Ever since the Global Financial Crisis, the world has experienced low inflation. Despite periodic warnings of inflationary pressures, inflation rates globally have been tracking well below historic averages.

Central banks have deployed loose monetary policy and quantitative easing at an ever-increasing rate to try and inflate global markets and in some cases to avoid outright deflation, but these interventions have been increasingly ineffective.

There have been many theories for the persistently low inflation, from hidden labour market slack to globalisation, but one theory that is gaining increasing attention is the deflationary impact of new technology.

Technological advancements, from iPhones to Uber, are inherently deflationary as their whole purpose is to enable goods and services to be produced and distributed more efficiently and at a lower cost. Yet these powerful deflationary forces are not captured in official models. This is particularly important now as COVID-19 has increased the pace of digital disruption, enabling the rapid, widescale uptake of technology in many sectors from education to healthcare.

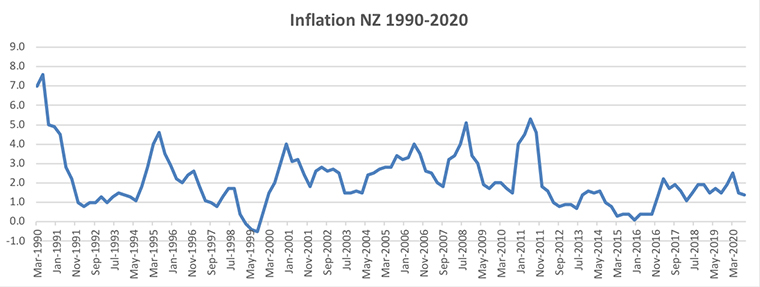

Inflation in NZ

According to the Reserve Bank’s inflation calculator, a basket of goods and services worth $1.00 in 1980 would have cost $3.54 twenty years later. By contrast, a basket worth $1.00 in the year 2000 only increased by 53 cents by 2020. There was a big drop in inflation when the Reserve Bank began inflation targeting. However, since the GFC, inflation has been easily contained below the “safe” 2 percent bound, despite low levels of unemployment and a tight labour market which are normally associated with higher prices.

From scarcity to abundance

Technology entrepreneur Jeff Booth recently published a book on the subject of technological deflation titled The Price of Tomorrow – why deflation is the key to an abundant future. In it, he argues that our economic models were not designed for a digital world, but rather for an environment where labour and capital were inseparable, where growth and inflation were a given, and where people created wealth by exploiting scarcity and inefficiencies.

Booth contends that because technological progress allows us to do more with less we are moving from an environment of scarcity to one of abundance.

Meanwhile, technological advancements like artificial intelligence will impact almost every part of the economy, driving down inflation to such an extent that ultimately it will be impossible for Central Banks to counteract the effects through monetary policy. He points out that we can already see this happening given in the last two decades it took $185 trillion of debt to produce just $46 trillion of GDP growth.

What is the solution? Booth argues the answer is to let deflationary forces take effect and to deal with the consequences now rather than facing worse consequences of unwinding an ever-increasing debt burden down the track.

Tsunami of debt

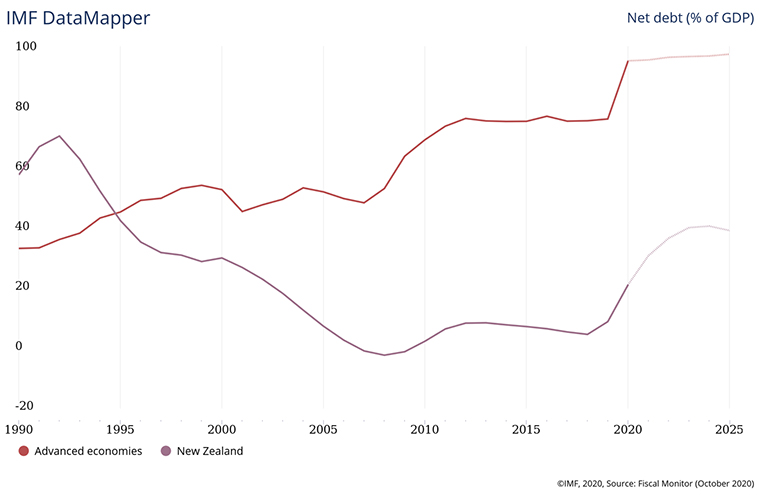

Global debt has grown to an eye-watering level over the last 20 years with the Institute of International Finance predicting total global debt would reach $277 trillion or three times global GDP by the end of 2020. In 2020 alone the level of debt increased by $15 trillion. The rate of global debt accumulation is so large the IFF has warned it will be difficult for the world to reduce the debt without adverse economic consequences.

In New Zealand the public debt burden is tipped to rise to 50% of GDP in 2024, a comparatively modest level compared to the advanced country average of close to 100% of GDP.

While the full impacts of a deflationary post-COVID world are not yet clear, such high levels of debt combined with prolonged deflation will make it much harder for the world’s economies to recover from the pandemic.

The costs of not addressing the ongoing impact of deflation may mean central banks and governments will be trapped into an endless cycle of inflating the market through monetary and fiscal stimulus.

What is clear is that the resulting ultra-low interest rates coupled with rising asset prices will only exacerbate the existing structural inequalities – and not to mention civil unrest – that are evident in many parts of the world today.

*Alison Brook is from the Knowledge Exchange Hub at the Massey University campus at Albany, Auckland. She is on the GDPLive team. This article is a post from the GDPLive blog, and is here with permission. The New Zealand GDPLive resource can also be accessed here.

26 Comments

Business strives to be more efficient and produce goods at a lower cost.

Our banksters want to see inflation i.e not price drops - they want us to pay more for stuff!

Get your head around that contradiction.

You forgot the third, possibly the most important part of the argument - consumers are chasing to buy more products and services at the lowest possible price; even if this comes at the cost of long-term socioeconomic degradation.

Haven't forgotten that nor limits to growth. But the contradiction of lowering costs via efficiency (eg the ability of a phone to be an office) leads to deflation as we can produce more at lower cost. But when we do this along comes Mr Orr with the directive to create inflation?

Surely this is absurd. How do they 'sell' this in economics school???

In a way yes. Every business I know in is looking at software or machinery projects to opt out or reduce the cost of employing humans. There is no upside in running a business just to pay your commercial landlord and your staffs over debt leveraged rent. One thing the lockdown has shown is that computer users can easily work remotely or from home. This will be seen in the next year as office leases are dropped or downsized as their renewals role around.

Less rent, less power, water bills, less time wasted in traffic, less commercial insurance. The list goes on. Commercial office landlords....

So everyone does away with staff, eh? Who do you sell to, in the end?

Welcome to the Limits to Growth.

Here, now, signalled since 2007 for anyone who can think from first principles, signalled from decades before to those who bothered to do their homework.

As they say, all bets are off. What was temporarily maintainable - growth - is now in the rearview mirror. All that was taught to economists, since WW2, is now varying degrees of irrelevant, through to completely wrong.

The 'costs' most avoided, were things called 'externalities'. Just one thing; physics, nature and ecology don't see them as external.......

Wages are slowly being eroded - so most people don't notice inflation in everyday goods...basically frogs in the pot.

The CPI is such a terrible measure of inflation. Everything anybody dreams of and works hard to obtain is getting more expensive at a rate much much higher than the CPI would ever suggest. Think housing, holidays, cars, education.

Jeff Booth's book is brilliant BTW. Thank you for referencing it.

Most people misunderstand what work is.

They don't 'work hard'. They endeavour to obtain a slice of the processed resources, supplied by real work (supplied by fossil energy). That slice is by tacit agreement, whether via bargaining or advertising or the social appreciation of the activity. But compared to fossil energy, labour is noise; too small to measure. And technology can only do efficiencies.

The best treatise overall (it's meaty at 800 pages, but worth every one) is this:

https://tel.archives-ouvertes.fr/tel-02499463/document

Alison could do worse than to peruse it.

I'm glad that they put off that that 'peak oil' thing for a couple of centuries.

Before committing ignorance to pen, think.

First of all, who is 'they'?

Secondly, how did 'they' 'put off', and what exactly, did 'they' put off?

Thirdly, where did you get the nonsense of á couple of centuries' from?

References please. Rigorous science-based ones too, if you don't mind. By which I mean, no economists allowed.

Try reading the first few posts here:

https://ourfiniteworld.com/

:)

PDK

***Patronizingly tells commentor to post only rigourous science-based references***

***In the very next line tells commentator to read from https://ourfiniteworld.com/***

PDK could give even politicians a lesson in hypocrisy.

The financial levers have been pumped so hard on a global scale since the GFC who's to say what the real value of anything is any more? This article does well to highlight the fact that technology is eating the world, and as a result of the follow on policy there are growing imbalances at every turn. Central bank governors are losing their mandate as fear and greed drive them towards increasingly perilous executive decisions. Technology will also disrupt them in due course, as people seek out markets and governance with real world indicators and hard constraints. Capitalism is not dead just yet, in spite of the best efforts of the neo-liberal establishment. On a long enough historical timeline the market always wins.

One of the RBNZ’s mandates is to maintain an inflation rate of about 2%pa and economists believe that QE ie printing money (increasing debt) will lead to inflation. But this is now no longer the case. Price inflation will only occur if the money is seeking goods that are scarce. Modern globalisation and technology means most consumer goods are no longer scarce. However shares and land are limited and consequently cheap money has driven prices higher. And the ridiculous situation we have is the RBNZ’s measure of inflation CPI doesn’t seem to reflect the inflation being experienced by the wage earner. Deflation of consumer product prices is overblown by the banks, they believe will delay purchases if prices are falling but we still need to eat and move every day. If the fridge breaks down it will need to be replaced quickly. The purchase of some larger items eg cars may be delayed but wont’t be put off indefinitely. So what is wrong with a little deflation?

Who is this woman? This is such an old story. I am looking at an article I wrote in early 2014 on why inflation would stay lower for longer and a key part of my argument was based on technological advances. I took a number of quotes from Brynjolfsson and McAfee's book, The Second Machine Age, Work, Progress and Prosperity In a Time of brilliant Technologies.

In countries such as the UK and US, inflation as conventionally measured has been decreasing for some 40 years, as can be seen in graphs from inflation.eu

Of course, this ignores asset price inflation. This was predicted by the American economist Hyman Minsky who saw that in the quest for monetary stability, financial instability will be created-precisely what we have now.

Well its a easy to follow narrative but until you question why it started with the GFC? Technology did not magically change when the crash occurred.

Here's an alternative lets start looking at Japan:

https://data.worldbank.org/indicator/FP.CPI.TOTL.ZG?locations=JP

who did not have to wait for the GFC to start struggling to get inflation. And then lets see if there is anything they were doing that rest of the world did not start doing until after the GFC.

More seriously, the evils of using monetary policy to drive interest rates unnaturally low for (any significant length of time) is a far better hypotheses for low inflation. It leads to distorted allocation of credit and therefore low productive growth, leading to low employment and thus low inflation.

Of course it's "hidden" labour market slack (credit Jeffrey Snider) leading to lower demand but why? Generally needing less people to produce the same amount has lead to each person consuming more (or purchasing higher complexity and more difficult to produce) until labour demand caught up. Maybe I'm out of touch but I don't think we have globally achieved enlightenment and stoped wanting more.

{kind=link}

"Booth contends that because technological progress allows us to do more with less we are moving from an environment of scarcity to one of abundance"

Yes - I can confirm this from the street

Its feels like everthing is getting cheaper (Like housing / food / rates / compliance..) while real wages can just buy more and more ... its hard getting rid of your wage these days

On top of that there appears to more resources everywhere I go; untapped plains, abundant fresh water and virgin land as far as the eye can see ...

Technological innovation and productivity improvement are great. Without them, most of us would still be working to death for mere subsistence, like in the Middle Ages. Lack of inflation is great, and cheaper goods means more affordable goods for everybody.

Rearguard Luddist arguments are sorely outdated and frankly ridiculous.

The issue is how to properly manage the "side-effects" of such rapid innovation, so to reduce the inevitable resulting disruption and inequalities..

Sorry, but we've had that discussion and should be moving on.

It was energy, lots of it, which raised our level of consumption (via raising our level of work do-able.

Technological improvements and productivity gains, are nothing but energy efficiencies. And those follow a law of diminishing returns as they run into Carnot and the Second Law (which unlike economic models, are immutable).

Sigh. It takes so long, doesn't it? Oh, and castigating an unwelcome message via naming (as per luddite or Malthusian etc) is a well-debunked approach. It's essentially shooting an unshootable message (truth/fact-wise) by denigrating the messenger. Spin 101 stuff. Let's take it up a notch, can we?

Time is short......

Life is too short for not following those countries with established Nuke energy power plant.

You dont appear to have noticed that wee Debt mountain we have built up ??

a headsup; its a PROMISE mountain

about how we promise the future will deliver ever more consumption and resources

Technology always disrupts established models. Big data is only starting on its road to monetization. AI is the enabling tech.

Maybe in the past technology advances still needed local labour components thus more of the gains where shared, now the gains all occur in a data center in a distant country. NZ is not even trying to tax these gains.

monetisation means 'I'm going to buy some processed parts of the planet with that'.

Which is where economics (as taught - which is somewhat of an oxymoron) and 'finance' and IT, miss the point. As do most who are parasitic on the energy/resources conveyor-belt.

Only PDK is the one who can see things clearly.

He was adorned this gift by the most righteous man; himself.

Technology brings efficiencies, in ways barely imagined before. The old political establishments are dreadfully inefficient, and massively over priced. But we never see the true costings of that. Few have even considered what this might be, A overall technological restructuring of Govt operations, personnel, and the methods where public participation becomes more routine is becoming an urgent priority.

We need to get back to some philosophy to give us guidance...

What give use meaning in this world? Were are we heading? Welcome to the Matrix unplugged!

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.