Today's Top 5 in tax is a guest post from Andrea Black, who is a tax commentator at letstalkabouttaxnz.com and was formerly the Independent Advisor to the Tax Working Group.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz.

And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

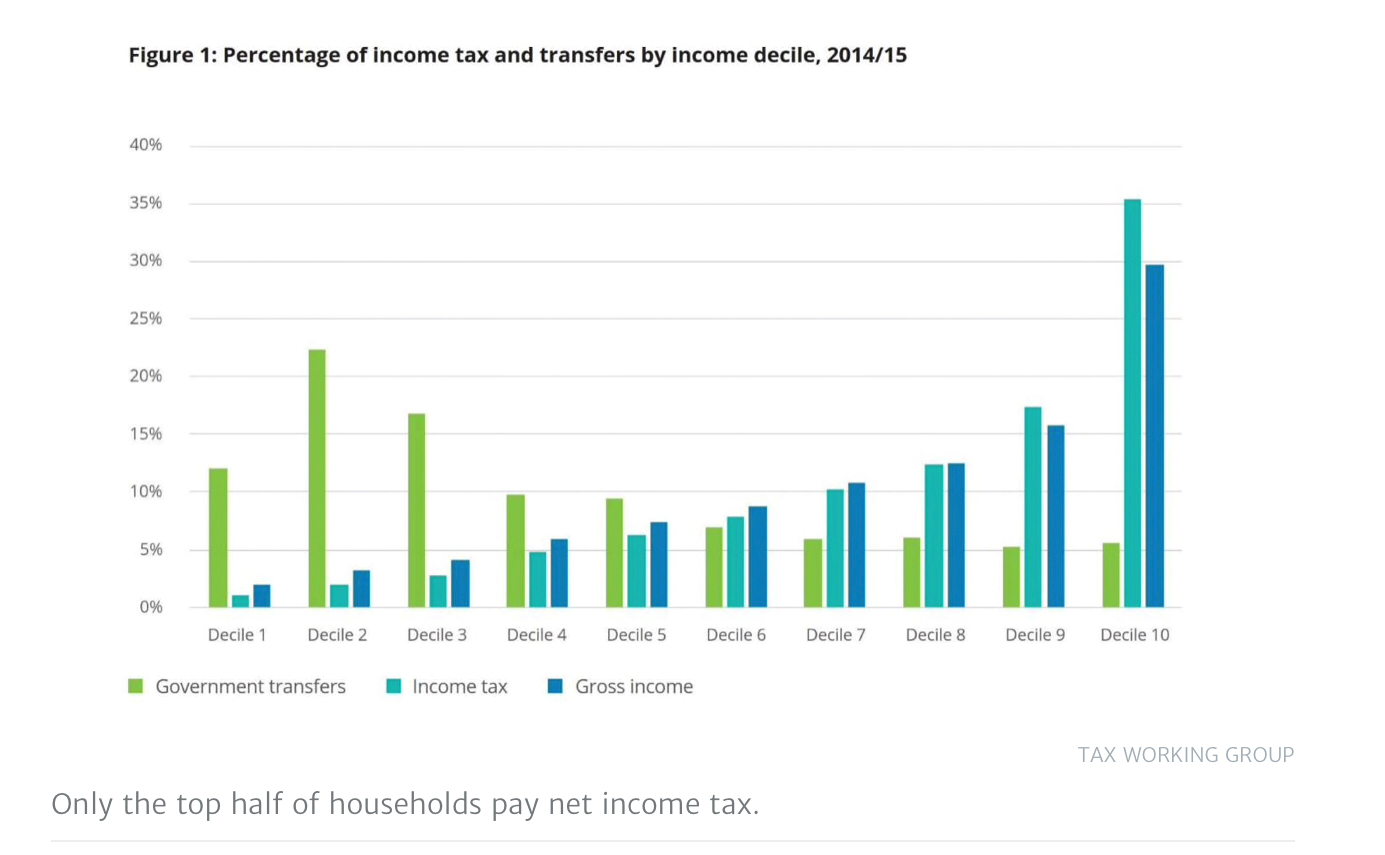

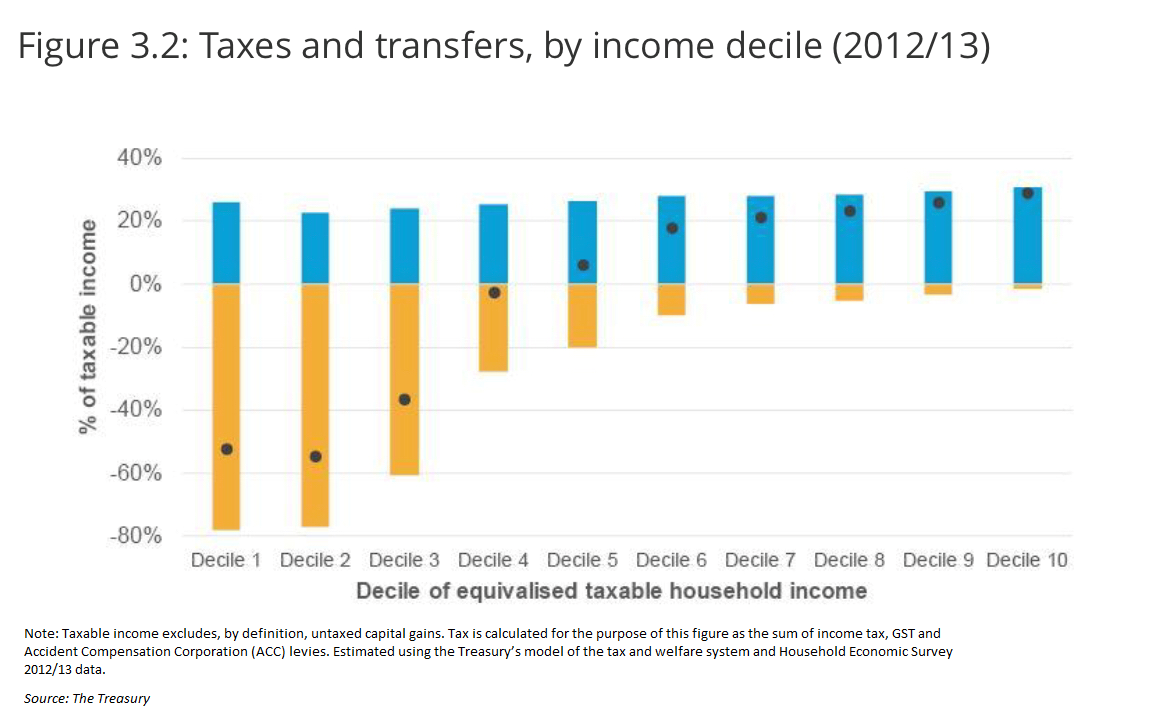

1. Income tax is progressive but the tax system isn’t.

This came up in a recent exchange on Stuff between Thomas Pippos Tax Specialist and CEO of Deloittes and Michael Fletcher Senior Researcher for Institute of Governance and Policy Studies and former Independent Advisor to Welfare Expert Advisory Group.

In his article Thomas showed that a very small proportion of taxpayers paid most of the income tax and then argued that the fact this group would also have a very modest level of untaxed capital gains was not significant.

As an aside I am not sure I would agree. My view is that a small group pays most of the personal income tax because they have most of the personal income. I don’t see that as a reason to give anyone a free pass on not taxing other forms of personal income such as capital gains.

But in the course of the article Thomas noted that “New Zealand already has a very progressive tax system. A small group pay the vast majority of all income tax”. Michael Fletcher disagreed and pointed out that the Tax Working Group had in fact said that “Overall, relative to other OECD countries, the tax system is not particularly progressive."

So how is it that two smart intelligent people could come to polar opposite views looking at the same information?

The difference between the two gentlemen is GST. Thomas is looking at income tax and he is right as far as income tax is concerned. When GST is brought in Michael is then right.

I find this all fascinating as it reflects how my view of the tax system changed in the course of the Tax Working Group. I had spent my life in income tax and – other than the trust and company rate which I accept are material – the personal tax scale is indeed progressive.

But when GST – and ACC – are brought in – the tax scale flattens significantly. And would flatten further if untaxed capital gains – no matter how modest – were also brought in.

2. Tax efficiency still lives even in a world of tax fairness.

Efficiency and Equity are two of the key touchstones for tax policy. Efficiency in the sense of minimising the effect tax has on economic behaviour and Equity in the sense of all sources of income should be taxed the same (horizontal equity) or that tax should increase as income increases (vertical equity).

In domestic taxation there is rarely a tradeoff between the two concepts and was why all of the Tax Working Group agreed that at least the capital gains from residential rental property should be taxed. It wasn’t fair that this income was untaxed while income from employment was and it was also inefficient to have capital being allocated in to this asset class away from asset classes that were subject to tax.

In international tax it is less clear.

Where the income wouldn’t be taxed offshore there is an argument that it is inefficient to tax it in New Zealand. This is the basis of lower rates of taxation on interest paid to non-residents as well as other situations like profits of the sales of shares by foreign venture capitalists. These are cases where to impose tax would either bounce back on to the New Zealand payer or investor or the investment might not arise at all. So it is efficient to tax the income paid to foreigners differently to that paid to residents.

And this was very much the received wisdom until the public campaigns on making Multinationals pay their fair share started. All the building blocks of the ‘not paying their fair share’ started life with an efficiency argument.

So with all the rhetoric around tax fairness and multinationals it was interesting to see Henry Cooke’s recent article in Stuff showing that the Government renewed a tax exemption for oil rigs. The argument is that without the exemption there would be less activity, higher costs and less tax revenue. I have serious concerns about the latter but the other two are efficiency rather than equity or fairness arguments.

Alongside efficiency concerns are also often ones of compliance cost.

The GST and low value goods was hailed primarily as an initiative to make the tax system fairer. Why should goods bought from local retailers be subject to GST while imported goods be exempt from tax? And while that is largely the case with this change, a recent Listener article has set out that not all suppliers will have to register and combined with an increase in the tax free threshold; some of the previous unfairnesses will become worse.

The increase in the tax free threshold, albeit only for goods for unregistered suppliers and contrary to the advice of the Tax Working Group, would have been for compliance and administration cost reasons. Every time a parcel is held up at Customs, it causes cost to Customs and inconvenience to consumers as their parcels get held up.

But the tradeoff is fairness. As people with parcels from registered suppliers will be now paying GST from the first dollar while parcels of $1000 or less from unregistered suppliers will pay nothing.

3. Or does it?

But on the other hand we have the Digital Services Tax which Amazon has recently said it will pass directly on to consumers. Here efficiency being traded off for fairness.

Previously I have been underwhelmed by the digital services tax for two reasons. First it only taxes digital services and secondly I thought, conceptually, it taxed the wrong people.

A digital services tax applies to the data and digital services provided rather than goods and services generally. So it will apply to the platform charges of AirBnB but not the provision of accommodation – that should already be taxed. It won’t apply when I buy an iPhone from Apple and it won’t apply to my monthly charge to use Word on my iPad. Yes GST applies but the DST won’t.

When I talk to people who are concerned about multinationals not paying their fair share they are always talking about the profits of the multinationals not particular types of profits. They are worried about Apple, Amazon and Microsoft as much as Google, Facebook and YouTube.

While there are policy reasons to target digital services only, as this is a tax for fairness not efficiency reasons, I am concerned it still won’t fully scratch the itch of the general public.

However, I must say I am fascinated that Amazon will be paying this tax. I guess its hosting other suppliers is more significant than its own selling of goods. Or maybe it is the data it now holds on our spending patterns.

The other reason I have been underwhelmed by the DST is that yes, users, data, and networks create value for the Tech giants but that value arises from the provision and use of a free service – Facebook, gmail, Google etc. So, value in but also value out. The people who are actually net benefiting are the users who are getting a service for free.

This free service is analogous to the free rent that home owners with no mortgage get – aka an imputed rent and the associated arguments for taxing it. That is the paying of rent is not deductible but the receipt of rent should be taxable.

So strictly speaking if anyone should be taxed it is us users on the value of the free service we are receiving. And of course that won’t happen anymore than imputed rents will become taxed but it does raise questions on the tax’s underlying rationale.

Or so I thought.

This was all before I watched The Great Hack that has just come to Netflix. No irony there. Holy Moly. Looks like the value to the firms far exceeds the value provided to the users of the free services. So I might be retreating to my first concern plus of course the risk of retaliation from the US.

4. Capital gains taxation still lives even though more capital gains won’t be taxed.

In the spirit of our tax system trying to apply rules to new technologies that weren’t around when the original rules were written, Inland Revenue has recently released two rulings on crypto currency given to employees in various forms.

The Tax Working Group received an excellent presentation from Rachael Gemming when she was at Inland Revenue – now at EY – on the issues and permutations with this asset class. (The actual presentation is mislinked to this submission but this is a good proxy of her advice.)

This all then fed into guidance from Inland Revenue on whether gains from sale of cryptocurrency were subject to tax. Unsurprisingly the Department concluded that gains on sale were subject to tax in situations where there was no income as this would indicate the cryptocurrency was purchased with the intention to resell. IR also concluded that any businesslike activity to generate these assets would be taxable.

So, even though the Government has decided not tax any more capital gains – the existing law is unchanged. This means that capital gains can still be taxed as income when they are part of a business or the underlying asset was bought with the intention of resale. And assets like cryptocurrency that have no income stream will be caught squarely within the existing provisions.

5. What’s happened to the Tax Advocate?

The Small Business Council gave its report to the Government a week ago and last week the Government released its Tax Policy Work Programme. Interestingly in the work programme is a reference to the Tax Working Group’s recommendation for a tax disputes for small taxpayers. However, the actual recommendation of the TWG was for truncated dispute rules for small taxpayers after the introduction of a tax advocacy service.

The concern behind the original proposal in the interim report was that small taxpayers when they find themselves in dispute with Inland Revenue will concede, rather than engage in the dispute process, as the costs of pursuing the dispute outweigh any tax under dispute. The integrity of the tax system suffers when it is only people of means who are able to engage or dispute decisions of Inland Revenue.

The Tax Working Group saw such a service as being independent of Inland Revenue possibly as a Departmental Agency which would report to the Minister rather than the Commissioner. This would also have the advantage of being able to provide the Minister alternative advice from the perspective of the small taxpayer.

The Minister himself indicated he was interested in the idea. Let’s hope it it in the Small Business Council’s report.

5 Comments

Re DST: "... the value to the firms far exceeds the value provided to the users of the free services".

This is simply the old adage restated: if you cannot discern the 'product' being accessed for free, You're the Product......

New Zealand is a great place to make tax free capital gains. Seems crazy that more New Zealand businesses don't see international growth as tax efficient, preferring instead to sell out to overseas owners for a smaller big pay day. Big lost opportunity to NZ business owners and the country's income. Why not offer some extra carrots to NZ business owners to do so.

Swear words were invented to describe people like you. You miss the whole point of taxes. The only reason they exist is to fund government expenditure. No tax is fair. If all government expenditure could be paid for with a 5% tax on lawyers, then that is all we would need. But to curry favour with all the Pauls who want to have their expenses paid for by the Peters, government after government has cranked up taxes until we are paying practically 50% of our income, more if local body taxes are included. No wonder we get a bit upset when governments make us pay tax on income we have not earned, (provisional) and makes us pay tax on this months income, but refuses to let us deduct this month's expenses (capital expenditure).

GST was the biggest scam of the lot. Dodgie Rodgie lied to us and said that every dollar of GST collected would have a corresponding dollar dropped from our income tax. What a barefaced lie. Perpetuated by every government since.

Now these "experts" come out from everywhere to make out that taxing Capital Gains is the way to go. Half of them say that deducting corresponding capital losses cannot possibly be a goer, showing their total lack of understanding of how business expenses work. Then they wonder why people do cash jobs. If the governments had kept their expenses to what they were when income tax was invented as a temporary measure to pay for World War One, we wouldn't have such ridiculously big government, we wouldn't need people dodging taxes whenever they can, and we might have more people looking after themselves, their families and their neighbours than we do now.

One more thing. Could someone please confirm that if I buy cryptocurrency and sell it for less than my purchase price, I obviously claim the deduction off my income taxes. The only correct answer is either, "Yes", or "No".

The previous tax working group advocated a land tax. Its least-bad in terms of impacting behaviour (efficient), yet also highly progressive (unlike GST). Its also a tax on wealth that's difficult to avoid. For those worried about bigger government: offset a land tax with lower income taxes to make the reform package revenue neutral.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.