By Gareth Vaughan

A new report on global debt levels features a "cutting-edge dataset" covering private and public debt for virtually the entire world dating back to the 1950s.

The report is an International Monetary Fund (IMF) working paper entitled Global Debt Database: Methodology and Sources.

Key findings from the paper include;

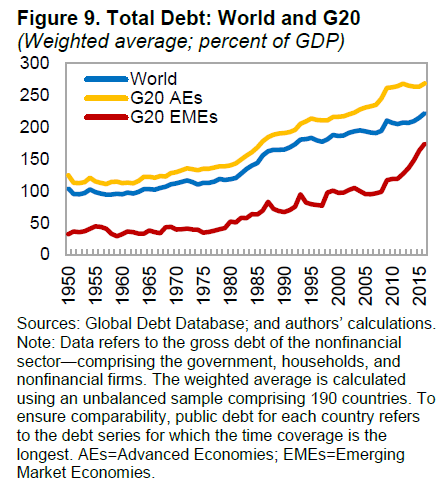

* Almost a decade after the collapse of Lehman Brothers, global debt, at US$164 trillion - or about 225% of global Gross Domestic Product - has reached new record highs.

* Global debt ratios have been on an almost uninterrupted ascending trend since World War II.

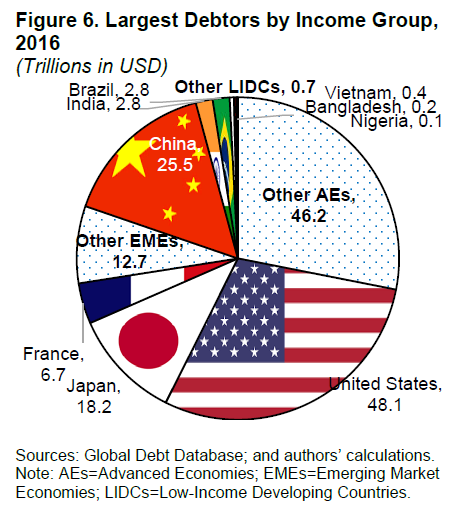

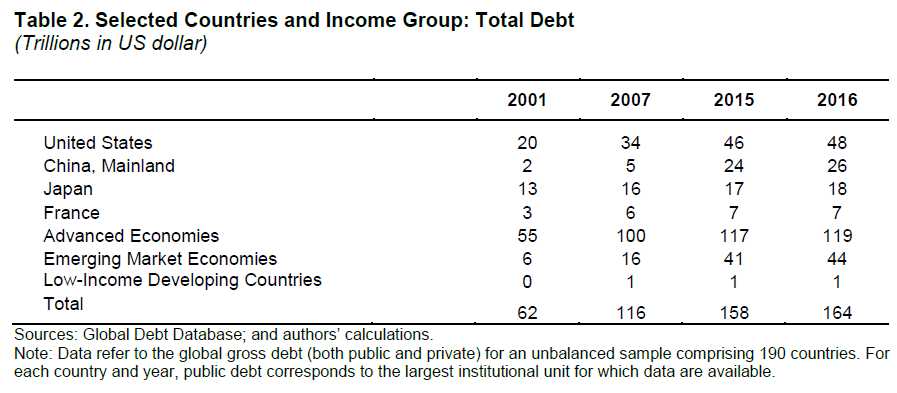

* The most indebted economies in the world are also the richer ones, with the top three borrowers - the United States, China, and Japan - accounting for more than half of global debt, which is significantly greater than their share of global output.

* The driving force behind global indebtedness has been the private sector, which has almost tripled its debt since 1950.

* Except for a short hiatus, no deleveraging has taken place at the global level since the onset of the Global Financial Crisis (GFC).

* Since the onset of the GFC in 2008, China accounts for almost three-quarters of the increase in global private debt.

* From a sectoral perspective, the driving force behind global indebtedness has been the private sector, which has almost tripled its debt since 1950.

'A new dataset that takes a fundamentally different approach to compiling historical debt data'

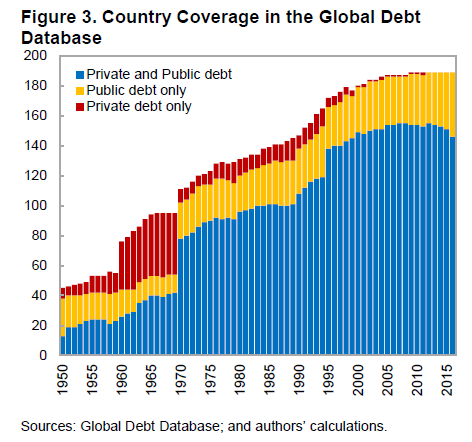

According to the paper's authors - Samba Mbaye, Marialuz Moreno Badia, and Kyungla Chae - their work describes the compilation of the Global Debt Database (GDD), a new dataset that takes a fundamentally different approach to compiling historical debt data. They say the GDD is the result of a multiyear investigative process and an extensive standardization effort to produce consistent time series of debt. It covers the debt of the nonfinancial sector, both private and public, for "virtually the entire world" being 190 countries including New Zealand, dating back to the 1950s.

The paper reports various measures of private debt ranging from core instruments such as loans and securities to total private sector debt liabilities, for both households and nonfinancial corporations, plus public debt from the central government to the wider public sector.

"One of the main benefits of this strategy is that it ensures the consistency of debt series throughout time. In addition, by including both the sovereign and private sides of borrowing, we can offer a global picture of total debt while accounting for the interlinkages between the public and private sector," the authors say.

"By including both the sovereign and private sides of borrowing for close to the entire universe of countries, we can offer a global picture of debt in the post-World War II era, which was not possible in previous studies."

Insights from this comprehensive database include that, almost 10 years after the collapse of Lehman Brothers, global debt, at US$164 trillion, or about 225% of global GDP, has reached new record highs. This figure includes government, household, and nonfinancial firm debt.

"Not surprisingly, the most indebted economies in the world are also the richer ones. It is nonetheless striking that the top three borrowers in the world [being] the United States, China, and Japan, account for more than half of the global debt, significantly greater than their share of global output."

The authors point out the emergence of China among the most indebted countries is quite a new development. That's because since the beginning of the millennium, China’s share of global debt has surged from less than 3% to more than 15%.

Meanwhile, compared to the previous peak in 2009, global debt is now 12% of GDP higher.

"That is, except for a short hiatus, no deleveraging has taken place at the global level since the onset of the GFC," the paper says. "This reflects an increase in both public and private nonfinancial debt but different country groups are behind these trends. Public debt increases have been mainly driven by advanced economies while the private debt surge is mainly explained by emerging market economies."

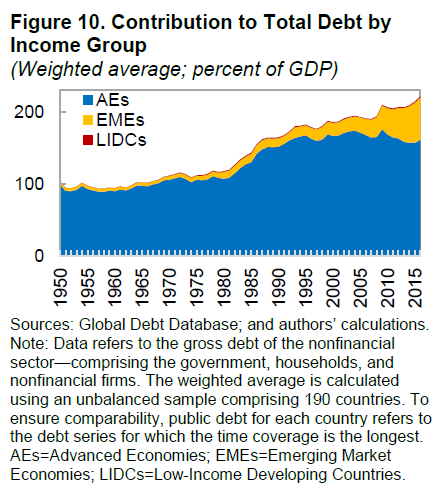

A longer-term view shows global debt ratios have been rising almost uninterrupted since World War II. Since the GFC, emerging market economies have taken the lead.

Low income countries account for less than 1% of global debt, well below their share of output.

Private sector almost triples debt since 1950

From a sectoral perspective, the authors say the key driving force behind global indebtedness has been the private sector, which has almost tripled its debt since 1950.

"The global leverage cycle was dominated by advanced economies for almost six decades, with the debt of the nonfinancial private sector reaching a peak of 170% of GDP in 2009 and little deleveraging since. On the other hand, the ascent of emerging market economies is a relatively new development, which started to accelerate only in 2005. But by 2009, emerging market economies have become the major force behind global trends. Private debt ratios doubled in a decade, reaching 120% of GDP by 2016," the paper says.

"Developments since the onset of the GFC are, however, almost match one-to-one trends in just one country. China alone accounts for almost three-quarters of the increase in global private debt. At the other end of the spectrum, financial deepening in low-income developing countries has been limited."

In terms of public debt, advanced economies have experienced a continuous increase, aside from a short interruption just before the GFC due to to favorable cyclical conditions. And although public debt ratios have reached a plateau during recent years, at more than 100% of GDP, they still exceed the levels seen in the early 1950s.

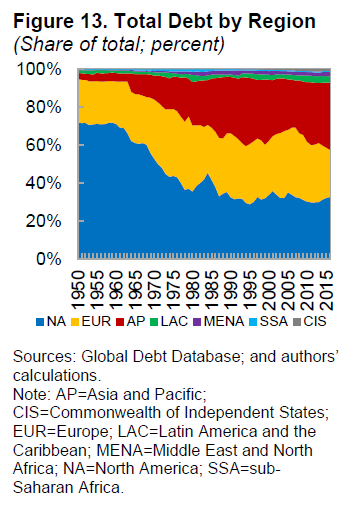

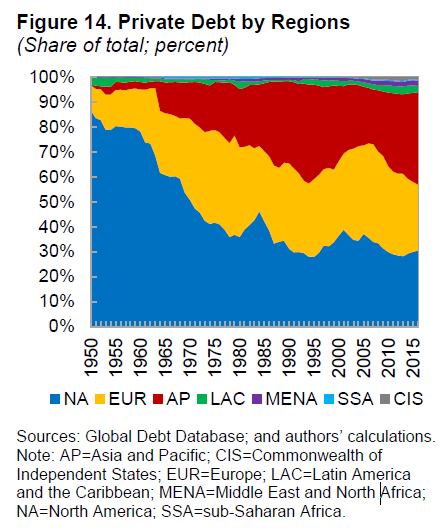

In terms of regions of the world, the most indebted ones are the Asia Pacific, North America, and Europe. In 2016 they accounted for 35%, 33%, and 25% of global debt, respectively.

"Since the early 1950s, North America was at the lead of the global debt ranking but was taken over by Asia Pacific in the early 1990s, partly due to rapid leveraging in Japan. Nonetheless, North America regained the top ranking at the turn of century and maintained it until the onset of the GFC. Since then, the Asian and Pacific Region has returned to the top position, this time thanks to the rapid credit increase in China. The ranking among the top three regions on private debt are pretty much the same, although the share of private debt from other regions is even smaller than total debt, reflecting lower levels of financial deepening in less developed countries."

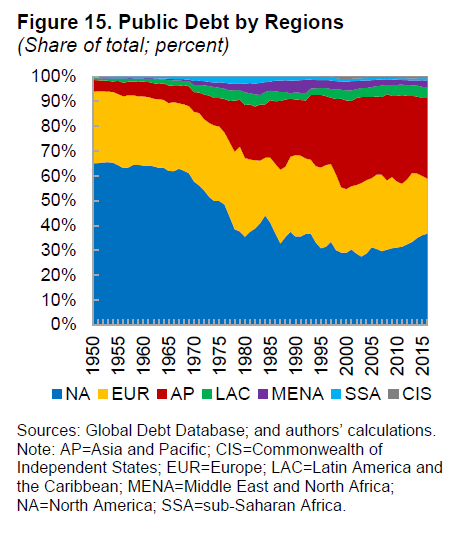

"Interestingly, the ranking on public debt has been similar to those of total and private debt until 2013. Since then, and unlike total and private debt, North America has been the highest debtor in the world among public borrowers," the paper says.

The IMF says views expressed in IMF working papers are those of the authors and don't necessarily represent IMF views.

*This article was first published in our email for paying subscribers early on Thursday morning. See here for more details and how to subscribe.

31 Comments

I don't think it will affect us negatively , down here in Godzone , if the world's leading 3 economies( USA / China / Japan ) have a credit crunch due to their staggeringly high debt levels ...

... 'cos we have permanently high house prices .... and cows .... lots of cows ... that should insulate us from the repercussions of a second GFC ....

Yessir Jim-Bob .... you can't lose with property ... and cows ....

...

That’s right Gummy you can always bring a few cows indoors to keep the house warm

Cows provide good insulation indoors

Tether the cows up to some flexible gas lines and all your energy needs are sorted.

As long as the interest keeps being paid and the profitability of that is sufficient to cover the defaults, the mountain will continue to rise. Is it as simple as that?

So it's a confidence game?

Well Andrew there is confidence and then there is over confidence. It is usually not untilthe results are in, that the experts can tell the difference.

Thanks Andrew all three links today. Reminded me as to when I was driving through a whole series of back country roads the other day, how the hell did all these get built. Most of them obviously to service primary production but these days our country cannot even afford to service them let alone build new ones.. Were our pioneers that much more productive. Doesn’t seem to make much sense given the development of mechanisation and civil engineering all of which supposedly add speed and lower cost of construction.

"No, the worst thing that can happen is that you fail to get an investment but are encouraged to keep on pursuing a used-to-be-good idea that died a year ago. You will have another good idea! It’s far more important to play the meta-game well — to do nothing and wait for the next live opportunity — than to keep propping up the dead opportunity with extraordinary effort. Bury your dead. Have a proper funeral. Respect the dead. Never forget the dead. And move on without regret."

On the economics side, the lesson here is that central bankers today are grieving the death of the so-called Great Moderation, where productivity rocked, inflation was tamed, and the business cycle was muted. But they can’t move on. They can’t bring themselves to have a proper funeral. They are expressing their grief poorly — not through anything like the Kubler-Ross stages of denial, anger, bargaining, depression, or acceptance — but through magical thinking, through the pathological belief that if only the right words are said and the right thoughts are thought, then the dead will show up at the front door as if nothing had happened. To understand the human pathology, read Joan Didion’s wonderful book. To understand the policy pathology, you could do worse than to read the Epsilon Theory note."

I knew it was all going to end in a theory

Now do you have a theory on your own pathology ?

Hilarious blog post

Keep up the deep thought

lol

So did chessmaster keep up to his name?

I'm registered on chessorg.com. mainly play online on phone and tablet.

And surely such confidence is waning.

There are some that live in an insulated world, so end up with a false sense of confidence

Its a question of confidence in the currency isn't it? I've been hearing of debt in particular US debt since I was in my high school years. Election promises to curb debt and in the end the same old same old. As long as the confidence rests in the nations ability to pay its promises who cares what the level of debt is and in particular US can always print money to cover its costs. USA with higher debt has a AAplus while NZ enjoys a AA.

Well, New Zealand's public debt is low compared to our OECD friends, however our private debt is one of the highest. I don't see a high-tech economy emerging in NZ or productivity picking up. With such high private debt levels here and the financial sector unwilling to lend to productive endeavors (manufacturing, software companies, fringe agriculture, R&D, etc) this might be as good as it gets.

Now the NZ government could increase public debt to invest in the aforementioned or even do 'helicopter money'. South Korea has companies like Samsung because the private sector is allowed to use government funding to grow high-tech businesses for 5 years, at which point they sink or swim. Some do sink but then you also get the Samsungs.

People and governments would do well to remember currency is not a magic wand. The more currency is printed, the less valuable it often becomes. Currency is a means of exchange .. who wants to cut off a lambs leg to exchange for a chicken? NZ could increase it's public debt (aka the money in circulation) if this newly minted money actually circulated rather than sitting in stocks, property or on a balance sheet - having a velocity of zero.

Most people in NZ are taped out, house poor or coming to the end of being able to use their homes as ATM's. Not a good situation! So while private debt (hopefully) sorts itself out, a public spend up could be good. The ball is with the government - unfortunately the current steady-as-she-goes budget could mean an economy dead-on-arrival.

NZ is in a pickle.

South Korea also has companies like Samsung because the military dictatorship at the time forced the oligarchical families to industrialise or lose their lot. Otherwise those families would have continued to invest only in shopping malls, restaurants etc. Consumption-based businesses.

Seems to have worked out?

Yes, indeed. Wasn't meaning to imply otherwise. Compared to say, the richest oligarchs in ...the Philippines, for example. Malls, hotels, restaurants etc. but not industrialisation that results in a larger middle class.

Its unsustainable! Just a matter of time before it all falls down.

Yes - as inevitable as rain. .

Saying this conveys zero information ; if you told us when and how that would have some meaning.

Er, has no one noticed what has happened in Argentina of late. Inflation at 25%, interest rates at 40%, apparently because they borrowed in USD and LIBOR is up. Turkey and South Africa are not far behind. Italy is about to come back on the front pages. All a consequence of rising world dollar interest rates, starting in 2015:

https://fred.stlouisfed.org/series/USD3MTD156N

Roger,

I'm thinking Argentinas inflation has alot to do with the extreme debasement of its Money..

https://fred.stlouisfed.org/series/MYAGM2ARM189N

Countries such as Argentina demonstrate the fallacy of governments spending beyond their means. It saddens me to see people advocating for gov to do a "spend-up". In essence, that results in borrowing from the future to get a benefit in the present. At some point, one gets to pay the bill, via currency debasement and/or recession as the debt load becomes unmanageable.

The people that argue that the spend-up increases the gov income by at least as much as the spending via increased velocity of money, well, that is the .gov version of the Reagan trickle-down theory. We saw how that worked out in the past in the US.

These more spending policies are a good thing for the people that gets the munny. Which is not always who you think. Most of it flows straight through the pockets of the recipients, whether they be hard working road builders or welfare dependents, it all ends up in the Aussie banks.

Harbingers, Cassandras, who can tell Roger? What is really scary for an old timer like me is that no expert, as was the case in 2008, can offer any specific explanation of a global financial “collapse” until after it has happened.

Actually, that is not true. It is the excuse used by those who didn't see it coming, and as long as they are in the body of the herd, they get away with it. Plenty of reputable people saw it coming, notably the banker's bank, The Bank for International Settlements, and people like Ragan at the IMF. Not for public consumption of course, and not a cool career move.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.