Here's my summary of the key events over the weekend that affect New Zealand, with news the risks of outsourcing by banks is now getting some renewed focus.

But first in the US, the expectation was that the non-farm labour force growth would undershoot the modest expectations set. But in the end it beat those expectations, even if the absolute growth level was itself modest. Incomes are rising +2.5% in this survey, far faster than inflation. This data will keep the US Fed on its track to raise rates again this year and to start shrinking its QE holdings. And that being the case, benchmark yields rose again after the data was announced.

Canada also reported better-than-expected employment growth.

And back in the US, a new report says that while their major banks are strong, they face some new risks, many of which are outside their control. The report found that risks to banks lie in competition from nonfinancial lenders and in the rapid development of methods of money laundering and terrorism financing. Many banks have also increasingly become dependent on third-party service providers (like Amazon, IBM and Google) to support key operations within their banks. Over time, consolidation among service providers has resulted in large numbers of banks becoming reliant on a small number of service providers. It is a risk that our banks also have.

In Canada, they are looking at toughening up on how banks qualify borrowers for mortgages. Proposed new rules would require all prospective buyers - even those with a down payment of over 20% - to undergo a so-called stress test before a bank can issue a loan. Under the stress test, prospective buyers would have to qualify for a mortgage at a rate roughly 2% above what's negotiated. Actually, that is something similar to what is in place here now on a de facto basis.

In the UK, there is playing out another example of how closely central bank regulators shift between their role and the companies they are supposed to regulate. An deputy governor of the Bank of England is lining up the role as head of Visa in Europe. Earlier in the year she was forced out of the UK regulator on claims of undeclared conflicts of interest with a family relationship involving Barclays Bank.

In New York, the UST 10yr yield has risen again, now to 2.39% after the non-farm payroll data release.

The price of oil has fallen by more than -US$1/barrel to at just over US$44 a barrel, while the Brent benchmark is now just over US$46.50.

And the price of gold fell even more by -US$9 to US$1,213/oz. And in NZ dollars, that has wiped out about all its 2017 gains.

The Kiwi dollar is basically unchanged at 72.8 USc. On the cross rates we are holding at 95.7 AU¢, and at at 63.8 euro cents. The TWI-5 index is now at 76.9.

If you want to catch up with all the changes on Friday, we have an update here.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

3 Comments

But in the end it beat those expectations, even if the absolute growth level was itself modest. Incomes are rising +2.5% in this survey, far faster than inflation.

And yet those with a short term liquidity preference still seek the safety of one month Tbills at rates below the fed funds corridor floor.

Furthermore:

If there is actual improvement in labor utilization, it is proceeding at a painfully slow pace. At least in that way it is consistent with general economic conditions over the past few years. Whatever has occurred in either direction, other than the work requirements re-imposed via SNAP the US labor force has proved itself unflinchingly apathetic.

The unemployment rate suggests, strongly, that it should be otherwise. A high rate of utilization at least with regard to potential “slack” would be a significantly strong draw of people back into the labor force. Yet, going back to the start of 2015 when the unemployment rate dropped to what the FOMC at the time considered “full employment”, just 3.1 million Americans have entered the labor force. Of those, 2.5 million did so all in the six months where many state governments resumed work requirements for food aid. Of the other 24 months, only 654k have participated.

To try to account for what is truly another embarrassing disparity, the FOMC in its last set of economic projections (June 2017) was forced yet again to reduce its estimates for what counts as full employment. The latest lower bound for the central tendency is now 4.5% unemployment, still in June 2017 above the currently calculated unemployment rate (up slightly from May to 4.4%). The reason for this continuous adjustment is the lack of wage acceleration cited above, leaving inflation to meander around on oil price base effects alone.

If the unemployment rate actually applied to the real economy in a meaningful sense, meaning accounting for the participation problem, wages would have years ago accelerated to somewhere around 4% or more in weekly earnings. That would then have pushed up consumer prices, in the aggregate, leading to the Fed’s exit under more normal circumstances. Instead, the FOMC is “raising rates” largely because none of that is happening, having finally come to the conclusion, forced upon them by reality, that it is as likely never going to happen. Read more

As fringe commentators noted at the latest G20 meeting :

“The Washington consensus was spread throughout the world. It was a time when the US, Japanese, British governments and the European Union were in unison about the need to push down wages, deny trade union rights, expand the reach of multinational corporations and create pure freedom for capital and commodities,” Varoufakis said. Read more

In New York, the UST 10yr yield has risen again, now to 2.39% after the non-farm payroll data release.

{kind=link}

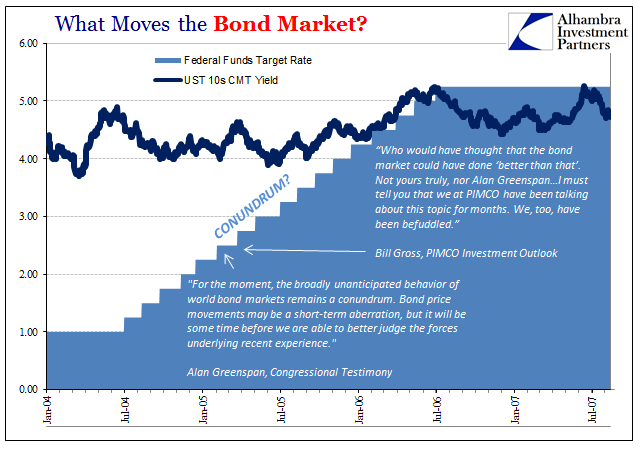

Inflation is at its core another proxy for opportunity, more of a lagging indication of its presence in the real economy and thus the successful dehoarding of money. But in Greenspan’s view, since no one in 1997 had any real idea what money was, the only way to truly measure the monetary condition inside the real economy was through things like inflation – and bonds. His Fed did so they thought correctly up until the 2000’s using a discretionary (not monetary) interest rate policy that was never actually fully revealed.

This largely why in the last fifteen years in particular bond markets have remained largely at odds with mainstream economics and orthodox economists. Through mostly the legend of Greenspan rather than actual monetary understanding, economists came to believe the Fed at the expense of the treasury market. If the maestro was tightening in the mid-2000’s, who was a treasury investor to say otherwise? Read more

Janet Yellen needs to be careful about what she says about Banking sector risks

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.