By Gareth Vaughan

With the Government and Reserve Bank having enabled banks to offer borrowers mortgage repayment deferrals, the Commerce Commission is preparing guidance for lenders on how to apply the Credit Contracts and Consumer Finance Act (CCCFA) to borrowers who experience financial difficulties due to COVID-19.

On Friday ANZ, ASB, BNZ, Kiwibank, TSB and Westpac said they had their ducks in a row to offer mortgage repayment deferrals for those whose incomes have been hit by COVID-19. The repayment relief is available to borrowers with loans secured against residential property, including owner-occupiers, investors and businesses. This is after Finance Minister Grant Robertson announced plans for a mortgage holiday scheme last Tuesday.

Consumer watchdog the Commerce Commission oversees the CCCFA. It is designed to ensure consumers are able to make informed choices, know what they're agreeing to, and are able to keep track of their debts. For lenders, the CCCFA requires them to act responsibly at all times.

"We are working on guidance for lenders applying the requirements of the CCCF Act to their work with borrowers who experience financial difficulties due to COVID-19. We expect to be in a position to provide an update on this later in the week," a Commerce Commission spokesman told interest.co.nz.

What the RBNZ capital concession on non-performing mortgages means

As reported on Friday, the Reserve Bank has issued guidance to banks that for borrowers taking advantage of COVID-19 mortgage deferrals, the loans should be treated as performing and not in arrears for capital purposes. If a loan is recorded as being in arrears, normally this significantly increases the amount of capital the bank lender needs to hold against that loan.

So just how much relief will this Reserve Bank concession provide the banks on loans soured by COVID-19?

It differs for banks using the standardised approach, where their credit risk exposure is prescribed by the Reserve Bank, and banks using the internal ratings based (IRB) approach, where banks set their own models for measuring credit risk exposure which they must then get approved by the Reserve Bank. The IRB approach is used by ANZ, ASB, BNZ and Westpac, whilst all other New Zealand banks use the standardised approach.

The Reserve Bank says for standardised banks the average risk weight is approximately 38% for performing home loans, while past due loans have a 100% risk weight. That means a standardised bank loan moving to past due from performing requires about 2.5 times more capital.

IRB banks have an average risk weight of about 30% on performing home loans. When an IRB bank mortgage moves from performing to non-performing a significant capital increase is required.

"The calculation for defaulted residential mortgage loans effectively means the bank needs enough capital to cover the full loss given default estimate for the loan. There are some other adjustments in the calculation, around the treatment of expected losses and how much the bank provisions for any losses once the loan becomes defaulted," the Reserve Bank says.

"Using typical NZ IRB bank estimates, we estimated that an IRB bank would need approximately eight times more capital per dollar of loan, when the loan moves from performing to defaulted."

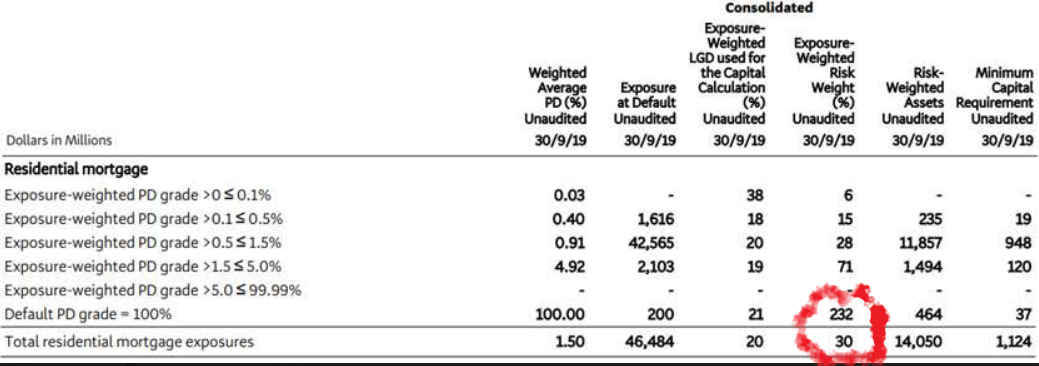

The example below, from BNZ’s 2019 Annual Report, shows an average risk weight across all residential mortgages - both performing and defaulted - of 30%, and an average risk weight for defaulted loans of 232%. (See red circle below). It also shows the bank requires minimum capital of $1.124 billion against $46.484 billion of exposures.

What about building societies and credit unions?

Non-bank deposit takers (NBDTs), including building societies and credit unions, are not included in the government-RBNZ arrangements enabling banks to offer mortgage repayment deferrals

" We are in contact with them and considering options,” a Reserve Bank spokesman says.

NBDTs accounted for just 1.14%, or $3.165 billion of the $278.387 billion of housing loans outstanding in January, and 4.2%, or $5.086 billion of the $121.212 billion of business loans, according to Reserve Bank statistics. However, their customer base is skewed towards the regions and includes some customers who the major banks wouldn't bank.

First Credit Union, which has 65,000 members, has already instigated a COVID-19 interest only option on loans for 12 months, says general manager Simon Scott.

"The requirement being that the members circumstances have been affected by COVID-19, loss of earnings etc. The member is also able to change back to principal and interest at any time of their choosing within the 12 months," Scott says.

"As a member owned financial co-op we are keen that our members understand that they should take the deferral for as short a time as they can manage, as it is in their best interests to commence repayments as soon as possible. Our average LVR [loan-to-value ratio] is very low so we are more than happy to assist our members in this way."

"We have had direct contact with the RBNZ and are very happy with the way they have interacted with us," says Scott.

Tony Cadigan, CEO of the Nelson Building Society (NBS), says NBS is working closely with customers impacted by COVID-19.

"As a small local building society we have intimate knowledge of our client base and a real willingness to help them during this difficult time. We are offering loan restructures, interest only, loan holidays, overdrafts, and temporary excesses. As most clients needs are different we personalise a package best equipped to assist them individually," Cadigan says.

"NBS is fortunate to have maintained conservative lending policies, so with low average LVRs we are well positioned to support our client base when they need us the most."

CEO Paul Bywater says the Wairarapa Building Society is "being very responsive" to its customers, with financial hardship packages being put in place. More information is available on the Wairarapa Building Society website.

Bywater cautions, however, that mortgage holidays are not the answer for a lot of people, merely kicking the can down the road.

"[We are] looking to individual customers for the best option for them," Bywater says.

Gavin Earle, CEO of NZCU Baywide which has about 60,000 members, says the credit union is in touch with the Reserve Bank and working through a range of options with the regulator.

"We continue to work in with our members who have been impacted, to put in place the best solution for their individual circumstances. Our team have a range of tools to put in place appropriate support for these members with personal loans and/or home loans who have affordability issues as a result of COVID-19," Earle says.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

6 Comments

I hope that for investors, their ability to qualify for the holiday is tied specifically to stoppage or significant reduction in the amount of rent they collect from their tenant.

& I hope in that case that the tenant is willing to pay to the landlord their share of the extra interest that the landlord will occur over the rest of the mortgage, given that they still have to pay the money back and interest accruals each day you are on a repayment holiday. I wish that a repayment holiday meant no interest accrued as I would sign up today for one, but alas it doesn't work that way.

The term mortgage 'holiday" is a misnomer and it has created a lot of misunderstanding, it's clearly a mortgage payment "deferral" not a "holiday"

Exactly, and tenants are taking advantage of this now sanctioned by our new patron saint.

"As reported on Friday, the Reserve Bank has issued guidance to banks that for borrowers taking advantage of COVID-19 mortgage deferrals, the loans should be treated as performing and not in arrears for capital purposes."

So more lending (more free capital) is being encouraged as bad debts mount. Not good.

In any normal situation when a loan goes into arrears the capital requirement goes up.

As the big Aussie banks are already using their own credit risk capital models (which are at a discount to the standard approach) they are going to have a huge bump in capital requirements after the holiday period is up and the borrowers still can't afford to repay the loans.

So where is this capital going to come from ?

Yip, it's a deferral.. it's compounded re-payment in the end. But like personal 'holiday' you have to pay for it, but if you clever enough you can have company pay your 'holiday'.. same principle here. Alternatively, as the whole world faces the same banking situation then borrowing of that reverse mortgage ideas? I would suggest to put that hard core asset quickly...into the up coming slow deflationary market, a controlled descend. You do have an option to wait, but at what cost? - still who knows? if & when the balloon will receive another Helium injection again. Both OZ & NZ still hoping that their current sponsors from CCP are willing to do remote capital injection again.. this time via 'remote online services'. As travelling restriction worldwide start happening.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.