The prevalence of interest-only lending has been in the spotlight in 2017 - largely due to the Reserve Bank honing in on its risks.

The initial focus was on residential property 'investors' and their attraction to it to keep current cash flows minimised. They need to do that if their implied goal is capital gain - operating costs (mortgage payments, insurance, rates, maintenance, etc) may be covered by rents, but the real payoff for them comes if and when they sell what they hope has been an asset that rose in value, thereby generating tax-free gains.

But interest-only lending becomes a financial stability risk "if everyone does it", the market turns and values decline.

With one third of all houses now rented (621,400 such properties as at December 2017), the numbers are significant.

In fact, residential property investors have borrowed $68.5 bln and their obligations involve substantial leverage.

On average, each rented property has $110,200 in debt. That is 30.4% of the national lower quartile house price in November. That compares with owner-occupied properties (of which there are 1,164,600 in New Zealand) who have an average of $147,700 in debt per property, which in turn is 27.4% of the national median house price.

These averages don't reveal the levels recent investors or recent house buyers are committing to. (RBNZ data series C32 give the gross amounts involved but not the numbers of loans that supports, so per-borrower data can't be calculated.)

Despite that higher level of average borrowing, borrowers who live in their own homes are much more likely to be paying down some principal with each mortgage payment. In fact, 84.6% are, building equity and financial resilience.

Residential property investors have the majority of interest only debt in the housing sector - $28.7 bln compared with $25.9 bln for owner-occupiers.

| RBNZ S32 | of which | ||||

| as at November 2017 | Total | interest only |

Revolving credit |

Principal & Interest |

Other |

| $ bln | % | % | % | % | |

| Owner-occupied housing | 172.006 | 15.1% | 6.2% | 78.4% | 0.3% |

| Residential property investor | 68.475 | 42.0% | 3.7% | 54.3% | 0.1% |

| Business | 103.756 | 37.4% | 30.4% | 29.2% | 3.1% |

| Agricultural | 60.379 | 63.6% | 23.7% | 12.4% | 0.3% |

| ----------- | ----------- | ----------- | ----------- | ----------- | |

| Subtotal | $404.616 | 32.6% | 14.6% | 51.8% | 1.0% |

| Personal loans | 11.105 | n.a. | n.a. | n.a. | n.a. |

| Financial institutions | 8.445 | 12.6% | 34.2% | 34.2% | 19.0% |

| Other | 2.665 | 23.1% | 19.8% | 25.1% | 32.0% |

| ======== | |||||

| Total all lending | $426.831 | ||||

But as this table clearly shows, borrowers for commercial purposes also like interest-only arrangements. Some of the lending classified 'business' will also be property-related, both by property developers, and by commercial property investment companies. Most business overdraft arrangements are also interest-only.

Rural borrowers have special seasonal working capital needs - often based on overdraft arrangements as well - that also lend themselves to interest-only.

All up, more than $133 bln of bank lending is on an interest-only basis involving no progressive principal repayment obligations (other than when the loan terminates). While this is not a high proportion in terms of the total amounts borrowed in the New Zealand banking system, it does represent a little under half the nation's annual GDP.

124 Comments

What? Agriculture principal and interest loans 12.4%?

Shocked.

42% interest only loans (investor category) is a cancer in the absence of capital gains. With rental yields as low as they are, the expectation of year after year capital gains is obviously huge. Its a symptom of the age of self entitlement.

I think the meaning of "as safe as houses" might soon be re-written.

A house of cards. Quite a few investors here have advised they are on interest only, and indeed if you didn't go interest only to maximise your leverage you were a fool. There's not even a pretense at building equity via principal repayments. It's just an out and out gamble on future capital gains. Makes you look clever on the way up the bubble, different story on the other side. If I read the numbers right about 40% of the residential market on interest only (?). Anyway, a big mess in the making.

We're so arrogant that we never learn.

All my loans are interest only. At the same time I have repaid over $400'000 of loans in the last 2 years. I just like to be in control of which loans I repay and how much I repay

All my loans are interest only. At the same time I have repaid over $400'000 of loans in the last 2 years. I just like to be in control of which loans I repay and how much I repay

Oh let me guess. You repay principal from your winnings on the pokies that you've accumulated from your "method."

Either that....or your wheeling out a weak attempt at a troll.

Yvil could have sold a property in that time. All my loans are interest only however I will sometimes pay off some capital in a lump sum when renewal time comes around. The sensible folk will have large credit facilities and channel money that would have gone into capital payments into savings and other non property investments. When the time comes to pay capital there will be a reservoir of funds to manage this comfortably.

I don't know why everyone seems to think people are maxed out, sailing close to the wind, in these low interest times. No, we are building up reserves and strengthening our positions while the good times continue.

ZS I hope you are representative of the majority. The only Property Investors I know, are negatively geared, topping up from their wages and maxed out debt wise. Their strategies are all the same, to sell one or two of their properties if they hit a road block or some other cash flow issue. But i'm 37, and they are all younger than me, so i'm guessing it will be the younger property investors, who have less experience and also less years to build equity under their belts who might struggle. I'm sure plenty of more seasoned investors have already taken profits and have a healthy buffer for the slow cycle stage approaching.

I also worry somewhat about amateur investors (including mom and pop investors) who have withdrawn equity to buy just one or two extra properties and also spent up on new cars, boats, holidays and lifestyle stuff.

I think a lot of negatively geared people are couples who both work. With the "mom and pop" investors they probably both work as well and have a mortgage free house. Their position is not as precarious as you might think with the negative gearing costs only eating into a small portion of their income. Like $300 a week while they are earning $2,000 -3,000 a week.

ZS, I am sure there are many in that situation, and hopefully more than not. As much as I would love to see housing return to affordability measures and a more equal distribution of wealth, I don't want to see an economic catastrophe sized housing crash! However, I remain concerned about that happening...based on the huge debt to income ratio of households in NZ (168%), which suggests that people are much more precariously placed than you might be suggesting. That level of debt in a low interest rate environment is not necessarily a problem, but if there is any tightening, then it will be a huge problem. The property investors I know are certainly couples with decent joint income, one couple is probably earning even more than $3000 a week combined. However, they owe more than $4 million, so their DTI is scary, they are very spendy and neither of their jobs are particularly secure. They are very much in "boom economy" jobs, if the economy slows, one of them would likely be looking for job.

Well said gingerninja

Yes ZS, I did sell a property and decided to repay some of my mortgages instead of splashing out on a new SUV. I also repay some of my loans when they come up for renewal (all are on short term fixed)

J C, I really don't understand your comment. Can you please explain what you mean by "winning at the pokies" and "troll" Thanks

Yvil, did you sell one of your houses?

Each to their own. To find oneself up to the gills with interest only loans at this stage of the credit cycle reads good on paper but the nuts and bolts of it are something else!

Interest only loans are just another punch bowl. Debt is debt and the bank can shift the land beneath you.

Yes I did, RP and rather than Splash out on a new expensive SUV, I think it's a good time now to further reduce debt. That made up the bulk of said repayment, I also repay 25-50k pa on loans that come up for renewal.

The point I was trying to make is that even though I have interest only loans, I do repay them (on my own terms)

In banking history, banks have mostly only lent riskier loans and products like "interest only" to their very best customers. Yvil sounds like a good example of this kind of borrower... someone who pays down debt on an informed schedule, according to what best optimises his finances. These types of debt have never crashed economies. It is the debt that cannot be paid, that was given to customers who are not likely or able to pay the debt back in anything but a hot housing market + loose lending environment, let alone an orderly informed schedule... that causes the painful crashes. It's the irrational exuberance that is dangerous, and sadly, we have seen that more recently in NZ, so I do think the risks are there.

Interest only loans in themselves can be very healthy and useful in a healthy/normal housing market. However, the percentage of interest only loans and the current household debt to income ratio in NZ are a concern, especially with low wage inflation. It should be a concern to anyone with half a brain regardless of whether you are a property millionaire, or a youngster on low wages, locked out of the housing market.

What I hope happens is that those who are over leveraged, see the writing on the wall and sell a property or two in an orderly un-paniked manner and reduce their overall debt, so that they can weather any tightening or credit crunch environment. If it's true that investors have been holding empty properties waiting for CG, then releasing those to the market, would also provide the benefit of helping to address the housing shortage.

What we do not want to see is the housing bubble burst spectacularly, government bailing out Ozzie banks, austerity, recession, unemployment and a generation of boomers losing their means to fund their retirement. We want a soft landing. This housing bubble looks to be deflating slowly at the moment, and that is exactly what is best for NZ. Housing affordability can be achieved more easily this way but it will take longer.

Nice one Mr Ninja.

Very, very well said Gingerninja, amen to that

1/3 being interest only is a very high proportion in my book.

I don't think it should be allowed for property purchases.

If they were completely banned, property prices would drop. Things would adjust. And over time the banks would become much more secure unless they dream up some other way to loosen their standards like increasing further, the term of the loans.

Interest only mortgages in residential property should be a tool only used to assist people who find themselves in hardship, to negate losing the house all together i.e. owner occupier.

Correct me if i'm wrong but am sure once upon a time interest only loans were classed as "non performing"

Not anymore :-)

And they should be short term. 6 months (none of this 5 year interest only contracts), and then one would have to reapply for an extension, and maybe limit the amount of extensions allowed for a property.

Interest only is also valid for bridging loans, but again should be set to a maximum term of 6 months.

"If they were completely banned, property prices would drop"

If we banned all lending and made everyone pay cash they would fall even more.

Yep, great idea Ralph. Homes might be affordable then.

Maybe our financial resilience would be much stronger if we didn't have to borrow so much for a home.

"We might need a banking system, we don't need banks"

A number of issues for property investors on interest only payments.

Generally an interest only arrangement indicates that the property investor is pushing cash flow limits with little fat.

When things get tight (increase in interest rates, personal redundancy or sickness, poor paying / redundant tenant, etc.,) there is little room to manoeuvre in the short term (i.e. the ability to reduce mortgage payments by moving from interest and principal to interest only).

In the medium term, the inability to meet interest only payments for above reasons will mean selling on a flat or most likely a falling market. Not only not the capital gain expected, but possibly penalty payments.

A high risk investment strategy that is just getting a little more risker with potential increase in interest rates and flat markets at best over the medium term.

Haha, we'll said Ralph

So $110,200 @ 6% in only = $127 per week. At 15 year mortgage it becomes $214 per week. Closing in on double and without a rate rise . The extra not even tax deductible. The capital to be repaid not even covering the declining values now upon us, so in effect a double whammy. Looking good for those holding back I'd say.

How do you think a BNZ total money loan would go.

I have yet to hear back from that esteemed organisation to the question I posed to them before Chrissy - "Why does P+I become 'term reducing' once the P has to start to be repaid, even if the I is covered by Offsetting?"

I'd assume that if they had a ready answer, I would have it by now.....( The Bank insist that the scheduled minimum amount of P+I is due after the 5 years Interest-Only only period finishes, even if the interest is totally or partially offset by Other Balances. I don't reckon it is! IMO Interest should charged only on the amount that isn't Offset and the Principal to be repaid is the amount - the correct amount - of the 'minimum' scheduled eg : Principal Outstanding /1044 payments of there is still 20 years to go etc)

Non performing loan status indeed.Very likely that Aussie policy change of stopping interest only loans being rolled over will happen here as well, if it is not already.

This will be an additional straw on top of the loss fencing, 40% equity requirement, extended tax flipper window, overseas ownership ban, changes in education/immigration scam, Chinese capital controls, and incoming changes to stop slum lording houses. That's a lot of changes in anyone's book.

How many more straws can the ponzi take?

... leemee see if I've read this right : The RBNZ ... the silly saps who pushed the OCR down to record low levels , and kept it there ... despite a stonkeringly exuberant housing market soaring monthly to nose bleed levels and beyond ... are now concerned that the market has pigged out on interest-only loans ...

Is that correct ? .... oh lawdy lawdy .... excuse me whilst I change the Gummy nappies ... I just larfed so hard I wet myself thoroughly ... saturated with the irony of it all .... haaaarrrrr deeeee harrrrrrrrrrrrr ....

Wee can always Depend on ya for a larf, GBH....

They pushed interest rates down to save over leveraged farmers (reduced debt repayments, increased income from lower NZ dollar).

Mr Billy English extended his influence to ensure that happened (plenty of "meetings" between him and Graeme Wheeler) around the time rates were subdued even in the face of house prices taking off.

... meebee our dairy farmers are " too big to fail " .... kind of like the US mega banks were during the GFC ... so they've become a taxpayer protected species ... well done , the Gnats !

Pity they didn't put quite so much effort into protecting the environment ... keeping our freshwaterways and lakes clean ... Sigh !

Interest only mortgages have effectively been banned in the UK. Only the very wealthy can get them.

I strongly believe the banks should be capped on the percentage of their mortgage book that is interest only- around 10 or 15%.

UK ? You’re talking about the country that WallSt uses because of its weaker financial market regulations

They have no problem allowing the poor to borrow

PayDay loan capital

I find those percentages astounding. A cap is needed.

Loans worth almost half NZs GDP have the highly indebted, paying only interest suddenly required to make principal payments ?

I’d call that a catalyst for changing times in property. The present relative quiet merely awaiting the crescendo

Gummy Bear is right

What cretinism at the RB

In case you missed it, here's how the Australians are handling the payments increase from interest only to P&I.

The founder of one of the country's biggest property investment clubs says its 20,000 investors can't afford their mortgage repayments after the banks shifted them from interest-only loans to principal-and-interest mortgages earlier than they expected.

"How would you manage if your bank told you you had to pay 45 per cent more per month on your mortgage?" Kevin Young, founder of Queensland's Property Club (previously called The Investors Club) told The Australian Financial Review.

http://www.afr.com/real-estate/residential/property-club-investors-stun…

The payment shock of an interest only mortgage reverting to a P&I mortgage reminds me of the teaser rate mortgage products in the US in the 2003-2006 period.

How many interest only loan borrowers are assuming that they can still roll over into a new interest only loan or extend the maturity of an interest only mortgage? How many interest only loan borrowers are even financially prepared to go onto P&I terms? For those not consciously aware of this risk, the first indication that many non professional property investors get may be the letter from the bank telling them that their loan payments are about to go P&I in the following month ...

Out of Australia -

A third of customers with interest-only mortgages may not properly understand the type of loan they have taken out, which could put many in "substantial" stress when the time comes to pay their debt, UBS analysts warn.

"We are concerned that it is likely that approximately one third of borrowers who have taken out an interest-only mortgage have little understanding of the product or that their repayments will jump by between 30 and 60 per cent at the end of the interest-only period (depending on the residual term)," he said.

"While these loans are well secured, we believe many borrowers may face substantial stress as interest rates rise or when they revert to principal and interest."

http://www.smh.com.au/business/banking-and-finance/one-in-three-dont-un…

Yes, not a bad comparison with the US teaser rates. I suspect very few borrowers (investors or occupiers) have made any real provision for what will happen when they go to P & I, they had assumed they would roll over or sell prior. I suspect some owner occupiers were so desperate to get into the market they got maximum leverage via interest only and are pretty much just hoping for the best.

Mum and dad investors 'fleeing' property, financier says

http://www.nzherald.co.nz/index.cfm?objectid=11973924

Would be interesting to know how many of these investors are selling their investment properties due to loans going from interest only to P&I and higher debt service payments which could be turning positive cashflow properties into negative cashflow properties ...

From a mortgage broker in October 2017 - many banks will do a full credit reassessment at the end of interest only periods. The test rates are 7-8% - they want to ensure that borrowers can meet debt service payments at those level of interest rates.

"I see the biggest concern for property investors at the moment being interest only periods coming to an end. If you have looked to extend your interest only period recently then chances are you know what I’m talking about. A lot of the banks will now do a full credit assessment at the time of your fixed rate roll-over and they will do this assessment at their test rate, on principle and interest over 25 years and using only 75% of your rental income. If somehow you pass that test, only then will they extend your interest only period. If not, then be prepared for an increase in your repayments"

As in the rural thread, if you pay principal you are generally using profit, which then attracts tax. Double whammy.

Yeah but isn’t the point of investing to make a profit? These people who think they are being clever avoiding tax are also avoiding making a profit. Seems stupid. It’s worked in a low interest rate/high capital gains environment over the last 20 years but there is every sign that is coming to an end.

Yeah but isn’t the point of investing to make a profit? These people who think they are being clever avoiding tax are also avoiding making a profit. Seems stupid. It’s worked in a low interest rate/high capital gains environment over the last 20 years but there is every sign that is coming to an end.

Yes, but you also have to consider that the system is pretty much fully geared to support continued growth in asset prices. It's a planned market without any consideration of the consequences.

One cannot say this happened under National's watch. It seems they watched very little except maybe tv adverts.

Not fair.

They kept a good eye on.......

Themselves in the mirror, and they liked what they saw.

"There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved."

- Ludwig von Mises

gingerninja, nice! - a very fitting quote ;-)

Just because a loan is interest only does not mean that principal is not being repaid. Suggest it would be common in the sheep and beef sector where the bulk of the income is received in the late summer/autumn for a lump principal repayment to be made annually , rather than monthly payments that go straight onto the OD in the period of the year where there is no income. A similar logic applies to the use of revolving credit.

True, true.

I'm sure everyone has forgotten that the 60% of (residential) borrowers work on the same model as a beef/sheep farmer; a pittance of cashflow throughout the year, followed by a lump sum payment.

Stunned we really are living in a fantasy world !!!!

An ex motelier told me 90% of Christchurch's motels are owned by Chinese.

excerpt taken from a Stuff article this morning. Note capital gains is at the forefront of a Landlords mind. Just goes to show the short term speculative element in today's housing. If Landlords were in it for the long haul (and yield) then the five year brightline and capital gains would be implemented - largely unopposed by Landlords.

Landlords rank housing policies (in order of favorability)

· Relaxation of current LVR restriction

· Longer fixed-term tenancies

· Healthy Homes Guarantee Act

· Extension of Bright Line Test

· Limiting rent increases to once a year

· Removal of negative gearing

· Ring-fencing tax losses

· Removal of 42-day notice to terminate

· Debt-to-income restriction

· Capital gains tax

https://www.stuff.co.nz/business/100461932/landlords-unconcerned-about-…

I think the speculators biggest enemy right now is not our Government but tomorrow's uncontrollable market forces.

I will repeat my comment here where i should have placed it. "I am the first to admit that matters of finance are not a subject that has interested me much. Thus I am a simpleton in such matters. However, to my innocent mind these figures suggest to me that New Zealand has created a situation where we as a nation can no longer afford our own housing market." Furthermore, it seems our farms are not far behind. This cannot end well.

It can end very well. Rapid sell of, of no preforming rental properties causing price reduction enabling our young and lower income families to purchase a home and have the security it provides. A few wealthy investors and multiple home owners take wealth cut.

This may well happen however the journey will not be without serious pain to the overall economy $68bn advanced to current residential investors the banks will not be very forth coming to the young and low income families after such an event.

I think NZ's housing market is now one of those situations of whether its best to die by a thousand cuts, or the swing of one large axe.

Macro-prodentual policies appear to be the scalpels used to assist the death by a thousand cuts, while the axe always remains and realistic threat.

I have had interest only loans for 35 years - rule 101 for investing - use other peoples money, use built up capital to improve your properties worth by renovating adding value, the debt to property value reduces makes you and the bank happy and now for the most powerful quote ever about property ............

I am the basis of all wealth, the heritage of the wise, the thrifty and the prudent.

I am the poor person’s joy and comfort, the rich person’s prize, the right hand of capital, the silent partner of thousands of successful people.

I am the solace of the widow, the comfort of old age, the cornerstone of security against misfortune and want. I am handed down through generations as a possession of great value.

I am the choicest fruit of labour, the safest collateral and yet I am humble. I stand before every person bidding them to know me for what I am and asking them to possess me.

I am quietly growing in value through countless days. Though I might seem dormant, my worth increases, never failing, never ceasing. Time is my aid and the ever increasing population adds to my gain. I defy fire and the elements, for they cannot destroy me.

My possessors learn to believe in me and invariably they become envied by those who have passed me by. While all other things wither and decay, I alone survive. The centuries find me younger, always increasing in strength.

Thanks so much for pointing out why it is we need to have extremely strong laws around investing in residential property. Without restraints we run the risk of a rentier class culture v a renting class one. One small group holding the assets, the rest having to rent it off them, oh wait.

Residential property should have all and any laws around it starting with the premise that it is firstly and foremostly there for people to make homes in, not for a few to make themselves rich.

Sounds like you want some sort of socialist utopia. There are plenty of places around NZ where houses are affordable. Hamilton and its surrounding area for example. Just because Auckland is expensive doesn't mean we should destroy the system, a system that largely works well.

How is that a socialist utopia?

Egalitarianism isn't socialist; it's just as much a pillar of capitalism.

Ironically though, all the so-called capitalists aren't interested in egalitarianism at all.

A thought experiment - if we were able to execute a wealth and knowledge reset/normalisation (all other factors ceterus paribus), who would come out on top?

Do you genuinely believe you could be in the top 5% after 25 years?

Or, do you honestly believe that you could even attain the same percentile rank that you are now?

I'll be the first to admit that I don't think I could.

This is exactly why the wealthier, despite being 'capitalists' loathe the idea of equality. Given this very thought experiment, the majority would come to the same conclusion as I; It would be very difficult for me to attain the same position given perfect competition.

Ironically whenever we talk of instituting laws around property investment, there is always the call to arms against socialism. Socialism is a shitty idea in theory and an even crappier idea in practice. However, the landed elite benefit from many aspects of it greatly.

Consequently I don't see any of you 'capitalists' advocating for the removal of any protections afforded to land owners.

All this political mud slinging is ridiculous. There has been zero socialism and zero capitalism in NZ or any other western-culture nation for that matter in any of recent history. If we had capitalism not a single bank would have been bailed out, and if we had socialism no one would be allowed to own property at all!!!

There is actually very little pure political ideology that can helpfully inform economics whatsoever and the constant reference to it in these pages is futile and unhelpful.

Psychology and understanding of human nature is much more useful. For instance, human beings have THROUGHOUT HISTORY proven that they can easily fall victim to shortsightedness, greed, vanity and therefore bias. This includes leaders, politicians, religious people, rich people, poor people and everyone in between. We need unbiased government legislation to protect us from ourselves. When we have biased or corrupt governments (which in my opinion, we have had in many western nations but have been told off for saying so here) then the problems of human nature become compounded and we end up in very tricky economic positions. Rapidly declining wealth equality is NOT EVER a good idea for any society. I find it very depressing when certain commenters on here make trite comments about jealousy and sour grapes because they own many properties and others don't. These commenters completely ignore the lesson of history, that wealth inequality invariably leads to degradation across all society, not just those whose wealth has been curtailed.

Capitalism requires legislation to provide the FAIRNESS to facilitate everyone having a fair crack of the whip. However, that is not what we have. Very few currently wealthy individuals can claim that their wealth is fairly achieved and a younger persons wealth is fairly absent. Structural factors in politics, legislation etc have set us up for the current trajectory of growing wealth inequality, and all that is brewing is resentment. If you think growing resentment between the richer and the poorer, the older and the younger, will end well, and will not be EVERYONE'S problem then you are plain ignorant.

You must have far too much time on your hands to feel the need to rephrase every comment.

Eh?

My point was exactly that we think of ideology as capitalism or socialism.

The naive misunderstanding and the need to think of societal ideology as binary is the issue.

Nymad my reply was more to Zach than you Nymad. You weren't political mud slinging. But there has been a lot of political mud slinging lately. And it's frustrating, when it lacks factual basis.

As for having too much time on my hands, I have a 9 and 5 year old on holidays, so just starved of adult conversation atm ;-)

My apologies, Ginger.

As a reply to my comment, I took it the wrong way.

A 9 and 5 year old - surely you don't tire of the "but why" questions?

Perhaps ZS and the political mud slingers could learn a bit from such a pursuit of curiosity :)

DP

The point I was trying to make, probably poorly, was that PocketAces seemed to want a utopia where anyone could buy a house anywhere. I was pointing out that New Zealand still offers that which she dreams of.

I think I probably would come out in the top 5% after 25 years. Not sure this thought experiment is of much value though as we and our social and cultural milieu are products of a very long historical process. It's like saying, if I removed part of you and then made you start again I bet you wouldn't be in the top 5%. I don't consider myself to be purely individual. I am the refection and the product of a unique people in a certain time and place. My history is everything that I am and the secret of my success.

ZS,

"I am the refection and the product of a unique people in a certain time and place. My history is everything that I am and the secret of my success."

Thank you for proving my point regarding egalitarianism.

You don't want equality at all.

You agree that so much of your wealth is derived from hereditary factors and luck - Don't ever mistake that as a product of capitalism. And, because of that I highly doubt that you would attain the same position as you are in right now. Actually, no chance. Likewise, I would give myself a very slim chance of attaining the same percentile rank or better.

A true capitalist would jump at the chance to have a global reset.

It's also hardly a "socialist utopia" merely describing what NZ has done to encourage affordable housing in the past, to the benefit of many now.

Is there such a creature as a true capitalist? Isn't that a Marxist term?

How can we have egalitarianism or a level playing field when there are different levels of intelligence, beauty, physical fitness, energy, mental stability and so on? These things are largely inheritable as well.

I don't want equality. Sounds like wanting to be a sheep in a field of sheep.

I like things just the way they are.

So it wouldn't be a bad thing for young Kiwis to receive the same benefits that you did in your day from wider NZ society then, from the sounds of it. Not equality of outcome, but a darn good leg up.

You are just a walking contradiction, aren't ya ZS.

It seems that every time you post a comment relating to sociology, economics, history, etc, you are brutally shot down for your lack of understanding on the subject on which you are referencing.

Thanks nymad for proving my point that we are not all equal and never can be. I'm not very handsome, not very tall, not very athletic, not even very smart, have a very low EQ, but I am in the top 10% economically. I feel this is good compensation for all these deficiencies.

To make up for my many deficiencies I just hope I can influence people toward a better world society.

ZS It's NOT about everyone being the same. It's about EQUALITY OF OPPORTUNITY not equality of everything.

Capitalism prescribes equality of opportunity. We do not and have not had that. This is what you are ignoring and this is the most important issue.

Equality isn't about being the same, it is valuing each other as equals no matter those levels of differences.

Love thy neighbour as thyself rather than exploiting them for as much personal gain as possible.

ZS,

It's the use of terms like "socialist utopia" and "evil capitalist's" and cheap insults regarding the political spectrum that I feel are detracting from any useful debate about the social and economic problems facing NZ.

I agree that we can't wipe the slate clean and somehow start again with an entirely equal society. To achieve that would require an unholy blood bath and it's unlikely to be possible or sustainable. However, my point is that human beings are inclined to short sightedness in serving what we perceive are our own self interests.

So as a thought experiment, using an extreme example, some clever geek invents a time machine, goes 10 years into the future and sees that the wealth inequality trajectory we are currently on, eventuates in a bloody revolution, where the disenfranchised youth overthrow the wealthy and powerful in a violent rampage. The geek returns and let us all know.... and then if we pretend that it's entirely up to the property asset hoarding group, to fix the current housing affordability crisis (so we are excluding any government mass building scheme or foreign investors etc), and that in order to avoid this fate, it is suggested that every single property owner who has more than 2 properties,is required to release them for sale back to the market over a 5 year period, and in doing so would save NZ from the awful fate.... would the asset holding group do this, or would they rather enjoy their privilege for another 10 years, watch the growing poverty and resentment around them and then just suffer the violence and revolution in the future?

Because irrelevant of an extreme bloody example...NOTHING good has ever come of growing wealth inequality.Nothing good has ever come of a system that perpetually privileges those with assets over those that don't. It always leads to some collapse and ensuing period of "dark age" of chaos. If there was actually a trickle down effect then it would be different but over the last 10 years in particular, this has not happened.

Wealth distributed more evenly is better for GDP, better for productivity, better for health stats, happiness stats and society in general. It has been said before in these comments, but the existence of a thriving middle class has proven to be crucial to a healthy functioning society and economy. There has to be social and economic mobility. The current system is crippling the middle classes and any possibility of social mobility.

Even without imagining that the current wealth inequality trajectory leading to something bloody and terrible, can we not agree that the path we are currently on will worsen society for everyone in some degree or another?

How short sighted are the wealthy? Why is that not a concern of the wealthy?

NOTHING good has ever come of growing wealth inequality.

That depends where you start from. You can have too much equality as well as too much inequality. If you start from a position where everybody has exactly the same, and introduce a new system whereby people will be rewarded in proportion to how hard and intelligently they work to produce goods and services that others want - then it is likely both that wealth inequality will grow, and also that improvements in living standards will result.

Nothing good has ever come of a system that perpetually privileges those with assets over those that don't.

Yes, being rich is better than being poor. Where would be the incentive to study, to work, to look for better ways of doing things, to create things that other people want and need, if it wasn't?

It is a matter of degree. Do we wish to become similar to Mexico and other nations with large inequalities in wealth. Wealth that makes them so prone to ransom or violence that they must spend vast percentages of it on attempts to keep it.

It's the mechanism that is usually behind the growing wealth inequality that is often the source of the problem. The current growth of wealth inequality is an excellent example.

Most of those who currently have the benefit of owning assets, particularly property assets are enjoying the benefits of what previous generations did to encourage equality of opportunity, and other factors such as demographics etc. Most of those who are currently holding the wealth in NZ are NOT necessarily more intelligent, talented, beautiful etc etc than those who do not have wealth via property assets. It is because the trend to protect equality of opportunity has been utterly neglected, and in some cases reversed in modern politics and culture.

Being rich is not necessarily better than being poor, when the poor organise and revolt, ask a headless French aristocrat or the Romanov family. The rich can suffer at the hands of an angry mob the same as anyone else. What is best for society is equality of opportunity. Not that every one is the same and owns the same, some will always have more than others, but that should be the product of talent and labour, not luck of birth. It's not quite as simple as that either, but at the very least it behoves governments to level the playing field as fairly and realistically as possible so that everyone has a fair, equal crack at the whip. If you choose to be lazy and lack aspiration for betterment, then that is your choice, but if you wish to work hard then you ought to be able to access the rewards of hard work that the previous generations enjoyed... ie home ownership and security in your old age. At the moment, wealth is a rigged game and that is the story than never ends well.

What data are you using for your statements about the current growth of wealth inequality in New Zealand?

Jesus? Really? Growing wealth inequality in NZ has been so well documented with so much data and so well discussed that it is beyond doubt, and you can easily google "wealth inequality New Zealand" and find page upon page of easily accessible data but sure, rather than acknowledge the problem, ask me for data.

But yes, Credit Suisse Global Wealth Report 2017, Oxfam International Report 2017, even our own IRD showed that "The Inland Revenue's high-wealth individuals unit shows the number of the wealthiest Kiwis jumped by almost 20 per cent between October 2015 and June 2016, from 212 people worth more than $50 million to 252" (and even then it is well documented that the richest pay disproportionately less tax and I can provide the evidence for that also if you are too lazy to do your own research). Statistics NZ found in 2016 in its survey of household wealth, that the country's richest individuals - those in the top 10 percent - held 60 percent of all wealth by the end of July 2015. Between 2003 and 2010, those individuals had held 55 percent. These are all statistics going in the wrong direction.

I could go on and on. But that suits you doesn't it? Keep challenging the issue exists then you never have to change anything that doesn't serve your own beliefs and interests?

"In New Zealand, income (and probably wealth) was being shared out more and more evenly from the 1950s up until the 1980s – but for the next two decades we had the developed world’s biggest increase in income inequality.Wealth and New Zealand - Great Divergence – but for the next two decades we had the developed world’s biggest increase in income inequality. in that time, the average income of someone in the richest 1% has doubled, from just under $200,000 to nearly $400,000 (adjusting for inflation). In contrast, the average disposable income for someone in the poorest 10% is only slightly higher than it was in the 1980s. (More details can be found in Wealth and New Zealand, published by BWB.) That means many New Zealanders struggle to pay their bills and lead a decent life."

http://www.inequality.org.nz/understand/

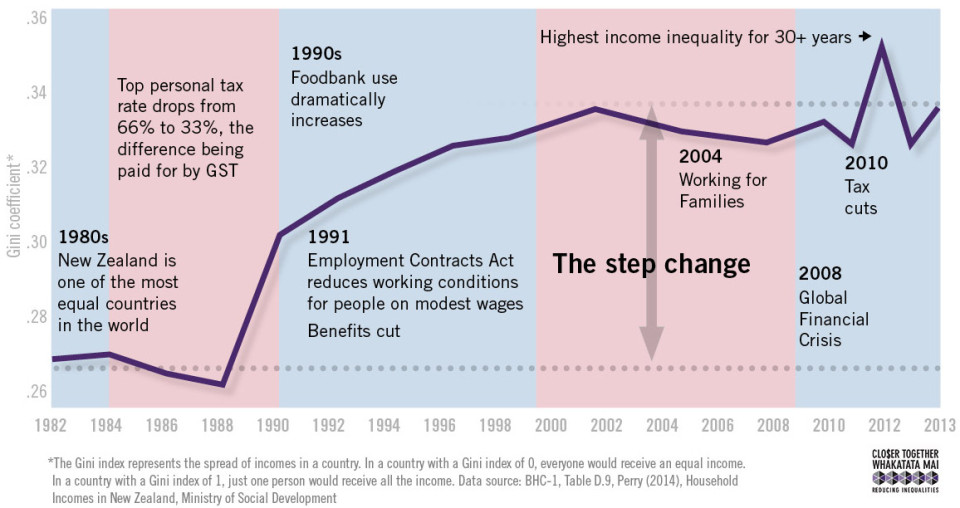

Or here is a graph;

http://closertogether.org.nz/wp-content/uploads/NZ-annotated-gini-chart…

{kind=link}

dp, sorry

"that should be the product of talent and labour, not luck of birth"

But of course talent and labour (the inherited drive/motivation/dna) are derived from luck of birth.

Free will is an illusion.

I'll have you know I worked damn hard to be born into the right circumstances to have a stable family life in a good location, receive a good free primary education and low cost tertiary education (not like those lazy young folk now), and get into a lucrative career. Damn hard! And I was very careful to choose parents and relations from whom I could inherit reasonably well!

None of this lollygagging around being lazy enough to be born to a poor family living in a damp house in a bad suburb! Or walking to school without breakfast or shoes! Not for me, no sir-ee!

Being born to a poor family and walking to school without shoes is not an example of poverty of opportunity. If you were able to grow up, get a job and you could afford to buy a house, or indeed multiple houses and be mortgage free by retirement. It is the fact that children born now in poverty, will be trapped there, that is the problem. Social mobility is declining.

Rastus, I think you will find that there are significant environmental factors that contribute to talent and commitment to labour. Almost no one is born without drive. Our species wouldn't exist if people were born without drive. And talent is a combination of inherited traits and learned skills. Yes some are born with more innate skills than others, but most people are born with enough traits to be able to learn a skill of value. And equality of opportunity also insures that the human species as a whole can benefit from the talent wherever in the social hierarchy it pops up. If the best mind in science, the mind that can cure cancer, was born in to poverty and due to social immobility, is never able to get to a career in science, we are all the poorer.

1. I suggest to you that nobody set out to grow inequality of wealth in NZ. The last 100 years is probably testament to the reverse.

2. Vast amounts of wealth redistribution does take place in NZ. What we call the 'rich' are in fact paying the lion's share of the tax bill.

3. Life has no guarantees of outcome and 'stuff' happens to everyone, some of it quite impactful on material quality of life. Nobody owes you or me any particular outcome.

1. I suggest to you that nobody set out to grow inequality of wealth in NZ. The last 100 years is probably testament to the reverse.

Indeed, the last hundred years shows quite the record of efforts to provide greater opportunity to many more in society, and reduce the monopolisation of capital and land to do so, and to get more people secure in their own capital of a home or farm.

And then a few decades at the end sort of abandoning a fair amount of that and reverting a bit to earlier models.

I am sure a measure of the change was due to 'western' elites awareness that communism was no longer such a threat to their power.

And the introduction of neo liberalism.

I think there is general agreement both National and Labour, in international terms, are both left leaning in political terms.

Yeah, definitely. An example of that was National's election promise to increase Working For Families, Accommodation Supplements etc., things we'd be much better off without (assuming other reasonable policies instead).

Doesn't mean we haven't seen economic liberalisation (ironically, by Labour) coupled with an abandonment of some of the social/housing policies of yore that served to create such an well-capitalised population, with a mixture of intended and unintended consequences.

2. No they're not, the truly wealthy find ways not to pay their share, you only have to look at the incongruous spikes that happen at the upper end of each tax band to see that. http://www.ird.govt.nz/aboutir/external-stats/revenue-refunds/income-di…

Those suspicious looking peaks at exactly the rate of a new tax band would be are the points of interest. You'd expect a steady curve down as you move up the income brackets, as less people earn more. Apparently in NZ we have a disproportionate amount of people earning suspiciously under each of the tax levels.

Then you can take a look at this - https://www.radionz.co.nz/news/national/257185/economic-crime-costs-up-….

Both statements are statements of fact Solidname.

You are, of course, entitled to the opinion that even if the rich do pay the majority of income tax in this country (fact) they should pay more anyway.

Beyond that you would have to define this term you use "truly rich", so we know what exactly you are talking about.

I think it behooves you to define rich in the first instance, the PAYE "rich" pay the lion's share of tax I agree, those that are otherwise rich often do not.

My statement is also a statement of fact el Ralpharoonie, I just gave you links to prove said facts. Would you like some more?

https://www.moneytips.com/how-the-mega-rich-avoid-paying-taxes

https://www.irishtimes.com/business/paradise-papers-how-the-rich-and-po…

Your first link specifically references, "the wealthiest Americans" (in its very first line).

Your second link has no mention of New Zealand at all let alone proof of tax fraud in NZ.

I conclude that although the articles contain facts they bear little to no specific relevance to New Zealand or the amount go tax the top 15% of NZ tax payers contribute to the income tax take.

An article that also contains facts - but *is* relevant o the NZ income tax take:

https://www.stuff.co.nz/business/81429047/small-number-of-taxpayers-bea…

Quotes from that article:

"By comparison, the top 3 per cent of individual income earners, earning more than $150,000 a year, pay 24 per cent of all tax received."

[This is what re-distribution through taxation looks like in NZ]

"Gareth Kiernan, an economist at Infometrics, said the data showed that New Zealand did not have the same issues that had driven protests such as the Occupy Wall Street movement, which rallied against a rich "top 1 per cent".

"New Zealand's income distribution is nowhere near as skewed as in other parts of the world. The rhetoric that surrounded that was irrelevant, from my point of view, for New Zealand.You could have people arguing that income distribution should be more even than it is but it's certainly not 99 per cent versus 1 per cent in New Zealand.""

You've posted an article containing a statement that I've already agreed with, the richest PAYE earners pay the most tax - I agree with that statement, I am completely in acceptance with that fact, I am concurring with that statement of truth Ralphy.

I am saying that PAYE earners are not (that's a negative) the biggest earners in NZ, those are the people that do not pay the requisite amount of tax.

Here's an article from the Herald, hopefully Kiwi enough for you - http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=10887756

And one from Newshub - http://www.newshub.co.nz/home/new-zealand/2017/01/revealed-new-zealand-…

Yeah fair enough, but 107 people?

Given human nature there will always be people who lie. Both about what they earn and what they are allowed to claim in benefits, (so both ends of the spectrum).

I don't think that really invalidates the broad fact that the top 3% pay 24%, so that redistribution is taking place.

From the Newshub article - 2 people now have as much wealth as 30% of the population. If 2 people have that much then 107 is not inconsequential unfortunately.

I'll be very careful with my wording here - IF those two individuals are utilizing one of these various tax I'll call them work arounds to be polite, then they would be paying tax on $70k, when they earn many, many multiples more than that.

This is why I find National supporters pretty amusing (not saying that you are one), thinking they're wealthy, when in actual fact they are enablers of extreme wealth, through their greed - clue we're allowed to access those same tax avoidances - as then we normalize the ultra-wealthy behaviour, because "everyone does it".

dp

ZS,

It may have escaped your attention that Auckland's population represents around 1/3rd of NZ's total population and that %age is growing. That means-and I want to keep this simple for you-that a lot of people NEED to live in the vicinity,to make the city work. Now,some of these will be well-paying jobs,such as my son and his wife have,but many will be in lower paying service related jobs.

The following list is by no means exhaustive;teachers,nurses,police,the fire service,those in retail,social workers,security guards,those in construction and so on. Without them,the city cannot function properly. The system is not working well for many of them,while self-satisfied,smug p........s like you congratulate yourself on how very clever you are.

In Auckland, the cost of living has increased so much that the people trained in these occupations are leaving Auckland ...

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11677339

http://www.stuff.co.nz/national/education/95039140/teachers-leaving-auc…

http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11957620

And why wouldn't they, eh? Makes perfect sense:

As of June 2016 REINZ data put the median Auckland house price at $821,000.

The salary range for teachers was between $46,000 and $72,000, for nurses it was between $47,000 and $64,000 (with 1-5 years' experience), paramedics $58,000 to $72,000 and police officers (1-4 years' experience), $53,000 to $58,000.

Sounds like we need a land tax.

It is actually shocking to think this is what makes you get out of bed each day! You genuinely believe that sucking the lifeblood out of other people by depriving them of the opportunity to own their own home, raising a family in that home, making memories, and when they retire, to have the financial ability to live life that they have been working so hard for, is justified? Not only that, you think its aspirational, and somehow elevates you to sit above them on the ladder of life! All because you were clever enough to use "other peoples money"

BLAH BLAH BLAH FOR ALL YOU LOSERS ( AND WINS )

A prediction for 2018 I came across probably true for every year..................................

I predict that this current crop of doomers will get even poorer in the comming year, as their negative attitude translates into self destructive behaviour. Eventually watching others get ahead will cause them to descend into silent despondency, only to be replaced by a new crop of doomers, hoping for a crash or some other calamity, so they can justify their own inaction and mockery of those who actually take risks and get ahead.

In other words, nothing will change !

HAPPY NEW YEAR !!!!

Dr Jane Goodall makes some very interesting reports in this discussion which you Shoreman probably will not bother to listen to. However, it shows why those that think like you are so very very bad for the future of the entire human race and especially its home planet. https://www.youtube.com/watch?v=g5WUIDzxUeo&t=2870s

If you have purchased something with an interest only loan, then you should be subjected to income tax on the profits, as clearly you have purchased with an intention to resell. How else do you pay the bank back?

I have interest only loans and I repay the bank at times and amounts that suit ME, that's how I pay the bank back

Just reckon the Govt/Rb should put a line through Interest only only and bring in a DTI ratio as well. Put investing back on a even playing field to every other borrower. Only big winner is the banks. Yes this would trigger a bit of a reset, but probably needs to happen at some stage so why not now, as all the heavily committed PIs seam to have the ability to drop a few properties...?

"EQUALITY" is mentioned a lot in the above comments. I do think equality is a bit idealistic and unrealistic.

- we are not born equal, we are so much better off in NZ than being born in a war torn country.

- what kind of equality are we talking about ? Possessions? Opportunities? Health? Lifestyle? Happiness?

- I certainly think there is no equality in the work provided from various people. If Joe stays home all day and plays video games, should he get the same as Bill who braves the traffic and works all day for the sake of equality?

It is my personal opinion, that if we have been born in a country at peace, with free schooling and we have enough food, come adulthood, we are responsible for our own life (and our family's).

It's our own choice how we:

- deal with our finances

- interact with our family

- treat our friends

- look after our own body (drinking, smoking, exercising...)

And we should accept the consequences of our choices without complaints

I am not discussing a nebulous unspecific notion of equality. I am specifically discussing equality of opportunity and the dangers of rising wealth inequality.

Of course every body is different, some work harder than others, some have more luck etc etc. You can't necessarily legislate for that. What you can legislate for is equality of opportunity, and make sure that the wealthy don't use their existing wealth, to perpetually hoard more wealth until we live in a feudal society in acknowledgement of the fact that this is actually part of human nature that will never change. Human beings just have that weakness, short sighted, self interested weakness. You can legislate so that taxes are even and fair and serve wider society most fairly and helpfully. That doesn't mean punishing the rich, but is doesn't mean favouring them either.

Too many long words. Does my head in. Got a simplified version?

Tax the Rich.

Ex Expat, that is a fundamental misrepresentation of what I have said. It says a lot about your own thoughts and beliefs that this is your interpretation.

RBNZ monitoring interest only lending

https://www.stuff.co.nz/business/100611670/reserve-bank-monitoring-inte…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.