Although they are providing an "indispensable lifeline" to borrowers impacted by Covid-19, mortgage deferrals increase future risks to both borrowers and banks because the missed payments are not forgiven and must be repaid, a paper from the Bank for International Settlements (BIS) points out.

In New Zealand in late March a mortgage deferral scheme was unveiled for borrowers whose incomes have been affected by Covid-19, offering relief for up to six-months on interest payments or payment deferral. Similar schemes were unveiled around the world as Covid-19 took a grip.

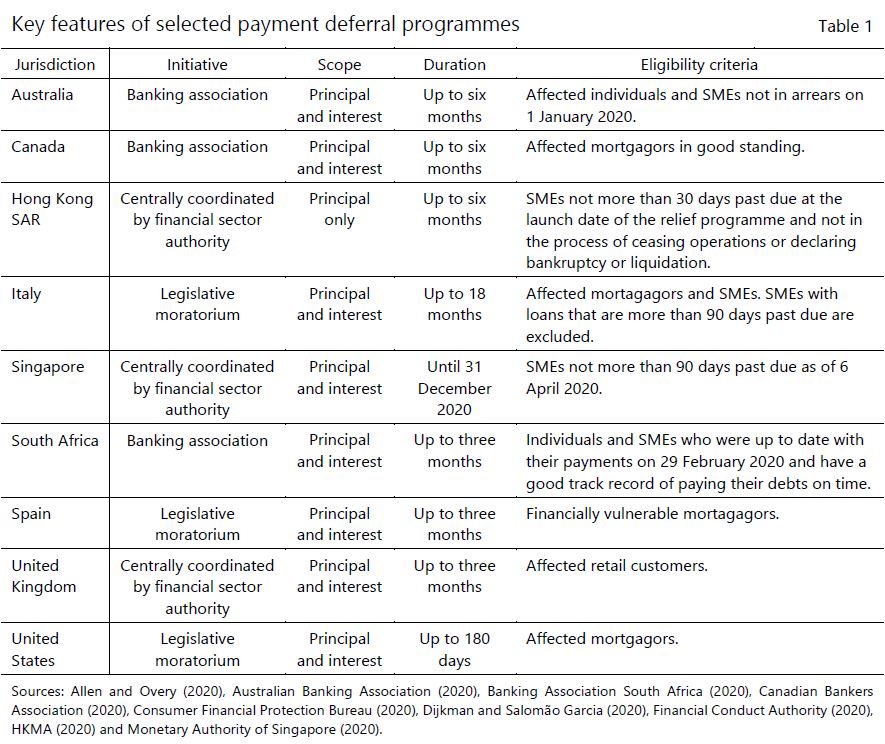

Rodrigo Coelho and Raihan Zamil of the BIS's Financial Stability Institute have cast an eye over the schemes in a report entitled; Payment holidays in the age of Covid: implications for loan valuations, market trust and financial stability.

"Payment deferrals increase future risks to both borrowers and banks, as the missed payments are not forgiven and must be repaid," Coelho and Zamil say.

"This can lead to a situation where the missed interest payments are added to the loan balance, resulting in a higher debt repayment burden for borrowers, once the payment holiday period ends. At the same time, IFRS 9 [International Financial Reporting Standard 9] allows banks to recognise interest income on these missed payments, raising prospective risks if borrowers are ultimately unable to repay."

"In addition, if the payment moratorium is lengthy, the deferred interest payments that are added to a borrower’s loan balance and the corresponding amount that are recognised in banks’ interest income accounts will increase, accentuating medium-term risks for borrowers and banks," say Coelho and Zamil.

"The extent to which these risks materialise, and how they affect the accounting classification and measurement of loans, depends on two factors: first, the borrowers’ ability to repay the debt once the deferral period ends; and, second, the availability of collateral support, including the existence of public guarantees that back the underlying exposures."

According to New Zealand Bankers' Association figures as of June 2, 63,486 customers had reduced loan repayments either by shifting to interest only, reduced principal and/or interest repayments on $20.2 billion of loans. A further 54,650 customers had deferred all loan repayments on loans worth $19.3 billion. That combined $39.5 billion is equivalent to 14% of the $280.759 billion worth of outstanding home loans as of the end of April, against the backdrop of rising unemployment.

Coelho and Zamil note that the financial stability implications of payment deferral programmes will be driven by the extent to which borrowers will be able and willing to repay their debt obligations once the payment holidays expire, especially in the absence of a public guarantee.

"The famous American investor, Warren Buffett, once said 'It’s only when the tide goes out that you learn who has been swimming naked.' The cumulative impact of Covid-19 and payment deferral programmes on bank balance sheets depends on many factors and will only become apparent over time. Therefore, the timely classification and measurement of credit risk is critical for banks to provide confidence to supervisors and their stakeholders on their financial health. Delaying loss recognition until the tide goes out may leave banks and supervisors with fewer options for dealing with the repercussions," say Coelho and Zamil.

The table below comes from Coelho and Zamil's report.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

12 Comments

"The famous American investor, Warren Buffett, once said 'It’s only when the tide goes out that you learn who has been swimming naked.'

How True !

If have to follow Warren Buffett - One has to wait and watch, for now.

Many who hate to accept that world not only NZ is entering into deep recession ...actually depression and with that obviously housing market will also suffer so the Best Advise for Now is Wait and Watch - This advise will be tortuoreous for them :)

He also said be fearful when others are greedy and greedy when others are fearful.

That has been translated by property speculators/landlords to mean that if people are fearful of a property bubble collapsing, that it is time to be even more greedy.

What’s the probability that mortgage deferrals will be extended once the 6 months expires?

Or that 30-year mortgage that you have, that had 25 years left to run when you went into Deferral?

"Let's reset it back to 30 years for you; or how about 35, to make the repayments doable?"

Sounds good - at 2.99%, but.....

Globally, some 40 year mortgage products have been issued ...

More enabling by the banks to use that same income and debt service ratio to lend more resulting in higher debt to income (& resulting in an ability to finance higher house prices)

i) $35,000 debt repayments @ 6.5% on 20 yr term means a mortgage size of 385,648

ii) $35,000 debt repayments @ 6.5% on 30 yr term means a mortgage size of 457,053 - 18% higher

iii) $35,000 debt repayments @ 6.5% on 40 yr term means a mortgage size of 495,093 - 8% higher

Going from 20 year term to 40 year term would result in mortgage sizes being larger by 28%.

Note: 6.5% used as this is the current stress rate.

Yes it's not surprising that there's going to be a huge amount of mortgage deferrals which will then result in mortgagees. You only need to take a look at how prices have been allowed to escalate where there's no economy to support them. Take NZ's Northland for example which is mostly dependent on tourism.

REA's are trying to sell properties there for 5 times their original 2013 RV with additional couple of 100k thrown on top for good measure! Crazy prices with much higher values then Auckland city!!

I am already seeing listing price reductions where I am, however its noteworthy that the original listing prices are well over what is reasonable. REAs are having a go and trying to uphold the boom time prices but its fairly transparent.

Yes I agree with you, I've also noticed that the very over priced Northland property is just sitting there and isn't selling. The reason why I'm interested is that we would like to move out of Auckland eventually and move to a quieter more rural area, but we wouldn't consider doing that if prices remain high outside of the city areas. It just doesn't make economic sense.

The banks are being squeezed at both ends - on top by the governments dictating their wishes that the peasants be spared in the short term, & its uptake from beneath, as the article spells out. This won't please the bank managers. In fact, when push comes to shove in 6 months time, I'm wondering how much kindness will still be on display? Kindness is a political trait, not a banking one.

This really is a no-schist-Sherlock article, innit? Extend-and-Pretend is shurely subject to them Limits to Growth....

"15% of business customers are under some form of relief at the moment"

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.