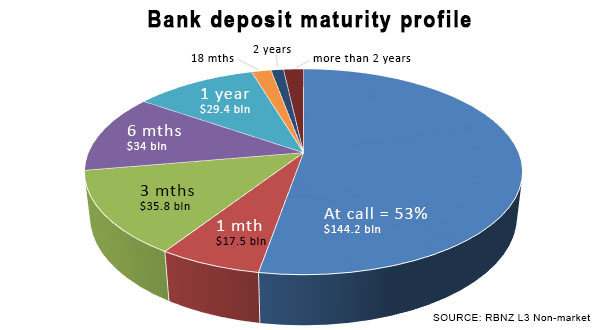

New Zealand bank customers (both household and corporate) have only $42 bln deposited with banks for one year or longer.

That represents just 15% of the total deposits we hold at banks.

Collectively, we are short-termists. In fact, very short-term.

And that is a problem for banks because their regulator requires them to have at least 75% of their funding with a maturity of 1 year or more.

Banks square that circle by borrowing wholesale for longer terms. They need that longer wholesale funding to meet their Core Funding Ratio minimums.

"Core funding" is an estimate of the funding of the bank that is stable and can be assumed to stay in place for at least one year. This includes shareholder capital, but it also includes a substantial part of the less-than-one-year deposit base as well based on estimates of the "replicating portfolio".

Much of our short-term money just rolls over endlessly. It is lazy money.

Banks model this behaviour and have a high degree of assurance that customers won't be withdrawing it suddenly. In other words, they 'know' it will still be there in a year (based on past experience). It is that proportion of short-duration money that can be included in their "core funding" calculations.

The "face value of funding by residual maturity" (L3) is overwhelmingly dominated by very short terms. 85% is there for 6 months or less as at July 2016.

A year ago, that ratio was 83%. Five years ago that ratio was 87%. The ratio has changed little over time.

To put this deposit data into perspective, here are the current components and how they relate to total loans and advances banks have made.

| Bank deposits | July 2014 | July 2015 | July 2016 | growth |

| a broad reconciliation | $ bln | $ bln | $ bln | % pa |

| Total household deposits (C17) | 129.9 | 145.1 | 156.8 | +8.0 |

| + | ||||

| Total deposits of companies/Govt/orgs | 98.7 | 105.3 | 116.6 | +10.8 |

| = | ====== | ====== | ====== | ------- |

| Total customer deposit funding (L3) | 228.5 | 250.4 | 273.4 | +9.2 |

| Wholesale funded component | 82.4 | 81.2 | 88.7 | +9.3 |

| ---------- | ---------- | --------- | ------- | |

| Total loans and advances (L2) | 310.9 | 331.6 | 362.1 | +9.2 |

Housing loans are growing by +9% pa according to C5 data, business loans are growing by +6.6% pa and rural loans by +5.5% pa.

[Thank you to Steven Hulme for referring to this data yesterday.]

36 Comments

The difference between a bonus saver and a term deposit isn't much. I'd rather have a the ability to pull out if anything scary happens. People that lock away their money seem to be using loan companies like Harmoney.

People who are locking their money away for a three/ five term at today's low rates will get short changed again as interest rates rise

will it be there in a year if an OCR event is signaled or will a lot suddenly disappear.

it can be moved pretty quick now a days

I would think they will not signal an OCR but enact it first if the worst case scenario happens

Er, OCR event?

Presume you mean OBR. Quite a bit of scaremongering about that eh

LOL yes OBR

It is obvious that you have not been to Cyprus. It is not scaremongering mate, it is there to be used when the bank/s fail. Remember the main banks in NZ are Australian, the country that guarantees deposits up to $250000. So we have the scenario where an Oz bank fails, New Zealanders get a haircut and the Australians are laughing all the way to the bank.

That is reality mate not scaremongering.

Even if there were an 'OBR event' despite the RBG saying there was no guarantee for New Zealanders' bank deposits can you imagine any Government doing that? It would be the death knell for any party particularly when Australians have $250,000.00 guaranteed by its Government

Where's your money Patricia?

This article kind of misses a few possible key reasons people do leave the money in a bank doing nothing. If you ever require credit from a bank or any other financial institution, it's a good look to have a healthy balance for one. And also, for many NZders fundamentally its more important to have immediate access to their money. So the puny pathetic locked in deposits rates these days hardly matter. Compounding becomes meaningless at certain levels of deposit vs interest, particularly when faced with rampant house price speculative growth.

When I can earn 3% interest with my savings on call at RaboDirect, why would I risk having my savings locked away for 12 months if it pays bugger all additional interest? It's not worth the risk in my opinion.

If banks want customers to deposit for longer terms then they have to make it much more attractive for them to do so. Not only are the interest rates pathetic even at longer terms, most banks now require 30 days notice to withdraw money from a term deposit prior to maturity and some also apply penalties for deposits withdrawn early. Depositors are also at the mercy of the OBR if it is ever activated and risk losing some of their savings. Meanwhile the banks are making $billions.

How much equity do the banks have invested here Missy - what returns are they getting on it ?

Don't ask Missy, ask the bankers, you know the ones that were bailed out when really they should have been made to go bankrupt and in league with politicians, have well and truly stuffed the world.

God knows what the returns are? But self calculated residential property capital risk weightings reported at 25% against 8% tier 1 regulatory capital demands is 2%. Not much room for judgements of error when it comes to lending above 50% of the asset purchase cost. Those in receipt of bank liabilities deemed deposits are really holding the bag at current interest rates.

Anyone putting money in the bank at 2% or even 3% is nuts, and needs to be referred for psychiatric help for having self harming tendencies .

The IRD gets 33% of the 2 %, leaving you with 1,66% and Inflation takes about half the rest in reduced buying power each year .

That reduced purchasing power is lost for ever on the capital sum , so the losses are quite simply exponential .

Why would anyone do it ?

Boatman - where would you put it ?

A very good question Grant A.

Yes, Investors dabbled in the alternative in the recent past and lost big, when the so called reputable businessmen turned fraud, and no punishment for that. Who will risk again ?

Yes, good question. One answer could be in a managed fund. Yes, I know, there are different risks involved. But presumably the question is being asked by yield chasers. So a managed fund could be an answer.

Some KiwiSaver funds have exceptional after-tax, after-fees track records. In fact, the best default funds have been impressive in this regard. See this. Fancy an after-tax, after fees return of 7% ?

Fancy an after-tax, after fees return of 7% ?

Hmmmm...

From an investment standpoint, the value of any security is inherent in the long-term stream of cash flows it will deliver to investors over time. Artificially jacking up financial securities through reckless monetary policy doesn’t change the cash flows that those securities will deliver over time; it only converts future expected return into past realized return, leaving nothing but risk on the table for years to come. Read more

I don't thonk so. from the frying pan into the fire.

@David Chaston It was a good question , and I will tell you that I have put it somewhere that I never imagined I would .......... Its in Bonus Bonds , and there is about 3 years income just sitting there , because I refuse to give it to the banks , and I may want it at short notice, if there is a major stock market adjustment , I will be in like a shot buying shares when the market is comatose ( it may take a very long time , but I hope the Fed increases rates soon to trigger a sell off )

The yield in Bonus Bonds has been okay , and I have been pleasantly surprised the first year was about 0,5% but this YTD its been 2,36% and its tax free

Quite simply I don't know what to do with it , the share-market is over-priced and I am already exposed there personally and with our Kiwisaver 100% in equities , Bonds are too risky and property has gone off the radar

IRD get 33%? no, 17.5% for most. Inflation definitly kills the rest.

Did you not point out a while ago recently that you had surplus cash you wanted to put somewhere other than the bank? So...care to say where you moved it too to avoid the psych ward?

We all know that, but where do you suggest we put our money. Under the bed, but that won't work will it, as the banks are now aiming to do away with physical money. Or buy property that gets trashed by tenants or ends up as a P house that cost heaps to do up and if you are lucky to sell. That is a real loss of purchasing power aye mate.

Perhaps people 'do it' because at call or short term means that it is accessible for those trifling matters such as urgent repairs about the house, the car breaking down or a great deal on something needed soon. Emergencies happen and most insurance claims carry an excess amount - sometimes into thousands in the case of your home being damaged.

Every budget advisor I have listened to states that we all should hold about three months income 'close by'.

No good having all your eggs in a long term TD or even a managed fund then.

How many are just one pay away from disaster?

Boatman,

I regard myself as rational(most of the time) and I have cash in a number of short-term PIEs with several banking institutions. Why? Well, for a start, the returns for longer terms are not in my view,sufficiently attractive.

Most of my capital in in the stockmarket and a rental property,but I always maintain a reasonable cash buffer for liquidity and to give me the ability to take advantage of investment opportunities. Where else should I keep this cash reserve?

I would of course like NZ to have a deposit guarantee scheme,but in its absence, I spread it over 4 banks.What do you do?

High time the tax rules are changed to allow the first $5000 in bank interest to be fully tax exempt....

Why? (Other than that would give you a special benefit.)

Then there will be an incentive to keep deposits longer term ? If businesses get heaps of benefits by the laws made for them by the MPs, why not for us ordinary citizens ? Don't we deserve them ? If Apple and Google and Starbucks can be favoured why not poor me ?

No different than the special benefit derived from buying and selling property. Why should they get tax free capital gains. Whole tax base on Financial Assets needs to be reviewed.

I don't know about the first $5,000, but the inflation portion of it should be. Conversely the inflation portion of the interest on any loan should not be tax deductible.

And because of the Aussie rules our Banks here (owned by Aussie Banks) have crimped the ability of long term depositors to access the money quickly in case of need. Now they need 31 days notice to withdraw Term deposits. A scam on the depositors, for sure ?

Smokey - a scam, your joking ? it's the regulatory requirements that incentives longer-term deposits for banks even minimum 30 days notice. They pay a premium for that and if that doesn't suit you then you choose something else - no mystery just choices

That rule was introduced just about a year or so ago. The banks worked without that rule for a long long time before that. What changed ? Because they were careless and required regulatory assistance to boost their solvency ?

This is just another way the legislators, regulators and the bankers screw the ordinary people who have not many alternatives. History is full of such moves.

Don't the Banks retain the right to recall the loans they make at anytime ?

Why should they insist on a notice period from the depositors who are lending money to the Banks ?

A contract is a contract. If term deposit is for a year the interest rate reflects this. The Banks had slack in allowing parts to be broken off term deposits, then when interest rates started dropping people started moving their money around or spending it. Still reckon in today's interest environment that term Deposit insurance should be available. When you borrow from them they want security, so do the suppliers of covered bonds.The era of free lunches is over

Don't say anything negative about banks. Grant A is watching like a hawk and will leap to the keyboard in defence. Strangely consistent in that respect.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.