By Geoff Simmons*

ACT’s plan for tightening the purse strings may not return New Zealand to surplus as they claim. It could even send us into a debt-deflation spiral much like we saw in Greece. Right now, debt isn’t a problem, so the quality of public investment should be the focus.

ACT’s argument is that their austerity would allow the country to return to surplus, and would allow for tax cuts. But should we be in a hurry to get the government books back into surplus?

Should we be targeting a rapid return to surplus?

Early on, some were concerned that COVID would create a supply-side crisis. This is where the supply of goods and services is constrained. It can lead to inflation and in those circumstances austerity measures like ACT are proposing can make sense. A country needs to cut its cloth to suit its means.

That isn’t the case right now. So far, COVID is a demand-side crisis. The private sector is being risk averse and has pulled back from investing. The public sector is rightly stepping into the gap and investing in their stead - for example by boosting infrastructure spending.

Our Reserve Bank is pulling out all the stops to help keep demand going. They are desperate to keep inflation at the 2% target, and most importantly above zero. Interest rates are at all-time lows – Government borrowing has even gone negative.

Government debt was low before the crisis and the borrowing happening at the moment isn’t really a problem – especially compared to what we are seeing overseas. This is particularly the case since the Reserve Bank toolkit now includes quantitative easing – where they are printing money to buy Government debt off the banks. That essentially means that we owe this money to ourselves. The debt could disappear in an instant with the stroke of a pen (or touch of a computer key).

In short, ACT’s claim that the current debt increase is fiscal “child abuse” is not only inappropriate but also shows a complete lack of understanding of macroeconomics. It plays into the myth that a country’s budget is like a household budget, when it simply is not. Countries like New Zealand control their own money supply.

With all this in mind, there really is no reason for austerity for the sake of getting back to surplus. Until confidence recovers and the private sector is willing to invest again, it makes sense for the government to pick up the slack, and run some deficits.

So, what about tax cuts?

Tax cuts

ACT’s second argument (one shared by National) is that if the economy needs stimulus it is best to come through tax cuts. Their argument is that people know how to spend their money better than governments do. This position is largely ideological, rather than based in reality.

A far better approach would be to stimulate the economy through a Universal Basic Income (UBI). This gives everyone $250 per week, no questions asked. It can be funded via a 33% flat tax and the massive savings in bureaucracy it would generate. To provide a stimulus the UBI could be temporarily higher, or the flat tax temporarily lower. This would provide a modern, simple and fair tax and welfare system.

Firstly we know that tax cuts – even those designed by National and ACT to target middle income earners – tend to benefit those on higher incomes the most. We also know that those on higher incomes are far more likely to save their tax cuts rather than spend them. This is even more likely in current uncertain times. If your goal is to stimulate the economy that isn’t hugely helpful.

One key aspect of the UBI is that people keep it if they work. Unlike raising benefits, this gets rid of the welfare trap and makes work pay. As a result, a UBI would massively benefit the working poor. Someone on the minimum wage would get about $6000 per year more, taking them over the living wage. Remember that 40% of our children growing up in poverty are in working families, and these people are very likely to spend any extra money they get.

ACT’s answer to the welfare trap is to create an even more punitive welfare system. They want to micro-manage what beneficiaries spend their money on, creating even more stigma and bureaucracy than already exists in the welfare system. That means spending even more taxpayer dollars on pointless paperwork.

This brings us to the final question: Do people know how to spend their money better than the government? Surely that depends on the quality of government spending. And this is where ACT does have a point.

Quality of spending

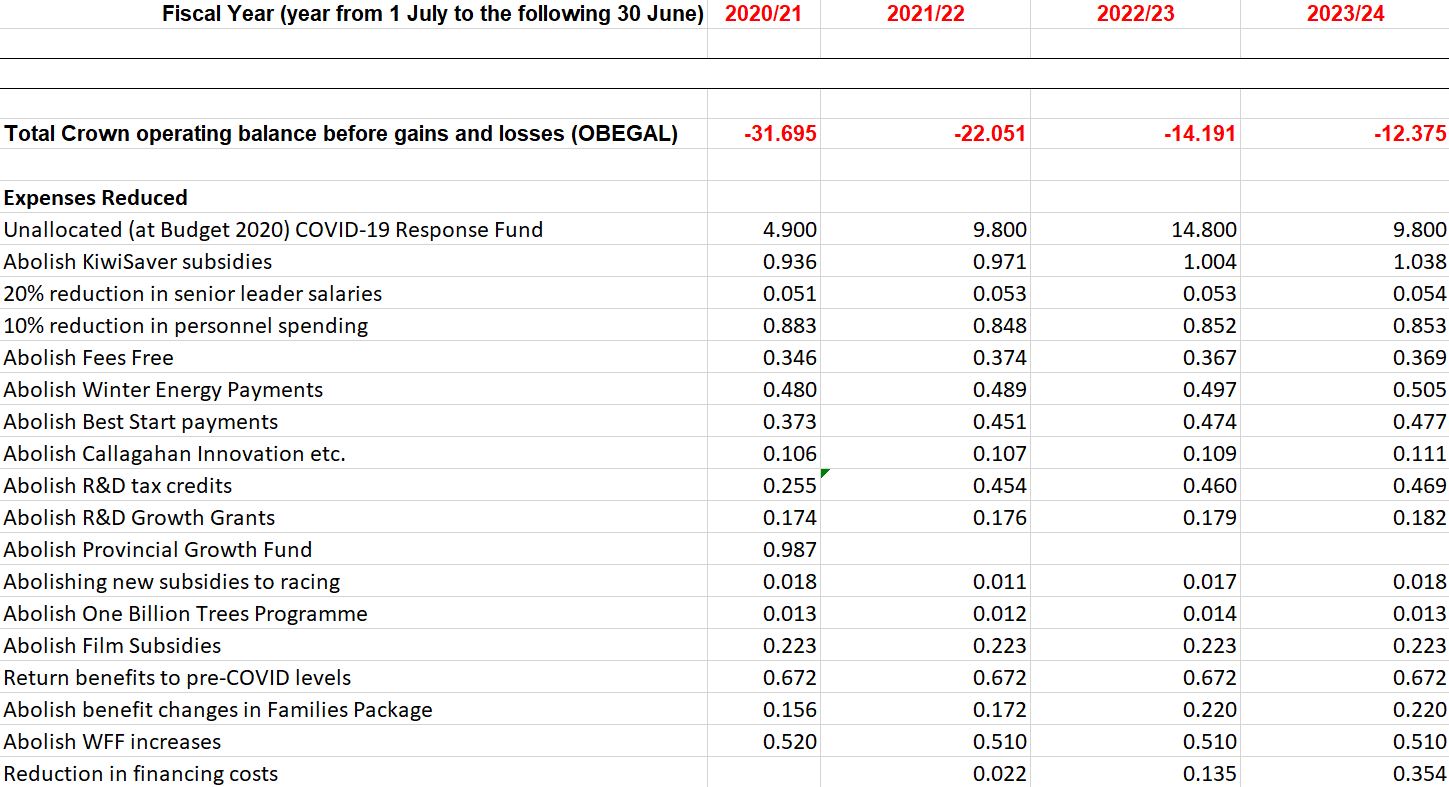

There is a lot of poor-quality government spending that could be dispensed with. ACT pointed out some easy wins like the Provincial Growth Fund and Racing Subsidies, but many of their other proposals would cause some real issues.

They would abolish fees free tertiary education and reintroduce interest on student loans. Without something like a UBI to counter this it would be real blow to students. Likewise they would slash benefits, abolish Best Start and Working for Families increases, which again without a UBI to offset, would be a blow to low income families. Kiwisaver subsidies would be gone, and given the state of our tax system, so would any incentive to invest in anything other than housing.

Perhaps most concerning of ACT’s targets is Research and Development tax credits and grants. Now again some of our Innovation budget could certainly be better spent, but slashing it wholesale would pose a real threat to New Zealand’s long-term growth. Here's a snippet of ACT's budget:

There is plenty of poor-quality government spending that could and should be reviewed. But there are also many important things that the government could invest more in. Early childhood education is a good example – it gives the best returns on investment across education in terms of improving both equity and lifetime outcomes. Primary and preventative healthcare is another great example of where money could be usefully invested. ACT chooses not to look at those, presumably for ideological reasons.

Instead ACT are choosing to swing the axe indiscriminately in a vain attempt to free up money for tax cuts and to get us back to surplus. This is a high-risk approach, given what might happen.

Could the ACT approach lead to a debt-deflation spiral?

The worst-case scenario here – the one that the Reserve Bank is working to avoid at all costs – is deflation. This becomes a self-fulfilling prophecy as spending dries up, businesses fail and prices continue to fall. When prices start falling people hold off spending as they might get a better price tomorrow.

Falling prices and rising unemployment then start to put pressure on wages to fall as well. When incomes start to fall, we enter the debt-deflation spiral. In normal times people can count on inflation to eat away at the real value of their debt over time. But with deflation the relative size of that debt grows, making it harder to pay back over time. As people’s relative debt grows, choking up even more of people’s incomes, the economy continues its death spiral.

If you think this sounds unlikely, it is exactly what happened in Greece during their recent crisis. We certainly don’t want it to happen here, and there is no reason why it should because we are in charge of our own currency.

What is the alternative?

With the Reserve Bank printing money, ideally the government would have a list of cost-effective investments they could make to stimulate the economy. Sadly, politicians tend to get involved and push their pet projects, which usually are far less cost-effective. We are seeing this sort of vote buying from all politicians right now, clearly showing the Reserve Bank can’t afford to give them a blank cheque.

An alternative to stimulate the economy would be a form of UBI/ helicopter payment/ debt jubilee. The Reserve Bank takes some of the money it is printing, and instead of giving it to the banks, gives it directly to the people. TOP’s view is that we should give a year’s worth of our proposed UBI; $13,000 for every adult and $2080 per child. To mitigate any inflationary impact, the Reserve Bank could mandate that it is used to pay down debt if people have it (because debt is the way money is created currently).

This would be a much fairer way to stimulate the economy and avoid a debt deflation spiral. It also trusts people to spend the money in the best way for them.

*Geoff Simmons is leader of The Opportunities Party.

55 Comments

Stimulating 'the economy' this late in the human trajectory, is an illegitimate target. It was 'the economy' which got us into this global shambles - and will end up killing us all off if allowed to continue. Hook, line and what happened to the fish Geoff?

And Act are only where and what they are, because of the impact of the human trajectory (not enough to go around, coming on mid-70's, leading to Thatcher/Reagan/Douglas et al).

But looking to the wellbeing of future generations? I can't think of a better goal.

It's speculating against unproductive assets that gets you in trouble, UBI is an interesting concept, lets see how it goes in other countries first, not need to be in a hurry.

Here's where that created money is going now, with inflationary effect widening the gulf between propertied and unpropertied. We need a property tax to divert that money from houses to a UBI that puts food on the table.

https://www.interest.co.nz/personal-finance/107301/reserve-bank-statist…

Here's where that created money is going now, with inflationary effect widening the gulf between propertied and unpropertied. We need a property tax to divert that money from houses to a UBI that puts food on the table.

https://www.interest.co.nz/personal-finance/107301/reserve-bank-statist…

Andrewj, I think UBI is ultimatly where we will end up world wide. Automation etc will take over but consumers have to have money. The monoply game has to go on. Some think a new form of trading like bitcoin will displace currency as we know it but in all reality it is all the same. All currency only survives if the participants believe in it.

ACT wanting in effect be abolishing new business growth along with our tech and film industry, not a good economic plan. And won't go down well with young voters.

I want to vote for people that are smarter than me, and TOP is the only party that offers that right now. Labour is waffle, National haven't had an idea for 40 years, ACT are cartoonish, the Greens have some good ideas but, like ACT, are full of the kind of people who believe everything they read on Facebook... Might be a wasted vote, but I don't mind given the alternatives.

I think the main problem with TOP is that they want to change the tax system too much at once (UBI / wealth tax / land tax). This creates fear; the middle class are scared of a land tax, the wealthy scared of a wealth tax, and the poor don't vote anyway. I get the feeling if they just went with this UBI policy (UBI paid for by flat tax and efficiencies), they would get more interest.

MMP would dictate TOP would get little of what they want anyway. The most likely outcome is Grant Robertson announces a policy of..... drum roll.... a UBI!

Don't you think there needs to be a significant change in the way our economy is structured? Some semblance of meritocracy would be nice.

"I want to vote for people that are smarter than me" - based on the rest of your comment you should vote for all of them.

TOP smart..... no just like all the others, all on an airy fairy dream.

C'mon mate, you like to bag people for their political choices ad nausem don't you, how about putting up yourself? Does it start with an N?

I bag all the parties because they are all useless.

Politians the biggest bunch of no hopers liers arround.

TOP is just another airy fairy BS dreamer that will get nothing done. Plus they still have the GM stigma well and truly attached.

Well the definition of insanity is doing the same thing over and over again (voting blue or red) and expecting a different result. What have you got to lose?

And vote TOP lol good one. That would be the worst call ever!

TOP are making the effort to address real, but otherwise ignored, issues in our environment, our society and our economy. Their policies may not be perfect but they are big-picture innovative and better thought through than the haphazard, off-the-cuff, ideology driven slogans that the rest seem to be coming up with. TOP's presence in our sluggish parliament may be enough to finally get some important issues on the table. They have my vote.

It is true that inflation on everyday item and used most have shot up and prices of things that are less consuned in changing environment like fuel has dropped - interesting how all this will unfold in comming future :

"But should we be in a hurry to get the government books back into surplus?" Nah - it's not like we have regular earthquakes here or anything. Let's keep the the kids credit card tab open at the bar and party on. If the kids start whinging just send a lemonade out to the carpark - they won't know they're paying for it.

"M7.0 - 7.9 Annual Average 0.26 - 1 per 4 years"

https://www.geonet.org.nz/about/earthquake/statistics

NZ has had a guts full of lack of implementation. How is the cat kill objective going TOP?

Thats been dropped with the former leader, Mr Morgan. Kiwis love their pussies.

Apart from the birds and the dolphins

The stench of Morgans irrational, will linger for a good deal of time yet.

Mortgan dropped you say... I would say there wasn't ever chance of getting anywhere with him arround but his core strategies are still there.

Lets say Gov issues $52b debt which is bought by the RBNZ to pay the UBI. for simplicity assume that the RBNZ is buying that debt directly from the government.

In Gov books: Assets:Cash at Westpac $52b (Dr) liabilities to the RBNZ $52b (Cr)

In the RBNZ book: Assets:NZ Government bonds: $52b (Dr) Liabilities: Crown settlement account: $52b (Cr)

Now gov pays every one in NZ their UBI by asking Westpac to credit their bank accounts:

In Gov Books: Expenses: UBI $52b (Dr) Assets: Cash at Westpac $52b (Cr)

In the RBNZ book: Liabilities: Crown settlement account: $52b (Cr) Liabilities: Banks settlement acc: $52b (cr)

NZ people: assets: cash at bank $52b (dr) Income: $52 (Cr)

Now at a waving of a pen, the RBNZ writes off the government debt:

In the Government book: liabilities to the RBNZ $52b (dr) Expenses: UBI $52b (cr) (i.e. there is no expense)

But how the RBNZ is going to record this? they can easily write of their asset (the bonds) by crediting it, but the money is now transferred to people via banks. The RBNZ cannot debit their liability (i.e. banks settlement account) to banks. This means that banks would need to produce $52b, which means they have to create $52b debt to all NZ people (i.e. lending $52b to people, who will need to pay it back to the bank).

So I am sorry to inform you that the debt does not disappears. That is why that the opposite of the QE is central banks selling their bonds back to people, not cancelling it out.

It sounded like the UBI was cost neutral; it was paid for by a flat 33% tax on all income and other efficiencies (less people would have claim to welfare etc). It can massively simplify the welfare system and tax system all in one go.

4m adult * $13k +1m children*2k = $54b

Total income tax from taxing everyone at 33%= $52b tax received currenlty $38b (so increasing total tax by $14b)

NZ gov currenlty pays about $15b in welfare. Even if we assume that UBI will completely replace this (which it wont, it wont even replace half of it), then the policy still requires $54-$14-$15= $25b increase in government debt (this is super optimistic figure). I would guess the actual debt will be more like $40b.

Thanks for the calculations. So Geoff is lying: " It can be funded via a 33% flat tax and the massive savings in bureaucracy it would generate"? Or maybe he meant an additional 33% tax!

Nobody's lying. There is an assumption that tax will be extended to cover property, a part of the economy that is undertaxed, with the inflationary consequences we see even now during the Covid-19 economic downturn.

Well, if they mean to tax all NZ assets at 3% deemed rate, then they will raise another $13b at maximum. NZ total net wealth was $1,367b, at a 3% deemed income rate, there will be an imaginary income of $41b which at 33% will produce $13b for them. They are still short by between $10b to $30b. It seems you have not done any work on what they say, and are happy to just accept their claim at face value. BTW, they must have done what I am doing. I should not be doing it, they should.

And it is simply ridiculous to tax asset that are being used to generate income at deemed rate. A rental house real income is the rent it gets. If you are going to tax a rental property at 3% of its estimated value, then you should surely not tax its rental income. If you are going to tax value of shares in a company based on their valuation (god knows how they are going to value companies, and almost 50% of NZ total net wealth is shares in companies), how can you justify taxing the company's income? if your argument is that a company's economic income is its realized income plus unrealized capital gains (as TOPS argues) then surely you cannot justify taxing it twice.

"NZ gov currenlty pays about $15b in welfare" - is this right?

https://www.treasury.govt.nz/information-and-services/financial-managem…

"The three largest areas of total Crown expenditure for the 2018/19 financial year were:

Social security and welfare: $34 billion

Health: $18.7 billion

Education: $15.3 billion"

Remember they would also implement a broad based property/asset tax regime which would also raise revenue.

Yes - their ideas look batty to start with. The more you look into them however, the more they start making sense. But it's a massive change that most people refuse to understand because they are so caught up with how things are now. We are in unprecedented times however reaching the end of the line of the existing system. There are multiple crises either in play or getting worst, climate, inequality, housing, health etc with huge issues around productivity and dead economic growth. This requires us to think and act boldly, with new solutions, not more of the same stuff that has got us into trouble. Continuation of the status quo is very quickly not becoming an option.

A fair chunk of NZ super wouldn't be needed with a UBI...

I did not include pension (which is about 60% of the welfare total) . If you add pension, the gap will further increase. I just assumed that the UBI will replace other forms of welfare.

Sounds like you didn't read their policy. I recommend reading their policy before commenting on their policy.

Also my comment is to show that TOP's claim that the RBNZ can simply write off the government debt (i.e. its deficit spending) is incorrect. They can never write it off. They can renew it to perpetuity, but can never write it off.

So TOP's plan is to implement MMT in it's mainstream form and assume it will work. Geoff you just lost my vote. To call QE money printing is grossly simplistic here, QEed bonds need to be paid back and it most defiantly matters if you leave the money you promised to pay back in circulation. Not that the public will likely understand but you need to show some more understanding on the practicalities of monetising debt.

What happens if you MMT plan does not work with your guessed amounts, do you double down again and again until we get hyperinflation. This plan is just as incomplete and wishful as every other parties.

In practice, QE bonds aren't going to be paid back, they will roll over into perpetuity. 11 years after the GFC before covid hit, what fraction of QE bonds had been repaid?

Mostly yes, but the debut still stays on the books (for debt/GDP and other things) and their QT has not completed because the recovery was never completed. QE does not make the next generations debt burdens disappear, that takes real printing and currency debasement.

If Geoff had of said what you said instead of instant free money because MMT, I would be less critical.

"QEed bonds need to be paid back"

Who to? Money is "borrowed" from the Tax payer. Then we ask for it to be "Paid back" by the taxpayer.

Can you lend me $50, don't worry... you can pay me back when you have another $50.

MMT is not new and nor is the belief you can get something for nothing. While this iteration is attractive in theory, it makes no sense in reality. If you suffer from alcoholism would anyone suggest a treatment of more alcohol? If you suffered Obesity would anyone think that could be cured with more food? We are now to believe somehow the Govt (a collective of us) can help us, by creating more money. Common sense would say austerity is the way. No one is denying there will be pain those with foresight might think we should experience it now and in doing so, to a lesser degree. Money: A means of exchange which has value relative to 2 things 1. Its scarcity and 2.The confidence we have in it. It would be incredibly naive to believe you could erode these 2 things and have not have capital flee. Capital will not sit idle while its value is being diminished.

I'm not sure they are good analogies. In this case we are suffering from not enough spending (economic downturn) and I think the best answer to that is for the government or RBNZ to encourage more spending, although I would prefer the government did it via helicopter money. The main thing is to pay it back during the better times; here in NZ we have a fairly good track record of doing that, in other countries not so much.

Wasted vote

May as well save engery and do something beneficial.

TOP voters do something beneficial for the society - by wasting their votes.

The only wasted vote is one that votes for the same thing expecting different results. Usually because people are part of the smaller and smaller cohort benefitting from the status quo or are too oblivious to see very real issues. Change will come eventually, whether it's violent or peaceful is likely up to the ability of the people to make smart choices. I also don't hold much hope of this.

Maybe going really hard in 20 more elections they could get to 5%.

Better chance than average that this will be the last election for TOP.

May reincarnate as the BOTTOM party.

$250 UBI with a 33% flat tax: So, deduct tax from $250 and you get about $167 in the hand. The author doesn't say otherwise! And does this amount replace existing benefits eg unemployment, sickness,etc? If so, the poor are on a hiding to nothing and the rich get even more money in the bank.

Go figure.

You need to go and read their policy before commenting...the UBI is tax free. The $13k/year equates to zero net tax on income up to $39k. It also is not abated so the poor don't get penalised if they wish to earn other sources of income. The current system results in a massive disincentive to work.

TOP's proposed UBI is nontaxable, so the $250 is $250 in the hand. Combining the flat dollar rate of $250 a week with a flat tax of 33% on all other income has the effect of creating a progressive income tax scale that begins $13,000 a year in credit.

https://www.top.org.nz/universal_basic_income

The author's wording doesn't unambiguously state that the UBI of $250 per week is gross or net of tax; neither does the mention of a 33% flat tax in the same paragraph necessarily imply that it doesn't apply to the UBI. The word 'flat' doesn't discount an interpretation that the tax applies to all income levels.

I can recall that over the last 72 years I have been obliged to ask someone to clarify whether their stated salary of say $1000.00 a week is net or gross of tax', and often the answer is gross.

But what do I know? I bow to your superior knowledge.

The author's wording doesn't unambiguously state that the UBI of $250 per week is gross or net of tax; neither does the mention of a 33% flat tax in the same paragraph necessarily imply that it doesn't apply to the UBI. The word 'flat' doesn't discount an interpretation that the tax applies to all income levels.

I can recall that over the last 72 years I have been obliged to ask someone to clarify whether their stated salary of say $1000.00 a week is net or gross of tax', and often the answer is gross.

But what do I know? I bow to your superior knowledge.

I don't want to dump the debt on the grandchildren (or dump any of our crap actually). And I think TOPs view on macroeconmics is wishful.

That ship has long sailed. The question now is should we use austerity to pull the ladder up after ourselves and leave the kids with massive debt and a down sized economy with no hope of generating wealth for them in the future, or should we be looking at more innovative options like TOP suggests?

These two statements seem highly contradictory:

"That essentially means that we owe this money to ourselves. The debt could disappear in an instant with the stroke of a pen (or touch of a computer key)."

"The worst-case scenario here – the one that the Reserve Bank is working to avoid at all costs – is deflation."

Politician speak with fork tongue?

Last time I've read, D/Seymour stating to give a brown students a chance (a bit R, but do correct if I'm wrong/misread this) - one thing for sure, third largest (still minority voters) of Asians ethnicity is still being discounted/ignored by Lab. govt. which is more focus on Maori & Pacifica students for their study seat placement & their govt. job applications.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.