As of July 31 borrowers holding $73.7 billion worth of bank loans were receiving COVID-19 related repayment relief.

The loan repayment deferrals were introduced for six months in March at the onset of the COVID-19 crisis. The Reserve Bank agreed last month that banks can extend these deferrals for up to another six months, to March 2021.

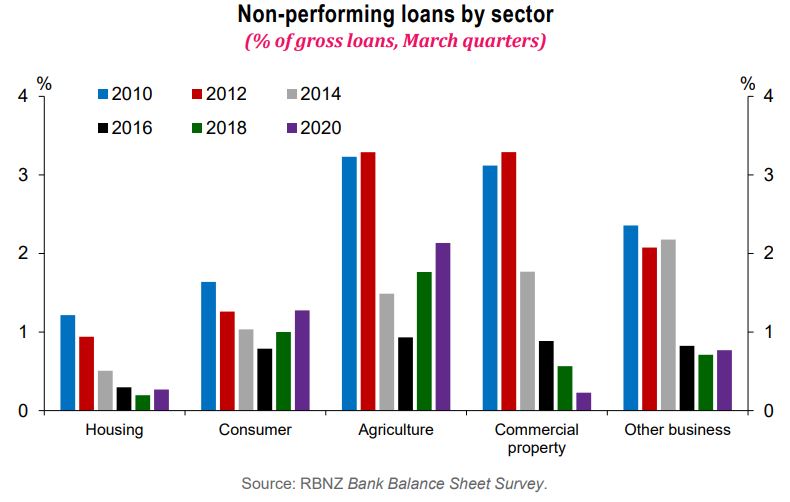

Banks aren't required to treat this lending as non-performing. Thus the latest figures from the Reserve Bank's Bank Financial Strength Dashboard show total non-performing loans across the sector of $3.488 billion at June 30. That's equivalent to 0.76% of total bank loans of $457.772 billion.

Reserve Bank guidance issued in March said banks should treat loans where borrowers are taking advantage of COVID-19 deferrals as performing and not in arrears for capital purposes. If a loan is recorded as being in arrears, normally this significantly increases the amount of capital the bank lender needs to hold against that loan compared to when it's treated as a performing loan. Under accounting rules banks are, however, required to consider future expectations in their loan provisioning when reporting financial results. This includes a future loss model with the bank's view of the outlook for economic conditions driven by the likes of unemployment, Gross Domestic Product and house price movements. As of June 30, New Zealand banks' total loan provisions stood at $3.143 billion.

Now, we don't know what percentage or value of the deferred loans will need to be treated as non-performing when the scheme is ultimately ended, whether that be March or further into the future. But here are a couple of calculations speculating on where banks' non-performing loans might end up. Remembering that non-performing loans are the combination of loans classified as impaired, and loans at least 90 days past due.

If, say, 10% of that $73.7 billion needed to be treated as non-performing, that's $7.37 billion worth of loans. Add that to the just under $3.5 billion of non-performing bank loans at June 30 and you'd be at $10.86 billion of non-performing loans. That would be equivalent to 2.4% of total bank loans at June 30. For some context in March 2011, after the Global Financial Crisis and just post the big Christchurch earthquake, non-performing loans were at 2.1% of total loans.

In a worse case scenario if 25% of the deferred loans end up as non-performing loans, that'd be $18.425 billion. Throwing those in with the June 30 non-performing loans gives you $21.9 billion worth. That's 4.8% of total bank loans, as of June 30.

In something of a statement of the obvious a paper from the Bank for International Settlements (BIS), the central banks' bank, pointed out in June that whilst an "indispensable lifeline" to borrowers impacted by COVID-19, loan deferrals increase future risks to both borrowers and banks because the missed payments are not forgiven and must be repaid.

The BIS paper said the financial stability implications of payment deferral programmes will be driven by the extent to which borrowers will be able and willing to repay their debt obligations once the payment holidays expire, especially in the absence of a government guarantee.

"The famous American investor, Warren Buffett, once said 'It’s only when the tide goes out that you learn who has been swimming naked.' The cumulative impact of COVID-19 and payment deferral programmes on bank balance sheets depends on many factors and will only become apparent over time. Therefore, the timely classification and measurement of credit risk is critical for banks to provide confidence to supervisors and their stakeholders on their financial health. Delaying loss recognition until the tide goes out may leave banks and supervisors with fewer options for dealing with the repercussions," BIS said.

The deferred loan figures come from the New Zealand Bankers' Association (NZBA). For consumer lending these show 88,558 customers making reduced loan repayments on loans valued at $27.5 billion. Another 61,063 customers had deferred payments on all loans to the value of $20.9 billion. These consumer lending figures, as of July 31, cover home loans, personal lending, credit cards and arranged overdrafts.

NZBA figures for business lending show 14,511 customers making reduced loan repayments on $16.3 billion of loans. A further 3,383 customers have deferred all loan repayments on $1.2 billion of loans. Another 3,533 customers have restructured $7.8 billion of loans due to COVID-19. The business lending figures include temporary or term business/corporate lending, stock or equipment finance and arranged overdrafts.

The vast majority of deferred lending will be secured lending. Home loans, for example, are secured by the bank against the property the loan is provided to the homeowner for.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

58 Comments

Hi Gareth, Article mentions data but does not mention the affect of it in NZ economy in diffetent probable scenarion - how bad will it be and its impact on economy and housing market in particular being major indicator of rock star economy in NZ and truly so as only sector that is booming despite panademic as getting all out support by government and reserve bank than other busineses.

Though it mentions that even if 10% default will be worse than GGC to bank but what all that will mean to economy and genetal public.

The NZ economy hasn't been a rock star economy since the late 1960's, when we had trade surpluses.

The only economists that promoted NZ as a rock star economy were the bank economists, who are nothing more than sales people; given confidence to the overseas lenders who kept the ponzi scheme going.

Ask these bank economists what the solution to this indebtedness, and they wont have one; because there isn't one without socialising the banks losses. Bank nationalisation.

Oof, that's a kick right in the reality gonads.

Surely to bank economists indebtedness is the solution not the problem.

And that primarily to build a facade of growth built on massive, record household debt and billions of dollars exported to Australia each year.

This running up our debt massively to pretend we are performing well, nurturing and inflating a protected sector through that massive debt...shades of Muldoonism.

The Deferral - is this why banks are being so tough/tight on new lending?

Or is it just pessimism on future joblessness, and future property price slumps?

It’s high-time the banks showed a little altruism.

Undoubtedly, they’ve profited enormously from housing loans over many years..... How about giving a little bit back to those who are struggling!

TTP

"How about giving a little bit back to those who are struggling!".. they are, it's called loan deferrals and low interest rates. Do you seriously think they should wipe segments of loans??

Hi Hook,

If anything, loan deferrals will add to banks' downstream profits - and well after interest rates have risen from current levels. They'll be able to hold their mortgagees to ransom for longer.

I'd like to see the banks dip into their fabulous profits - and now.

Most bankers that I've come across live in either Ponsonby or Karori - or Hokowhitu in Palmerston North - and they drive German cars......

They could give a little more.

TTP

And for anyone who thought the confusion of the Government response to Covid19 gave them an opportunity to grab some 'free' money (replacement wages) that they might not be entitled to, be aware that the Integrity Intervention Unit of the IRD is out and about with enthusiasm. There's cross-matching of all sorts of data going on.

Already had a phone call from MSD about round one, expecting a 'please provide your workings' for the resurgence subsidy as well. As they should.

We had same within two days of round one, got ird phonecall so I thought that was reasonably diligent.

So you took both subsidies?? Interesting, given some of your comments here.

Everyone's a socialist in a recession.

Besides which, every property investor is a welfare beneficiary in NZ these days anyway.

Bollocks IR are out and about. Because.......MSD are doing this....not IR.

By the time a lot of the deferrals wind up, the borrowers will be on interest rates a lot lower than they were when COVID hit. This will make it easier for borrowers to ride it out... at least on the family home. The risk as I see it is debt to pay for holiday homes, vehicles and a business.

Ntokyo, This too is based on assumption that only part earning/wages of family income is affected.

Only when the tide goes out do you discover who's been swimming naked.....old saying but well said by Warren Buffet in a recent interview in current situation.

It also depends when the family home was purchased - at the peak but more imiprtant to watch out is unemployment data and business closing down data as that will have domino effect in the economy including asset class, once various subsidies and stimulus ends.

Uncertain time boosted by printing of money with hope that this uncertainity will end before the stimulus ends and everything gets back to normal BUT will it OR again more printing and stimulus.

Wait and Watch

As I have said before, the hard times are still to come.

Let's hope that we don't have another lockdown - if we do it's gonna get real ugly.

If a loan is recorded as being in arrears, normally this significantly increases the amount of capital the bank lender needs to hold against that loan compared to when it's treated as a performing loan.

So interest rates on savings go up, right?

Without the current artificial environment the nature of a bond is that in the market the return increases with increased risk but TD’s have fallen from 2.9% to 1.5% to .5% and heading to zero and the risk of bank default and a possible OBR event increased substantially with some 140,000 households on some form of mortgage deferral.

The constant news feeds of Mortgage holiday assistance, help for business, partnering with the Government to loan money to business and relaxing of RBNZ of capital adequacy requirements. There are absolutely zero statements on protecting deposit holder’s money. Instead we get BS statements of be bold and take risks and lend with deposit holders’ money from Robertson and Orr. The finance minister refuses to bring forward the deposit guarantee not that one being proposed is of much use with limit of 50k whereas the Australia and the US have 250k. Interestingly since the US federal deposit scheme was introduced in 1933 by President Roosevelt it has cost the tax payer absolutely zero.

Government is interesfed in protecting borrowers - no problem BUT why not take intiative to protect savers.

Why is ni expert / media asking government : Just like trying to protect borrowers / debt why is government not taking steps to protect savers.

You can't have low interest rates/mortgage deferrals on one hand and have increased or stable deposit rates. I would have thought that was pretty easy to understand

We saw in Cyprus, Greece and Ireland the inability of governments to preserve their sovereignty on behalf of their population in the face of threats from foreign banks. Given the share of debt and trouble held by Australian banks, you wonder at what messaging is flowing between Aussie banks and our RBNZ / government right now.

It's become obvious that all the intervention from government printing is now the new normal and people are treating it as such. Any attempt to wind back wage subsidies or loan deferral schemes will result in mass economic carnage. That means no gubbmint of any colour will do it.

The past decade of printed money based increases in "economic growth" showed that as soon as governments tried to remove their distortions, their economies convulsed and threatened to tip over. So governments quickly had to to reinstate their distortions and keep increasing them to create more "growth" again. If you think distortions introduced by consecutive NZ governments are any different, I have news for you. The pain will never be felt, the can will be kicked further and further.

Can has to burst at one point and that point is not too far away

Yes but I and many others have voiced that over the last ten years and yet here we are, the can is still moving down the road in one piece.

A piece of my brain is starting to believe the impossible.

I think in the next 6 months we will see a mix of further can kicking and d day arriving.

More can kicking will limit some of the carnage, but only ultimately to a point.

Bank's provisionings are clearly inadequate, considering the big amount of mortgage debt being supported by temporary relief measures. I can see the credit rating of NZ banks being on a downward path.

There is a potential mountain of bad debt that is going to hit the housing market, which no zero (or negative) interest policy is going to be able to remove.

And there are still savers ready to invest in NZ bank's term deposits for a return of 1% p.a., and with no government guarantee ?? And speculators forecasting increases in house prices, in an overly inflated assets class subject to future potentially overwhelming strains ?

The whole thing does not make much sense to me. It makes much sense to me as the flocks of investors queuing to buy Hertz shares.

Hoping that things will magically sort themselves out with more QE and negative rates is utterly delusional.

Totally agree. There are absolutely zero statements on protecting deposit holder’s money. Instead we get BS statements of be bold and take risks and lend with deposit holders’ money from Robertson and Orr. The finance minister refuses to bring forward the deposit guarantee not that one being proposed is of much use with limit of 50k whereas the Australia and the US have 250k. Interestingly since the US federal deposit scheme was introduced in 1933 by President Roosevelt it has cost the tax payer absolutely zero.

Not putting in place an NZ government guarantee while protecting those who have never learnt fiscal conservatism and live a life fuelled on credit upgrading houses and buying a boat and the latest iphone, car and 8k TV instead of paying off there obligations is a disgrace,

I wholeheartedly agree, 100%. Depositors are being asked to subsidize speculators and to take risks with no corresponding reward. It is just not worth it.

Experts in interest.co.nz should take intiative to highlight and ask from government.

Why Is borrowers / speculators supported at the cost of depositors (Many depositors are of age where taking high risk may screw their retirement)

Orr has stated that he is helping the 90% of people indebted at the expense of the 10% with cash and this ok. Orr and Hawkesby et al are a disgrace

Agree. Others have been quick to claim Orr should be exempt from criticism or pressure but I cannot agree. Reserve Banks have a role to push back on government too for the right policy tools to manage inflation without adverse effects, where the RBNZ in recent years has very happily and openly spoken of their desire to push up house prices for the 'wealth effect' instead.

Thus, wider NZers whose wages are being devalued and wealth is being transferred by the RBNZ to asset holders have every right to get angry and take action to pressure the government and the RBNZ.

The majority of the 10% with cash. Got that cash from the 90% who are indebted. Once you cash out of the Ponzi you are still exposed to the realities of it.

I would like the Interest reporters to expose daily that the Government is robbing kiwisavers with its FIF tax regime to the extent they are in international equities. On 1 April 2020 they happily tax everyone on 5% of their kiwisaver balances even though the vast majority had gone down substantially. Further as they recover during 2020 they will tax them on 1 April 2021 on another 5%. So yes, we get taxed when kiwisaver makes losses and then get taxed again when the recover to pre-existing levels. So this Government is not doing any favours to kiwisavers. It’s a tax cash cow for the Government that nobody wants to talk about. The same applies to anyone invested in equities outside NZ and Australia. All the while gains in houses supported by Orr and Roberston remain tax free.

" Government is robbing kiwisavers with its FIF tax regime to the extent they are in international equities." It's actually called an FDR rate and the reason is the majority of Companies on offshore exchanges pay little or no dividends as opposed to most NZX Companies that do. If you choose to place a large amount of money into KS schemes then that is the price you pay. The idea behind the FDR was to promote/support investment into NZ Companies listed on the NZX. You should also remember the $512 tax free "gift" provided by the Govt should go a long way towards paying your FDR requirements - if it doesn't you have far too much money sitting in KS.

NZ is far too small for the amount of money that's available for investment and totally insufficient for asset diversity. FDR is a smokescreen as the flip side is the CV (comparative value) tax option so even if the FDR was abolished the CV would have you paying unrealised capital gains tax. Fairness has little to do with FDRs and CV's implementation. It was just another revenue gathering exercise. Far easier to implement than a realised only capital gains tax on residential housing and generally unknown to those mainly concerned with residential housing CGT

Interesting point you make re: FDR etc, which I don't necessarily disagree with. As for NZ being too small re: investment, I'm not so sure. NZrs had ample opportunity via NZSF or ACC or even directly to invest in a number of companies - Synlait, Oceania,Rocket Lab,Pacific Edge,ATM, to name a very few. Most chose to turn their backs on these companies and the result was the companies went elsewhere for their funds. When NZrs in general and many commentators here in particular get over their fixation with housing (it is what it is) then perhaps investment can be repurposed. Bleating about the housing market failings actually does nothing to address the issue and I dare say most commentators here aren't subject to those perceived failings anyway

Its actually called the Foreign Investment Fund rules. The FIF regime was not designed to promote investment in the NZX? It doesnt apply in Australia. It had been around a long time before it starting applying to kiwisaver. Originally the FIF and CFC rules were to tax holdings in jurisdictions that did not have a similar tax regime to NZ. We had a grey list of exempt countries including USA, UK, Canada, Germany, Australia, Japan, Norway and Spain. Then in late 2000's Michael Cullen increased its application to all countries except NZ and Australia. The overall impact on your retirement funds for a lot of working NZers would be a 100k plus less at retirement due to the money not compounding and being taxed on an unrealised basis than taxed when investments are realised. And a $512 rebate annually makes up for this?

A good history of the FIF rules by Craig Mac. They came in during the late 1980's but conveniently the grey list exemptions were removed when kiwisaver came in.....

https://www.stuff.co.nz/southland-times/business/78448898/taxing-times-…

All subsidy and stimulus ultimately come down to protect housing market.

A long time ago I used to believe in saving. We were fed the line you must save and debt is bad.

Fortunately I saw the light and wasn't able to save due to NZs low wages, but I was able to borrow. Then I figured out why scrimp and save to pay it off with rates falling. It's hard to undo the thoughts of a lifetime but it does seem like debt is the new savings.

May be best for banks to simply forgive all the mortgages under deferral under a Jubilee scheme.

The RB can underwrite this, or NZ & others could launch an attack on the Cayman Islands & retrieve the trillions in hidden trusts/shell companies.

Current ultra-low interest rates are already a significant form of debt forgiveness.

The devastating result of which (further asset bubbles, mis-pricing of risk, destruction of savings and therefore of future opportunities for productive investment, mis-allocation of resources, potential loss of confidence in the currency and in the financial system etc.) will be make themselves clearly visible in the future, of this there is no doubt.

There is no free lunch.

Plenty of free lunches in the shell companies in the Caymans etc, and in the Apples, Googles etc

Although they aren't by any means free for the lowly taxpayer who bears the brunt of government income by way of PAYE and GST;

https://www.interest.co.nz/news/99949/budget-2019-summary-all-tax-colle…

Well done on finding that info - quite interesting. The question I would ask is, given that supply of labour is about the lowest risk form of commercial transactions what would you replace it with and how would you factor in an RFR? Given that Company Tax is a 1/3 of PAYE, does this not suggest that a Company is carrying 3X the risk that an employee is to make the same dollar?

The response was to the manner of companies relinquishing their tax obligations thru creative accounting and offshoring of entities in tax havens - i.e., most directly at the multinationals that screw every taxpayer the world over.

The IRD could easily hire the former architects of these structured finance transactions and transfer pricing structures to understand them and attack them. The ATO in Australia has successfully done this now for a number of years with some big wins against multinationals. Instead our IRD focuses of dumbing down its skilled workers and transforming the business with very few skilled workers left.

That's fine if the government then hands everyone else a free house too.

In the space of a week - Another ¼ acre section gone

The inventory of these properties is diminishing

Last week 11 Hayr Road Three Kings sold for $2,900,000 land value only at $2377 per square metre

This week 18 Arthur Street Ellerslie sold for $3,813,000 land value only at $3140 per square metre

It will be bulldozed - might try selling it for removal - unlikely

This week a house on 1214 sqm section in the central Auckland suburb of Ellerslie sold for $3.813 million – $1 million above 2017 CV

https://www.oneroof.co.nz/news/38376

Pay attention to the price per square metre for the land

One Roof news /article are cherry picking to reflect and create FOMO.

This is not to undermine that housing market is very strong - it is all time high and has never been as strong as now.

At least there is a saving grace in that the residential property market is going absolutely mad, and people should be able to get out very quickly and profitably if they need to.

That said for most of us, paying the mortgage is a lot cheaper than renting in the same area.

It was cheaper but now if paying premium for the same house than the affect of low interest is nullified.

I wouldn't quite agree with your last sentence. In upper value areas it is still much cheaper renting, unless you have a large deposit. It's typically equivalent in mid value locations, but assuming a good deposit.

Delay means same to pay plus extra interest in 6 months. At which point unemployment will be higher. Extend and pretend indeed

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.