This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

Building more houses is not going to reduce house prices much (although it will help more people to be decently housed). The inflation driver is financial speculation based on leveraged borrowing. Until that is addressed, house prices will continue to boom.

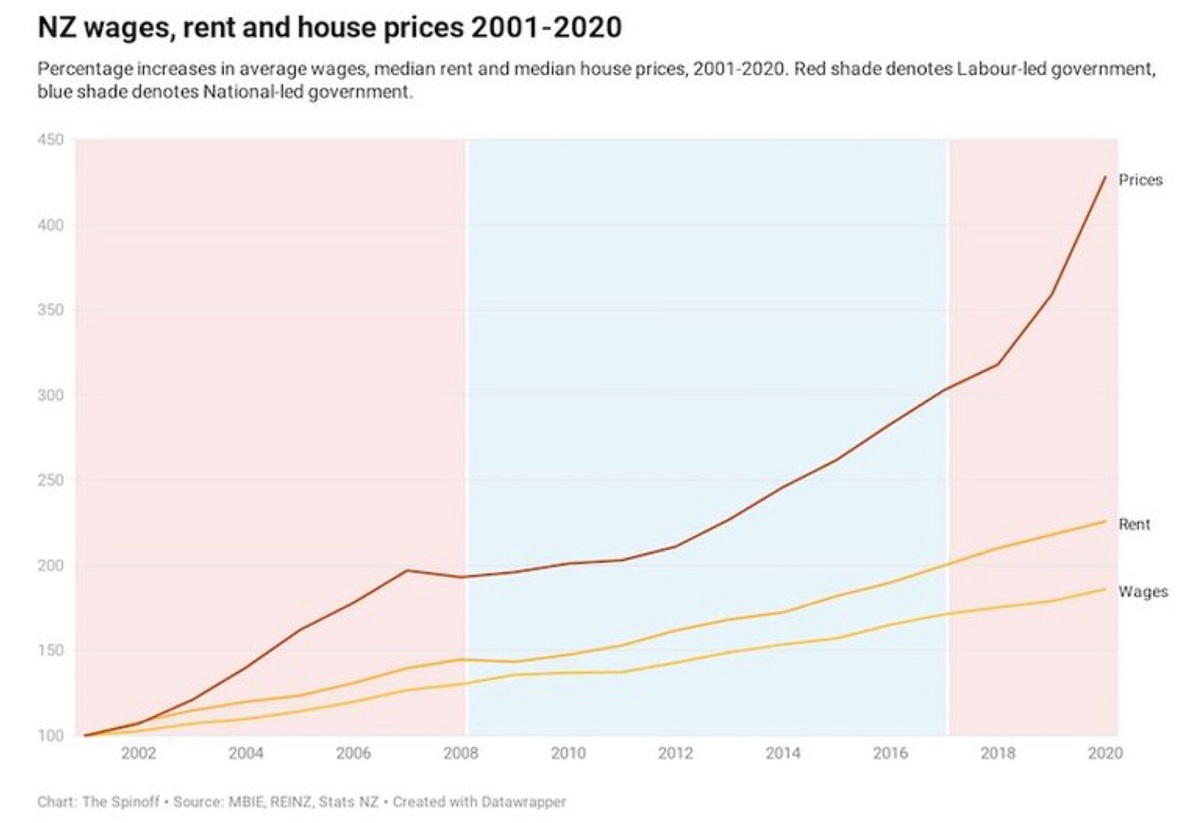

Policies based on theories which do not fit the facts are not going to work. Thus it is with most of the suggestions to control houses prices. The most salient fact about house price inflation is illustrated in the shown graph (below). (It comes from Duncan Grant published in Spinoff.) Since 2002, house prices have been rising substantially faster than rents and wages and consumer prices. There have been two bouts of very rapid house price inflation but there was stagnation from 2008 to 2012. (For a longer but not as up-to-date series.)

It is difficult to explain this graph by claiming we have not been building enough houses. We did not suddenly slow down house building in 2002, speed it up during the GFC and slow it down once the economy recovered from the global shock. (In fact construction fell after the GFC.) Certainly there is a housing shortage and we should be building more houses. But that will not have much effect on overall housing prices.

The faulty policy conclusion arises from a reliance on supply-side economics (which is part of the neoliberal framework). Of course one should pay attention to the supply-side of an economy (as we did in the previous paragraph) but we should not ignore the demand-side. Sometimes it dominates behaviour and has to be managed. Indeed, given that the disjunction between housing price trends and general price trends was evident by at least 2007 and attention solely to the supply-side has proved ineffective in repressing the prices for over a decade since, we might think to have learned.

Why have those prices been rising faster since 2002 compared to their past pattern? What changed then? There was an enormous injection of international liquidity following the Bush II tax cuts. That enabled New Zealanders to borrow more offshore, via their trading banks, greatly leveraging their housing equity. So the high house-price inflation is the result of a speculative spree financed by offshore borrowing. (It may not be coincidental that the housing price inflation seems to have accelerated following the Trump tax cuts.) Cheap interest rates have not helped.

When world liquidity closed down during the GFC, it became harder to borrow offshore, people became risk adverse and, not surprisingly, the speculative spree was retarded until the liquidity recovered in the mid-2010s.

Speculative booms are difficult to manage. They are not helped by tying one’s hands behind one’s back by ruling out a capital gains tax. That would both make the speculation less profitable and suck extra cash out of the speculative market, in effect reducing the amount of oil being poured on the flames.

Another approach is to reduce financial leveraging. That is what a loan-to-value ratio regime does. The difficulty is that borrowing is necessary for those purchasing a home for a first time. One way around this would be to have higher LVRs for such purchasing compared to the ratio for second home purchasers and those increasing their leveraging by upgrading their housing. While this might be difficult to administer nationally, the RBNZ is reintroducing a more tiered scheme and trading banks are tightening up their criteria for lending.

The neoliberal hands-off framework tends to argue that dealing with speculative booms is not a concern of a minimal government. While the social costs from speculating on a lottery, bitcoin or a game may be negligible, once there is borrowing lenders will be exposed too. It is not so much the speculative boom that is the problem but the speculative bust which follows, especially the pressure from those collaterally hurt for taxpayer bailouts. Government stabilising the boom before the bust is prudential.

The neoliberal pays little attention to the distributional consequences of a speculative boom. Leveraged speculation is only possible for those who have some wealth (or can convince the financial markets they have it – Trump?). So during the boom there is an increase in wealth inequality. Practically that means that those low in financial wealth – as most of the young are – are excluded and cannot buy their own homes.

In the bust, the increased inequality may not simply reverse. Certainly some high flyers do badly but often it is those with a modicum of wealth who suffer, while those who were arranging the lending go scot-free.

For example, a lot of people invested their surplus savings in finance companies before the 2008 GFC and lost their shirts when it turned out that the companies were into high-risk investments. But most of those who managed the poor quality investment continue to wear collars and ties.

In summary, the government which ignores a speculative boom does so at cost to it, or perhaps its successors, and certainly to the economy as a whole.

I’ve not written a lot about the policies to quell the speculative boom; the above are chiefly to illustrate the underlying mechanisms. For all the public hysteria, the government may not have many policies available to it either.

If a speculative boom has been under way for almost two decades it is not going to be easily suppressed (except by a disruptive bust). Have you noticed that some of the loudest critics (including the National Opposition) did little when they were in office? (Which is not to ignore lamentable performances by some Labour Ministers of Housing; that excludes Megan Woods.) You only have to look at the way that the housing portfolios have been mucked around with – National split the supply and demand parts of the housing sectors – to see a shambles.

If this is a pessimistic prospect for housing – and, because of the sector’s size and importance, for the whole economy – at least this column has tried to provide an analysis consistent with the historical facts. However, policy proposals for this complex problem will be dominated by answers that are clear, simple, and wrong.

Brian Easton, an independent scholar, is an economist, social statistician, public policy analyst and historian. He was the Listener economic columnist from 1978 to 2014. This is a re-post of an article originally published on pundit.co.nz. It is here with permission.

155 Comments

Excellent points.

We must immediately crash any type of speculative behavior liked to housing. BAN investment in housing as long as we need until prices reach affordable levels of 3-5 times the average household income.

Monitor regions individually and reintroduce ability to invest just once we can afford it as a country.

Which point of NZ history could every one have house in the past?Home rate was 20% + years ago and houser was much cheaper but not everyone could buy a house.

I presume by home rate you mean home ownership. If so how far back are you going to get 20%? around 1880? Home ownership rates have been constantly falling for at least the last 40 years mainly because of the scourge of property investors and mass immigration.

I'm as against property investors and mass immigration as the next person but you cannot simply blame them for dropping home ownership rates.

If all our mass immigration had been the highly skilled and therefore highly paid immigrants our govt talks about then they would all have built new homes. It is not mass immigration that causes decreasing home ownership it is low-paid immigration.

Similarly all investment is not bad. The young Chinese investor I met last year who is investing (risking) his $10m in converting two decrepit houses on adjacent sections into building town houses and apartments that are currently for sale is doing NZ and home buyers a favour. NZ should encourage and reward such investors.

Maybe the property investor you object to is me - bought the neighbouring property and have rented it out for the last 15 years. Cashflow it has been break even but our crazy govt has let that house triple in price. It we sell it the profit would exceed my wife's hard earned income for the same period.

You've hit the nail on the head Lapun. You're absolutely right.

I would add that the FHBs of today are just not tough enough and have missed an opportunity to do something constructive to advance their cause. With the wealth of social media available today, for instance, why did they not organize street protests over the last year or so? And I don't mean protests a la "Trump's mob" which amounted to insurrection. Street protests are a legitimate democratic process that achieved unbelievable successes in the 1960s and 1970's. I took part in a few of them. There is even a photograph of myself (easily identifiable), in a book called the "The Swinging sixties" by Graham Hutchins, protesting against the French Nuclear Tests in the Pacific.

Another possible reason why some young FHBs don't become more active in their protests could be that they really want to just join 'the club'. Inotherwords, they not only want their house to live in, but deep down they really want the investment properties as well.

So get off your comfortable couches FHBs, after you've arranged the protest on Facebook or similar, and take to the streets. You may then find yourselves taken more seriously.

I agree. I'm surprised that all those locked out of the housing market are not 'camping out' outside the Beehive and in a high profile area in Auck. They are like Labour - all talk and no action.

They should also be camping out in front of the RBNZ main office in Wellington.

Lapun.. agree with what you say. Guys like your Chinese investor friend are a big positive for NZ and we should welcome them. The problem is, as I see it, is that there are 10 or 20 of these low paid, low skilled economic migrants who are a massive net negative on our country for every immigrant that is a net positive. And more importantly, not being really selective in who we allow to live and work here means the numbers are such that it (immediately) contributes significantly to our high rents and also (with a lag of 5 or 6 years) to our devastating house price inflation. Of course there are other factors but mass immigration is one of the major ones.

I do not object to investors. They are just playing by the rules but IMO, the Govt needs to ensure property investment is not a viable and profitable business. It damages our people too much and this damage will grow exponentially. BTW: I also bought my neighbours house in Mt Roskill in about 2000 so I was one of those big bad investors too. But it has to stop or we will pay a massive social price, and the current situation is simply not right.

Hi Karl. I think the 20% he was referring to was the home loan interest rate.

The point being made is that if you refer to house price to income ratios without mentioning interest rates, its kind of a silly point. Back in the day when house prices were a lot lower compared to wages, interest rates were a lot higher so most of your payments went to paying the banks interest bill. Today most of your home payment goes to paying down your principal. Either way they still take 25 years or so to pay off ( often stretched to 30 years now )

The real kicker for young people now are the huge deposits they need to save up, not the price to income ratio as interest rates have balanced the majority of this out. Imagine trying to save a $200,000 deposit. Very Very difficult.

This is a complete misunderstanding of how the system works.

Up until the early 1990's, the median house price multiple was historically always approx. 3x income, in spite of whatever the interest rates of the day were.

Interest rates have very little effect on house prices if Govt. policies allow supply to keep pace with demand. As does the rate of immigration etc. NZ policies used to allow this up until the 1990s but since then, the introduction and subversion of the RMA, and the compact city ideology that restricts growth as meant supply has always lagged behind demand, almost irrespective of what the demand is.

There are other jurisdictions that have just as high immigration and as low-interest rates but have policies that allow supply to equal demand, and their house prices are 3x median multiple. There is no reason why you cannot have 3x median multiple and low-interest rates, just like other jurisdictions do.

What people miss, is that when supply can almost equally demand in real-time, then the supply and demand cycles are in syn, they are predictable and you can plan the supply of materials and labour to meet that demand. Developers are only trying to build to no more than equal demand because if they oversupply then prices could drop and they lose money. If they are going err on the side of caution then it is best to undersupply, and if the rules allow you to engineer this, all the better, because it allows you to have a defacto shortage, and thus you can charge more. This extra is as non-value added costs from a purchaser perspective, ie you may more in price, but get no more in amenity.

This does not mean that amount of demand is not important, it just means, whatever amount of demand we have, then our supply policies should allow us to meet that in a consistent and at the rate of demand.

Jamin... Thought he may have been referring to interest rates. Agree with your post totally. Getting the deposit is the problem especially when for many, rent is taking about 40% of their income. And it is basic common sense that as the number of people who need somewhere to live grows massively (mainly through immigration) every year the cost of rent will also grow with it.

Saving 200K deposit while paying 600 PW rent. Good luck with that. You can see why so many just use any spare cash to buy drugs and whisky to forget about reality. I would probably do the same in their position.

Around 1990 ~74% of households owned their home. This has dropped to ~65% now, with no sign of the trend changing. Are you happy with the direction of travel?

https://www.stats.govt.nz/news/homeownership-rate-lowest-in-almost-70-y…

Some of this may be explained by recent immigrants not yet being in a position to purchase a home.

It would be interesting to see the trend of NZ-born home ownership to get the full picture.

Under 60% since the turn of the century??

Of course not, but many more could afford a house years ago than can now. This is the real problem, as time goes by we are making things worse, not better, yet banks keep making the same or higher profit but on a longer period of time.

Well put.

The only emphasis needed is that lefty unadressed, the problem isn't going to get better with time. I will get worse.

this is a great article that explains the ongoing problem with speculative bubbles - which is the "tulip effect" as the bubble gains popularity - the middle class and those least able to afford the bust - that will inevitably come - jump feet first into the speculation hoping for a way to get rich quickly, the problem is this is when the savvy buyers either get out or hunker down leaving the newcomers to ride out the subsequent bust. We have seen this time after time - the 1987 share crash, the housing bubble in the US that preceeded the GFC - those who thought they were going to get rich actually ended up poorer.

Now here's where this housing bubble gets "potentially nasty". Speculators who have used "equity" in their main residence to buy other properties in the bust run the risk of not just losing their investment property but also their main residence - especially if the bank is forced to sell the investment property and cant recoup 100% of the mortgage then they will sell the property used as "equity" to recoup the loan. The bank NEVER loses.

The media and the financial advisors never talk about this issue when the boom is on - which is a shame because far too many people wade into these situations with their eyes closed. When a bank is saying they want 40% equity - they are really saying we think the market is well overvalued (potentially up to 40% overvalued) and we will protect the banks interests- not the borrowers to make sure we dont lose out. Investors worrying about gathering enough equity to buy into the market in these circumstances are thinking about the wrong thing.

You are right and it's investors who've hung onto properties for years that are selling off at this point

dago

What is the source of information for making your assertion?

Its contrary to information what I am hearing.

I was told of an informal survey at a Property Investor Association meeting that this was not the case - many investors see increase in yields with increasing rents, upside for capital gains, and no low risk alternative as to where to place their money. .

It was indicated that investors were looking to buy rather than sell and this is borne out by Tony Alexander's January survey of REA which comments 31/% more of REA are noting investors looking to buy (albeit it down from the November high).

Of course the Property investor association would say this - its in their interest for people to keep buying property, the same goes for mortgage brokers and financial advisors. In fact a number of "quality advisors" are recommending that their clients sell off "defective" or low quality stock whilst the boom is on, a boom is a quick way to make a buck on what is typically unsaleable property - especially if you can sell to a first home buyer or naive investor who is in the FOMO stages.

Keep in mind the property industry and even Goldman Sachs were promoting getting into property in the US in Aug 2008 - just before the toxic loans all fell apart and people were still buying heavily into the sharemarket in Sept 1987.

ikimpaul

This is not Property Investors Association saying this - is is property investor at a meeting in an usual open discussion discussing amongst themselves the state of the market and how they feel about it. As is usual meetings informal show of hands are shown on a number of aspects - it is attendees only and is not reported.

So this is investors for their information only with no vested interest in keeping people buying properties as you incorrectly assert.

As I said, there is every reason for them to hold their properties as was discussed - increasing yields on purchase price as rents increase, upside to prices, and lack of alternatives for investment . . . . and that's logical and not rocket science as to why most are staying with their properties.

I am the source, it is has been my observation along with my husband, as we have looked into the history of 100s of houses for sale in Wellington over the last 9 months. Tightly held properties are being let go. That's not to say investors aren't buying them

"That's not to say investors aren't buying them"

RBNZ data supports that - mortgages to investors (whatever one thinks) is 1.5X that to FHB for all of last year (about 17.5% vs FHB at11%).

This has been the continuing trend since RBNZ first published mortgage data in 2014 and is consistent with Stats NZ data showing increasing number of houses being rented and homeownership declining.

It is a concern that over the past thirty years that home ownership rates for 25 to 35 year-olds have declined from 65% to 35% (NZ Stats) and that is getting increasingly worse - not better.

It is a concern that investors are accumulating properties not divesting them . . and your comments suggest otherwise.

Just because you have some casual observations of investors selling that may be at normal levels (I got out of investment property in 2016) so it is unsound of you to jump to a conclusion that long term investors are selling out - the available data and logic doesn't support that.

30 year old's, often with children, being unable to purchase a first home is a crime. It will lead to a breakdown of our social fabric. It possibly already has .

Someone think of the transexuals!

Rosenstein... are you missing that annual "golf trip to Thailand"?

I was once a 30 year old, with children, without my own home. It wasn't a problem.

Why should that lead to a breakdown of our social fabric?

My observation is that a number of FHB are _also_ investors. A number of them will buy for themselves but others used as a proxy for foreign investments. This will be a means of circumventing the 40% LVR restrictions.

The fundamentals of housing is quite different to a ponzi like tulips as it an essential service that pays the owner rent. It doesn't matter what you purchase for, as long as you are paying the mortgage (interest only) you dawn ride out any storm..

Long may the property party continue!

The DGMs hate to see it!

we do indeed

because it confirms we are seriously in the S##t

B727,,, would you like to also see a heroin epidemic destroy the whole fabric of NZ society?

House price inflation is the equivalent of raiding the Balance sheet to give your business some income...

Like running a bar where you are letting the punters put another round of drinks on the tab because they dont have enough income... (its just temporary right)

But your bar turnover is doing GREAT guns...

Long may the property party continue!

The DGMs hate to see it!

Will give you benefit of the doubt and suggest your comment is just trolling. But it is stupid. When property bubbles burst, they affect everyone. They do no discriminate, whether you played the game or not. They should be avoided, not celebrated. My feeling is that this bubble is as bad as any seen in recent history and potentially as catastrophic as the Japanese bubble. For most people's sake, it would be good if I'm wrong.

We're either in a bubble to dwarf all bubbles -- bigger than 1929 -- or this time *really is different* for some reason, maybe the nature of our tech or globalisation. If history is any guide, we're in the crapper... but it's true that the future doesn't always look like the past.

but it's true that the future doesn't always look like the past.

This is true. What we're going through is unprecedented. Notice how many of the armchair warriors are now all experts on money printing and how the suburban bolt-hole is the refuge from all the financial chicanery. Something doesn't add up.

.. but it always rhymes.

"Have you noticed that some of the loudest critics (including the National Opposition) did little when they were in office?"

Which is logical

Its an illusion that Policies can now deliver good times for all

The surplus simply isnt there and we are way in Ponzi territory

More financial leverage is all we have

So its talk and point and talk and point & tinkering around meaningless sidelines

It also assumes that governments are able to do things. There are two things which governments can do badly: do nothing and do something. They don't act when they should and when they do act they do things for the purpose of being seen to do something. What we need is a transformational government that does what is required.

The Govt must be relieved to have the Covid outbreak to deflect from the housing crisis as they can only handle one problem at a time.

'Economist Brian Easton says building more houses will not reduce house prices by much; house prices will boom until speculation based on leveraged borrowing is addressed'

HOW TRUE.

New houses built are more expensive so price will mot fall and old house as are being chased by developers price will not fall instead will multiply and is multiplying.

Government and many so called experts Shout about supply is only to hide behind the excuse as do not want any action to be taken on speculators and surely Mr Orr and our dear PM is intilligent enough to know and doing as have no intend to control the ponzi.

Why would anyone do any business when can earn in millions bu speculating in housing market and that too tax free by hiring a good accountant.

So true, anyone who's been following property knows exactly what caused the sudden post covid spike, and it was not some sudden dip in supply or increase in population, even though those factors have laid the groundwork it did not cause the super-heated spike of 120k in 9 months. Sudden supply-promises are deflection, excuses for lack of action. RMA reform is going to take 2 years anyway. By then a bungalow in Wainuiomata will be wort 1.5million and half the country will be driving around in Teslas and Mercs while the other half raid the couch for coins. Grant Robertson who is merrily dragging this out, is being overtaken by impatient snails as he dithers and makes announcments about announcements, it's beyond a joke now

The only reason behind the increased supply strategy is the number of jobs and economic activity this generates, which will in the short term compensate for the impact of COVID. This Government by doing this is basically pushing an even larger problem down the track since basing a country's economy on a construction bubble has never ended up good either.

What is worrying , is that a 35 -40 percent fall in house prices, a number on the periphery of bank testing, and seemingly an outrageous number, would only take the country back to price levels ( especially New Zealand ex Auckland) last seen in 2017, just 4 years ago.

Clearly stress testing should be on a dynamic rather than fixed basis. As Ireland proved you really can have a crash exceeding 50% of housing value if your run-up is long enough and there is a supply/demand imbalance.

This is why banks now require 30-40% deposit. In a scenario of 30-40% house price fall, guess who looses their deposit...not the banks.

Banks - the biggest gang in NZ

If we had productivity growth (as measured by GDP per hour worked or per capita) we probably wouldn't be having this conversation. An asset price bubble has replace our productive economy.

Everyone blamed National but is Labour any different. Supported by Mr Orr.

In practical terms I think many of us are struggling to see any differences at this point. It's difficult for Labour or National to find any political space to maneuver. Prime Minister Ardern has the edge over Judith Collins when it comes to that slick sell however but I can't see anyone in the National Party with that same Teflon touch and policy-wise they've been stuck in neutral since John Keys second government.

Is any party remotely credible on this besides TOP?

Labour is the new National.

What are the odds of a Labour/National coalition some time this decade? Got to be better than 20 to1?

Simple fix: DTI.

DTI for investors ONLY ie not applicable to owner occupier FHB's. We need to bomb investors, Air B n Bs land bankers and owners of unoccupied homes out of the market with every bit of firepower we have. Houses will not just disappear off the face of the earth if we take measures to ensure these investments are not commercially viable.

Translation: tax and punish the others, just not me, please make them suffer but spare meee, thanks

A targeted DTI does not tax or punish anyone, it just takes the punch bowl away from investors. There would still be a whole world of investments out there available to anyone, just not ones that lock people out of buying their own homes.

Being denied a particular avenue of investment, of the many available, does not meet my threshold for 'suffering'.

Particularly when we have tens of thousands of people living in vans, tents, motels and garages.

Yvil... no, tax and punish actions that are seriously harming NZ as a whole. My very elderly parents are landlords so indirectly I am lobbying to pay more tax. Why? Because it is the right thing to do for our country. There is a decent chance I will own rentals again at some stage in the future. It is not about me or you for that matter. It is about what is right for NZ especially for our marginalized people who need things to change.

My anecdotal experiences of watching other people buy houses is that people will always borrow close to the upper limit of what they are able to. Having more houses available for buying will result in prices being lowered only slightly as you are shifting a point in the middle of a bell curve of income and credit availability.

Its slightly more complicated for FHBs as they only save enough to meet deposit requirements for an entry level house but then again this willingness and ability to save can also be modelled on a bell curve.

This is speculative behaviour driven by the belief or truism of most market participants that prices that prices will only go higher. Until this belief is broken we will see this behaviour and the only way to stop this is restricting borrowing. There are plenty of other instances of government stepping in to stop people engaging in destructive behaviour towards themselves and others.

The thing is, the Government knows this, it is blatantly obvious - house price growth is directly related to cost of credit. What the Government is excited about, is the economic potential energy it can channel. They see house bubble hysteria as a good thing, that's why they are headstrong on addressing it with:

'The housing crisis'

'We must build more houses'

'Remodel the RMA'

'First home buyer grants for new builds'

'Kiwibuild'

'Free up more land'

etc etc etc.

...anything to drive job creation and the knock on effect.

That's it in a nutshell.

I don't think it's *just* the cost of credit, although I agree that is a very important factor. See my comment below. Credit wasn't cheap from 2001 to 2006.

There are a range of demand side factors.

It’s also about the availability (supply) of credit. Since the mid 80’s, deregulation has allowed banks to expand credit - particularly mortgage credit- pretty much unchecked, apart from their assessment of borrowers ability to pay. More recently, the reserve bank has imposed deposit limits on mortgage lending. The RB could also (but chooses not to) provide guidance on bank lending eg it could encourage lending on economically productive activities rather than speculative lending on housing. Richard Warner in his book and video “ Princes of the Yen” discusses this in regard to postwar Japan.

Correct.

Which makes the child povery virtue pantomime by princess tooth tooth that much more repulsive.

It is abusive for her to continue this pretence at empathy, when at best her actions display rather limited sympathy, at worst only pity. There is a huge difference. It is very important to understand and be able to distinguish between them. But we don't really bother to teach this in our society. We don't take mental health seriously. Many people don't learn about setting healthy boundaries and recognizing abusive relationships until much later in life, if ever. It is hardly surprising that Ardern is easily able to fool the general public, and could quite likely see yet another term, despite continuing to ignore the incredible and urgent need to act with genuine compassion here.

Edit: spelling.

Good point.

Also try dealing with Megan Woods, who is in charge of housing. Very condescending, and close minded.

Absolutely. The opposite of what we need. A great reminder that genuine change that benefits the most in need, almost always comes from the bottom up, not the top down. I would love to be surprised come the end of this month, but I have zero hope for that.

Fake little B isn't she. Glad I didn't vote for that

Excellent article.

I don't know if there is any research on this, but I suspect the high levels of immigration post 9/11, especially from the UĶ, were a very significant factor in the post 2001 boom. That was a significant 'demand shock'. It wasn't just English people, it was also a lot of mid to high income kiwis bringing pounds back with them (then, of course, one British pound equaled $3)

The hand over of HK in 1997 and the destruction of a functioning SA in the 1990s probably didn't help. It is ironic that many Brits who fled to NZ around 2000 came here partly to escape the toxic effects of mass immigration in their own country. And now they are seeing their adopted country making the same huge mistake.

True. I came from the UK in 2003 and couldn't buy fast enough. I can clearly remember total disbelief that as a foreigner without residency (it was applied for) that I was permitted to buy. I had the profit from a small house in London that had tripled in price in 12 years. If I'd arrived two years earlier it would have been financial property buying bliss. I was lucky enough that my only Kiwi friend in those days was a relative of a builder so I bought an old proper kiwi house; I did read about a wealthier UK family who arrived at the same time and bought a leaky home - not a happy story..

Thanks for the anecdote. I think this was huge. I know a large pool of kiwis who returned from the UK in that 01-04 period, I reckon it had a huge 'demand shock' effect.

There is clear evidence that it is not just demand influences like cheap credit and immigration. Supply does affect house prices and rents. The evidence is quite clear when the different towns and cities in NZ are compared.

For instance. Infometrics economist Brad Olsen says it proves what we’ve known all along. “Those areas that have a higher proportion of their housing stock built in the last 10 years, more houses coming through, has seen prices not rise at the same clip as elsewhere,”

https://www.tvnz.co.nz/one-news/new-zealand/exclusive-data-proves-lack-…

Of course supply matters. It's just that much of the rhetoric and proposed policy responses focus on the supply side and not the demand side.

I am glad you agree supply is important Fritz because this supposed economist is saying it doesn't matter much at all - which is not what everyone else is saying - that it is both supply and demand factors - no silver bullet - a range of demand and supply solutions is required.... This article is based on a Duncan Garner TV3 graph of national house prices FFS. Brian clearly has not considered that house prices might not be set nationally - there is no national or international trade in houses - houses are different to milk powder. A huge factor is the specific spatial economics of each town and city. I doubt Brian has read any of specialists on the topic - Bertaud, Glaeser, Moretti etc.

Think about my points re: the period 2001-2004. It was a massive demand shock, and even if we had had much more elastic supply I think it still would have struggled to respond.

However, the fact was that housing elasticity was awful at that time. If you think district plans are bad now, think again! They were so restrictive in those days.

That's why prices boomed in the early 2000s, not because of cheap credit (it wasn't of course cheap). Demand was stoked by hot money coming in from overseas, and with an immigrant profile that was more skilled and wealthier than what we have seen in the last 10 years. And our planning system was not geared up to respond.

And the Labour government was pretty average at building state housing.

I agree with your early 2000s immigration demand shock thesis Fritz. That tally's with my experience too. The Clark/Cullen government were hopeless with housing. Clark remove market rents on state houses which was good but she seemed to think that was enough housing reforms for her administration.

you and Fritz sound like two "true-blue" property journeymen chanting hackneyed tunes

Hahahahaha :)

Nothing could be further from the truth.

"re: the period 2001-2004."

There was a of lot jumbo sized 5 bed 3 bath mono-clad homes in those days with one house to a 600sqm section.

Would have consumed a disproportionate amount of contractor time for the eventual 3 or 4 occupants

Now many are being reclad or replaced and eating up more resources

I think the Nats focused too much on supply, at the expense of demand side considerations.

And Nationals narrative is even narrower than supply. Supply for them is all about planning restrictions. National never talk about the lack of supply of housing related infrastructure or the low rate of public housing building compared to the per capita rate of the 1930s to 1970s.

Speculators know these supply restrictions exist, they know new builds are not coming fast enough to undercut there business model so they are quick to respond to demand shocks with leverage buying.

Auckland will be the interesting market to watch though. Its build rate per 1000 residents is ramping up. It hasn't reached the point it did in Christchurch post earthquakes which did halt price and rent rises. But it is tracking in that direction.

Yes, exactly, but then we have to look behind the data on the build rate per 1,000, eg are they mainly apartments that are not as popular post-Covid, and if they are just more at a dearer price, then that is not the same as more at a cheaper price, etc.

Secondly, as we have discussed, the whole council rates issue needs to be addressed. The reality is they haven't been charging existing homeowners enough, and many have actually needed new subdivisions to come online to cover the upgrade costs of older subdivisions regardless of any new connections. if costs were apportioned properly, many inner-city residents in older subdivisions would have their rates double.

Good points about rates. But 'keeping rates low' has been the mantra of local body politicians forever.

Unfortunately it catches up with you big time, and that's what we are seeing in Auckland.

Profligate council spending doesn't help, either.

But I think rates has been a bigger issue.

Those ratepayers who have demanded that rates should not increase much should not whinge about Auckland's traffic, beach water quality etc.

There is a choice to be made between price (and capital gains), and operating costs (and yield). The norm. is if one is high, the other is low. NZ has chosen capital gains over yield.

In Texas, it is the other way around. Houses are 3x income, and yield as a % is higher (although rent is still cheaper than NZ) which can also cover slightly higher rates (to cover true operating costs). But it's an easy calculation to see which is better. Imagine NZ house prices at 3x income and rates 50% higher.

At the moment we are paying 6x plus income and NOW councils are looking to put rates up 50% plus, the worst combo of all. An alternative would be to see what rates should have been paid to date as a deferment which on selling the property could be paid back out of all the extra capital gains made ie stamp duty/sales tax.

Brendon... of course it is both supply AND demand but in almost all discussion on the housing issue immigration settings are not even mentioned and if they are it is a brief notation at best. I am not sure I have ever read or heard an in-depth commentary. interview or debate about the implications of immigration on our rent and house price crisis. Pre-election campaigns, debates and interviews were the perfect example. And I have not heard the PM (or any of her ministers for that matter) even mention immigration (in relation to housing and rents) once since she was elected. Also there have been numerous opportunities during interviews for media (John Campbell, Duncan Garner etc) to go deep on it but they haven't even raised it at all. Why not? Are they scared of being cancelled, are gutless, have vested interests. are ordered not to or all of the above? Frustrating.

Bernard Hickey is good on immigration. Yes politicians should be honest that if they let the population rise by 1/2 a million people a decade then they have a responsibility to help local government provide the infrastructure and housing for those people. Instead what we have seen is prime ministers and finance ministers being very silent on their infrastructure obligations while taking credit for the improvement in the government books because immigrants bring increased GST, PAYE etc.

https://thekaka.substack.com/p/three-lonely-and-large-elephants

One of the reasons I like the independent housing commissioner idea is that it would force politicians to be honest. If population was rising rapidly due to immigration - making housing affordability targets unattainable without large infrastructure spending - the housing commissioner would say so publicly.

Bizarre isn't it Karl. I suspect it's a mix of vested interest and concerns around perceived xenophobia.

I think probably a lot of pollies and media know that immigration has a big impact. I really do feel that despite their words, they don't actually give a shit about housing, and in fact want the party to continue...

I think politicians get trapped by believing the best political move is to make no explicit promises. That being free from accountability is a clever political move. 99% of politicians do not make their implicit obligations explicit. Such as, if they make the decision allowing lots of people to come into the country then they have an implicit obligation for ensuring the system copes with that demand pressure. Or if they provide a massive stimulus to the economy then they have an obligation for ensuring everyone benefits from that stimulus.

The problem of not making promises - is it means clear expectations can not be set. For instance the government could say they will keep building public housing at an increasing rate until even the lowest decile groups are paying no more than 30% of their income on rent. If the public believed them because the statements were accompanied with genuine actions this would stabalise price and rent expectations.

But because clear expectation are not set, then a demand shock - such as lowering interest rates and removing LVRs spirals into a ponzi demand effect. House prices rise - FHB fear they will miss out - they believe they must buy before prices rise even further. Property investors greedy capital gains expectations rise even further, they buy property based on that expectations, and so on. The public do not trust silent politicians which means price expectations continue to spiral upwards. Can kicking, finger-pointing, blame-shifting by the various housing institutions is seen as evidence that politicians will not act on their implicit obligations (even if some efforts are made - the public do see the evidence - so do not trust them).

In summary because politicians so carefully avoid accountability they trap themselves in a situation that they cannot control.

Nailed it....and they wont change for fear that the capital flows will be reversed and the consequences of such....a rock and a hard place.

The only painless solution was to nip it in the bud and its now in full bloom.

Exactly. Now it is in full bloom, they simply don't know what to do with it. If they do nothing, it will keep growing worse (at a faster rate), but if they nip it now, it will hurt. Sometimes a little pain is good.

Good article. At start of Covid-19 lockdown 2020, there was only a mere forecast of a property slide. Yet, action to forestall the perceived risk was immediate. Removal of LVR's, loan moratorium, slashing of mortgage interest rate by flooding the system with cheap money. Throwing flame accelerant to ignite the housing market!!! . They sure went in "hard & fast". That oft repeated ( & now stale) sloganeering by PM on the Covid-19 crisis. But, now that the housing market is actually ( nor perceived) ablaze, what happens???? Go in ""soft & easy"????Announcement about pending announcement, tossing the ball back & forth between RBNZ & Min of Finance, kick the can further down the road !!!! Welcome to the la la world.

Nope they are not going in at all to try and sort the problem. The issue is that increasing house prices is psychologically seen as a "Good Thing" because it has a knock on wealth effect and people spend money to keep the economy going. This is all really a last ditch effort, throw the kitchen sink attempt to keep "Everything moving"

How to discourage the use of unrealised capital gains (i.e., leveraging) in the housing market?

Tax the gains at the time of drawdown as opposed to at the time of sale.

Or just tax the value of the capital, with an LVT or imputed rent.

Have been saying this for a long time. House prices are all about the availability to credit. If you already own, you can simply leverage up when interest rates drop. Which is what happens, so new supply gets owned by existing owners and the price of entry means FHB's compete against those already in the game.

If we built a hundred thousand houses tomorrow, prices wouldn't go down because asset owners would simply leverage themselves up a bit more to buy them all. And why wouldn't you when it's the only way to get easy returns on your money?

Re "If we built a hundred thousand houses tomorrow, prices wouldn't go down because asset owners would simply leverage themselves up a bit more to buy them all." Blobbles the evidence about the effect of supply refutes this.

Landlords are not going to buy a house when there is a superabundant number of new houses coming on the market. They will be concerned they will not find tenants. With a superabundance of supply the housing market becomes a buyers market.

Brendon, if that were accurate we'd never see bubbles.

But the bubble happens because investors go on recent price action. They *will* continue to buy with a superabundance of new supply on the market, so long as they're seeing profits made on similar investments in the recent past. Investors can sell to other investors. So long as there's credit available, the party can go on for quite a while before anyone realises that there is no real shortage.

Christchurch's house and rent prices stopped rising when the build rate per 1000 residents hit about 13. Overseas some cities have not experienced property bubbles because their supply response was strong enough to counter local and global demand shocks. This is the nonsense of Brian Easton thesis. He says the demand shock was some global liquidity event in the early 2000s that I have never heard any other economist mention as being significant. But for the sake of examining Brian's thesis if we accept that is true - then being a global liquidity event - it should have affected all the cities and all the houses that are connected to global finance - equally - but it didn't. Clearly proving there are other factors involved and Brian's property bubble thesis is not the whole story.

As I have said before, I think we need to be cautious comparing with the Houston's of the world.

Auckland or NZ's population growth and housing demand profile can be quite volatile, much more so than Houston which although has experienced strong growth it has been of a more predictable and less volatile type.

When it's more volatile and boom/bust like Auckland it makes it trickier. That is, we are more prone to 'demand shocks' than Houston, which simply has consistently strong demand.

I could accept that. NZ is a small ship easily blown around by big demanding seas. But we need to get better at responding to demand shocks. I am from Christchurch - it is not a model-city and it took quite a few years to respond housing-wise to the earthquakes - but it eventually did. We need to get better at that. Then expectations will alter so that capital gains speculation and FOMO is not so dominant. In my opinion getting better would involve a big public housing programme, active land management, infrastructure financing and a more permissive planning regime. I also think there should be clearer direction given from a housing commissioner.

NO, NO, NO. Immigration is strong and variable in Houston and Texas, but supply can match whatever the demand is so it is predictable, and thus can be planned more easily.

The reason Auckland is more volatile and boom/bust is that the system does not allow supply to meet demand, NO matter what that demand is. This is how you develop if you want to extract as much money from a buyer as the buyer can bear. If we had the same land policies as Texas, we would have the same median income multiple, just like we used to.

The key component of this is what price you can buy the fringe land for, ie at about its rural price. This not only means your input cost is less, but so is your holding cost, ie if demand says don't develop, then you can leave it undeveloped and make a holding income of its rural value. In NZ because of the rentier price you paid for it, then holding costs are huge, and force many developers to continue to develop their original number of sections/houses even if the market has changed.

Edited- I have done some research and although growth rates in Houston haven't been quite as volatile as Auckland, they haven't been far off.

Except they havnt stopped rising in Christchurch despite the fact there is an oversupply of built houses.....drive around sometime and see how many are unoccupied. The supply issue is overstated, the problem is the price (and inflation) that restricts access to the market but fuels bank profits and all underwritten by the state.

And why would all cities be affected?....the money flows to where its able and safest and captures return....not all cities meet those requirements but theres a few prime candidates that certainly do and they are targeted.

So the cheap credit pushes up prices in cities where it gets the most return. Would that be in places that have population growth and other demand growth factors yet have unreasonable restrictions on building and have infrastructure bottle-necks?

Not necessarily "most" return but certainly ease of access...it would be interesting to compare where the biggest bubbles are with 'ease of doing business' tables....i.e. you dont want to park your wealth somewhere where if needed it was difficult to get out....and NZ, Australia, Canada all fit that bill with Govs committed to open capital flows ...and their markets are small enough to influence but stable enough not to easily collapse.

Yes, they will. Why? Because if prices tomorrow are guaranteed by governments and their monetary policy arms to be higher than today, then they buy up large.

For almost a year we have been building almost as many houses as we ever had. At the same time we have had negative immigration. So when you say "Blobbles the evidence about the effect of supply refutes this.", recent history proves you wrong. I assume you are referring to Christchurch with your evidence, however this was a lot more complex than simply an increase to supply of housing - the earthquake has had many social and economic consequences over many years in Christchurch, which are slowly being sorted out. That has made Christchurch an undesireable place to settle for immigrants (I know of 2 who moved there for cheap housing, but have since moved back to Auckland and another is about to go to Wellington... both in IT, both talk about how Christchurch is a bit of a mess). As those issue are being sorted out, guess what house prices are doing...

In a competitively, functioning market, yes you are correct. But we DO NOT have that, in fact we are miles from it thanks to central banks and compliant governments. And there is no end in sight for all those distortions and the "prices are guaranteed to be higher in the future" truism that this supports.

So monetary policy is guaranteeing houses prices now. That will be news to RBNZ because house prices is not in their legislative remit. Here is a question for you Blobbles. If existing houses are leveraged up in price what is stopping FHB and build-to-rent property investors using cheap credit to fund affordable new builds? Couldn't they get affordable housing that way?

It is not in the RBNZ remit correct and you will note that they do not want it in their remit. If you read between the lines, they don't want it in their remit as it will create competing priorities. Basically they cannot do x and not cause y, they know it, we know it, they don't want to admit it, but will by deny GRs request.

The thing that is stopping FHB's from entering the market with affordable housing is that banks won't lend to them (they don't have collateral) to build the places they want at the price they can afford. Banks aren't really interested in low cost housing which may not increase in price given the outcomes of low rent builds (read slums), particularly when the alternative is to lend more to people to buy existing housing or new builds on pieces of land which will result in McMansions (which always go up in price as guaranteed by the RBNZs policies). Banks far and away prefer to lend to those who are buying big flash new houses (new land with strict covenants that force McMansions) or existing houses where the land is close to a city (location based). You will note we have hardly built any houses that we need outside of government, instead we are building houses that make the most amount of capital gain.

Build to rent developers? Dreaming, all "investors" are interested in are capital gain, renting has far too much risk associated with it. For reference, see the number of empty houses in the country (over 10%). https://www.stuff.co.nz/life-style/homed/119636091/200k-empty-ghost-hou…

If the government introduced a punitive empty homes tax, that might change the game. However it goes against their current mandate for "sustained moderate increases" in house prices, so are unlikely to do anything of the sort. I would be delighted to be wrong about this.

"So monetary policy is guaranteeing houses prices now" - where on earth do you think "cheap credit" has come from?? Do you honestly think dropping interest rates and creating $60b and giving it banks where they lend 60-80% of it into the housing market is NOT causing artificially cheap credit? That's literally what the RBNZ wanted to do and succeeded at doing.

Blobbles I have looked at lots of cities from around the world with affordable housing. Christchurch is not my preferred model - but there is clear statistical evidence - especially in the rental market that supply had a significant effect. The common factor of successful affordable cities oversea is they all had was strong supply mechanisms, which meant they coped with various demand shocks, not least global monetary conditions.

I am not saying demand is not important. Foreign buyers ban for instance. Interest rates. Immigration/population growth obviously... but to call NZ's housing crisis a property bubble caused by cheap credit is missing most of the story.

Have you seen the ghost cities of China where there are an estimated 80m empty apartments, yet prices remain high? Even in cities where the prices are often 20-50x median multiples, they will have empty apartments all over the place. The Chinese are about as property obsessed as kiwis, in terms of investments. And they are also supported by their government and central bank. Guess what they have had? An explosion of cheap credit over the past 2 decades...

At what point is it a problem of cheap credit? When we have 20% of our houses sitting empty while we still have a housing crisis and prices are still going up by 20% a year? 40%?

Only a 1/3 of cash in china is in banks. They don't trust their Govt not to grab it so they put it in everything from jewelry to property as a commodity and store of wealth. It's a cash dump and it's immaterial whether the property is occupied or not, and if kept empty then the property is 'new' even if it is held for many years.

And it's even better if they can buy property outside China, as then it is safe from CCP hands. We let them buy property here when the favour is not returned.

I think this is a fairly common misconception. Yes, overseas property purchases are preferred as a store of wealth (and for face) in China for the reason you state. Local ones aren't so much about "to stop the govt taking your money", because everything in the country could be taken if the government wanted to. The government knows exactly who owns what property in China thanks to it's clear registers of property ownership, so could step in at any time and take peoples property just as easily as taking money from their bank accounts. The locals know this all too well as it is exactly what Mao did (my family was former land owners in China who were subject to this).

Property ownership in China is more about investments in safe havens where they can get a return on investment (the Chinese are, as a people, good at finances), as they have fairly high inflation and the stock market is almost considered gambling. It's also a cultural thing, to be able to provide houses for growing family members. But while the motivations are different in China vs NZ, the effects are similar - huge credit availability and high house prices. The difference? China could probably house itself twice over from the amount of supply they have, both empty and underutilised housing. The point I am making is that there is NO supply problem in China, but there is still hugely expensive housing.

The point then is, the housing return is on the capital gains side of the investment, not yield, ie no yield on all the empty properties. If the demand is there for empty properties then as long as this demand is greater than the actual houses built (even if they are empty), then there is still a shortage, hence the expensive housing.

The houses are just another commodity and the investment is not for their direct functional value.

And with a long-term hold mentality then no one knows the value of the secondary market ie, the resale open market. This is exactly what happens with new sections and housing that are developer lead, and that is why most banks have a risk factor (discount value) for any developer pricing. They consider the true value of the asset when it is sold on the open market between two equal/standard purchasers, eg Mum and Dad sellers selling to Mum and Dad buyers.

Yes, exactly. We have commoditised housing as assets which are sure to appreciate in value given that governments and central banks virtually guarantee capital gains (via QE, promises about increasing prices and ever lower interest rates). So supply will barely matter, until you sort out this issue. This is why it's a non functioning market, a market has RISK with every sale, but currently there is no risk because the capital gains is being all but guaranteed.

I think Dale was agreeing that China might have commoditised housing, which are simply bought as a store of value.

I dont see that in NZ..??

Pretty much all of the houses I drive by, in Auckland, are occupied.

Not sure why u think there is no risk..... or that it is a non functioning mkt.

Im expecting a downturn within the next few yrs. And part of that is because supply does matter.

Capitalisation rates cross the economy have dropped greatly over the last ten years. Interest rates for savers are now negative in real terms. There lie the answers in relation to the demand side of the house-price equation.

The additional factor of particular importance in relation the homeless issue has been the fastest population growth rate in the OECD, driven by exceptional immigration rates, which has outstripped the physical capacity of the economy to provide the necessary increased number of houses.

Finding solutions requires addressing the fundamentals rather than band-aid attacks on symptoms.

KeithW

Yes Keith absolutely correct ''Finding solutions requires addressing the fundamentals rather than band-aid attacks on symptoms''.

It’s about monetary conditions and supply.

Why do investors not invest in building houses if the return on savings is so low Keith?

Much easier said than done unfortunately. Specialist role and not for newbies. What about employ some experienced developers in an advisory role through chamber of commerce or mbie. There would already be suitable candidates working for kainga ora. Currently you have to go through consultants that charge the earth and so its in their interests to string you along. They promise anything before you sign them on but afterwards it all changes and by then it's hard to change

If building floor space was an affordable thing to do, which it should be, but it isn't, then the build-to-rent sector would be booming and that should take the heat out of the market.

Brendon,

Investors are investing in new houses, at least in Christchurch where I live. However, the new-builds tend to require significant commutes. Tenants tend to prefer close to the central city. Yields on new-builds in the suburbs are not particularly attractive relative to inner city investments. It is all about location in relation to tenant demographics

KeithW

Last years National Policy Statement on Urban Development is designed to open up more favourable locations for building for build-to-rent and build-to-own investors. Unfortunately it is taking time to implement at the local government level. If efforts are made to speed up and reinforce the process then this supply effect will strengthen and in time will counteract the recent monetary demand stimulus.

Top article Brian, it would have been great to end it with some practical suggestions (in your opinion) to address house price inflation

Says the landlord...

Simple: increase OCR to 1% immediately, and stop money printing. You would see housing prices decreasing significantly, and pretty quickly too.

"Building more houses is not going to reduce house prices much"

Ah pardon me sir... economics 101 supply/demand/equilibrium.

Speculators speculate when there is an expectation of capital gains so remove the expectation and you remove the demand.

But it isnt just the speculators who are buying or keen to buy. There is also a fair amount of latent demand from potential FHB who cannot buy because they dont have enough deposit and the more that prices rise their situation gets worse. Even though paying a mortgage would be cheaper than renting.

Keeping a lid on prices is the start and having an abundance of choice for homebuyers will certainly help.

Exactly - "Speculators speculate when there is an expectation of capital gains so remove the expectation and you remove the demand."

How to remove capital gains expectations - provide certainty that supply will respond to demand.

Lower interest rates does make building houses easier to finance. It also makes infrastructure financing more affordable. This is true both for private and public sector housing. These factors need to be allowed/encouraged to respond strongly to the speculative property bubble.

"How to remove capital gains expectations - provide certainty that supply will respond to demand."

The govt (central and local) has allowed price escalation to take hold in Western BOP. There is a big shortage right now, the number of homes for sale in tauranga has shrunk to less than half what it was. Result... prices shot through the roof, up over 10 percent during the latest 3 months. Absolutely criminal, as prices dont tend to come down much if at all

There’s a reason why there’s an Economics 201. Supply and demand is obviously fundamental but there are many many other factors that can override them, at least in the medium term.

Yet another article from Easton about housing that fails to even mention the impact of half a million net new migrants in the last decade. He has become irrelevant and should be put out to pasture.

.

Meantime in Wellington;

https://www.nzherald.co.nz/nz/students-sleeping-in-cars-as-weekly-welli…

#rentcontrolnow.

Use the lever of house prices not the other way around

Kate

How will rent controls provide houses for those students currently sleeping in cars that your link refers to?

KeithW

It would bring rents down to an affordable price for those on the student allowance + accommodation supplements;

https://www.studylink.govt.nz/products/rates/student-allowance-rates.ht…

https://www.studylink.govt.nz/products/rates/accommodation-benefit-rate…

There are plenty of 1 and 2 bed apartments and small houses in Welly for rent, but not at an affordable price for students either on their own or sharing;

https://www.realestate.co.nz/3944304/residential/rental/503s166-victori…

https://www.realestate.co.nz/3943493/residential/rental/a32-bedford-str…

https://www.realestate.co.nz/3943481/residential/rental/7-d35-johnston-…

https://www.realestate.co.nz/3941936/residential/rental/345-childers-te…

As the person in the article explained, she is paying $245/week in rent alone for a single room in a shared house. That's nearly all of the AS and the SA combined.

That's so sad. How can they study and learn when sleeping in their car? NZ does not deserve educated citizens if it treats people this way.. It deserves to turn to shite and the best people leave and only a few flailing property investors left to prop up the poor - good luck

Leveraging the Mathematics

An AKL home-owner owns their own house mortgage free valued at $1,500,000

They were planning on buying an investment property valued at $1,000,000 prior to 1 January 2021

As a result of the Labour Government and RBNZ ministrations both properties escalated in price 20% over 12 months

The LVR required to buy the investment property is currently 30% requiring a deposit of $300,000

From 1 May 2021 the deposit rises to 40% or $400,000

The equity in the owner-occupied house has risen $250,000 over 2020

No problems, plenty of security. Could afford an LVR of 50% easy. Didn't have to do a thing.

So Brian Easton is an economist who doesnt believe in supply and demand. That says it all really.

Why not use school boy mathematics to work out what is going on. It is well documented that rental investors (those that buy to rent out to tenants) account for around 25% of all sales. That leaves 75% of all sales to owner occupiers be it FHB or existing owners moving. Surely the vast bulk of the buyers must have the biggest impact. In Tasman District they have the smallest ratio of rentals to owner occupiers of any region in NZ yet the prices increases are as high as anywhere. 10 new building consents per 1000 population are issued compared with Auckland at 9.5 and even lower in Waikato. Clearly the economists and politicians need to resubmit their thesis. You all get a fail. Go and study the situation in other countries and see if you can see any trends there.

"It is difficult to explain this graph by claiming we have not been building enough houses."

That graph has got nothing to do with building enuf houses.

The only thing that graph tells me is that House prices have been going up faster than both wages and rents.

Common sense says it is cheap credit + immigration (new money) that enables this.

One of the most basic and useful ideas of economics is the idea of supply and demand..

When there is a misalignment of supply and demand in housing, then there is a probability of a speculative boom going to happen.

Misalignment happens mainly because Construction seems to be a boom/bust , kinda, sector. ( Developers go broke in a downturn).

The seeds of this current boom were sown during the GFC period where The construction sector went into , maybe, the biggest depression since the great depression.

At the same time immigration was climbing ( graph 1) https://www.infometrics.co.nz/top-ten-things-know-migration/

A real imbalance between supply/demand , created the speculative boom.. ( cheap credit is the fuel).

I recall crunching my own numbers back in 2014... I found that most houses in provincial towns were selling at below replacement cost. ( the cost of the section + cost of building was far more than the price of an existing home ). eg houses in Gisborne and Wanganui were selling for $150000 -200000. If a new house was to be built and a section was $150,000 plus 150sm house x $1500/sm = $225000... = total $375,000 ...then how on earth will a developer make a profit???

How much of a premium does a new house sell for. ?

This "Gap" has nothing to do with "speculation". AND the gap is kinda Asymmetrical. ie. the forces that respond to demand take quite a while to respond. .... ( the demand for existing homes has to reach a level where prices make building new homes profitable )

Throw in restricted land supply and building cost inflation AND Council grafting..... and you end up with a very misaligned supply /demand dynamic..

Out of this comes the "specualtiveBoom", in my view..

If Easton was serious in exploring the causes of house price inflation, he would have investigated the supply side of the story..... a little more seriously.

I trade the mkts ...and there is a stage where the fundamental forces of supply/demand give way to speculative forces, where price movement itself generates increasing demand . ( Normally increasing prices should reduce demand ).

Are we too late in this current cycle to change things in a meaningful way ( mitigate demand )..? ( Easton's article is relevant in this regard)

It looks like we might go the way of the irish , where going into the GFC they were in the throes of a construction boom.... building houses ..for the sake of building houses...( speculative construction ), and then they had a serious crash..

In a way, we need a decent "Crash" . Just as the great depression changed peoples attitudes to debt, so might a decent crash , here, in NZ.

Most NZers do believe house prices can only ever going up...with only small aberrations...here and there.

ps... If John Key had been truly wise he might have rescued the Construction sector back in 2009 , and started building State houses . There were already reported housing shortages back then .. If Govt can be counter cyclical with its investment.... that might be a good thing..????

However. Now we have an (upper) middle-class. and the problem with neoliberal social democratic parties is that they’re timid. They avoid upsetting the corporate, business elites. They focus on feel-good social justice issues and not nearly enough on economic (equality) justice." They will (the current government) blag there way through as many terms as they can to maintain the status quo. The MMT Bomb set in place for the Millennials to discover just like an IED somewhere further up the road in the future, after the party stops.

You have nailed it!

What do u mean by .."MMT bomb" ?

Modern Monetary Theory. Print(QE) until you drop!

Are u saying the MMT bomb is a good thing or bad thing..? for millennials

Bad if you have no means of paying off the debt. MMT will only work if you tax to keep inflation under control and then use it to pay down debt.

But, as we all know, neoliberal governments and conservative governments do not like the "tax" word let alone implementing a tax or increasing taxes. Therefore MMT will fail.

If new houses were less $ than new houses, wouldn’t that drag down the price of existing houses. Cheaper land and cheaper building costs are what’s needed.

All things being equal, yes. The price of all residential land is set by what price the fringe land can be bought for.

The dearer on the fringe, the dearer (relative) it is going back in than if it had been cheaper on the fringe. This line from fringe to CBD is the same for any city in the world. The starting point on the fringe matters as it affects all land pricing.

Shuush Brian, remember (whisper).. we must only stated about the supply & demand thingy... no distortion.

It is proven that actually the IQ across the ditch is far superior on extracting the bottom line from 'IQ deficit NZ'

We have just received a list of material price increases ranging from 2% - 18%; & also advised that increases were coming so often & so fast that it wasnt possible for our merchant to give us advance notice. Ad to this recent additional requirements (attenuation tank $5,000; mascerating pump $6,000.00; water garden $10,000.00) to add to all the other extra we have had to pass on to our clients. I am really interested to get feedback on how this helps house affordability - let alone first home affordabiltiy. The building industry faces a tsunami of cost increases - & its not letting up. Also like feedback on how we can sensibly provide a fixed price contract when no-one knows what the costs are going to be 3-6 months down the track

peter.may, very interested in your comments from a planning perspective. I'm assuming this is a new build/single dwelling home?

I would have thought these requirements would have been known/required as conditions of consent and/or in the PIM (because, yes, you should be able to provide a fixed cost - plus contingency - price. In other words, these items should not be 'additional' (in the sense of additional unknowns, or unexpected costs to the client) but perhaps they are additional in relation to new rules in a plan that weren't there previously?

My experience is that we are now building residential homes on more difficult (i.e., what could be termed) marginal urban land - land that in many cases was a natural runoff in the past (i.e., open, pervious space). Hence, the sites come with additional requirements, for example the attenuation tank as a means to achieve 'hydraulic neutrality' (i.e., prevent flooding/ponding in the receiving neighbourhood)?

I'd be interested to know what city/district plan your build is in and whether you'd say it was a more difficult site.

Yes, I've spoken to a lot of builders lately who are aghast at rampant materials price inflation. I think it could be connected to disrupted freight schedules and movements. And these issues might become the norm going forward. We might need to rely a lot less on imported goods - which would see us needing to design-for/from-local and there may be many new, small scale manufacturing opportunities coming up.

Hi Brian - nice piece and you are one of the few commentators to get this right. Most confuse the market for 'housing service' with the market for housing investment. So they assume/infer that if only the rate of house building would increase 'the market' would reach some sort of equilibrium and price escalation would dwindle. Not while mortgage rates are 2.5% per annum or thereabouts, and other favorable settings tax/leverage remain and term deposits earn 1.5%. The investment motivation and market dominates prices. And most of the key factors (interest rates, taxation, risk weightings) are set by the government.

Let’s level the playing field. Ban the use of equity in one home to fund another. Ban the use of interest only loans to fund another. If someone wishes to purchase another property, they can save a deposit and get a traditional home loan as first home buyers do. Those who are already in this position should be given a few years grace to either restructure their loans or sell their properties. Let’s do what’s right by our future generations and give them a fair go. Let’s not create an even greater divide between the haves and have nots. Let’s bring our house prices back to where they should be, and we’ll all be better off.

Bank debt leverage drug like junkie behaviours sure need fixing.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.