Here's our summary of key events overnight that affect New Zealand, with news the US Fed has adopted a more hawkish tone.

The US Federal Reserve has issued a short statement today announcing a +25 bps rise in its policy rate. The new rate range is 1.75% to 2.00%. The statement might have been short but it was a sort of victory statement saying it is meeting its inflation and full employment mandates and that the prospects are that this situation will endure. The rate increase was widely expected. Also expected was the changed emphasis, dropping its crisis era wording. The stage is now set for more rate increases, and they may come at a faster rate. In fact, the Fed's dotplot is now for four rate rises in 2018, up from three. We have had two so far (March and June), so another two this year are now expected.

The actual rates American consumers are paying for credit have been rising as the Fed hikes have come through. And they will likely rise further now.

And underscoring the rising price background, data out today for US producer prices records them rising at the rate of +3.1%. That is their fastest rate of increase since January 2012.

Meanwhile in Frankfurt, they are on watch for the ECB rate review decision (tomorrow). The ECB is expected to signal that their €2.6 tln QE program will start winding down, and the details of how they plan that are eagerly awaited.

In Germany, their courts have imposed a €1 bln fine on VW for their use of diesel-cheat software and their management's response to being caught out.

Given the locking in of higher US dollar interest rates, we will need to keep an eye on how that affects emerging markets. It might not be pretty.

The UST 10yr yield is up at 2.98% following the upbeat Fed statement. The Chinese 10yr is at 3.71% (up +2 bps) while the New Zealand equivalent is now at 3.03%, up +2 bps.

Oil prices are up a little today and now just over US$66.50/bbl. The Brent benchmark has followed to just over US$76.60/bbl.

Gold is unchanged at US$1,295/oz.

The Kiwi dollar will start today unchanged at 70.1 USc. On the cross rates we are however a bit firmer at 92.7 AUc, and 59.5 euro cents. That keeps the TWI-5 at 73 and still in its very tight June range.

Bitcoin threatened to go under US$6,000 earlier this morning but has since recovered somewhat and is now at US$6,297 which is -6% below the price at this time yesterday.

This chart is animated here. For previous users, the animation process has been updated and works better now.

The easiest place to stay up with event risk today is by following our Economic Calendar here ».

Daily exchange rates

Select chart tabs

27 Comments

Higher interest rates coming and higher taxes...what could possibly go wrong?

I hope so, got money in the bank

That’s good, the banks will need it when a lot of their collateral goes up in smoke.

I bet I can take it out faster than selling a house

I bet the banks will know they are in trouble before you do

The writing is on the wall. Who dares read it?

Unless its in Braille, at least 5 that I know will ignore

"It sounds awfully familiar, doesn’t it? Other than inflation which is now more deflationary (beyond consumer prices) especially in the labor market, there is this renewed tendency to blame us for systemic issues that have little to do with us. "

http://www.alhambrapartners.com/2018/06/13/down-this-same-road-again-on…

US Fed can declare true victory once its balance sheet has returned from the current four trillion to under one. No thanks to Trump, I can't help but imagine it to be over six trillion in the near future.

Isn't Trump just doing what Obama should have done but wasn't allowed to, ie overspend freely to get everyone back to work? If Obama had been able to overspend as freely as Trump, then presumably the Federal Reserve wouldn't have had to. The US is officially at full employment but there is very little wage inflation and very low participation, ie, the official unemployment numbers are gamed. The US is a funny sort of mix of first world and third world.

Very true Roger.

Paul Krugman wrote at length on the need for massive Govt investment - Roads, Bridges post 2008 - actually a quite limited response in the scheme of things.

We can't entirely blame elected officials for their shortsightedness in picking adrenaline economic boosts such as QE and tax cuts over structural reforms and infrastructure investments.

Elected governments have a 3 to 4 years window to keep opinions tipped in their favour. People grow increasingly impatient over the visible outcomes of large fiscal spending. Very few acknowledge that the large outlay is followed by a prolonged gestation period and actual benefits are realized at a gradual but sustained pace.

A transport system overhaul in Auckland will take upwards of $30 billion and 5 years to build at which point, there will be indirect flow-on benefits to the economy and well-being of people in the form of improved productivity and mobility of workforce. The previous government chose instant solutions such as flooding the country with cheap labour and prop up housing to artificially boost the economy instead.

NZ median house price hits new record high of $562,000 - https://www.reinz.co.nz/Media/Default/Statistic%20Documents/2018/Reside…

Auckland median house price only down 1.3% on same time last year $852,000 vs $862,800 - REINZ have the most accurate up to date data

Auckland volume up, but median price down. Akl HPI =+0.6%, rest of country HPI +6.8%. Auckland stops, regions overshoot, anybody know what comes next?

Go fill your boots, before you miss that runaway train champ.

Declining trend increasing for HPI in Auckland?

- 1 year 0.6%

- 3 Mnths -0.4%

- 1 Mnth -0.6%

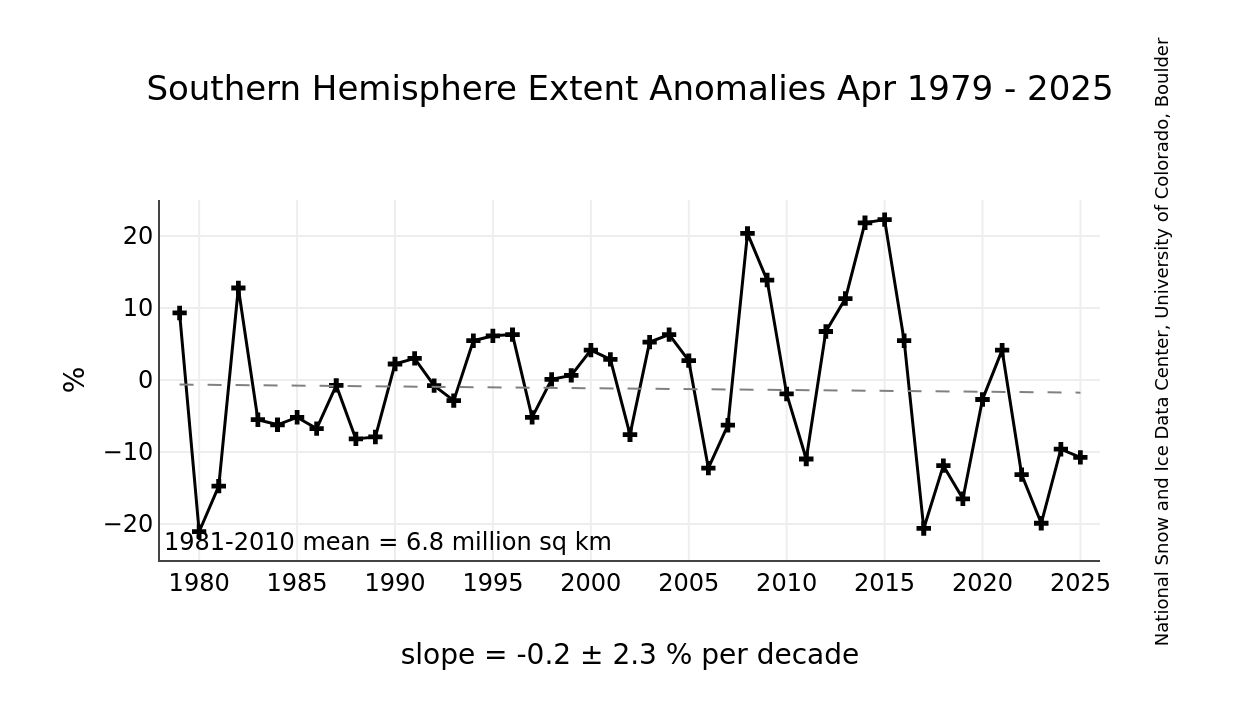

Heres one for Profile. Antarctica has lost 3 trillion tons of ice in only the last three decades. https://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=12069988

...and the long term trend in the satellite era. May Antarctic sea ice is higher than it was in 1980... Long term trend of 1.7% gain per decade for May. I guess the Herald forgot to mention that. Stupid data spoiling a good scare story.

{kind=link}

greetings, old friend

Pretty sure I predicted it last month, but I'll say it again: US treasury 10-year minus 2-year spread will go below 0.4 in June 2018 (this month).

"The stage is now set for more rate increases, and they may come at a faster rate. In fact, the Fed's dotplot is now for four rate rises in 2018"

Watch the US go into recession mid-late 2019 and backpedal on interest rates in early 2020

And if that happens... will they drag everyone else down with them again?

I would say so, there's weakness in so many countries already

I guess the trigger point for a global recession seems to be elsewhere this time around with Italy verging a collapse (10 times the GDP of Greece), UK's dramatic slowdown, Australia and Canada's household debt, Japan's national debt and China's corporate debt to name a few.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.