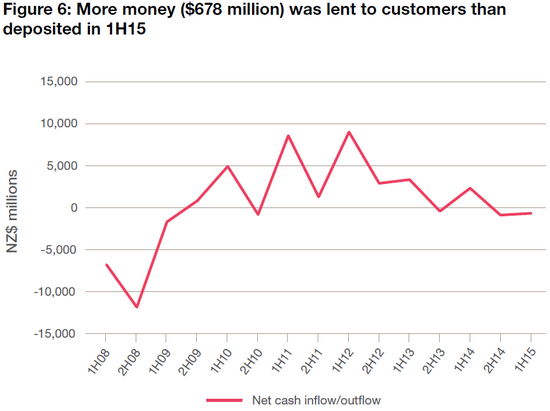

One section I always find interesting is the funding one. The latest one confirms growth in customer deposits didn't keep pace with lending growth. This means funding outflows exceeded inflows by $678 million. As PwC's Figure 6 below shows, this makes it two halves in a row, for the first time since the height of the global financial crisis, where lending growth has outpaced deposit growth.

"With the second consecutive period of new lending outpacing new retail deposit funding, the banks will be required to rely on wholesale funding or retained earnings to fund further lending growth," PwC points out.

As credit rating agency Standard & Poor's noted earlier this week New Zealand still has a "material dependence" on net external borrowings, which make up about 30% of domestic customer loans and 25% of the banking system's total liabilities.

The most recent figures from Statistics New Zealand showed an annual current account deficit of $8.6 billion, or 3.6% of GDP, for the year to March. NZ's external debt position, showing the difference between overseas lending and borrowing, dropped $2 billion to $138.9 billion, or 58.1% of GDP, in the March quarter. Statistics NZ noted an increase in reserve assets held overseas was partly offset by overseas investors buying debt securities issued by banks during the March quarter.

If the big banks continue pushing more money out the lending door than they take in the deposit door, it'll be interesting to see what impact this has on the current account deficit in coming months.

PwC's figures show deposits from customers grew by $9.2 billion in the first-half to $237.3 billion. And, as of March 31, that represented 69.8% of total funding at the big five. Total funding stood at $340.2 billion, up $7.2 billion, or 2.2%, from the second-half of the banks' 2014 financial years.

Gross lending, meanwhile, rose $10 billion, or 3.2%, to $325.2 billion over the same time period.

PwC figures also demonstrate the impact of the Reserve Bank's core funding ratio and liquidity policies, with a deposit-to-loan ratio of 73% up significantly from 56.3% in the second-half of 2008.

To put a different spin on the $678 million funding outflow figure, that's equivalent to about three and a third days of residential mortgage lending based on last week's Reserve Bank new home loan approval figures. They showed $1.4 billion of loans were approved during the week.

And another factor to watch in terms of deficit contributors, is dividends paid by the four Australian owned banks. The Commonwealth Bank of Australia owned ASB's annual results last week showed ordinary dividends almost trebled to $1.14 billion in the June year from $400 million last year. That was equivalent to 135% of ASB's $846 million annual cash profit and ate into the bank's retained earnings.

For their 2014 financial years ANZ NZ, ASB, BNZ and Westpac NZ paid combined dividends of $2.561 billion.

*This story was first published in our email for paying subscribers. See here for more details and how to subscribe.

13 Comments

Considering that most wages and salaries are deposits, this can help people to conceptualize the magnitude of bank lending. However, I think that most people who have any interest whatsoever now understand that the relationship between lending and bank deposits becomes more insignificant by the day. Australia's banking system relies on wholesale funding for the banks to make profit, so that naturally extends to us. Therefore, it's savings in Japan and other countries that gives us the fuel to take on bigger loans, particularly for property investment. While this might seem intuitively wrong to the average person or household raised on conservative values related to money, our institutions have adopted and internalized a global mindset towards capital.

I'm not sure why this is not taught in high school economics or perhaps it is.

Please explain what you mean by "household raised on conservative values related to money"

or can we simply say == Austrian?

ie I am not sure at all what you are referring to as high school economics, except high school economics is a simple bit of economics designed to start teaching children about economics and usually has no real world match.

Conservative values in that if you spend more money than you earn or save, you go bankrupt. Furthermore, if you want to purchase something like a house, you are required to save a deposit.

I think that most people are unaware that govts can't go bankrupt under the a monetary system where money can be created instantaneously. I also think they are unaware that banks borrow offshore (wholesale funding) so they can make more profit on the money they lend us for mortgages.

I would think that it's good that people understood the above as they underpin our systems and institutions.

"I think that most people are unaware that govts can't go bankrupt under the a monetary system where money can be created instantaneously"

The difficult problem is people that believe that.

If it was true there would be no purpose for taxing the population as the government could borrow indefinitely, and things like Grexit's wouldn't even be a thing, let alone a mass currency mover.

Governments with their own currency can print indefinitely, so if they have borrowed only in their own currency, they cannot go bankrupt. Greece does not have its own currency, hence the problem. Argentina borrowed in US dollars and got into bother.

Most governments will want to protect the value of their currency for a bunch of reasons and so are judicious about how much printing they allow. For less solid reasons they mostly delegate printing to commercial banks, as in New Zealand. The commercial banks in NZ have printed about $23 billion in the last year. That's a key driver of their ability to have paid themselves $2.5 billion in dividends in the year. The fact inflation is close to zero suggests there is nothing wrong with this amount of printing, although I think there could be a range of questions whether overall monetary policy is ideal, given asset bubbles, a high current account deficit, very significant loss of wealth through asset sales, and other issues.

Doesn't work like that in practice.

Even if Teddy's bank had gone ahead, rapid printing to stimulate the economic spending would have resulted in (contracted) debt shrinking. So under that umbrella, the theory is the government could keep printing to have whatever infrastructure it wanted. eg NZ or Sweden to print unlimited currency to pay all education bills; no longer would cash be a barrier to education so anyone who wanted an education could have one - free !!

Buuuuttt. Government meddling in one part of the market. What would be the point working for shrinking money (trading power) anywhere else in the economy? Only working for government (which produce nothing of real value, for a connected reason) would produce any inflation-adjusted income.

So government must budget itself based on the whole economy not just one piece.... so if they give everyone free currency equally, what need would there to be work? Real production would have to be enforced by other means...which means there's a fake value currency, and a "real money" which has no currency only government force.

They use the banks because that one they can control people, especially young people, through debt and life needs. Without that system what control of scarce resource can there? Who gets the Ferrari and the Mercedes? Who gets the 5bd 3bt 3g with coastal views? Who shovels or fixes the sh..ter? for a community to function someone needs to do some of the less fun jobs, and only a few get the best chunk of the kill. The banks ensure that and their owners rewarded and protected appropriately.

a government printing what it wants to stay out of bankruptcy would destroy all of that. (hyperinflation)

I don't think anyone's suggesting governments should print unlimited amounts of money; rather that they can, and so cannot go bankrupt if all their debt is in their own currency. For mostly the reasons you outline, governments wish to protect the value of their currency- hence inflation targets; but also want economies to grow, hence increase in the money supply. I think who prints, and under what economic circumstances, is an interesting, but different, subject.

except... that they can't.

Oh sure, in "theory" it's possible. Just as it's possible for me to print my own currency.

but without tax and interest enforce-able by force, fiat currency is worthless. There are Roman and Greek examples of cities and governors printing their own currency and trying to create endless money - but money doesn't work that way. Money is trade - people just stopped taking it, neighbouring nations refused the coin, or would regard it only for it's bullion value.

That nations own debt swallowed it and its people - a modern example is Cuba. where you have the local "old" peso, and the modern "new peso" that the tourists can buy and use to trade. The exchange rate last time I heard was about 300 to 1 IF you could find someone to take it, AND if you could get a local who had 300peso to their name. Because the government paid its debt to its soldiers and supporters with currency, there was no reason for those services to trade with others. Almost a reverse Greece. The government was "rich", its suppliers were "rich", but the currency was worthless for trade because no-one else could buy anything with it. Sure the government could keep printing and pretend it had no debt but it just made everyone bankrupt, as deadly force was used to stop other money (trade) occurring, yet all non-government trade was worthless...and government trade had no value-add (margin, by 6 forces analysis speak) beyond its internal structure.

Yes I thought it would be something like this, however

a) a nation's economy is nothing like a household economy, the latter model simply does not scale up to the former.

I would prefer "old fashioned" as a phrase myself as laid out below.,

b) there are such things as a 100% even 110% loan but these seem to be offered in right wing, un-regulated, free markets, which is a contradiction to "conservative" surely? Also here 20 years ago 80% was the norm max, now it seems like 95% is. That % driven higher by the wishes of the bankers to make profit also a pretty right winger view? So the Q is why have conservatives allowed ever increasing LVRs? and then just listen to the likes of notaneconomist's on ppls rights to buy no matter what. So what I am pointing out is the contradictions in our discussion. Now myself I refused to get a bigger mortgage 20 years than I got considering 60% way big enough which I guess tends to make me " old fashioned" it "paid off when my wife because to ill to work as we could cope.

If most ppl are so unaware on how borrowing is done, (and considering how so much has been said on this for many years ie NZers dont save enough that surprises me) then surely it is their failure? Also in terms of borrowing offshore I see that as no consequence, except in extremis. ie

Such lending does indeed underpin our economy and its a concern but most ppl just dont seem to care of the risk or impact if foreign investors turn tial and run (witness Greece) . Besides which what is the alternative? there is none really unless you want a severely restricted and regulated economy as a result. Now as an "old fashioned" type yes I'l agree lending is too lax, but would pro-business conservatives?

(a) actually yes it is, and yes it does scale - you just have to remember to scale all factors not just the ones you want.

(b) I got a 110% loan for my dairy operation.

Sure it's tough meeting the interest payments, and the bureaucrats keep thinking I was ripping off the system because my income and retained earnings weren't high enough for their liking, and telling them there was was no money for pay rises just hit the employee denial wall (ie "you _must_ be paying yourself $80,000 because that's what we say the position is worth, and everyone else says that's what they're getting (which was bs)).

why give me such a huge loan? why take on such huge debt?

(1) I had significant security in residental houses.

(2) The operation provided considerable cashflow, more than enough to service the loan even to 15% interest.

(3) I had the skills, backing, and experience with that exact operation.

why wouldn't I take a 110% ? why wouldn't it be given? How is that lax? I did my diligence, bank did theirs' , it was our risk to take; and no-one was asking for bailouts - only fair price for customer demands.

but governments like households, if they produce nothing for the customers, receive no trade income. they can cut finer and finer, but in the end no real growth = no real growth. they can't just print themselves more favours (currency) without alienating everyone else(rest of family expected to cover the workload).

Considering that most wages and salaries are deposits, this can help people to conceptualize the magnitude of band lending. However, I think that most people who have any interest whatsoever now understand that the relationship between lending and bank deposits becomes more insignificant by the day. Australia's banking system relies on wholesale funding for the banks to make profit, so that naturally extends to us. Therefore, it's savings in Japan and other countries that gives us the fuel to take on bigger loans, particularly for property investment. While this might seem intuitively wrong to the average person or household raised on conservative values related to money, our institutions have adopted and internalized a global mindset towards capital.

I'm not sure why this is not taught in high school economics or perhaps it is.

the fact that "our" institutions have adopted a wrong global mindset towards capital doesn't make that mindset right, it makes "our" institutions wrong.

i wonder if the "modern" view of high debt and money printing is sustainable, it is a relatively new experiment at the global scale it is occuring. Do you feel like the global economy is going well as a result of these policies? My feeling is that we are nervously dodging bullets.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.