Well, New Zealanders, apparently you can have your cake and eat it. You can save money in big dollops, while also borrowing massive amounts to put into houses.

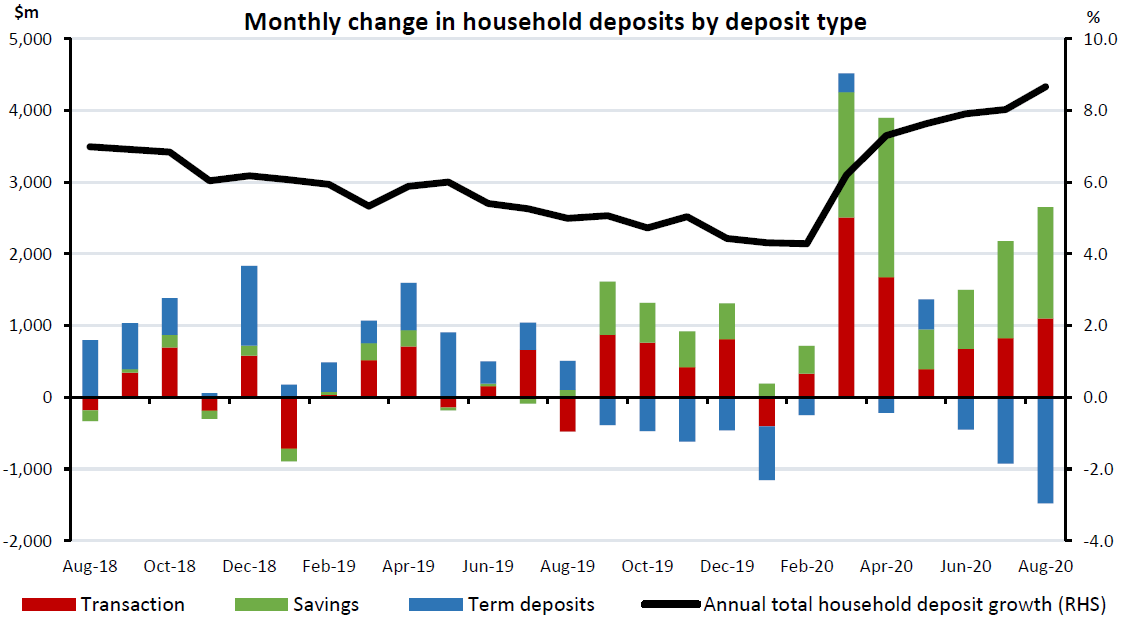

According to deposits data compiled by the RBNZ the amount held by Kiwi households in the bank increased by a further $1.174 billion in August, bringing the amount sitting in bank deposits to $197.5045 billion.

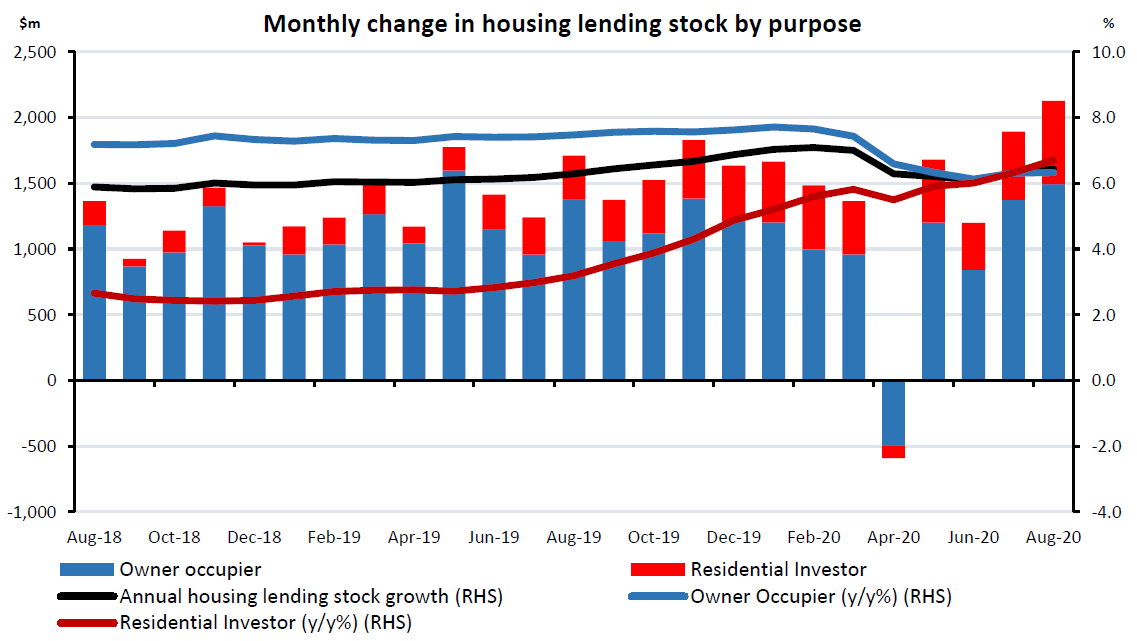

On the flip side of the coin though Kiwis increased the size of the outstanding mortgages pile by $2.142 billion to $287.729 billion, the highest monthly increase in lending since March 2007.

On the deposits, the latest monthly household figure gives an annual growth rate of deposits of 8.7%, which is the highest in four years.

That 8.7% is really neither here nor there, however, since the amount on deposits has increased $13 billion just since the Covid crisis mushroomed in February, which actually gives an annualised growth rate of about 14%.

Figures can deceive somewhat though.

Term deposits are dropping (falling $1.5 billion in August), while all the growth is coming in savings and transaction accounts - which suggests money being 'parked' in expectation it will be needed soon.

But it's also possibly a comment on the non-existent nature of interest on term deposits now.

Then, however, on the other side there's the increased size of the outstanding mortgages pile by $2.142 billion to $287.729 billion, which as said above is the highest monthly increase in lending since March 2007.

It gave an annual increase in the size of the housing debt of 6.5%, which is the highest rate since the 7.1% recorded in March just before the lockdown put a temporary freeze on the housing market.

The RBNZ said annual growth in residential investor lending also overtook growth in owner occupier lending, up to 6.7% versus 6.3% for owner occupier.

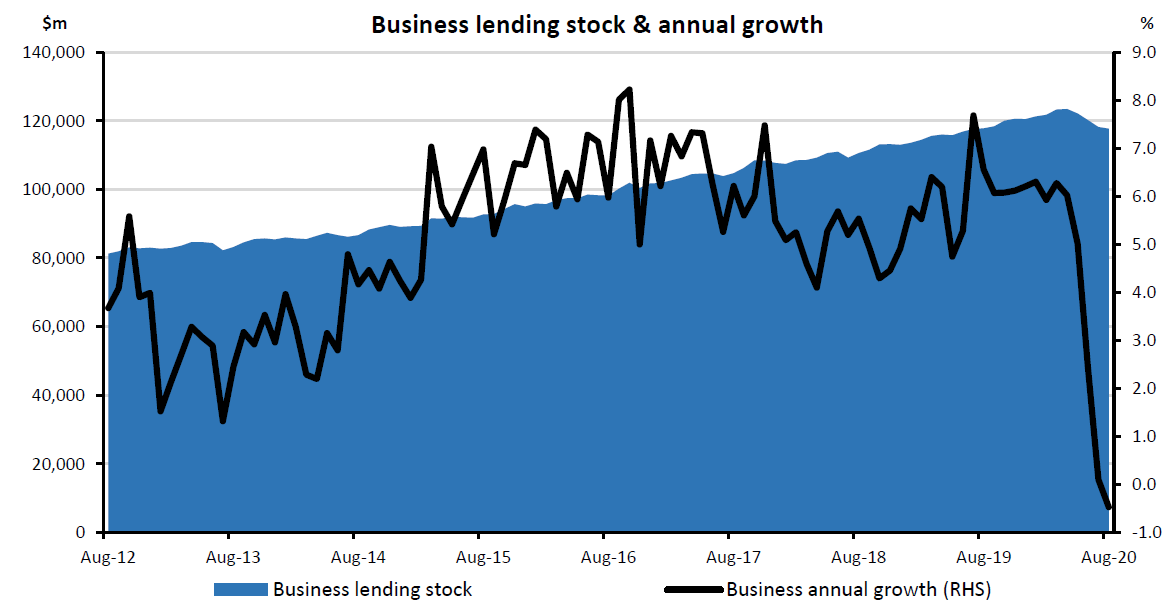

At the same time though, annual business lending growth turned negative for the first time in nine years, with business borrowing down $496 million in the month to $117.7 billion, with annual business lending growth dropping -0.5%.

The Reserve Bank gave the following key points for August 2020:

Total housing lending stock rose by $2.1 billion (0.8%) in August 2020 to $287.7 billion, the highest monthly increase in lending since March 2007. Annual growth in residential investor lending also overtook growth in owner occupier lending, up to 6.7% vs 6.3% for owner occupier.

Total consumer lending stock fell by $188 million (-1.3%) in August to $14.7 billion. This included a $120 million drop in credit card lending for banks. Annual growth in consumer lending fell to -11.5%.

Total business lending fell further in August 2020, down $496 million (-0.4%) to $117.7 billion. Annual business lending growth also fell into the negatives for the first time in nine years, down to -0.5%.

Total bank household deposits went up $1.2 billion (0.6%) to $197.5 billion, however this included a $1.5 billion drop in term deposits. Meanwhile transaction & savings accounts went up $1.1 billion and $1.6 billion respectively. Term deposits now make up less than half of total household deposits.

49 Comments

Would this suggest our bank sector is illiquid? Looks like a loan to deposit ratio of 145%. This is only mortgage debt too right?

That's not how the modern banking system works. That's the textbook definition. Which banks take deposits from customers, then lend out those deposits as loans. The modern banking system and money creation is very different.

Translation - Poor FHB's borrow massive amounts due to LVR restrictions being removed. They will be in major debt for many many years and will be in extreme peril when interest rates go up, however rich boomers with second homes sold them to these poor FHB's at inflated prices then put all that money in the bank.... the end.

Yip. Wealth transfer from the FHB generation to Boomers in exchange for massive debt (far in excess of what Boomers had to take on to get their houses). FHB generation also get passed the tax burden. Life is good.

Rubbish. They have been stress tested at 5%-6%, will pay it off in 30 years, and will enjoy average capital gain of 5%-7% annually over that period. Moronic doom merchants don't have a clue.

So based on your 5% capital gain a year they will double every 14.5 years. At 7% doubling every 10.3 years. Does this sound logical to you going forward? How would buyers every pay them off? Are you expecting some boost in job prospects in NZ that will create new industries that will pay big salaries?

What has the annual increase been over the past 30 years? About 5% if I recall correctly. No doubt plenty of people back in 1990 thought 5% annual growth for the subsequent 30 years would be "illogical".

How do buyers in London pay off an average 3 bedroom stand alone house at NZD $3M? The average Auckland house transplanted into London will cost you over 20x median UK income. In the future this type of house in Auckland will likely be over 20x NZ income and terraced units will be the norm instead.

In 30 years the "average" new house in Auckland will likely be a 90sqm townhouse, at a more reasonable income multiple than a stand alone house.

Do you base all your past returns as the predictor of future returns for everything? So all the Sh#t houses being sold now in Auckland for $1m getting a 4% yield and $800 a week will be $3m in 30 years and renting for 4% yield meaning $2300 a week?

You have chosen London as your comparison. But I would argue Auckland is a little sh#t box city on a small island in the South Pacific with little prospects other than bringing in migrants continuously to grow vs London is one of the financial centers of the world. What happened in London has zero relevance to Auckland. NZers kid themselves wealthy want to move here and we even have the press writing this that Americans want to move here due Trump etc but out of 400 million people a handful do. But we bring in low skilled people and students to keep the bottom end of the market increasing. For your dream for Auckland above to happen that is the only option. But the salary and wages wont be able to pay the rents. Perhaps the Government will having everyone on an accommodation supplement and pay it for them?

What if the comparison is say Arlington in Dallas Fort Worth. The fastest growing city in the US. I used to live there in the 1990s. It was fast growing then too and prices were low. Today https://www.zillow.com/homedetails/6414-Vintage-Lake-Dr-Arlington-TX-76… NZD650,000 buys you this. They do have areas 20 minutes away where multiple billionaires live too. More https://www.zillow.com/community/rockingham-estates/2084662490_zpid/ and thousands more, You can get new like this https://www.zillow.com/community/rockingham-estates/2084662489_zpid/ for NZD$450,000

Thoughts?

A 5% growth rate (as DD mentions) would mean that a 1 million dollar house in Auckland will be actually worth $4.3m in 30 years. Sounds very plausible!

I'm sure people on an average NZ wage would service a $4m mortgage with no trouble....

It will happen. In 1990 many people would've scoffed at the idea that the average Auckland property would be around $1M in 30 years.

Again, in 30 years time the average wage earner will be buying a terraced unit/townhouse in Auckland, not a stand alone 3/4 bedroom house.

I still think $4m would be a big stretch when wages are barely increasing.

So did the guy in 1990

If you're going to compare house prices of London to Akl then you need to compare salaries too. End of. In NZ prices have only gone up because the next person to buy your house after you borrowed more than you did. In the past if it ever looked like the queue of "bigger suckers" was drying up, the RBNZ would just drop the OCR which lowers banks funding costs which results in banks dropping their mortgage rates. This means said "bigger sucker" is able to borrow more and the queue fills up again. So this all works until there's no longer someone able to borrow more than you did and thus pay more than you did for your house. When will that be? Well when the RBNZ can no longer lower bank mortgage rates (via cheapening bank funding). Aka when the RBNZ go negative OCR next year then what? The FLP will help lower bank funding so the merry-go-round will continue a little longer but then they have no more ammo after that. The safety net of lowering rates to make borrowing cheaper that has supported NZ's house price appreciation of the last 30 years is about to be dissipate. Add on historic low immigration and no tourism due to the border closure along w/ double digit unemployment (employment...you know...the thing that mortgage holders and tenants rely on to pay their mortgage/rent) and you have a very "resilient" market.

I did compare income - "20x median UK income"

London is a powerhouse in the financial world. Canary Wharf is money making machine. Tower Hill has heads of some of the biggest insurance companies. The list goes on. Auckland we sell houses to one another for more and more and host boat races that nobody outside are tiny group of the worlds population know about it. When I was in San Francisco the America's cup happened to be on and most people did not even know it was on or what it was....A comparison to London is a joke. When I lived there in 2004 there were 7 million people by 2020 there are 9 million.

You've just described why London is currently much more expensive than Auckland. A 3 bed stand-alone house with a yard in London is 20x the greater London average annual income. Easily looking at NZD $3M.

Go back and re-read my comment. I'm obviously not comparing London of today with Auckland of today. London once had an average price and price to income ratio of Auckland today. Any yet somehow, miraculously, it changed over time into what it is today. There is no reason the same can't happen to Auckland. This is what the trend has been and will very likely continue to be.

The average salaried generally don't own property in London they just rent so it might not be a relevant ratio. They say its Average Salary in London, England: London £37k.

So what has happened in London may not be relevant to what may happen in Auckland.

But I take you point.

If we can get some good unemployment numbers no matter how low interest rates go even negative if you cant pay back the principal you eventually have to sell. As you can tell I am anti allowing investment in houses for tax free capital gains and using the financial system to protect it at all costs.

"The average salaried generally don't own property in London they just rent"

Most households, about 52%, in London own their own home. This compares to about 62% in Auckland. Not vastly different. But I'm not sure what the relevance of this is.

I lived and worked in London as a town planner, so the place isn't totally foreign to me.

My point is simply that people in 1990 would never believe the average price and price to income ratio of Auckland today. Just like most of this site's readership today can't fathom what these figures will be in 2050.

The point is that if the average in 2020 is GBP37k they dont have a sh#t show of ever buying a property now. The point then is the number of times the average salary to buy a property may become a nonsensical measure in the London market.

I lived in London too and worked at Canary Wharf in Finance. I have close family who bought a few properties there in the last 5 years.

But again you are choosing London as what might happen. Why not inner Mongolia? Why not Dallas Texas? Why not the Gold Coast? London suits the narrative that things are going to boom in Auckland for ever as London just keeps going. But I think other markets are just as valid or more of a valid comparison than London. As only real estate agents say London, New York and Auckland in the same breath....

Extrapolating past returns will always work. Guaranteed. A subsection of the economy can always and forever compound much faster than the whole. Guaranteed.

Said nobody ever. But learning from the past is prudent, ignoring it is moronic.

so DD does that mean we are back to picking the moment when it all changes and hoping we are one of the lucky ones that gets out before we lose 10-40% of the paper value of our house? Winners and losers, we all have fingers crossed that we are not the losers

"...to put it into terms Kiwis most definitely understand: You can save money in big dollops, while at the same time borrowing massive amounts to put into houses at the same time."

That's what increasing speculative national debt produces - sellers pocketing their profit and the next buyers having to borrow more to pay those departing sellers.

The question posed the other day, stands: "Who is selling?" and if those that are selling aren't re-buying, but stashing the loot ( deposits up; borrowings up), then what's happening is totally predictable - and will continue as long as we allow it to.

How does it end? It's called - Negative Equity.

The US housing market has some scary stats...https://wolfstreet.com/2020/09/25/fha-mortgage-delinquencies-hit-record…

Subprime, No Problem? FHA Mortgage Delinquencies Hit Record 17.4%, as Fed Triggers Mad Land-Rush in Split Housing Market

by Wolf Richter • Sep 25, 2020 • 136 Comments

Atlanta metro: 53,000 FHA mortgages are delinquent. Houston metro, 47,000. Just FHA, not including other delinquent mortgages. And when forbearance ends? By metro.

10 Most at Risk Metros, FHA Delinquency Rates, August 2020

MSA # Delinquent % Delinquent % Seriously Delinquent FHA Share

1 Atlanta-Sandy Springs-Alpharetta, GA 53,135 21.2% 14.2% 21%

2 Houston-The Woodlands-Sugar Land, TX 47,410 22.2% 14.3% 19%

3 Chicago-Naperville-Evanston, IL 39,740 22.4% 15.5% 14%

4 Washington-Arlington-Alexandria, DC-VA-MD-WV 29,855 22.1% 15.5% 14%

5 Dallas-Plano-Irving, TX 27,712 19.2% 12.2% 15%

6 Riverside-San Bernardino-Ontario, CA 22,894 17.3% 11.1% 21%

7 Baltimore-Columbia-Towson, MD 21,425 19.9% 13.2% 19%

8 San Antonio-New Braunfels, TX 17,156 19.0% 11.4% 19%

9 Orlando-Kissimmee-Sanford, FL 16,811 20.2% 13.9% 22%

10 Tampa-St. Petersburg-Clearwater, FL 16,355 17.4% 11.8% 20%

Lest we forget, the government raised $34.595 billion new deposits since the end of March. August alone accounted for $3.64 billion. Admittedly, as of August $23.761 billion had yet to be dispensed into individual accounts since it remained parked at the RBNZ in the Crown settlement account.

Offset mortgages must skew these figures slightly. Having $200,000 in your bank deposit offset against a quickly deteriorating mortgage! Money in amount accumulates quicker than money out!

Which everyone should be doing! Borrow as much as you can at 4.5% (or whatever), Floating, and pay no interest on whatever you borrow whilst it's Offset. It's ready-drawn liquidity for whatever and whenever it will be needed. No one should be 'repaying the mortgage' at these low-interest rates - no one. They should be retaining the debt, offset against credit funds.

The downside? That risk is not Compensated ie: You owe the bank ( the mortgage debt) and the bank owes you (your deposit) and if it all turns to custard you won't' be fast enough to repay the debt before 'your' deposit money is quarantined.

(PS: Why we allow Offsetting is beyond me!

The fastest way to curtail my above suggestion is to levy notional Income Tax on any Offset Account. If you're Offsetting a Floating Rate Mortgage at, say,4.5%, then notionally calculate the interest receivable at that rate for tax purposes. Income Tax was always due on Interest Receivable (and still is if it's not Offset) until The Rules were manipulated by the banking fraternity to encourage more borrowing)

Doesn’t a revolving mortgage achieve the same thing, but safer in the event of a bank lockdown as your debt has been repaid. But you are still able to redraw on the loan account in normal times.

A bit like having a $500k credit card. But what's stopping the bank from freezing revolving mortgage facilities?

Well, nothing I guess, but at least you have less liable debt than the offset equivalent.

Seems a bit risky to be borrowing big given the level of economic uncertainty.

Good thing we have policies like the LVR so that people won't get FOMO or overextend themselves. Wouldn't want people to end up in negative equity should a downturn happen.

*Sigh*

"Kiwis increased the size of the outstanding mortgages pile by $2.142 billion"

"business borrowing down $496 million"

There you go Mr Orr, the two numbers you should be staring at for the rest of the day. Think hard, then think harder. About your actions and their consequences. Then please resign.

Maybe more businesses are borrowing by mortgaging against the house?

Under RBNZ rules, if the purpose is business related, the lending must be coded as business

https://www.rbnz.govt.nz/statistics/s33-banks-assets-loans-fully-secure… they only went up by 10m

Initially, I thought the same.. until I realised he could be genius with intention... the only way to drag things down which is very stubborn, is actually to prop it up in more extremities. The only way to let gravity works on gliding plane with engine cut off/no more gas, is to pitch it up to the stall point, the rest is gravity & spiral fast rotational down movement. History will be the judge of it.

Yes increasing leverage with deteriorating fundamentals. The fragility of the financial system has greatly increased while prudential controls have counterintuitively been removed. From my own point of view, I removed 30k of p2p lending in Feb because I was worried about a wall of defaults. Little did I know the government would backstop everything and everyone. Now that money is stranded at negative real rates. It will either be sent either offshore or onto domestic stocks. Term deposits are useless at this stage because they remove optionality, all thats on offer is return-free-risk. The risk with cash is to the downside from bail in or more probably currency depreciation, and almost certainly medium term inflation.

Savers are not being treated very well, which appears to show with the number opting out of TD's. What would happen if savers / depositors decided to target one bank, and withdraw all of their money away from one targeted bank out of protest over the continued lowering of the interest rates? Or maybe even all banks. I recall that this was often talked about with petrol companies when they kept raising prices uniformly across all petrol companies. All lowering interest rates is doing is keeping the housing bubble growing, which is what it seems they want to happen. Maybe some of this money that has been moved from TD's into savings accounts, is to be moved into other asset classes, such as housing, or gold, or shares, when the time is right.

100% agree Savers are not being treated very well. I have been told that you are not rated as a High Value Customer unless you have debt at banks. I am not talking about private banking options etc but internal rating. I have done exactly this and not bothered with TD's since late March. Its cost me a lot in lost interest but I am happy to get none with the ability to move money fast especially as when we went into lock down. A tip is increase your direct credit limit to the max on offer which for me is 250k a transaction if you want to be able to move money fast with no daily limit.

The proposed 50k guarantee would largely be useless to me but the arrogance of Orr and Robertson to say effectively they are helping the 90% who are debt fueled while screwing anyone who has been conservative and saved is a disgrace. The one thing I have learned from all this is just how far RBNZ and Govt will go to protect house prices. I would have been happy with an insurance guaranteed account with zero interest for a portion of my money but now we have zero interest anyway and banks being pushed hard to keep the housing marketing going up. In a normal times if bank insiders under provided for dud loans they would have been crucified and in jail but I cant believe the RBNZ are the ones suggesting this.

I suspect there are many like this, based on how many people have moved from longer TDs to their money being in shorter term TDs or oncall. But if a bank failed, will the government let people lose some of their money, when they could just print money again to prevent it? It would damage the reputation of NZ banks forever. We only need to look at what happened with the reputation of the NZ sharemaket after the 87 crash, which didn't seem to affect other countries as badly as it did NZ.

Likely to get an OBR event but there again if you are first out no problem.

From liquidity studies, most likely it will start with any banks that have large exposure to the non-productive RE/lands - But you are spot on there about the timing to get out. This is the time to plan your quick account maneuver pathway, activate it gradually my advise. Better than sorry later, off course you can dig/spy the recent stress test by RBNZ with regards to the banks - but past experiences told me something that difficult for them to control: 'Public crisis of Confidence', this one will always hit like a Tsunami. We can only hope, it's a small one but you never know.

Those OZ banks, anecdotally already started to feel the fund movement to the bank which care more about productivity I would say. I let you decide which bank it is, that openly not opening their loan book towards personal car loan or wait & see the magic growth tree of NZ RE wealth. Remember no one should care about ROI these days, think about return of your whole investment capital is more of the focus, diversify for safety (banks/Not TD, bonds, shares, gold, FX etc) - reduce/eliminate your debt level. Plan your flight path/economic storage to any countries which are willingly understand on how to be brave on economic pill medication for recovery.. austerity etc - NZ will still opt for prolong denials.

Fairly evident that it’s not FHB with large deposits

So two entirely different set of people

So not cake and eat it

The FHB save the dough (pun intended) for a deposit, which although 10% is the same as a house used to cost, take on massive lifetime of debt and the boomers who sell their overpriced cooler boxes eat the cake, that sweet tax free cake.

What choice do FHB have as both Labour and National will go all out to support the ponzi - May be vote Green

In recession uncertain time, when people are not confident about future, saving goes up. Nothing unusual about it.

Low interest rate supported by government stimulus creating FOMO and many are been forced to borrow to extreme to enter property resulting in more and more money going in House (In fact most money going to stock and housing - in NZ it is maximum in housing bubble), so again no surprises.

As of today most houses are going as soon as listed and that too 20% to 40% more than pre lockdown level so anyone and everyone with cheap and easy money is into housing. Many business people have dumped their business or taken back stage and all concentrating in building / construction.

Houses are not going the same day as they are listed it's just the MSM continuing to pump the market. Average days to sell is still up at 39 days and how hot the market is totally depends on the region. The government is simply doing everything in its power to stop the property market from crashing and when I came to this realisation I bought a house.

"Many business people have dumped their business or taken back stage and all concentrating in building / construction."

Are you on drugs?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.