Banks are chasing cheaper forms of funding.

KPMG’s latest Financial Institutions Performance Survey (FIPS) shows bank funding costs continued the downward trend they’ve been on for the past two years, in the three months to March.

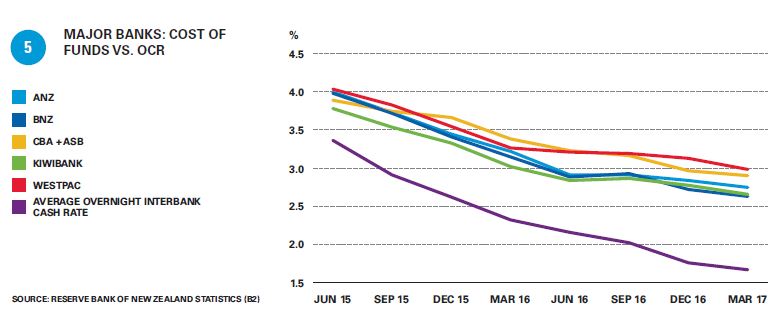

“Interest expense relative to average interest bearing liabilities has contracted by a further 19 bps to 2.79%, an all-time low observed by this survey, as the OCR of 1.75% remains at its lowest point since the RBNZ adopted it in 1999,” KPMG says.

“Across the board, all survey participants recognised lower funding costs ranging from 2 bps to 15 bps.”

KPMG goes on to explain: “ANZ, ASB and BNZ all appeared to switch to cheaper forms of funding.

“ANZ’s interest cost decreased by more than the decrease in interest-bearing liabilities, reflecting a decrease in more expensive sources of funding.

“ASB and BNZ’s interest-bearing liability base rose slightly this quarter while its interest expense declined, thus also showing a switch to cheaper sources of funding…

“Westpac’s interest-bearing liabilities shifted downwards by a sizeable 4.21% this quarter and its interest cost shifted in a similar direction, albeit not with the same magnitude.”

The net interest incomes of all the banks surveyed dipped 3.01% to $2.22 billion, in the quarter.

More broadly, the FIPS has found the banking sector experienced a slight dip in profits in the March quarter, in contrast to the previous quarter when it bounced back from two successive quarters of decreases.

The sector’s net profit after tax decreased 2.85% to $1.20 billion.

KPMG’s Head of Banking and Finance John Kensington says the overall dip in profits is “just a recognition of the competition in the market, the slightly uncertain geopolitical times and a reflection on the NZ economy as a whole: resilient, going well, but not booming.”

The decrease in profits was attributed to a reduction in both net interest income and non-interest income, as impaired asset expense increased.

Operating expenditure control continued to be a strong focus for the sector, with operating expenses reducing $34.11 million.

Gross loans and advances remained relatively stable with only a $4.59 billion (1.19%) increase, the slowest quarterly increase for three years.

Despite slightly larger loan books, interest income for the quarter was down 2.46% ($124.30 million), showing that competition for quality lending is still healthy.

“We’ve seen the industry continue to focus on quality lending, which has led to a decrease in total provisioning levels. This indicates the banks are generally confident in the quality of their loan books at the moment,” Kensington says.

KPMG says the regulatory landscape remains busy with further promulgations and announcements across a range of topics including dashboard reporting, debt to income ratios, outsourcing, dual registration and the Capital Review, all this at a time where there is increased focus on conduct and customer-centricity coming from sector participants and regulators alike.

16 Comments

THANK YOU JENEE !!!!!!!

I have been banging on about how our banks have been super- profitable at depositors expense as their overall cost of capital has declined .

And while strong and stable Banks are welcome , we should not ignore the massive dividend flows paid to the Parent Banks overseas

Every man and his dog had a go at me accusing me of not understanding how bank funding works , and I suspect it was more to do with my views on some issues than what I had actually commented

I think it's in preparation for some loans to start defaulting. They've widened their margins in expectation of some collateral damage.

Couldn't agree more.

I'm not here to argue but I would like a clarification:

"KPMG report shows the banking sector's interest expense relative to average interest-bearing liabilities has contracted to an all-time low"

I understand that as the banks being LESS profitable, not more profitable. Is that not the case ?

If you want to look at both sides, look at Table 1 (NIM).

Overall, the drop in lending rates was greater than the drop in funding rates, thus a drop in NIM - for all banks. Thus why profits are down.

Thanks sferris, so the 1st comment by Boatman and the 11 thumbs up don't really make sense, do they ?

Boatman,

I'm not sure if I'm the man or the dog who had a go at you,but I had good reason. You very recently posted/boasted of your knowledge of bank funding and then baldly asserted that their WACC was under 5%. When challenged,you rapidly backtracked,so I believe I am entitled to question just how deep your knowledge really is.

I am not here to defend the banks and I think it is regrettable that none of the major banks are domestically owned. It is almost inevitable therefore that the parent companies will treat their subsidiaries as cash cows. However,I would like to know just what you consider to be an acceptable level of return for our banks. Your detailed knowledge should allow you to answer that.

I too was privy to that thread.

Boatman had a very interesting way of calculating said WACC, also I recall.

You ask a good question, in that what an acceptable level of return is for banks.

Everyone is far to quick to moan about nominal returns, but often have little understanding of the dynamics of the institutions.

... the world's biggest hedge fund sounded an identical end-of-an-era warning ( to Citibank's). Central bankers were now reducing the supply of that intoxicating liquidity that for so long has pushed asset prices higher, and driven interest rates lower....'... that should say something to you about the risk that might mean because we've never lived with it before.'...we now find ourselves "at the end of that nine-year era of continuous pressings down on interest rates and pushing out of money that created the liquidity-fuelled moves in the economies and markets...the odds of a market crash are rising as the global economic cycle slows - the auto, commodity, industrial and retail sectors are all showing signs of stress - at a time time when strong US jobs growth leaves the Fed with no option but to reduce its monetary stimulus. "In every previous such down cycle for the last ten years, central banks have responded by printing money. But this time, they are doing the reverse, which must, one thinks, exacerbate the trend."....Investors, however, are failing to heed flashing warning signs..."to my mind, we have finally globally hit the peak of the cycle. A peak we hit in 1979, 1989, 1999, 2008 and now. Can you see it?"

http://www.afr.com/opinion/columnists/jamie-dimon-ray-dalio-both-fret-a…

I'm a bit confused,

- cost of source of bank funding has decreased

- revenue to banks from interest earned has also decreased

Which has decreased more ? Have the banks become more profitable or less profitable Jenee ?

It's in the graph. Cost of funding has decreased more than the revenue to banks from interest.

I'm really not sure it's in the graph. I think the graph only shows decreasing cost of funds, not revenue from interest

All I see are pathetic term deposit rates being offered.

And a whole lot of recently instigated unfavourable "terms and conditions".

Yes ocelot, and funny how the RBNZ aren't moaning about the banks moves, RBNZ lower with banks higher could save some banks in the near future and the RBNZ are part of this, didnt American do a similar thing after the GFC,

I think there's a fair bit of confusion in those graphs - a banks cost of funds is what it pays over wholesale rates, and as the graph clearly show, that spread is widening

Confirm what 's being paid on the O/N funding value claimed here.

Please note ANZ publicly offers10 bps on O/N depo.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.