There’s a question I’ve been asked more times than I could possibly count during my time writing about things financial.

It’s along the lines of: What is the broader impact – if any – when a company’s share price falls substantially?

It’s a question with many answers. Often the answer might actually be: Not much.

Or, it can be: A lot.

If you apply that question to Fonterra, then I would have to say that, unfortunately, for Fonterra shareholders, the ramifications of a falling share price right now are potentially pretty serious.

And I reckon this is something being broadly overlooked in the recent discussion about the travails of our country’s giant dairy co-operative and its upcoming large financial loss to be announced next month for the year ended July.

The Government’s seemed to view the situation as a question of whether the corporate entity of Fonterra needs bailing out and whether that would be appropriate.

That’s missing the point.

The more salient issue surely is whether the dairy farming sector itself might ultimately need bailing out if Fonterra can’t get itself back more on an even keel.

Is that a little melodramatic, you say?

I hope it is.

It might well not be though.

I cite as some evidence the rather extraordinary statement Fonterra CFO Marc Rivers made through the NZX on July 5 after the Fonterra share price had tanked seriously the day before, at one point dropping from $3.75 to $3.45.

The first thing to note is that it’s pretty unusual for a company to comment directly on its share price, unless it’s specifically asked to do so by the NZX – if for example there’s been a sharp movement in share price for unexplained reasons.

There’s no indication Fonterra was asked for any such explanation – it just chose to give one. (Normally if the NZX has enquired about a share price movement, the NZX will also publish the inquiry on its site – and there was no such inquiry published in this instance.)

So, Fonterra’s key finance man commented on the share price. In amongst comments to the effect that Fonterra was striving to improve its financial position and reduce debt there was this quote from Rivers that I think is the key:

“While the share price does not impact the Co-op’s balance sheet or our ability to operate and pay our bills, it does impact our farmers’ balance sheets.”

Yes, that’s right. A tanking share price might have ramifications for farmers’ debt loads. Rivers knows this. And he's worried.

How many farmers directly use Fonterra shares as collateral for loans? And how’s that security looking right now?

Any bank that’s loaned money to a farmer with Fonterra shares as at least part security for the loan might be feeling a little queasy.

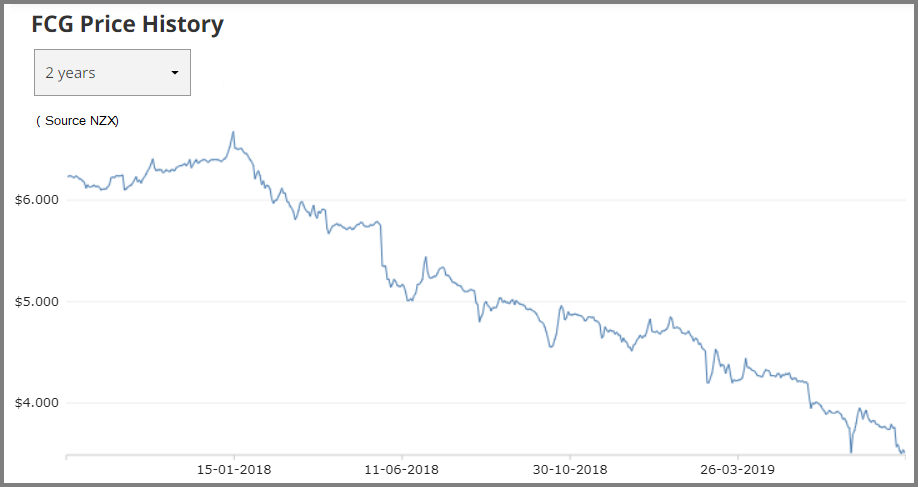

The Fonterra share price was $6.39 at the end of 2017.

It then moved up to as high as $6.68 on January 12, 2018, but has been on a downward trajectory since.

It’s worth noting that when Rivers made the statement to the NZX on July 5 it was in respect of a share price that had hit a low of $3.45 the previous day.

On Monday Fonterra Co-op Group shares closed on $3.50. The associated Fonterra Shareholders Fund Units that offer non-farmers a chance to share in the financial performance of the co-op also closed on $3.50.

So, the share price is still at levels presumably Fonterra - on behalf of its farmer shareholders - is very uncomfortable with.

At recent prices the Fonterra shares are down about 47.5% in the past year and a half.

That’s a serious drop in the value of security.

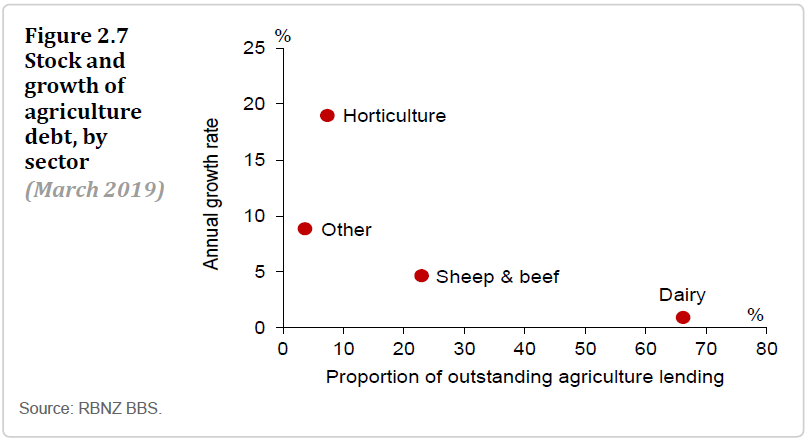

According to the most recent RBNZ monthly figures on sector credit, there’s $63.6 billion of outstanding agricultural debt.

And according to the RBNZ’s most recent Financial Stability Report in May, dairy debt accounts for about two thirds of the agricultural debt.

That means about $42 billion of dairy debt.

That’s a lot.

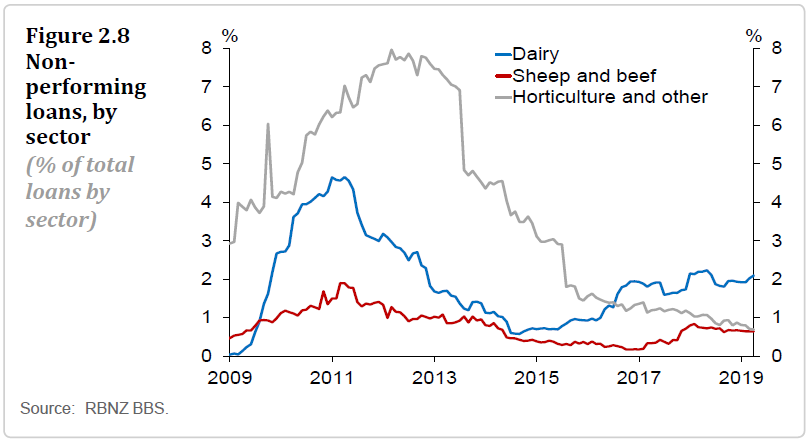

In that last FSR in May the RBNZ noted that most dairy farms have been profitable for the past three seasons as dairy prices and production have been good.

“…But some farms struggle to make profits at current prices, particularly those with large debts. Around 35 percent of dairy farm debt is to farms that have more than $35 of debt per kilogram of milk solids (kgMS) produced annually.

“On average, these highly indebted farms require a price of $6.20 per kgMS just to break even.”

Fonterra currently forecasts a price range of $6.30 to $6.40 for the past season and $6.25 to $7.25 for the season that’s now under way.

The RBNZ went on: “Banks have so far taken a long-term view in supporting stressed dairy farms and working with them to strengthen their financial positions. But given its high debt levels, the dairy sector is susceptible to higher interest costs or working expenses, and to changes in banks’ business practices.

“Vulnerable farms must reduce their debt to improve their resilience to future downturns. However, options for addressing problems at financially stressed farms appear constrained at the moment, as demand for dairy farm land is low.”

See that quote there? The sector is susceptible "to changes in banks' business practices".

Clearly there is concern that the banks might change their tune.

What happens if the banks start seeking more security for loans? Or if they start resisting on refinancing?

The banks have shown restraint to this point. But they are not charities. They want the money they loan back and get nervous if they think there’s a chance that might not happen.

The upshot is that if enough farmers start getting put under pressure from banks – then that probably does become a Government issue.

It’s no longer about Fonterra. It’s about a hugely important industry for New Zealand and is about livelihoods.

What does Fonterra need to do?

Under its new leadership there’s no doubt Fonterra is earnestly setting about cleaning up its mess.

The problem is, once you start really looking under rocks you discover more and more bad things. And so that seems to be the case for Fonterra.

It probably surprised nobody that Fonterra discovered more problems with its fanciful offshore assets.

What will have shocked is the fact that around $300 million (Fonterra rounded it to $200 million by adding back in the $100 million profit on sale of Tip Top Ice Cream) has had to be written off the value of NZ consumer businesses.

This suggests that while attention has been distracted by the offshore follies, serious traction has been lost in Fonterra’s home market. Unchecked such a loss of traction could be pervasive and threatening for the whole business.

And while the writing down of asset values is always described by companies as “non-cash” that is, while true at face value, somewhat misleading as well.

'Real' losses

The fact is a company’s required to look at the value of its businesses and brands and if the earnings from those businesses and brands are not matching the valuation the company has for them – well, then write-downs are necessary.

And while that’s ‘non-cash’ it’s very real. It’s a real loss of shareholder value. The company values those parts of the business at less than it did before because they simply aren’t worth as much – and its shareholders’ funds that are cut. It’s a real loss of value.

In the case of the valuations of the NZ consumer businesses, Fonterra’s effectively saying that shareholders would now get $300 million less if those assets were sold up and the proceeds returned to them. So, the loss is ‘real’ all right.

So, Fonterra needs to keep cleaning up the mess. But, I think it needs to do much more than that.

If all we see from Fonterra’s board and management over coming months is continued write-downs and restructuring and chopping of things then this will be debilitating.

As difficult as it might seem for Fonterra at the moment, the co-op needs to articulate a plan. And soon. How can it go forward from here?

It needs to say how it is viewing itself. What is Fonterra? What does it plan to achieve? How will it be structured? And how will it get to where it wants to be?

Vital step

The talk about capital structure that’s apparently been restarted at board level is an essential first step. Fonterra needs to work out some way of accessing more capital. And that’s not a fanciful thing. It needs to do this. Otherwise it’s in serious trouble.

It might be too much to expect any fully formed strategy to come out of Fonterra in time for the annual result announcement next month. But I reckon it needs to be pretty soon after that.

There needs to be some confidence flowing back into the market.

And if there is some confidence, maybe the share price might perk up.

And that might take some pressure off. Farmers happier. Bankers happier.

But there’s a heck of a lot of ‘ifs’ here.

Not much time

I don’t think anybody involved has got a lot of time to sort this out.

And if the Fonterra share price keeps flagging. And if farmers are being put under intolerable debt pressure. Then something might give.

Which is why we can’t rule out the possibility that the government may yet have to move in to bail out – not Fonterra as such – but New Zealand’s dairy industry.

I think it is that serious.

How the hell did we get here?

Well, recriminations later.

Let’s fix this.

26 Comments

If Fonterra shares are used as security as part of overall farm financing, then that introduces serious concentration risk. Apparently Fonterra still have 24 staff on >$1m base salary. So at a collective level I struggle to have any sympathy for dairy farm owners. They are the shareholders, they appoint the Board and they let this mess metastasize under their watch (and they missed the A2 phenomenon).

Also, the New Zealand Dairy Industry is not Fonterra. Or is it?

I have plenty of sympathy for dairy farmers wrapped up in the M. Bovis saga.

I don't have much sympathy for dairy farmers leveraging off the share price of their Fonterra shares. To do what? Buy the neighbours farm? Big risk, big rewards and potentially big losses.

If Fonterra losses are an issue, why is their no discussion on Foreign Bank profits taking $5 Billion profit per year offshore.

THis is a far bigger annual loss to the NZ economy, and yet its met with silence, or worse, when the FOreign Banks profits are announce in the media as a record, its hailed as a great success story.

For who.

We all pay into the Foreign Bank rort, while Dairy Farmers basically work damn hard dusk to dawn to become NZ's largest exporter at $20 Billion p.a.

So how can Foreign Banks at $5 Billion profit p.a., make 10 times more than our largest exporter.

This might be one of the reasons the farm payout is so low, we're being income stripped by Foreign Investors who care little about the country making the profit, as they have a mortgage which has little risk v the land owners equity which can evaaporate in an instant.

It should be the other way around, Fonterra (NZ) makes $5 Billion and Banks make $500 million.

Imagine the health care, police and roads that could buy the country.

There is no logic in your hypothesis whatsoever. For a start, the $5b (it’s not $5b by the way as some earnings are retained) is earned across a wide range of banking activity unrelated to dairy. Bank dividends accrue to those who provided the capital, sometimes referred to as capitalism. There are New Zealand capitalised banks but New Zealanders do not support them in sufficient numbers, they will go with ge best price every time. Who do you bank with?

Here's the logic buried deep beneath the layers of the NZ Investment Account Deficit.

The reason NZ businesses just might be struggling to profit may have something to do with the $20 Billion surplus Foreign Owned Companies including Banks are generating out of NZ business through super profits that we have been slowly rorted with over the last 30 years, which would tally to $600 Billion missing dollars from our economy at todays value.

This is a massive hit to a small fragile economy that has rolled over to Neo liberalism like a puppy getting a belly rub from the World Financiers to do their bidding to create their huge rewards from lil ole NZ.

Who got the belly rub to allow asset sales offshore to such a massive level, now that is the question that has no logic.

" Fonterra needs to work out some way of accessing more capital. "

First they need to be open about where the capital they have accessed previously has gone, in the last ten years or so 300 million kgs MS increase in supply has meant share purchases of near $2b plus the $500m share float which then is leveraged to $5b or more with the 50% debt/equity.

Fonterra has never had a problem accessing capital just a problem saying where it's gone.

Fonterra needs to work out some way of accessing more capital.

It is interesting in hindsight to look back on TAF and what it was championed as bringing to the cooperative, for example:

The security from the changed capital structure [under TAF] will enable Fonterra to pursue its global ambitions which include increasing the proportion of milk produced on overseas farms that it owns, notably in China where it has just announced two more dairy farms west of Beijing. It can also increasingly make selective processing investments, as it has in Sri Lanka where it processes local milk and produces yoghurt, and Chile.

https://www.interest.co.nz/rural-news/61887/fonterras-trading-among-far…

When you are in the business of land banking on the back of tax free windfalls, you do not get a bailout.

“…But some farms struggle to make profits at current prices, particularly those with large debts. Around 35 percent of dairy farm debt is to farms that have more than $35 of debt per kilogram of milk solids (kgMS) produced annually."

“On average, these highly indebted farms require a price of $6.20 per kgMS just to break even.”

yep. 2010 article -

"The idea that businesses should generate a return sufficient to cover the cost of capital doesn't seem to apply to farming. That is, the yield most farmers and horticulturalists achieve does not cover the cost of fully funding the market value of the assets they purchase".

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=10…

One of your points, about the share price putting farmers in trouble is actually a huge success.

A purpose of TAF was to shift the redemption risk from Fonterra books. It worked but of course most were blind to the fact it shifted elsewhere and the sellers of the scheme at the time weren't going to say.

Well here it is.

Excellent questions put here David.

What if banks change policy on re-financing?

Look at what is happening in Australia to RE where just that is happening.

Debt is not an endless party and as you suggest, if its leveraged against share price, dangerous policy

... absolutely no sympathy for Fonterrible . . and no bail out !!!

Back in the day when the Commerce Commission recommended against Fonterrible being allowed to form as a farmers co-op , a few of us predicted the dire outcome if the government overruled that finding ... Helen Clark overruled the CC . ...

.. the rest is history . . A series of production bungles... idiotic wastage of money on offshore investments ... over payment to farmers . . And multimillion dollar salaries for many within head office . ..

That's what it looks like from the outside looking in. Also, you can add in the negative externalities of dairy in general and, specific to Fonterra, they missed A2.

GBH. I heard through the grapevine that the executives at Fonterra (and Fletchers and the ACC) were all reading the recently released book from an American Management Guru (but I forget his name) called "You deserve it: How to Feather your Own Nest in a Rudderless Corporation".

I wouldn't mind getting hold of a copy if anybody knows where.

GBH. I heard through the grapevine that the executives at Fonterra (and Fletchers and the ACC) were all reading the recently released book from an American Management Guru (but I forget his name) called "You deserve it: How to Feather your Own Nest in a Rudderless Corporation".

I wouldn't mind getting hold of a copy if anybody knows where.

like I said, blood in the water

Nitrates in the water ...

24 people in Fonterra earning over $1,0m ................. geez , if this is true then the farmers should be outraged .

Just getting an understanding as to how anyone can 'earn' that and justify it in a co-op where almost all decisions are taken by committees , eludes me

... the benefit of a committee is that no one person can be held responsible for a decision that ultimately burns $ 1 billion of shareholders capital ...

But that any one if them can subsequently bugger off and collect a multi million $ golden milkshake...

I'd suspect many farmers would rather punch them in the face than shake their hand.

You bail out Fonterra, you will be indirectly bailing out the Banks.

Let the Banks also agree to an appropriate hair cut.

NZ dairy industry has been under threat ever since the sale of the Crafar Farms in 2010, at least.

It would be a great article to see where and why Fonterra has crapped out in the local N.Z market. If it cant sell milk here why for gods sake is it trying to big note it overseas!!

As bad as things might be, I refuse to buy any dairy products from foreign owned outfits, if I want to treat myself it's Lewis Rd, otherwise mainly Fonterra products. I refuse point blank to buy anything (so that is not just dairy) sold under the Goodman Fielder banner, I have no desire whatsoever to increase the profits of Wilmar, the world's largest palm oil processor who owns it.

There is the saying "pay peanuts and you get monkeys" but the way it works is that there have been very big peanuts paid at Fonterra and we just got fat monkeys.

The vast salaries and number of those at Fonterra is an absurdity. I think we could save some hundreds of millions. A maximum salary of $200 K, would result in a clearout of the bloated furry ones. And quite likely lead to a better selection of managers.

There are 6000 staff on >$100,000.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.