The Reserve Bank (RBNZ) has agreed to help banks extend the mortgage repayment deferrals they’ve been offering their customers since the end of March.

RBNZ Governor Adrian Orr confirmed this on Wednesday, further to his deputy, Geoff Bascand, a couple of weeks ago saying he didn’t want to see an abrupt end to the offering.

Orr hoped to finalise details with banks next week.

He urged people not to flood banks with inquiries, as the details of what will be offered are still being ironed out.

“As always, an extension is not permanent,” Orr said.

It is ultimately a bank’s decision whether it enables a customer to defer the principle and interest repayments on their mortgage.

What the RBNZ can do is treat the loan as performing, rather than impaired. Impaired loans require banks to hold more capital against them.

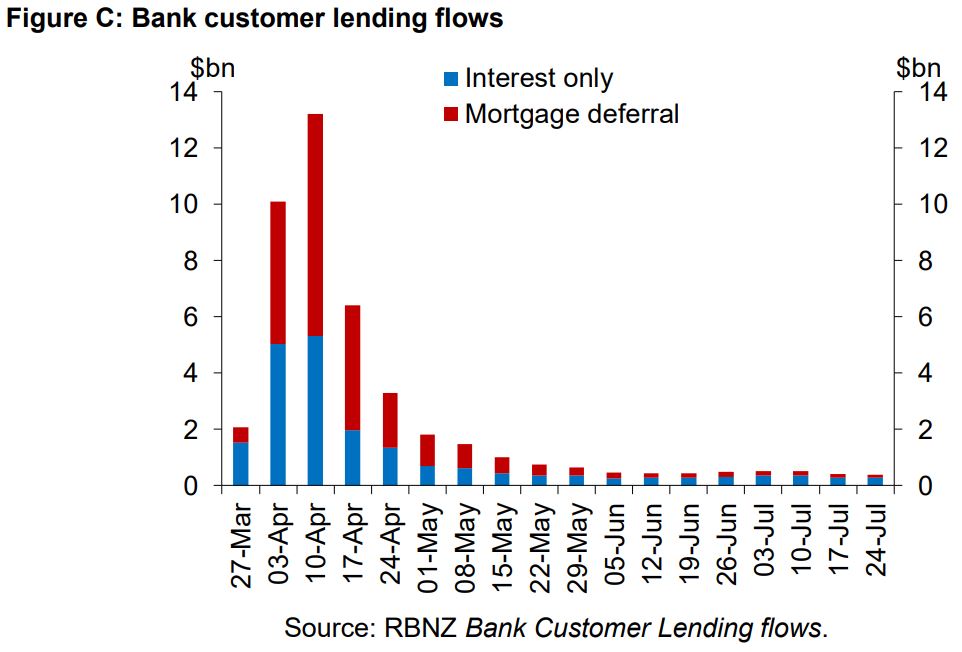

Bascand on July 31 said there were $20.6 billion of residential mortgages that had principal and interest payments deferred, and a further $18.3 billion of mortgages that had moved to ‘interest only’ since the onset of Covid-19. This represented 14% of the banking sector’s mortgage book.

80 Comments

“As always, an extension is not permanent,” Orr said.

Technically not permanent if you have to keep extending it every 6 months.

Ultra low interest rates are also not permanent, right?

Who has suggested ultra-low rates are anything other than permanent?

Sort of reminds me of the kiwisaver holiday, which people can just keep extending, if they don't want to pay into it.

What amazes me is that we are towards the end of a major wealth building phase in the monetary cycle yet people are living month to month with little to no savings to support themselves and their businesses. Seems that the instant gratification buy it now and pay it off in the future is back firing spectacularly across the world. The Collective answer is to issue more debt on top of the existing debt that is crushing individuals, families and businesses. There will eventually be a day of reckoning when the total amount of debt issued is simply too much for the system to bare. At this point can we expect the reset button to be pressed.

And we have record household debt levels.

The "wealth effect" seems more the realm of special effects. We resist productivity growth, we resist creative destruction, we resist giving families affordable foundations for building a life...instead we only live more and more beyond our means, while it's not so long since we tut-tutted at Greece for the same.

The economy is now confirmed to be 100% about house prices.... pathetic

How do you figure that? Do you think the smart play is to just let half the country bankrupt?

14% according to the article, and yes.

14% is the primary effect, the secondary effect is a generalised bank collapse and depression. This crash would be so dramatic and shocking it may take a decade to recover and it would be entirely the creation of monetary policy failure.

All that you have described will happen anyway so best to let it happen globally. Best to let happen now. “go hard and go early”, so we can start to rebuild a better world.

No experts and No reserve banks knows what they are doing - experimenting and hoping to delay the inevitable as the ride that they are on cannot be even slowed - forget about stopping. Instead will have to keep adding fuel from 60 billion to 100 billion to 120 billion to 150 billion and interest rate from 0.25% to minus 0.25% to minus 0.75% and so on.

Father Forgive Them for They Know Not What They Do

Don't kid yourself...

These banksters have known all along what they have been doing. Maximise their short term bonuses, privatization of their profits and socialize their losses.

The're gone too far down a rabbit hole they now cant get out of, and worst still for them they cant even escape to their private island retreats; and the numbers seeking natural justice are mounting against them.

I can see them bolting their doors shortly; pun unfortunately intended.

Hence perhaps why we need covid 19 or 20 to restart a new world??

The monetary policy has already failed. Economy is painted into a corner by central bank stupidity and property greed.

14% is the primary effect, the secondary effect is a generalised bank collapse and depression. This crash would be so dramatic and shocking it may take a decade to recover and it would be entirely the creation of monetary policy failure.

People usually think "I'm not in the 14% so I'm alright". Similarly, they think "I've paid of my home so I'm alright".

It's amazing how little people understand how property bubbles affect everyone in some way on the way up and down.

It would have been smart to not let the property bubble form. But it has formed.

Most people would rather see a bunch of greedy and stupid property speculators get wiped out than a currency collapse.

Couldn't agree more

Problem is, the greedy speculators got out already, and the 'mom and pop' investors are left carrying the can along with the struggling FHB's looking to start a family.

The very smart ones have. The rest of them are doubling down. Go join up some of the facebook property speculator groups where the character and intelligence of these people are on full display. It's quite a spectacle.

These mom and pop investors volunteered to be bag holders. The way for FHB's to stop struggling is for the property market to correct.

Please.

"'Mom and pop' investors" are speculating all the same.

Remember that policy makers falls in that bunch...

Even a 20% decline in prices would just take us back to levels of a few years ago, was anyone saying houses were undervalued or cheap then?

And these idiots say they don't want an "abrupt end" to the extend and pretend - stopping something by definition will be abrupt, doesn't matter if it's now or in 5 years time.

As Sharon Zollner put it - "at some point, someone is going to have to be allowed to make a loss"

Yes its called "Market Price Discovery" and houses should be allowed to exist in a free market, not artificially held up by this government.

Surely didn't take a pandemic for you to figure that out?

Surely didn't take a pandemic for you to figure that out?

Same in Australia..... big problems emerging over there with the property media, I mean news outlets trying their best to spruik any slightly positive Housing news. What did people say on the way up... “ Auckland is about 6 months behind Sydney.” Wonder if that is the same on the way down?

Let's see how long they can keep going like this! This virus has changed the way how we run the economy now. Remember, the factors kept our economy running strong before, such as tourism and education for international students, are not working now. Endless injecting money into housing market and defer mortgage repayments might make it even worse.

Might? You're an optimist!

I'm surprised the New Zealand Dollar isn't yet on a hiding to nothing with these clowns in charge.

Their number one priority, as always, is shamelessly pushing property prices higher while devaluing the savings and wages of productive kiwis.

Non performing loans are performing. Cool. Repayment holidays forever. Cool. Anything and everything to prevent the insane housing bubble they blew starting to leak air.

every country is effectively doing the same thing, so the currency will likely just tread water. but perhaps depreciate a bit as no longer "safe"

i was suspect of gold/bitcoin or whatever before because in nzd it would be relatively stable, i.e. usd depreciation. but now? maybe some upside to hedge against devaluation of nzd

@Jen'ee - I don't understand the graph. Is it reporting the value of new interest only/mortgage deferrals each month? Is there any data on the total ($39B) value of these and the rate of change?

Yes, so it's reporting the value of loans that have gone interest only and have been deferred each week. You can see people rushed to get relief at the onset of Covid. The question is how many of these people will take up the opportunity to extend that relief a bit longer. You can see the raw data here. This series appears to have been updated since Bascand did his speech.

I have to say it looks more and more like the Banks and their Global Shareholders are pulling the strings in NZ, and the Govt is meekly following along supporting long term debt enslavement of the NZ population. An asset reset is beyond due - just let it happen and get it over with like Iceland did in the GFC. The other article today had ASBs forecast well down as they make allowance for loan impairment. Is it worse than we think...?

"What the RBNZ can do is treat the loan as performing, rather than impaired"

Extend and Pretend: A pure, administrative victory snatched from the jaws of economic defeat.

Not necessarily. It makes a certain amount of sense.

If the banks can have a "quiet word" with those borrowers that they (must by now) know are unlikely to ever repay their loans, they can encourage them to liquidate during the extension period. Thus save the borrowers from bankruptcy, and rid the banks of the impaired loans at the same time.

There is no way the banks will do such a thing. Just look at the environment they are in - they damn well know that when they eventually ask the RB to bail them out, they most certainly will.

Like Ireland where the ECB intimidated the Irish government into taking on property speculator debt to protect the ECB, the Aussie banks will be pushing the New Zealand taxpayer to absolve them off their own risk and irresponsible behaviour. If that happens we should consider what the NZ taxpayer should receive in return.

What most folks don't realize is that the central bank is providing a window for the banks to gradually put pressure on non performing loans i.e. their customers.

Heart of hearts most economists know that there is going to be a blood bath, however their intent is to minimize the gore at the cost of the tax payers, for now.

Bugger me. There is seemingly no limit to my list of "things that 12 months ago, I would have deemed inconceivable".

Inconceivable! - Princess Bride Guy

Ah. How we miss the more innocent days of The Great Vizzini, when being an ill informed, boastful, blaggard was a point of mockery, rather than a political qualification.

Hmmm, so let's play the game of what things you now deem inconceivable in 12 months ? Just for fun and also to open up our minds.

Can't wait for your list GN

Well, now of course, i have adjusted to the "new normal" so am prepared for all kinds of unholy unprecedented shenanigans to be unleashed... I can give you a list of things that until recently I would have considered inconceivable but now more possible maybe?

UBI?

UBI and MMT seem highly possible now. Hells even debt jubilee doesn't seem outside the realms of possibility.

Some of my thoughts on what may have become possible err to the darker side though... civil wars in Western countries (alt-right vs extreme left), demise of western democracy (arguably happening before our very eyes already), WW3.

Buy bitcoin

I started getting interested in bitcoin in 2010 and was mining by 2012. But thanks for the advise.

Gingerninja, a book you may enjoy - if darkly - is Stefan Zweig's The World of Yesterday. An Austrian Jew who grew up in the heyday of liberal thinking, globalist and optimistic Europe only to see it decline into a series of unthinkable events. A brilliant read, though.

I'm plastering at the moment and getting through a lot of books via audible...just on Mark Blythe's "Austerity, history of a dangerous idea" currently but have queued you recommendation up for next. Thanks!

I shall check out Blythe, cheers.

My list of things that are absolutely impossible in 12 months:

1) A 90%+ effective COVID19 vaccine - corona viruses are just too tenacious and tricky

2) Trump as president - definitely off the table given demographics and his track record

3) Hot war in the South China Sea and/or just Taiwan - nobody is that silly or accident prone

4) Average AKL house price below $750k - I scrunched up my imagination but just could not conjure the image

Funny because I think all those things are probable.

2) Trump as president - definitely off the table given demographics and his track record

I mean, I would bet actual money that he WILL win the election.

I am sure Trump will win, went on tour across USA late last year and the Americans love him

Trump is guaranteed to loose the election, actually getting him out of the White House is the real problem.

I've recorded a Calendar item for 1 year time to see how wrong I turned out to be.

How about the Dems printing $10T next year... heard it here 1st

Immigration numbers intentionally reduced by any government (i.e. either Labour or National coalitions)

What does a business do when their main debtor owes more than that creditor business can afford to lose?

Most often, grant that debtor extended terms in the hope of repayment.

It rarely works, of course. But that's human nature - Hope.

And what do we have here today from the RBNZ? Hope, that given time all will work out ok.

"When all that's left is Hope, there is no hope"

(NB: I may seem highly critical of the RBNZ, and I am, but frankly this mess is not of their making. They are trying to sort out an irretrievable mess created by Government(s). It shouldn't be the Central Banks' task to rescue the economy. It should never get to that stage. But it has, and all the tinkering in the world by monetary authorities isn't going to save the situation. It's passed saving. All that matters now is how each of us is prepared for whatever we think is going to happen.

Why do I feel like enabling banks to treat loans which people have stopped paying as performing rather than impaired is basically just accounting fraud?

Because it is fraud.

Exactly. It's the total destruction of all financial savings, just to protect bank profits. Considering NZFs voting demographic, its truly breathtaking that hes doing nothing to stop it.

The requirements to provide higher capital for impaired loans were introduced so shareholders take more risk , not just depositors. It worries me that they are taking this requirement away, probably when it is most needed. If the banks don't want to increase capital requirements, they should get as many people repaying as possible, so there's a more clear idea of how many really are stressed, and what the losses might be.

I'm not supprised by the extension, but would like to see the banks only offer this to customers who really need it, and not people who are just trying to free up cash. Then we will all have a better idea of true impairment.

Ahhh yes, where is Printer8 now? As I remember he scoffed at the idea when I said this would be extended forever...

Extend and pretend, these will never be paid back, further painting ourselves into a corner, adding more and more fragility to the financial system.

Hi blobbles

I'm here, so wrong on two accounts. :)

Your memory is playing tricks. I never been of that view; in fact if anything of the view that RBNZ and government actions still have a distance to go. I'm just content, just sitting, watching and waiting for whatever and in no hurry.

However, I find your comments amusing - you claimed considerable experience in bank lending but hadn't even heard of mortgage "holidays" until they were announced and then posted in anger as you thought it meant free money. :)

Where did I claim I had no idea what a mortgage holiday was? This is the problem with reading Internet comments without context, everyone assumed I was saying one thing, without carefully reading the comment. Which was that people will not be in a position to pay higher mortgage costs later, having deferred payments now. Hence they will need to be paid out somehow. We see how now by deferring forever and non performing loans treated as performing.

Note you stated:

"It is not deferred for ever - that is not what the term "holiday"in terms of loan repayments usually and commonly means"

As I said then and I will repeat again, if it is deffered forever, is it a holiday?

Now if this was normal bank lending practice, why does the government need to be involved? I know you don't want to think about that, but the reason is that they are back stopping these non performing loans. They will eventually need to bail out the people who are taking these, probably by paying the amount that has accrued during the time the loan was put into "holiday" status, if not even more. That's if the scheme can ever end, which IMO is highly unlikely. But if it eventually ends and bailouts ensue, that will be free money.

I understand that you want to be obtuse with your thinking, but I suggest you think deeper about the implications of a never ending government backed loan deferment scheme.

Cheers Blobbles

I stand by my original comment as you quote. :)

Those paying interest only - but with principal payment deferrals - will still have to pay back the principal at some stage.

Those on both interest and principal deferrals will need to pay both the accrued interest and principal later.

To think otherwise is foolish.

Nice to have that down, if you believe that people will have to pay back both interest and principal, why do you think this has to be government backed?

Come on, you should know what's happening... and why are we now treating non-performing loans as performing? To add to previous comments I have made, I now know 3 people on mortgage holidays, one is saving the money, one has bought a new motorbike and another I talked to last week has used the money "saved" to upgrade their new car. None of them are in any better position to pay back their mortgage in terms of income, I know 2 of them are significantly worse off (their partners have reduced or stopped working). Will they be in any better position to pay off their mortgages once the "holiday" ends? Possibly, if they restructure their loans with a lower interest rate, but otherwise, I have my doubts. Why do you think the government was scared of having everyone come off these schemes, particularly when most reports indicate the economy has largely gone back to normal?

Blobbles

You need to explain to the three people you know what "mortgagee sale" means. Ignorance is great until reality kicks in.

I suggest that you read the bit below from BNZ to correct your misunderstanding.

Cheers

This from BNZ:

"Repayment deferral (mortgage holiday)

You could be eligible to apply for a home loan repayment deferral for up to six months (including a three-month checkpoint). Once confirmed, the principal and interest repayments will stop immediately.

Deferment of all repayments should be considered carefully, as interest will continue to accrue during the time payments are not being made, and added to the amount outstanding. Interest will be charged in the usual way. The amount outstanding and regular repayments may be higher at the end of the repayment deferral period and more interest may be paid over the life of the loan. "

Blobbles - I hope that you noted the bit about "interest will continue to accrue . . interest will be charges in the usual way . . be added to the loan".

You are babbling that I don't understand what I already understand. As being obtuse is clearly your strong point, there is little point continuing.

So is new zealand still free market??? Why are we not letting the market do its course of death and rebirth?

Great question. I think the fundamental problem is governments have decided they are responsible for a certain inflation range. That drives them to control interest rates to try and control inflation, and once the market signal for the price of money is obscured we end up with an economy sloshing around in a casino.

Because too many of those in charge of business, central banking and government agencies have their wealth in property investment. Thus, others must be sacrificed to protect their wealth.

That's just lazy thinking.

The govt are actively delaying the inevitable. It wont happen overnight, but it will happen

Hey Sluggy, yes I agree but how much longer can the madness continue ? How long is too long ? another year ? another two before it all implodes ? what will be the trigger ? Personally I thought the pandemic was the trigger so if this doesn't work I can only think of other things and they are much much worse.

I've been pondering the same issue. For years the signals of mainstream desperation (eg suicide, homelessness) have been building. My current bet for western countries, with the US at the front of the wave, is:

1) The rioting and looting we are now seeing in places like Chicago is what will build into the end game.

2) Politicians who want to scoop those votes promise free stuff and vague things like change, and in office fail to deliver (of course - its all impossible)

3) Zombie corporates, powerless govts, and the waste of destructive revolution sap energy as standards of living collapse into a Greater Depression

4) Asian economies rise comparatively, reorganising to decouple from the west, and they take over more of the lead on innovation, getting ahead on automation and AI (if not already)

5) On the scale of a decade, massively deleveraged (bankrupted, defaulted and written off), western business and households develop fresh determination and start clawing their way back up, but from behind this time

The above is all in the context of my generally apocalyptic view of the future, which is:

1) That an increasing proportion of the population disappear into their shitboxes to play games, be entertained and take drugs etc, subsisting on a UBI and happy enough about it not to go back to step 1. They disappear into the background and have little to do with step 5 except as reliable voters for UBI type govt spending, and as spenders of UBIs

2) Steady degeneration of the environment and exhaustion of resources pushes up costs, making the boom years of the 1950s and 60s for ordinary workers never remotely repeatable this century

Now please tell me I have it all wrong.

We haven't had a free market here since 2007.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.