This Top 5 COVID-19 Alert Level 1 special comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Illustration by Cathy Wilcox, The Age.

1) Bloated bank balance sheets.

Financial results are due from several Aussie banks this month. Of most interest on this side of the Ditch will be the annual results from ASB's parent Commonwealth Bank of Australia on August 12. They come against the backdrop of Victoria's lockdown as the state battles COVID-19. Loan loss provisioning will be under the spotlight.

As banking analysts Brendan Sproules and Thomas Strong at Citi put it; Australia’s COVID-19 recovery has been derailed by the need to introduce a Stage 4 lockdown in Victoria until mid-September. The banking sector is thus in the eye of the storm.

For the banking sector, we believe the prospect of rolling lockdowns will likely result in 1) a persistent portfolio of loan deferments; 2) creating solvency challenges for small lenders; as well as 3) slowing the dividend recovery, as regulators seek even higher capital buffers.

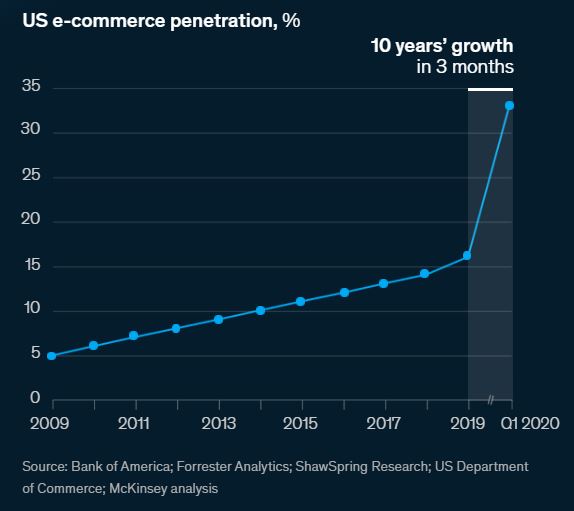

Sproules and Strong, who are based in Melbourne, also point out the COVID-19 crisis has blown out bank balance sheets. We've witnessed something similar in New Zealand with a surge in deposit growth and cautious lending.

Since the COVID-led crisis began, bank balance sheets have become bloated. The net result of slow lending growth and rising deposit has been a surge in liquid assets pooling on ADI balance sheets. In just 4 months of this COVID-led crisis has seen ~$145bn of excess deposits has been accumulated, as well as ~$95bn of short and long term debt repayment in just 4 months.

The bloated balance sheets will have serious implications for future revenue growth. A continuation of fiscal support programs, particularly in Victoria is likely to continue the trend of dampening lending growth and keeping deposit growth high. The structural nature of the build in system deposits means funding costs will be lowered as TD spread contracts and long term wholesale funding is reduced. Management forward statements on NIMs will be telling as it appears not to be included in FY21 consensus estimates.

[Chart removed at Citibank's request.]

In addition to CBA's annual results, ANZ will provide a third quarter trading update on August 19. That'll be preceded by one from BNZ's parent National Australia Bank on August 14, and one from Westpac on August 18.

2) A second Keynesian revolution?

I recently did a Zoom interview with Steven Hail, a lecturer at the University of Adelaide School of Economics and a Modern Monetary Theory (MMT) economist. Hail is a friend of Stephanie Kelton, professor of economics and public policy at Stony Brook University and author of the recent high profile book The Deficit Myth: Modern Monetary Theory and the Birth of the People's Economy.

In this Struggles From Below article Hail suggests MMT is a second Keynesian revolution.

There are many other differences between traditional Keynesian economics and Modern Monetary Theory. And yet there are enough similarities for us to regard MMT as, essentially, a second Keynesian revolution. Much that was taken for granted about economic management 100 years ago was challenged by Keynes in the 1930s. Something similar is happening now. The idea that central banks should be left to manage the economy is up for debate. The notion that governments in countries like Australia should balance their budgets or seek to run surpluses is rejected by today’s revolutionaries.

If the second Keynesian revolution is successful, journalists and economists will focus on inflation risk when discussing federal budgets, and will cease talking about budget ‘black holes’ or debts they claim future generations will have to repay. If a deficit is not inflationary, and if it supports the economy at full employment, its size won’t matter. The economic narrative will shift to the deficits that really matter, particularly the jobs deficit and the climate deficit. Then we can focus on what it will take to build a better and more sustainable economy after COVID-19 than the one that preceded it.

The pandemic has brought our economies to their knees; it’s through stimulating investment, as opposed to austerity-fueled starvation, that we’re going to get them fighting fit again—and a Green New Deal may well be the perfect mechanism by which to do that.

For those interested Steve Keen, the professor of economics who I interviewed in April, is recording 12 videos in which he builds a model of the "strictly monetary aspects" of MMT.

3) Are we still afraid to ask for help?

Back in May I spoke to Andy Hamilton, co-founder at small business support forum Manaaki and former CEO of The Icehouse. Hamilton has now posted this Manaaki Insights Volume One, July 2020 article on Linkedin.

One of the insights Hamilton highlights is business owners being reticent to ask for help.

Out of every 100 people who visit Manaaki, 99 consume content, and just one actually asks a question. Halfway through Covid-19, we added a feature where users could ask questions anonymously. And guess what – the number of questions doubled that week.

Insight: As Kiwis, we’re proud of our DIY mentality. But it can also hold us back. Believing we can handle things ourselves can stop us from asking for help.

Insight: Everyone’s reason for getting into business is different and deeply personal. They may be striving for fame and glory, carrying their family name, or just trying to make ends meet. That’s why asking for help can make people feel so vulnerable, and why many businesses ask questions anonymously.

Insight: Some people are happy to search our content to find the answers they’re looking for. Not all business owners are looking for exposure, in fact, most are not. It reminds us of conferences and classrooms when only a few people actually ask the questions, and that’s ok!

Challenge: How do we create environments where business owners can feel comfortable to ask for help, but if they don’t feel that way, they can still seek guidance or input?

4) History repeats itself in America where masks are concerned.

The New York Times has this fascinating article how, just as today, face masks took centre stage in political and cultural wars in the United States in 1918 and 1919 when the influenza pandemic swept across the country.

Sound familiar?

In 1918 and 1919, as bars, saloons, restaurants, theaters and schools were closed, masks became a scapegoat, a symbol of government overreach, inspiring protests, petitions and defiant bare-face gatherings. All the while, thousands of Americans were dying in a deadly pandemic.

There was even something called the Anti-Mask League.

As the contagion moved into its second year, so did the skepticism.

On Dec. 17, 1918, the San Francisco Board of Supervisors reinstituted the mask ordinance after deaths started to climb, a trend that spilled over into the new year with 1,800 flu cases and 101 deaths reported there in the first five days of January.

That board’s decision led to the creation of the Anti-Mask League, a sign that resistance to masks was resurfacing as cities tried to reimpose orders to wear them when infections returned.

The league was led by a woman, E.J. Harrington, a lawyer, social activist and political opponent of the mayor. About a half-dozen other women filled its top ranks. Eight men also joined, some of them representing unions, along with two members of the board of supervisors who had voted against masks.

“The masks turned into a political symbol,” Dr. Dolan said.

Wow – UK coal use has fallen to the lowest level in 250 years

— Simon Evans (@DrSimEvans) August 3, 2020

Amazingly, the 8m tonnes used in 2019 was similar to levels last seen in 1769

By wild coincidence, 1769 is the year James Watt got the first patent for his steam engine pic.twitter.com/zu9xLSS6Vp

Okay, so this one isn't related to COVID-19. Instead it takes us back BC (Before COVID) when we took international travel for granted. It's the staggering tale of how former Green Beret Michael Taylor organised the escape of ex-Nissan chairman Carlos Ghosn late last year, as told to Vanity Fair's May Jeong.

Ghosn skipped bail and fled to Lebanon, via Istanbul, from Japan, where he had been arrested for alleged financial misconduct at Nissan. The Japanese government has sought Ghosn’s extradition through Interpol, but Lebanon appears unlikely to hand him over. And Japan doesn't have an extradition treaty with Lebanon. For his troubles Taylor wound up in a Massachusetts jail, and says he hasn't even been paid, Jeong reports.

The Financial Times reports, however, that Ghosn made US$862,000 in wire payments to a company linked to Taylor's family, according to documents submitted to a US court.

Jeong details how Ghosn stood accused of a "staggering range of financial crimes." These include; underreporting US$80 million in earnings over an eight-year period, shifting more than US$16 million in personal losses onto company books, and using shell companies to bill Nissan for his lavish lifestyle. Nissan also claims Ghosn's mansion in Beirut was bought and renovated with almost US$15 million in company funds. (Ghosn’s Beirut house was reportedly damaged by the massive explosion there this week). Ghosn says the charges against him are part of a corporate plot, aided by Japanese authorities, to oust him from Nissan.

Ghosn escaped Japan by private jet on December 29 last year. The escape was some operation, as Vanity Fair details.

Taylor knew from experience that the biggest enemies on any rescue mission are the captives themselves, and their families. “Once they know you are going to help them,” he says, “they start telling you how to do things.” First Ghosn insisted on going by boat. Then he wanted to fly out of Tokyo. Then he demanded he leave immediately. There was “constant tension,” according to Taylor, and it took enormous discipline to remain committed to his original vision.

Throughout that fall, Taylor assembled a team of operatives with varying talents: maritime operations, airport security, IT, police, countersurveillance. It was like casting a heist movie, each man indispensable for his skill set. Most were ex-Special Forces, guys Taylor had known for 40 years or more. They had spent their lives operating in a world where people were contacts, groups of people were cells, and information was intelligence. Those who hadn’t met in the military had crossed paths in their civilian lives—skydiving at the local airstrip or moonlighting as coaches on the high school football field. The men had been trained to be fighters, and now that the War on Terror was ostensibly over, there was nothing left to fight for. Taylor’s cobbled-together ranks embodied a central Marxist concept—the reserve army of labor—and Taylor was in a position to put them to work.

The first call Taylor made was to a military officer in the Middle East who had retired into the business of gem appraisal. He would be Taylor’s deputy. Taylor also called a man he had been in combat with in Iraq who now provided private security. That man, well connected in Asia, assembled dossiers on everyone involved in the operation: Ghosn, his colleagues, his wife, the managers of every airport terminal that might provide an avenue of escape.

And then: the jet. Taylor needed to find a charter company that wouldn’t ask too many questions. His men began calling outfits all over the world, feeling them out. Could they handle a passenger who required a high level of discretion? Could the transaction remain off the books? Every place they called failed the test. Then they heard about a Turkish company rumored to have flown gold out of Venezuela in violation of U.S. sanctions.

A key challenge to be solved was how to get a VIP out of Japan who didn't want to be seen, and couldn't appear on the manifest. The solution? A box.

With the flight option secured, Taylor got to thinking about how he could smuggle a person across international borders undetected. “Eventually,” he says, “you get to a box.”

The box would have to be big enough to contain Ghosn and heavy enough to account for his weight. Taylor had one of his men measure the door to the cargo hold on the charter plane. Then he had a staging company in Beirut build two black plywood boxes with reinforced corners—the kind used to store and transport loudspeakers. He stipulated that the boxes be a centimeter narrower than the cargo door on the jet, so they could be loaded without issue. He had casters affixed for easy maneuvering and holes drilled in the bottom so Ghosn could breathe. Ghosn weighed 165 pounds. He would be taking the place of subwoofers in one of the boxes, and those weigh about 110 pounds. Close enough, Taylor thought.

Cartoon from The Week.

12 Comments

Sproules and Strong, who are based in Melbourne, also point out the COVID-19 crisis has blown out bank balance sheets. We've witnessed something similar in New Zealand with a surge in deposit growth and cautious lending.

Has government undertaken direct transfer payments to in need recipients' bank accounts? Has the RBNZ swapped excess settlement cash for government bonds which acts an offsetting bank asset?

Not sure about here but the bond rates started climbing in Australia so the RBA bought up bonds at a generous rate.

The capped 25 bps yield target 3 year note hardly moved up. There were other motives in play. RBA open market operations results

Must be some truth to the rumours of bad news coming up.

#2 one of the opportunities i see with adopting MMT is a move away from a dominating conversation about Government debt to a detailed analysis of Government policies, their effect, and effectiveness. The independent media and public scrutiny and analysis doesn't really happen as much as it should today because everyone worries about Government 'debt'.

"What are the effects beyond creating even more policy wonks and FTE in Wellington?" would crush most policy proposals at the first hurdle.

There is that risk, but why not building focus groups for a particular policy? Actively engage as many sides of the debate as possible to work on the wrinkles? So no more wonks than normal a Lead appointed and to build and consult with a focus group. For transparency that focus group are identified and their inputs a matter of record?

No credible economist is pushing MMT, it is the economic equivalent of "flat-earthers" or "anti-vaxxers", the sort of rubbish you can get away with in a post-truth world. You only have to look at Argentina (9 defaults) to see what happens when you print and spend, or Lebanon, or Zimbabwe, or . If you run long-term current and fiscal deficit's there is going to be a day of reckoning. Flick through these images for what MMT looks like.

https://www.gettyimages.com.au/photos/hyperinflation-germany?mediatype=…

Rubbish. The US has been 'insolvent' for decades. Along with many other countries. And there is no penalty to be paid it seems.

You can say it's coming, but is it? Do you actually know that? Or can they stave off hyperinflation forever?

I'm guessing Ghosn still got that strong plywood box. His villa in Beirut apparently not very far from water front and he survived the recent blast.

The Aussie bank results will be interesting, it's been a wretched and chastening 3 years for them, this is the crisis they never had in 08. They do not have the risk appetite or investment banking divisions that have plugged holes in the likes of HSBC and JPM results and 0% rates will hit profitability.

"MMT... journalists and economists will focus on inflation risk when discussing federal budgets, and will cease talking about budget ‘black holes’ or debt"

Actually this for me rephrases the MMT hype in a much more useful way. I can see it not as a toy for the government to use to have more freedom to spend as they choose, but maybe something that forces the government/economists/journalists to be more honest about what inflation and spending really mean.

However the fear of hyperinflation will possibly block any attempts to really explore MMT.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.