The NZ Super Fund would lose over $20 billion - more than half its current value - in any repeat of 2008's Global Financial Crisis, the Guardians of NZ Super say.

However, they do estimate that any such losses may be recouped within about 20 months.

In the NZ Super Fund 2018 annual report released on Thursday, the Fund's Guardians have outlined an exercise modelling what would happen in the event of another major global meltdown. See video here

Chief Executive Matt Whineray says the Fund’s high exposure to growth assets is set by the board in the 'Reference Portfolio', a simple passive low-cost portfolio of listed equities and bonds that serves as a benchmark for the Fund’s investing activities.

"In the short-term, growth assets can be volatile, moving up and down in price. The Fund has the ability to ride out and potentially benefit from these short-term movements. In the long-term, the Fund’s exposure to market risk from growth assets such as shares is expected to pay off in the form of higher returns than the cost to the Government of contributing to the fund."

Whineray says by taking on the market risk associated with growth assets, the Guardians accept the risk that markets may experience sharp drops in value, be they driven by financial or political shocks, large commodity price movements, natural disasters or war.

'Largely unavoidable'

"It is largely unavoidable that a growth-oriented portfolio such as the Fund will fall in these periods.

"...Having made the choice to expose the Fund to short-term volatility in order to generate long-term returns, the key is to ensure we have the discipline and resources to hold our course when volatility happens. Critical in this is understanding what these times could look like, before they happen."

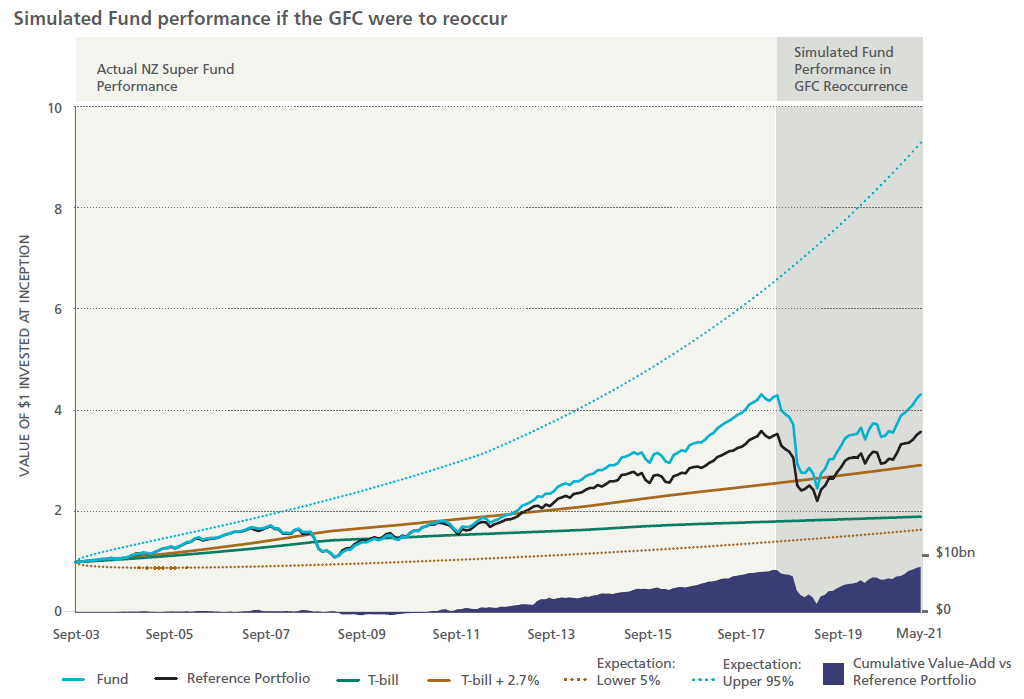

The Guardians have produced the below chart, which shows a simulation of what would happen to the Fund if the Global Financial Crisis (GFC) period of returns (2008-2011) were to be repeated. For the scenario, they used the Fund’s current asset mix and a representation of how the Fund’s active investment strategies would react to market movements.

"From peak to trough (a ten-month period), we estimate the Fund would lose $20.3b (-52.6%) in a repeat of the GFC. The notional Reference Portfolio benchmark would fall by 44.7%.

"The reason we estimate that the Fund would lose more money than the Reference Portfolio benchmark is largely because we expect our strategic tilting programme would buy more growth assets as they fall in value. This is because the times when the global economy and financial markets are in distress are those that present the best buying opportunities for long-term investors such as ourselves."

Whineray says these numbers would not necessarily be reflected in the Fund's annually reported returns, as market volatility does not always line up with our fiscal years - "hence the largest annual downturn we experienced in the actual GFC was -22%".

"The GFC was characterised by both an unusually sharp drawdown and rapid recovery in financial market values. This is a relatively rare occurrence; recoveries from significant market crises can often take longer than this. In general, however, the Guardians believe that equity markets eventually mean-revert to higher fair values following transitory periods of crisis. As a result, the Guardians expect the Fund would earn back losses suffered by our active strategies in subsequent years as markets recover.

"The above simulation also illustrates how, in a repeat of the GFC, the Fund would recover its initial value, and catch-up lost ground, within 20 months."

Whineray says, however, the expected recovery in the Fund’s value, is only feasible "if we are able to 'hold the course' with our investment strategies through a market cycle".

'Major risk'

"So, the major risk to the Fund is not that it will experience significant volatility in its returns - we know that will happen. The major risk to the Fund is that we lose our nerve, close down our investment positions and lock in the losses experienced in the crisis. This would significantly impair the ability of the Fund to fulfill its long-term purpose."

Whineray says as the Fund becomes bigger in dollar terms, and grows as a share of the economy, its gains and losses from short-term market volatility will also increase in size.

"We encourage stakeholders to understand that the main challenge in persisting as a long-horizon investor is in looking through short-term shifts in value and focusing instead on more appropriate and long-term metrics of success. Even considering the risk of market crises, the Guardians’ view is that the Fund’s market risk and active strategies are appropriate and compensated risk exposures for a long-term investor."

He says the Fund is "well-placed" to withstand short-term losses, as there is no immediate need to withdraw capital from it. Short-term, volatility in the Fund's return is an expected outcome of the Board's choice of the level of equities in the Reference Portfolio. These fluctuations can be treated as “paper losses” with little long-term ramifications for the Fund’s ability to fulfill its purpose.

Whineray says the Fund achieved strong returns in the 2017/18 year thanks to a combination of market growth and its value-adding strategies. Equity markets were characterised by strong returns and exceptionally low levels of volatility in the first half of the financial year, "followed by the re-emergence of volatility at the start of calendar 2018 – a more normal situation and one from which we were well positioned to profit".

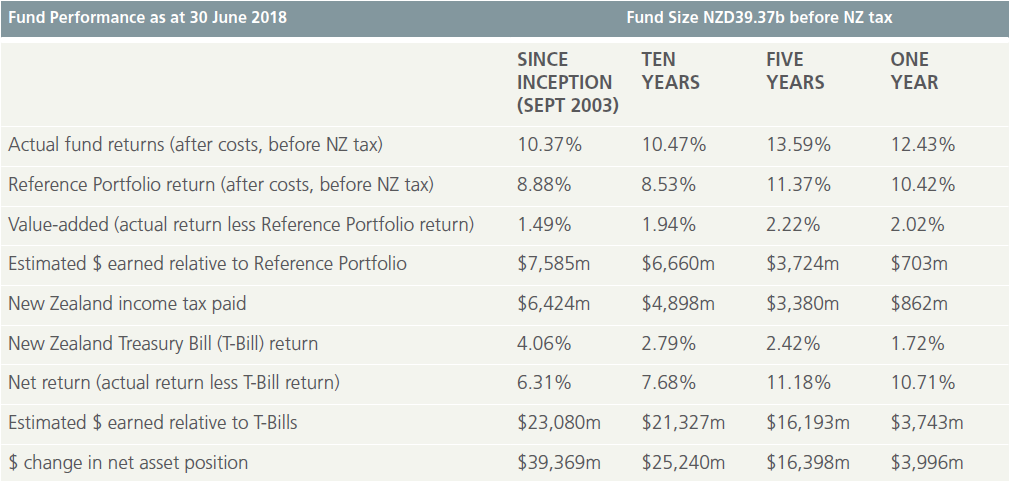

Whineray says the Fund again out-performed global markets, returning 12.43% (after costs, before NZ tax) over 2017/18. The Guardians’ active investment activities added value of 2.02% (NZ$0.7b) on top of a Reference Portfolio (market) return of 10.42%.

The Fund finished the year at NZ$39.37b before New Zealand tax, an increase of NZ$4.0b.

The overall Fund’s out-performance of the Reference Portfolio was due mainly to the success of its strategic tilting programme, a positive performance by its single largest investment, Kaingaroa Timberlands, and the active collateral mandate.

Looking ahead, Whineray says the external environment appears "challenging".

"Global growth is beginning to decelerate, inflation is starting to rise in some developed markets and financial conditions are tightening with the withdrawal of central bank liquidity. While trade tensions have been escalating, the contagion into financial markets has been limited to date.

"With many markets at or above fair value, our response has been to lower the level of active risk and maintain higher than normal levels of portfolio liquidity. We remain committed to our long-term investment strategies and will continue to take a highly disciplined approach to active investment."

New Zealand investment

Whineray said because New Zealand is a small economy, most of the Fund is invested offshore.

"This is prudent from a diversification perspective and is considered global best practice. We are, however, committed to finding attractive investment opportunities in New Zealand, and a significant proportion of the Fund’s active, value-adding investments are domestic ones.

"The 2017/18 financial year was notable for the further development of our new Investment Hub approach to generating domestic deal flow. A major milestone in this was the launch of Māori investment fund Te Pūia Tāpapa, with which we have agreed to become a preferred partner."

Then Finance Minister Bill English in mid-2009 officially directed the Fund "that opportunities that would enable the Guardians to increase the allocation of New Zealand assets in the Fund should be appropriately identified and considered by the Guardians".

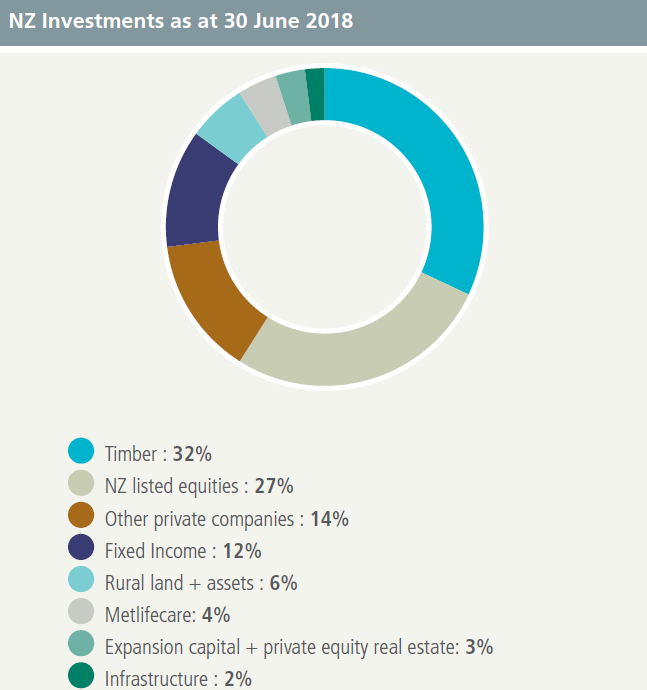

Whineray says while the dollar figure of the Fund's investments in New Zealand has increased from $2.4 billion to $6 billion in the seven years since 1 July 2009, the proportion of the overall Fund that is invested in New Zealand (in value terms) has reduced from 21.3% to 15.4%.

"The proportional drop reflects the strong performance of global equities in recent years, even after significant new investments by the Fund in New Zealand."

Whineray says the Fund is one of the largest institutional investors in New Zealand and plays a significant role in New Zealand’s capital markets.

"While we believe the Fund has an advantage when investing domestically (versus internationally), in a global context, New Zealand is a very small investment market (it comprises just 0.1% of global listed equities markets). For our New Zealand investments, therefore, we require an additional return that will compensate us sufficiently for the risk of concentrating more of the Fund’s portfolio here. As one of a few investors of scale in the country, we also maintain a high level of price discipline."

Auckland light rail

In May the Fund submitted an unsolicited proposal to the New Zealand Government offering to assess the viability of the Auckland Light Rail Project for commercial investment.

Whineray says the Fund's consortium partner is CDPQ Infra, a wholly owned subsidiary of Caisse de Dépôt et Placement du Québec (CDPQ), a CA$300b pension fund owned by the Government of Quebec. CDPQ Infra is responsible for developing and operating infrastructure projects including Montreal’s 67km light rail network. "Together with CDPQ Infra, we are now participating in a NZ Transport Agency-led procurement process for the project."

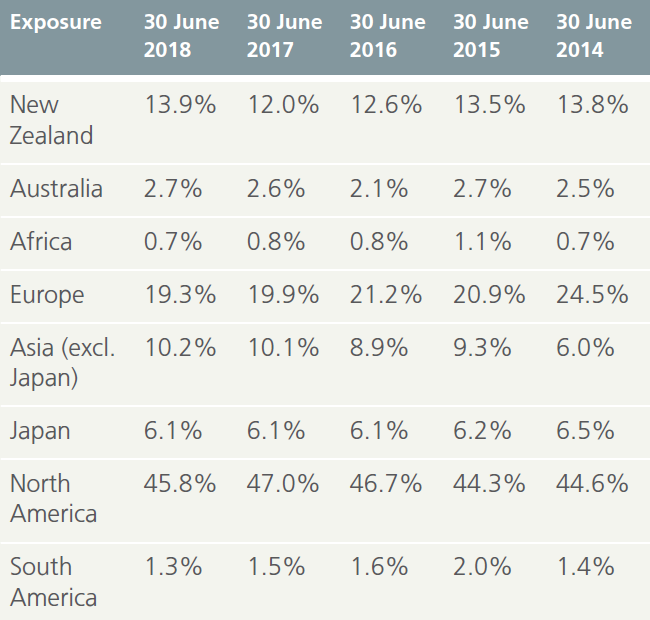

The below table shows exactly where, geographically, the Fund's money is invested. Note that this calculation includes foreign exchange hedging instruments such as FX contracts and cross-currency swaps, so the percentages for NZ investment look somewhat different to the percentages cited above, which do not include contracts and cross currency swaps.

29 Comments

I think a quick recovery cannot be assured when Central Banks have limited interest rate margin to use as stimulus. Countries debt levels have blown out during the growth faze which might mean limited head room in a downturn. I wouldn't count on a quick recovery this time around unless there is debt forgiveness on an unprecedented scale. In any scenario, many will have to carry unprecedented losses.

Also if that's the Super fund, what happens to the house deposits in Kiwisaver. I know they're meant to be for retirement too but the banks have closed the door on mum and dad so kiwisaver now funds the housing market Ponzi too. A global correction could wipe out the pool of buyers with enough in kiwi-saver to afford a purchase. What then happens to the housing market?

Anyone following standard advice would not have money earmarked for a house in the next few years invested in the stock market. I'm sure some don't follow the advice, but I would expect that most do.

Agree completely mfd. But it is the kiwisaver accounts that are now being actively raided to fund the deposits for buying, because the FHB's can't save it any other way due to rising rents and living costs. That's the reality, a kiwisaver fund gets to a 20% deposit level and gets stripped bare (the banks encouraging the saver) to buy an over-priced asset (house). The banks then return the interest on the new loan to other kiwisavers, thereby allowing them to get close to perpetuating the Ponzi. It's genius banking! Use kiwisaver to fund loans on 10-1 ratios, that pay interest to those saving in the kiwisavers for the next tranche of loans. All the way the bubble is perpetuated by the very savers that are desperate to jump into the bubble.

Just because money is in Kiwisaver doesn't mean it's in stocks, people wanting to use it to buy soon should be in a defensive, largely cash, Kiwisaver account. The situation doesn't really change just because money is being saved in the Kiwisaver wrapper except there's extra goodies offered if you build up your deposit there rather than in regular savings accounts.

I agree, the assumption of more massive monetary stimulus in response to a repeat share market crash is highly questionable now. Also the illiquid nature of the NZSF portfolio makes it hard to value in good times let alone bad.

It's fascinating how many people assume that the next downturn will be as bad as the GFC if not worse. The GFC was abnormally damaging, there is certainly no guarantee that we'll see another similar event any time soon. I read an interesting article recently pointing out that after the double crashes of the Great Depression, there were no 40%+ crashes from 1938 until the 70s, and only a couple of 30%+ crashes. Maybe we've been conditioned by the Dotcom Crash and GFC to expect meltdowns, and we won't see one again for decades.

https://awealthofcommonsense.com/2018/09/what-if-stocks-dont-crash/

No guarantees of course, the future doesn't always look like the past. Maybe the next one will be even bigger.

I would not invest in light rail .............

Depends how the contract is written. Knowing how the Ak council operates, ratepayers will carry all the risk.

Their investment horizon likely stretches as far out as a century on some part of that portfolio, there will be plenty of peaks and troughs inbetween.

If a recession or worse is on the Horizon then selling the riskier assets and crystallizing gains seems sensible unless the fund is so big that such sales would move the market, if not perhaps someone will explain why not?

No-one knows how far away the horizon is. They could sell now to avoid what turns out to be a 20% fall, but what if they miss out on a 40% rise before that happens? And then when do they buy back in? How do they know the 20% fall is not the start of a 50% fall? If they delay, how much of the recovery do they miss out on? What are the transaction costs in selling out and buying back in again?

Quite apart from the obvious difficulties in successfully running a strategy like that, there is significant career risk for the person making the calls.

With those returns we should let the over 65s put their money into the fund for a guaranteed lifetime annuity of say 6% - money stays in the fund when they die ("investing in NZ"). Zero risk for retiree. More money for the super fund. Puts a bit of competition into the currently stagnant annuity and reverse mortgage market. Private providers can still offer products that allow some money back after death. Give it a catchy name - KiwiBond? Maybe administer through KiwiBank? Just need to set the rate so that it's better than a term deposit and yet low enough that all costs and risks are sufficiently covered. Could perhaps index the rate to inflation or the prime rate for lower risk to the retiree.

The last crash was 40%. The simulation looks about right. Takes a while to get to the bottom. Trouble is, no one knows how to time the market. For instance, I predicted a month ago that the UST10-2 spread would go negative four days from now. It doesn't look like it is going to.

The risk remains that dollar credit will seize up globally, with disastrous consequences for countries that have to borrow dollars to cover deficits

http://www.atimes.com/article/has-the-derivatives-volcano-already-begun…

Recall from somewhere when the great depression took hold the USA had little option other than to suspend repayment(s) of WW1 loans they had made. The UK in particular was $billions worth. Did they ever get it all back? Don’t think these days the USA is in any position to act similarly.

You are so right and that event would trigger a liquidity crisis which will become the real Elephant in the room.

Correct. But it would not be the typically referred elephant that everyone feigns not to see. It would be the rampaging elephant that would leave little in the room unbroken!

That's what happens. They invest in long term(and largely illiquid) assets.

You accept the ups and downs.

You thought 2008 was bad? Wait for GFC2 to come it will be a big fall to the bottom of the cliff.

not sure of the logic of the State investing superannuation savings into the stock market. Investment theory states that over time funds will at best achieve the market. If that's the case leave it in individuals hands to make that call, and tweak tax to incentivise.

The flip side is the NZSF should be selling down now. And reinvesting once the market recovers. However if all state owned pension funds exhibited the same behaviour then they would exert significant market influence, and likely trigger a crash.

All studies show that people are really bad at self-investing. They take their money out at the wrong time, make uninformed decisions, etc. Take a look at some of the academic studies on Oz and US retirement investments - very depressing in how badly people do. Not that we need to go full nanny state - people can still save and invest their Kiwisaver however they like. But we need a safety net (also see my post above for an option for those who want a safe retirement income from their KiwiSaver money - KiwiBond). By the way, if you look at the graphs above, the fund is outperforming its benchmarks. Given they can invest in things like light rail, which traditional funds can't, it is possible for them to outperform indexing. They make it clear that they will go down more than the benchmark in a crash.

i sold my portfolio last month Avatar99. there are always winners and losers in life, thats a given. My argument is that the sharemarket is fundamentally a riskier investment, and i don't believe the state should be investing in this type of vehicle with its mandate to chase capital gain.

Never got into Kiwisaver, that $50 a week was better off going on your Mortgage. Guaranteed return on your money. Never trust others to do what you can do yourself.

You turned down a guaranteed 20+% ROI to pay down a debt costing ~4%?

The debt was costing me 8.6%. I basically retired at age 48. No regrets, I think I would stay with the same plan if I had to do it all again.

Okay.

I think we can agree that no one should ever listen to any advice given by Carlos henceforth.

If you have an employer who will match your contributions you'd be crazy not to snap that up. If not, you're crazy not to put in ~1k a year and grab $500 from the government. There are no other investments with that kind of risk adjusted return.

I'd also say it doesn't make sense to put in more than 3% (assuming that is >1k) - better off saving the excess elsewhere with more freedom.

If the fund is being built up to fund expenditure far off into the future then any financial crisis would be just noise. That's the problem when your assets are marked to market, you get the current price but it's a bit meaningless till you plan to start consuming your investments.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.