This Top 5 COVID-19 alert levels 1 & 2 special comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Fewer businesses were liquidated in the first 8 months of 2020, than in any year since 1999. pic.twitter.com/kRA4p85OWO

— Andy Fyers (@andyfyers) September 29, 2020

1) Universal basic income experiment provides a big boost to wellbeing.

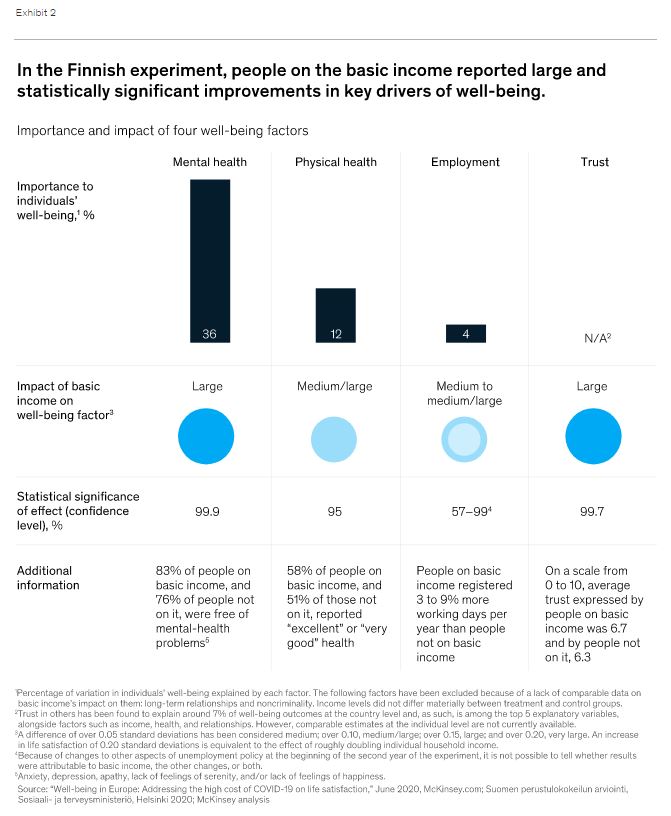

Against the backdrop of the economic fallout from the COVID-19 pandemic, McKinsey & Company's Tera Allas, Jukka Maksimainen, James Manyika, and Navjot Singh have taken a look at Finland's universal basic income (UBI) experiment. They conclude that while it may have only led to a small increase in employment, it significantly boosted multiple measures of recipients’ well-being.

The two-year study involved a treatment group of 2,000 randomly picked, initially unemployed people. They received a guaranteed, unconditional, and automatic cash payment of €560 monthly instead of a basic unemployment allowance of a similar amount. Even with a housing allowance thrown in, which basic-income recipients were eligible for, this level of support was significantly below the incomes of most Finnish households. All other unemployed people, who continued to receive standard benefits, formed the control group.

The McKinsey authors note that people on the basic income were more likely to get employment than those in the control group, and the differences were statistically significant, albeit small.

However you read the findings on employment, other effects were clear: people on the basic income reported significantly better well-being on multiple dimensions. Average life satisfaction among the treatment group was 7.3 out of 10, compared with 6.8 in the control group—a very large increase. To experience a similar lift in life satisfaction, we estimate that a person’s income would need to go up by as much as €800 to €2,500 per month—60 to 170 percent of the average per-capita household income in the European Union. Indeed, the difference was big enough to erase the gap in life satisfaction between unemployed and employed people.

These significant positive findings on well-being are no mystery: the basic income seems to have improved all the major components of life satisfaction (Exhibit 2). People receiving the basic income reported better health and lower levels of stress, depression, sadness, and loneliness—all major determinants of happiness—than people in the control group. Recipients of the basic income also demonstrated more confidence in their cognitive skills, assessing their ability to remember, learn, and concentrate at higher levels than the control group did. And the basic income enabled people to perceive their financial situation as more secure and manageable, even though their incomes were no higher than those of people in the control group. Finally, basic-income recipients expressed higher levels of trust in their own future, their fellow citizens, and public institutions.

A key lesson from the Finnish experiment, McKinsey adds, is the complexity of implementing a UBI.

Policy makers need to decide how it should interact with a large number of other policies, such as child benefits, housing benefits, pensions, health insurance, and taxation; for example, in the Finnish experiment, basic-income recipients were eligible for housing allowances but not for basic social-assistance payments. Unless such linkages are streamlined, they could detract from a basic-income system’s potentially considerable savings in administrative costs.

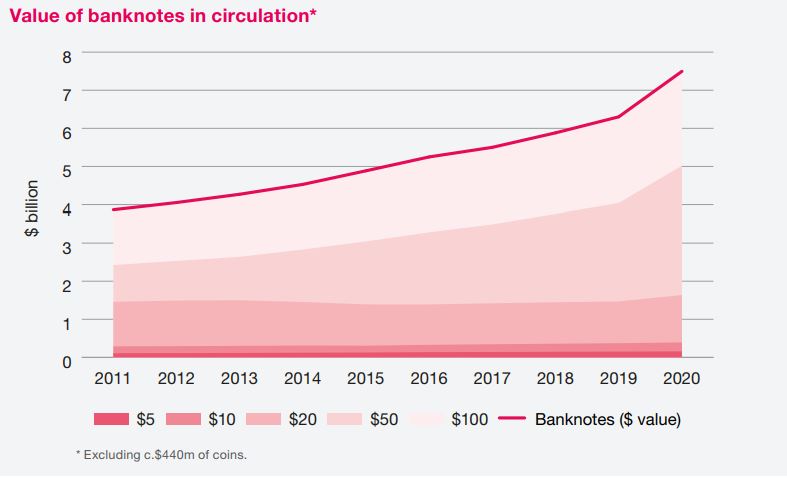

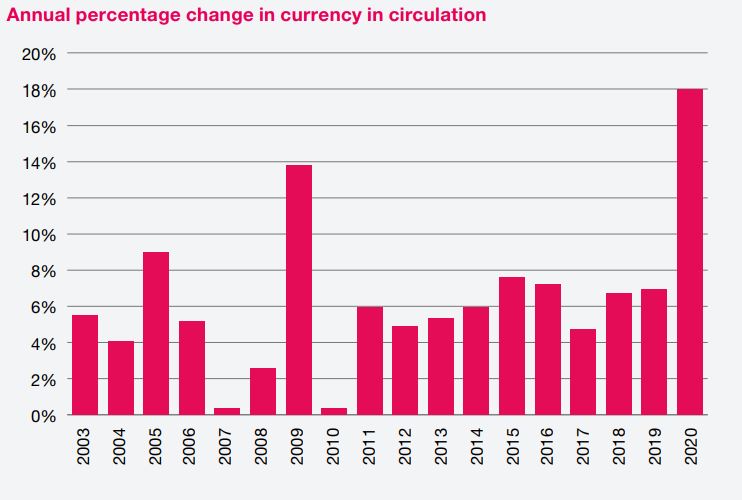

2) Reserve Bank ramps up cash in circulation.

The Reserve Bank issued its annual report on Thursday. It includes more detail on how, like toilet paper, cash was in demand during the early days of COVID-19.

At 30 June 2020 currency in circulation was $7.9 billion – $7.5 billion in notes, $0.4 billion in coins, an increase of 18 percent on the previous year. Most of this demand occurred during the lead-up to the COVID-19 lockdown when banks and the public required cash, mainly for precautionary purposes

I hope people hoarding both toilet paper and cash didn't get them mixed up...

During the COVID-19 readiness and response stages, we ensured that sufficient cash was distributed within the system and arrangements were in place to meet the needs of the public. Cash in circulation increased by $1.2 billion (+18 percent) in the year ended 30 June 2020, with almost $0.8 billion of this issued in March, associated with the COVID-19 Alert Level 4 lockdown. Banks began returning excess cash in May and June, a trend that is expected to continue into the first quarter of 2020-21.

3) What will Aussie mortgage deferrers do when their time's up, and how many are delinquent borrowers?

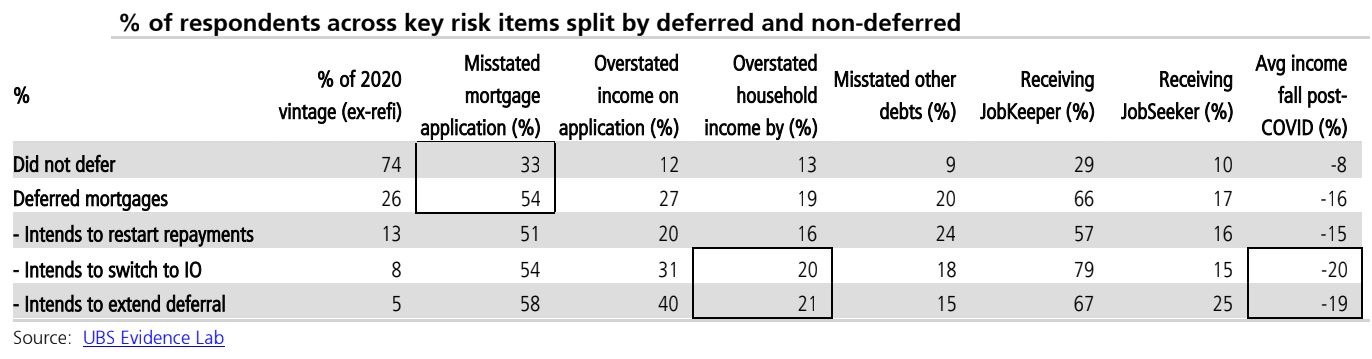

UBS' Aussie banking analysts have issued the sixth annual version of their Australian mortgage survey. And appropriately for this COVID-19 dominated year, they've focused on mortgage deferrals. The firm surveyed 904 Aussies who had taken out a mortgage over the past 12 months.

Many of the borrowers surveyed anonymously admitted they hadn't been completely honest in their loan applications.

We found the credit quality of the home buyers ('front book') in the survey is weaker than data shown by both the banks and APRA ('back-book'). This is in-line with expectations as home buyers (survey excludes refi) are more likely to be younger and more highly leveraged than the book as a whole. Once again, we found 37% of the sample stated their mortgage application was not "completely factual and accurate", a level consistent with the previous five vintages. Of more concern, the credit quality of customers who misstated their mortgage were significantly weaker than truthful customers. We found that factually inaccurate mortgagors: (1) have seen household income fall an average of 13%; (2) 36% have deferred repayments; (3) 66% have a household member on JobKeeper/JobSeeker; (4) 71% withdrew Superannuation.

Meanwhile just under half of those with COVID-19 related mortgage deferrals plan to revert to normal payments when their deferral period ends.

As the bulk of mortgagors approach the end of their six month deferral period, we found: 47% of deferred mortgagors intend to revert to normal payments; 32% intend to switch to Interest Only (IO); 21% intend to ask to extend deferral. However, the credit quality of customers intending to ask their bank to extend their deferral is concerning. Of these customers we found: (1) 40% overstated their income in their mortgage application (by 21% on average); (2) 15% understated other debts; (3) 67% are on JobKeeper; (4) 25% are on JobSeeker; (5) They have seen their income fall 19% since COVID on average (in addition to the amount they overstated). Unfortunately, we found the financial position of those asking to move to IO is only marginally better.

The 2020 survey illustrates factually inaccurate mortgages are materially higher credit risk. APRA has stated mortgage deferrals should only be extended on a case-by-case basis. We believe the banks need to undertake significant due diligence before extending deferrals or moving deferred customers to IO, as a large number of these borrowers are likely to be under more stress than the banks perceive. Many of these customers should be considered delinquent, in our view. Given this stress, a recovery in employment and house prices is critical to the banks' performance.

UBS says data from the major Aussie banks, who are the parents of the big four Kiwi banks, shows about 7% of mortgage customers, or 10% of mortgage balances, have deferred their mortgage payments due to the COVID-19 pandemic. However the UBS survey shows 26% of respondents have deferred their mortgages.

We believe this is likely to reflect the fact the survey contains only new home loan customers (front-book, ex refi) whom are likely to have larger mortgages and higher loan-to-valuation and debt-to-income ratios.

New Zealand's loan repayment deferrals were introduced for six months in March at the onset of the COVID-19 crisis. In August the Reserve Bank agreed banks can extend these deferrals for up to another six months, to March 2021.

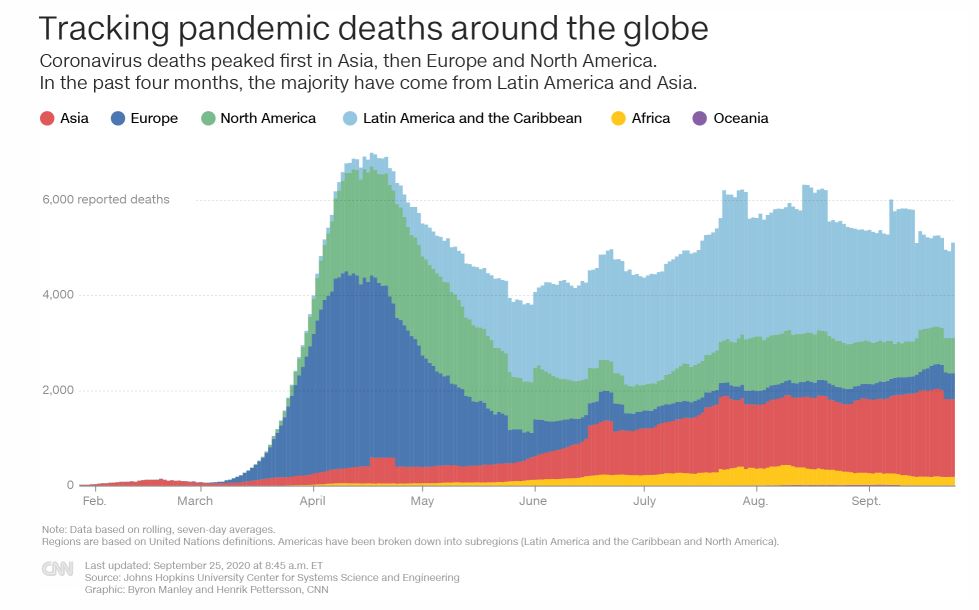

4) Has the Brazilian city of Manaus reached herd immunity?

In the MIT Technology Review Antonio Regalado has a fascinating story about COVID-19 in the Brazilian city of Manaus. The Amazon city was ravaged earlier in the year, and the suggestion is a form of herd immunity may have been reached now.

During May, as the virus spread rapidly in Manaus, the equatorial capital of the state of Amazonas, dire reports described overwhelmed hospitals and freshly dug graves. Demand for coffins ran at four to five times figures for the previous year. But since hitting a peak four months ago, new coronavirus cases and deaths in the city of 1.8 million have undergone a rapid and unexplained decline.

Now a group of researchers from Brazil and the United Kingdom say they know why—so many people got infected that the virus is running out of hosts.

In a report posted to the preprint server medRxiv, a group led by Ester Sabino, of the Institute of Tropical Medicine at the University of São Paulo, says it tested banked blood for antibodies to the virus and estimates that between 44 and 66% of the population of Manaus has been infected since the city detected its first case in March.

“From what we learned this is probably the highest prevalence in the world,” Sabino said in a phone interview. “Deaths have dropped very rapidly, and what we’re saying is that it’s related.”

Manaus may now be able to provide information on how long immunity to COVID-19 lasts.

Going forward, the Amazonian capital could now help public health officials better understand how long immunity to covid-19 lasts and how often the virus reinfects people. The blood survey clearly showed that with time, people’s antibodies become harder to detect. That could mean individual immunity to the virus is not permanent. “Manaus may act as a sentinel to determine the longevity of population immunity and frequency of reinfections,” the authors wrote in their preprint.

Chart: CNN.

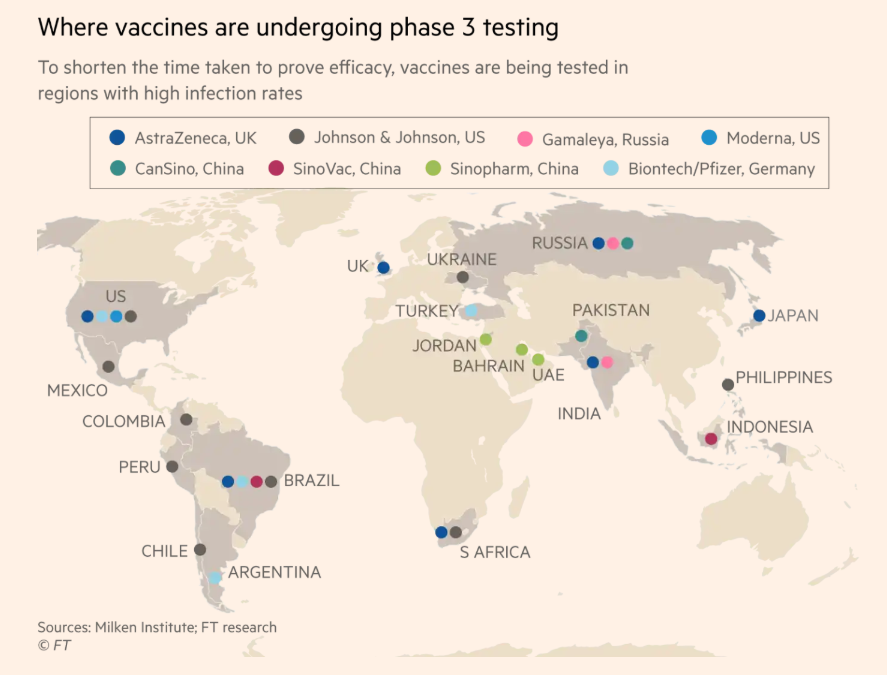

In its non-paywalled COVID-19 coverage the Financial Times takes a look at progress in the race to develop a vaccine. The FT notes a pragmatic approach is being taken by most of the developers, and any vaccine will likely only provide temporary immunity.

While it is commonly hoped that a vaccine will completely prevent individuals from getting infected, this result is rare, and has never been achieved for other coronaviruses or strains of influenza. Instead, a more pragmatic goal, adopted by most of the vaccine developers, is the prevention of symptomatic Covid-19 infections. That is the stated objective of the AstraZeneca, Moderna, Pfizer/BioNTech and J&J vaccines.

“What we really want from a vaccine is to stop people being admitted to hospital, going to intensive care and dying,” said Andrew Pollard, who is leading the AstraZeneca trials at Oxford university. “It is likely to be a much bigger hurdle to completely prevent asymptomatic infection.”

Immunity, boosters and side-effects

Given the growing chorus of experts warning it is likely the vaccine will confer only temporary immunity, the capacity to “boost” the immune response at a later date with another shot is important.

“The assumption at the moment is that we’ll be shooting to get to a year’s immunity,” said Kate Bingham, chair of the UK government’s Vaccine Taskforce. Seven of the vaccine candidates in phase 3 are designed to be taken in two doses, to increase the chance they will trigger an effective immune response. Only J&J and CanSino are trialing single dose shots.

“Even if you have a vaccine with a second dose, you may need to boost every year,” Ms Bingham said.

Map: The FT.

Cartoon: Matt Wuerker, Politico.

37 Comments

Interesting to see that the US, UK, and EU does not trail any vaccine from China.

Spurred on by America, the UK continues to alienate China with a ban on some students now reportedly planned. Post-Brexit, it should be trying to build bridges with Beijing, not burn them. Link

China never signed up to the COVAX sharing agreement. They clearly chose to go it alone but with a fair amount of hacking along the way.

So does OZ, NZ & Canada, if you're live longer in NZ (at least the past 25-30yrs) - you should realize by now that third largest Asian voters by ethnicity group in NZ is only here to be harnessed on their hard work & pay the taxes. But they are subject to more discrimination or indirect discrimination. Check NZ nationwide students healthcare seats allocation or initial job placement buddy - It's 'the majority' pushing narrative to uplift the 'number two & fourth' ethnicity numbers - and, yea just skip that the third one by the way - Welcome to NZ, now let's move & build OZ.

The effect of a UBI in terms of statistically significant better mental health outcomes is very compelling. Just look at the increase in spending we are committing to improved mental health outcomes. Makes you think.

Love the last line:

US consumption will crater unless somehow the millions of unemployed workers who still desperately rely on government stimulus find a job (spoiler alert: they won't).

what exactly?

that more free lunches & handouts can trump physics?

The life you ordered is basically out of stock ... hence the Mental health issues

A UBI is nothing but a poor bandaid

The world economy now has massively reduced OUTPUT & this creates stress all through the system. Fiat Debt is collapsing

We have lost the momentum of turning one form of energy into another and paying ourselves a wage in the process

We have lost the momentum of turning one form of energy into another and paying ourselves a wage in the process

and all the while the asset holder haves have more. David Harvey explains it as accumulation by dispossession.

I think we agree in that the future of work (i.e., wages) doesn't look anything like the present notion/aspiration/ideal of work.

"the asset holder haves have more.."

More paper claims ... yes, while fiat holds. As you know, you cant eat a house

A UBI is essentially being floated to let em eat cake and buy time

Are you saying the UBI is being floated by the haves to buy time to accumulate more? Perhaps. Regardless, if one of the overall benefits is better mental health/less stress across the population - then people will be better able to cope with what are likely large social/economic adjustments coming. Maintaining social cohesion in times of crisis/shock/change is really important.

More puts the spotlight on education, schools..

You will need between $20b to $30b more in taxation in NZ to finance the UBI plans of TOPs (which in terms of the amount is relatively modest), even if we adopt the TOPs taxation policy (33% flat rate, plus (effectively) 1% wealth tax on all assets privately held). How do you propose to finance that? I think that is the main and primary barrier to UBI. Otherwise, who will say no to free money and who will deny all the positives associated with more free money for everyone?

For UBI to add up, you will need to either tax everyone who actually works at 66% (from 0) or tax all the assets at 3% (i.e. deemed return of 9% at 33%) (with no exception).

You don't have to tax anyone, anything!

With MMT, or it's similars, 'money' is just created as figures on a spreadsheet - call it Government Debt if you need a name for it - and hand it out to individuals as UBI to consume and speculate with. Everyone gets wealthier.

It doesn't matter if the Government Debt figure is $1 billion; a Trillion of $100 trillion does it?! They're all just another figure. All that matters is that individuals don't have to work and they don't' have to pay tax and they get the means given to them to consume and keep The System going.

Read this you’re not even close...

Fully costed policy document

https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/2692/attachmen…

Where's your source?

Most of NZ is now on a benefit of some sort and we spend huge money on not just the benefits but delivery of these.

I would be very surprised to if the UBI as proposed by TOP would cost more. And then factor in the motivation to actually get up and go to work because you can now keep any extra would solve many other issues we have.

The current benefit system is massive drag on NZ, both financial and its dependency creation. An elephant in the room that has got NO coverage in this election cycle...when it's one of our biggest issues.

He has no source, he mostly made it up and it's all mostly wrong.

Maybe he's discussed the numbers with Paul Goldsmith?

The real problem isn't the volume of money required, it's what do we do with the ex MSD and other now redundant workers.

I cant believe that they had to do a study to prove that paying people lots of money to not work made them happier than making them work for that money! Next up, a study looking at "does getting a good nights sleep make you feel more rested?".

With AI, automation, massive unemployment and the gig economy on our doorstep we need to act now

https://www.top.org.nz/universal_basic_income

While I'm often skeptical the more I read about UBI the more compelling it appears to be. It may not be a question of if but when this is adopted.

You think they will finance it from printing money? there is not other way for it to financially add up.

Any advanced knowledge of the efficacy of any of the Covid19 vaccines currently in trials but already in mass production could be extremely powerful for investors. Not only investors in the pharma companies themselves but the wider market. Hopefully, the senate committee members can resist the urge to trade this time and just be content with the flow of bribes from the lobbyists.

They are proposing a UBI that will cost about $52b. They propose to raise everyone's tax to a flat 33% which will increase government income from personal income tax to $52 from the current $38b (so increasing total tax by $14b).Well, that figure is incorrect because TOPs says that their UBI will either replace or reduce other social welfare payments that are actually subject to tax, while UBI is not. So if UBI reduces total social welfare by $20b, then the corresponding tax will reduce by 20b* 33%= $7b. So they will actually have $7b ($14-$7) more in taxation from this source.

They also propose to tax all NZ assets at 3% deemed rate. NZ total net wealth was $1,367b (Source: NZ Stats), at a 3% deemed income rate, there will be an imaginary income of $41b which at 33% will produce $13b for them as an absolute maximum. I will say why they are very unlikely to raise even a remotely close to this figure in my next comment. but for the sake of argument, lets say they will raise a total additional income (a very generous and optimistic estimate) of $20b ($7b from income tax, $13b from wealth tax) to cover the $52b UBI.

They say that UBI will replace some of the existing welfare, but do not give details of what is replaced with what. For example, will UBI replace super? will it reduce super? will it replace other social benefits? So without them giving details, it is not possible to know the reduction in actual expenditure if UBI is introduced. But lets be generous and say that UBI will reduce the social welfare from the current $34b by 60% to $14b ( a big assumption off course). That mean they are short by $12b under a very optimistic scenario.

I think that TOP leaders do not believe in their proposals, as they do not even bother to cost them in details to show how they will work.

Maybe you should read the document you’re not even close...

Fully costed policy document

https://d3n8a8pro7vhmx.cloudfront.net/garethmorgan/pages/2692/attachmen…

So if UBI reduces total social welfare by $20b, then the corresponding tax will reduce by 20b* 33%= $7b. So they will actually have $7b ($14-$7) more in taxation from this source.

Er, no, the tax receipts would be reduced by whatever tax is currently paid on current social welfare. Since we don't have a 33% flat tax at present, most of the tax paid by benefits is going to fall into the 10.5% bracket.

They also propose to tax all NZ assets at 3% deemed rate.

No they don't. They deem all property to have a return of 3%, which is then taxed at 33% = effectively a 1% asset tax. If your property is already returning more than 3%, then you're likely to already be paying more than 1% tax on your equity, and so there would be no change in tax for you.

which at 33% will produce $13b for them as an absolute maximum.

Their calculations show they expect to raise $8B from the property tax.

They say that UBI will replace some of the existing welfare, but do not give details of what is replaced with what.

Yes they do.

You should be very embarrassed for this comment Believer. The information is all available out there, instead it appears you just made this stuff up on the top of your head because you couldn't be bothered to do any research.

Obviously a Believer in something else other than evidence. Come on Believer, this is some fairly simple stuff you have got completely backwards here. At least read the policy before trying to tell us how it won't work. And if you don't understand it, ask questions rather than making definitive statements which don't gel with reality.

Please read the policy and the tabulations that accompany it... your rants are not accurate.

Having just read (and am re-reading and considering adding to home library) Joel Kotkin's 'The Coming of Neofeudalism - a warning to the global middle class', I'm more inclined to think that a UBI, controlled as it would be by what he terms the 'Clerisy' - them as wot determine broad policy. cultural norms, the Overton Window etc - is just another Sop to the New Serfs. The old song line (from Government Cheese, Rainmakers) applies:

"They'll turn us all into beggars 'cause they're easier to please" - full lyrics here.

The new class structure resembles that of Medieval times. At the apex of the new order are two classes―a reborn clerical elite, the clerisy, which dominates the upper part of the professional ranks, universities, media and culture, and a new aristocracy led by tech oligarchs with unprecedented wealth and growing control of information. These two classes correspond to the old French First and Second Estates. Below these two classes lies what was once called the Third Estate. This includes the yeomanry, which is made up largely of small businesspeople, minor property owners, skilled workers and private-sector oriented professionals. Ascendant for much of modern history, this class is in decline while those below them, the new Serfs, grow in numbers―a vast, expanding property-less population. The trends are mounting, but we can still reverse them―if people understand what is actually occurring and have the capability to oppose them.

Thanks for this Waymad. Kotkin's book looks worthy of some time.

The resource stocks dwindle, the numbers demanding them grow.

The displaced are going to be from the bottom, up. When it's into what WAS the middle class, it's game over. The Elite can't buy enough to keep growth going, and without growth you don't have finance as we knew it.

Ham n Eggs upthread has it completely right. And anyone stupid enough at this stage, to think financial twiasts of any kind can chage physical outcomes, is barking; up the wrong tree, mad, take your pick.

Point about the study is that the financial twist of a UBI can change mental health outcomes, not physical/resource-related outcomes. And we are going to pass on this world to future generations (unless struck by a comet, or obliterated via caldera eruption, or all-out nuclear war, etc.) whether we like to think about it or not. Life doesn't end as de-growth and power-down :-) begins - as is evidenced right now given we're all here and its all happening!

"They conclude that while it may have only led to a small increase in employment, it significantly boosted multiple measures of recipients’ well-being."

From what I've read I would say negligible increase in unemployment. Plenty off well being though. The intention of UBI was to get the unemployed to start working. Apparently not hence UBI was disbanded by the Finns. Experiment was for three years I think.

You can't start and/or keep working in paid work if there is not an abundance of such paid work. The future of work will be much different going forward - more seasonal, more casual, less ongoing, less secure.

I love that political cartoon of Trump's scams, though apparently Nature may have the last laugh perhaps he should have shown her more respect. NYT article: Trump Tests Positive for the Coronavirus. "The president’s result came after he spent months playing down the severity of the outbreak that has killed more than 207,000 in the United States and hours after insisting that “the end of the pandemic is in sight.”

https://www.nytimes.com/2020/10/02/us/politics/trump-covid.html

If we end up with rampant inflation there won't be much difference between cash and toilet paper.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.