Even +20% growth by the challenger banks has failed to materially change the market dominance of the five main banks in 2017.

The strong are staying strong.

And their customers are sticking with them.

High levels of service, a fast shift to the convenience of online services, and a general inertia by customers has seen the big mortgage banks retain most of their mortgage share. Regulatory changes around LVR restrictions and speed limits have ensured the home loan landscape is restricted enough to allow no material threats to their market dominance.

Much of the challenger bank growth is on the back of 'investor' lending in the first part of the year, and that is something that was closed down in the second half.

Even among the majors, most were unable to grow outside the general market shifts. Perhaps the exception has been ANZ which has made meaningful 'progress' in its chase for larger mortgage market share. Their mortgage book grew by almost NZ$6 bln according to the latest RBNZ G1 data. Their lending for mortgages grew from 55.4% of all their lending to 57.5% in 2017, growth that far outpaced their main rivals.

Most New Zealand banks qualify to be labelled 'mortgage banks' - the exception being the BNZ. Most bank loans are mortgages, reflecting the dominance of residential property in the New Zealand economy. Here is the latest RBNZ data:

| Proportion of mortgage lending of all lending | Mortgage | Market | |||

| as at June | 2017 | 2016 | Lending | Share | Growth |

| Main banks | % | % | $ bln | % | % |

| - ANZ | 57.5 | 55.4 | 68.940 | 29.9 | +9.4 |

| - ASB | 65.4 | 66.0 | 51.283 | 22.3 | +7.3 |

| - BNZ | 46.4 | 46.2 | 36.618 | 15.9 | +8.0 |

| - Kiwibank | 92.6 | 92.3 | 16.531 | 7.2 | +7.0 |

| - Westpac | 60.1 | 59.7 | 46.576 | 20.2 | +5.1 |

| Weighted averages & totals, main banks | 59.0 | 58.2 | 217.948 | 95.5 | +7.6 |

| Second tier banks | |||||

| - Co-operative Bank | 92.6 | 92.7 | 2.015 | 0.9 | +15.7 |

| - HSBC | 37.7 | 36.4 | 1.491 | 0.6 | +18.5 |

| - SBS Bank | 78.4 | 76.8 | 2.783 | 1.2 | +21.6 |

| - TSB Bank | 82.4 | 80.9 | 3.970 | 1.7 | +23.4 |

| Weighted averages & totals, 2nd tier banks | 65.1 | 69.2 | 10.259 | 4.5 | +20.6 |

| Source: RBNZ G1 | |||||

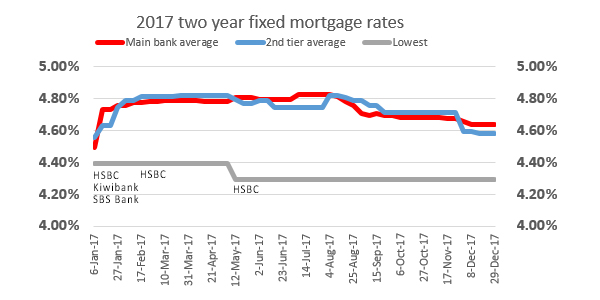

This time last year we observed that mortgage interest rates were likely to rise in 2017. And they did. Most of the rise came early in the year and there was a slow and minor retreat in rate levels as the year wore on.

Market and regulatory conditions saw an unexpected trend however; the main bank rates were often very competitive with the challenger banks, and it has not been until December that the second tier banks have been able to restore their rate advantage.

The market share pressure #1 ANZ has been able to exert on its main rivals has been intense. And it has been able to do this without compromising its carded offer rates. This pressure however has brought #2 ASB to the point where it has felt the need to open up an advertised rate advantage.

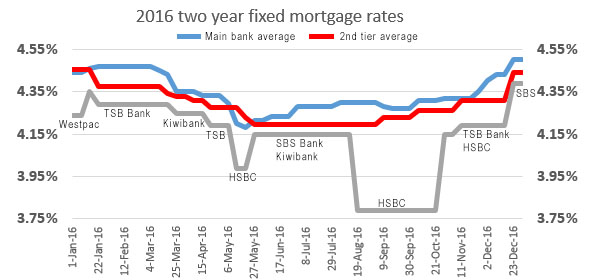

Just how different 2017 has been from 2016 can be seen from this chart.

In terms of overall price competitiveness, here is how these banks positioned themselves on average over all of 2017, and at the end of the year.

Admitedly, this is for the popular two year fixed term, and not every bank chose to position its fighting rates at that duration (the Co-operative Bank as an example).

| relative price competitiveness | 2016 average | 2017 average | year-end | year-end | |

| two year fixed only | rate % | rate % | rate % | premium % | |

| #9 | Co-operative Bank | 4.38 | 5.24 | 4.69 | -0.55 |

| #7= | ANZ | 4.39 | 4.76 | 4.65 | -0.11 |

| #7= | Westpac | 4.33 | 4.76 | 4.65 | -0.11 |

| #6 | SBS Bank | 4.25 | 4.75 | 4.69 | -0.06 |

| #5 | BNZ | 4.35 | 4.74 | 4.65 | -0.09 |

| #4 | ASB | 4.35 | 4.73 | 4.59 | -0.14 |

| #3 | Kiwibank | 4.30 | 4.71 | 4.65 | -0.06 |

| #2 | TSB Bank | 4.24 | 4.66 | 4.64 | -0.02 |

| #1 | HSBC Premier | 4.21 | 4.32 | 4.29 | -0.03 |

The scale of the interest rate increase from 2016 is also evident in this table.

A mortgage may be a 'commodity' these days but price (as represented by carded rates) doesn't seem to change the borrower's choice of bank that much, certainly where the differences are very small.

But there has been one bank, HSBC Premier, that has offered up a substantial rate advantage - but only in return for customers with the very best financials. But given that this will be most borrowers who have had a mortgage for ten years or more, it is somewhat surprising their loan growth has only been +18.5% in 2017.

It seems very few of us will move even for a 0.35% benefit.

21 Comments

BNZ's parent NAB, set off down the business and commercial lending path when the GFC hit, thinking that productive growth in their lending book would be the answer to what ailed the economy. Fools! The NAB, like it's subsidiary BNZ, got left behind by the 'smarter' banks that saw that the only source of future revenue would be housing loans. Will they too now play 'catch-up'? This time next year will give us the answer, but if things do 'get worse/go bad' then Kiwibank's 93% reliance on property lending looks precarious.....

Yep, Kiwibanks numbers have the whiff of a future bailout about them

BW

Your comments defy logic

Surely commercial lending was in fact prudent if as you later claim a reliance on housing loans “ Looks precarious “ as you state !

I enjoy the scrambled brain opinionated here

Google the words Irony and Sarcasm. It might help you.....If it doesn't I can only assume that some sunspot activity is interfering with your gaseous particles.....or perhaps you are just being glib?

Interesting, so it looks like rate "competitiveness" has little impact on the growth rate among major banks. I'd have sort of guessed that actually, after all if a business poaches customers with lower rates it's likely low quality and flighty growth whereas winning business through brand management, innovative products, class leading service etc. likely wins loyal customers over time.

The large gulf between short term fixed mortgage rates and the high floating rates mean most borrowers are kept locked in for 1 - 2 years so less chance of switching banks.

NZ consumers are sitting ducks for duopoly groceries, mon/duopoly building supplies, 4-opoly banks, and low competitive pressure on any essential product.

Meanwhile low income renters pay most of their income on rent

https://www.stuff.co.nz/national/100219091/why-rent-really-is-too-high-…

A situation created by the Socialist policies of Labour (100% house price increase nationwide) and National (nationwide 50% house price increase) giving excess privilege to house owners by encouraging foreign capital to pour into mortgages (and bringing in lots of new low skilled workers to keep wages down).

As bw pointed out above, the settings favour low productivity investment. Why am I calling these policies Socialist you ask, surely that's a good thing? I guess I mean, deluded in intent. They attempt to fix a real problem but end up being a band aid that does not identify the cause or deal with it, and you end up being a useful idiot for someone else, in this case the banks.

https://en.wikipedia.org/wiki/Useful_idiot

Please note the delight in the prospect of bloodshed, Lenin was a mass murderer by choice, in short a nasty bastard, not a nice guy at all, but somehow we still allow his polarising and destructive thinking to contaminate our own, despite the appalling suffering it causes.

Nasty bastards can be found just about anywhere on the political spectrum, especially when you get into the authoritarian part of it, Augusto Pinochet springs to mind for a kicker.

I couldn't agree more. They are the enemy of a civilised society.

My comment was to beware the wolf in sheep's clothing as we deal with the inevitable swing to socialist thinking brought about by the gross incompetence of both political parties and their advisors when it comes to housing. There be dragons and they are like a thought virus in our heads.

My general viewpoint is that the people are best served when government allows them to by and large make their own free and unforced choices as seems best to them. Government achieves this by adjusting and adapting the rules to prevent undue privilege accruing to any one group of the many special interest groups that exist. Standing above this, however, are the issues that pertain to preservation of the society from outside forces that seek to destroy it. It ain't easy and solutions based on More Central Planning are always seductive in their simplicity.

Dictators are the visible face of a regime.

I read this last week. I wonder if people are so different?

By nature, horses instinctively seek leadership. Leadership involves choosing the direction for the group and providing security to all others in their herd. Leading horses are usually calm, stable and wise. A leader can be an older mare, and she helps to keep the other horses safe and lead them to food. The other horses respect her very much for her wisdom, experience, guidance and providing safety. Her wise decisions to travel to food and water or to run in case of emergency literally mean the difference between life and death.

I don’t find those qualities in a 37 year old accidental prime minister who has yet to prove her wisdom and don’t want NZ to be the guinea pig while she gets her experience.

Ex Expat, give the new Government a chance! After nine years on auto pilot, productivity, poverty and the housing crisis won't be fixed in a day! Stop complaining and embrace change like the positive person you claim you are.

https://www.radionz.co.nz/news/national/333086/nz-s-weak-productivity-i…

BTW, are you the anonymous individual whose ONLY criticism of our leader is that she looks like a horse? http://www.newshub.co.nz/home/politics/2017/03/jacinda-ardern-responds-…

If so, consider yourself relegated to insignificance!

Retired Poppy, I simply posed the question whether humans share the same need that horses do for leaders. I think they do. I challenge you to find any post I have made about the PM’s physical characteristics. It is your mind working overtime if you think there is a connection in this post.

You know I work in high risk company consultancy and you have apparently done the same in a bank. I’m better placed than most to see what puts companies in this situation and I see the same traits in this Government. Reckless spending. The only difference is that they can cover their mess with taxation. That’s why they deserve opposition at every turn, in my opinion. There is absolutely no obligation on my part to give them any chance. My objective as a paid up National Party member is to see them out of power and I will highlight every mistake that they make and promise they break. It would be no different if National was in power and Didge etc were doing the opposition.

PA, You have to ask yourself what sort of personality wants to be a politician in the first place. Terribly cynical I admit but if they ran a suitable psychological test on most politicians it would reveal that having power over other people was a big percentage of their psyche. Nothing new, been like that since before recorded time.

That's the massive problem with the system. It self-selects for shallow used-car salesman types who want power and can turn on the superficial charm long enough to convince the rubes. Sometimes I think we'd be better off conscripting the people who won't put themselves forward, like for jury duty. At least that way the percentage of venal narcissists won't be any higher than in general population, and we'd get a few competent introverts to actually get shit done rather than basking in the limelight.

When is the 6 o'clock news going to have the smiles of young couples and families walking into there new, sparkling, healthy homes? With the Labour minister benevolently looking on. Can't wait to see the reaction of the Nats. Of course they "were doing it already". Not.

Good question. Hopefully I am wrong and they will prove my cynical suspicion of their ability to actually deliver to be completely based on my own personal delusions.

The thing that gets me is that house building is a really, really simple bit of manufacturing, so why is it so dysfunctional? If aeroplanes were built like houses then most of them would crash.

The thing that makes it all the more frustrating is that they should only take a few days to build, like 7 days.

https://www.youtube.com/watch?v=5Npxw3WHO1s

https://www.youtube.com/watch?v=rwvmru5JmXk

New sparkling healthy homes like the ones been built as affordable housing in Queenstown - $449,000 for a 44sqm 1bedroom house with a kitchenette?

https://www.odt.co.nz/regions/queenstown/workers%E2%80%99-affordable-ho…

In Auckland 6x7 m is called a shoe-box as student accom.

And guess who pops up - Shamubeel Eaqub - budding property mogul

Queenstown's first major affordable and worker housing complex has been approved.

In a resort desperately short of reasonably-priced locals’ housing, developer New Ground Capital (NGC) has the received resource consent from Queenstown Lakes District Council to accommodate about 600 people on the Frankton Flats.

Here is New Ground Capital

http://www.newground.co.nz/about/

Good on New Ground. All power to them. New Zealand needs a lot more of them. If the multi residential property owners could cash up on all the (foreign) capital gains they have enjoyed, and start investing "for real", rather than sitting tight on a retirement fund, - the ground might start to shift. Mum and dad Landlording looks very unambiguously unproductive. Just don't ask me to. Too much risk.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.