This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

A short film representing Boomers v Millennials in the property market https://t.co/EPzytIUTKR

— Nate Rarere (@oldmannato) June 13, 2021

1) Could central bank digital currencies remove the need for the bank middleman?

The Bank for International Settlements (BIS) has had a lot to say about central bank digital currencies (CBDCs) lately. It's latest instalment comes in a chapter of BIS' Annual Economic Report.

Central banks around the world are at different stages of adopting, or at least considering adopting, a CBDC using an electronic record or digital token to represent the virtual form of a country's fiat currency, which in New Zealand's case is the NZ dollar. Here in NZ, we'll be hearing more about the potential for a local CBDC from the Reserve Bank sometime this year.

As you'd expect from the central banks' bank the BIS chapter extols the potential virtues of CBDCs, pours scorn on cryptocurrencies as speculative assets with a wasteful energy footprint, dismisses stablecoins as an appendage, and sounds absolutely terrified of big tech's potential in payments and broader financial services, market power dominance, and raises concerns about such companies mass access to peoples' data.

One of the issues highlighted is the potential for CBDCs to cut out intermediaries such as banks, thus giving the public a much more direct relationship with their central bank. I would add, however, that this isn't the preferred BIS option. It's in favour of a status quo model with central banks working with private sector banks. But nonetheless it's a thought provoking concept.

CBDCs could provide a tangible link between the general public and the central bank in the same way that cash does, as a salient marker of the trust in sound money itself. This might be seen as part of the social contract between the central bank and the public. CBDCs would continue to provide such a tangible connection even if cash use were to dwindle.

Vital to the success of a retail CBDC is an appropriate division of labour between the central bank and the private sector. CBDCs potentially strike a new balance between central bank and private money. They will be part of an ecosystem with a range of private PSPs [payment service providers] that enhances efficiency without impairing central banks’ monetary policy and financial stability missions.

Central banks and PSPs could continue to work together in a complementary way, with each doing what they do best: the central bank providing the foundational infrastructure of the monetary system and the private PSPs using their creativity, infrastructure and ingenuity to serve customers.

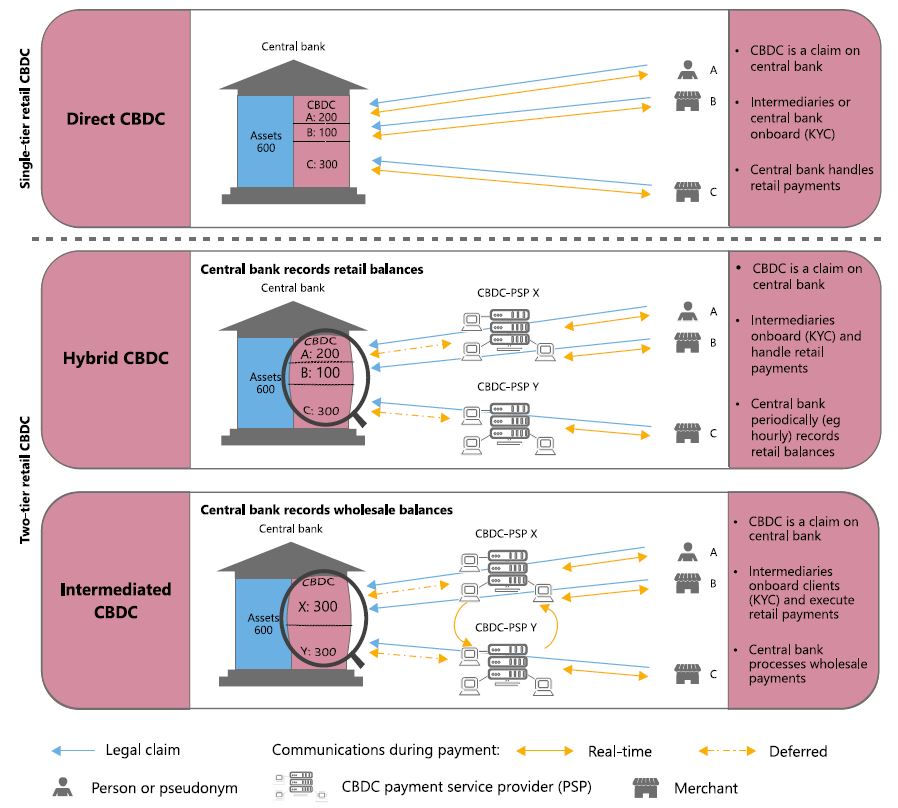

Indeed, there are good arguments against a one-tier system fully operated by the central bank, ie a direct CBDC [see graph below]. Direct CBDCs would imply a large shift of operational tasks (and costs) associated with user-facing activities from the private sector to the central bank. These include account opening, account maintenance and enforcement of AML/CFT rules, as well as day-to-day customer service. Such a shift would detract from the role of the central bank as a relatively lean and focused public institution at the helm of economic policy.

Equally important is the long-term impact on innovation. Banks, fintechs and big techs are best placed to use their expertise and creativity to lead innovative initiatives, and integrate payment services with consumer platforms and other financial products. Central banks should actively promote such innovations, not hinder them.

Most fundamentally, a payment system in which the central bank has a large footprint would imply that it could quickly find itself assuming a financial intermediation function that private sector intermediaries are better suited to perform. If central banks were to take on too great a share of bank liabilities, they might find themselves taking over bank assets too.

For these reasons, CBDCs are best designed as part of a two-tier system, where the central bank and the private sector each play their respective role. A logical step in their design is to delegate the majority of operational tasks and consumer facing activities to commercial banks and non-bank PSPs that provide retail services on a competitive level playing field. Meanwhile, the central bank can focus on operating the core of the system. It guarantees the stability of value, ensures the elasticity of the aggregate supply of money and oversees the system’s overall security.

However, as households and firms hold direct claims on the central bank in a retail CBDC, some operational involvement of the central bank is inevitable. Exactly where the line is drawn between the respective roles of the central bank and private PSPs depends on data governance and the capacity for regulation of PSPs.

Retail CBDC architectures and central bank-private sector cooperation

In the direct CBDC model (top panel above), the central bank handles all payments in real time and thus keeps a record of all retail holdings. A hybrid CBDC architecture (middle panel) incorporates a two-tier structure with direct claims on the central bank, while real-time payments are handled by intermediaries. However, the central bank periodically updates and retains a copy of all retail CBDC holdings. By contrast, an intermediated CBDC architecture runs a wholesale ledger (bottom panel). In this architecture, PSPs would need to be closely supervised to ensure at all times that the wholesale holdings they communicate to the central bank indeed add up to the sum of all retail accounts.

Source: Adapted from R Auer and R Böhme, “Central bank digital currency: the quest for minimally invasive technology”, BIS Working Papers, no 948, June 2021.

2) Why you can't debase a fiat currency.

I enjoy the informative and thought provoking work of Bloomberg editors Joe Weisenthal and Tracy Alloway. You can check out their Odd Lots page here.

In one of Bloomberg's recent email newsletters Weisenthal shared some interesting thoughts on what the rise of cryptocurrencies highlights about our fiat currencies. Remember the gold standard, a monetary system where a country's currency or paper money has a value directly linked to gold, was finally ended in 1971 when US President Richard Nixon severed the direct convertibility of US dollars into gold.

Fiat currencies have dominated since. Fiat money is government-issued currency not backed by or convertible into anything else such as a physical commodity like gold or another country's currency. It's backed by the government that issues it.

Weisenthal points out that much of today's thinking about money still dates from the gold standard era.

The rise of crypto has brought new awareness to fiat currency. It makes sense. The first time in a fish's life where it ever thinks about water is when it's flapping around on a boat deck gasping for oxygen. It's only through the introduction of some seemingly oppositional force that we become aware of the world we're immersed in.

We've been swimming all this time in the world of dollars and yen and francs and pounds, and so we haven't had the chance to really think about fiat currencies. And it shows.

So many people's mental models of money are rooted in gold-standard thinking. People talk all the time, for example, about how we're going to "debase" the currency. But that word makes no sense in the fiat realm, as it logically relates to the concept of making a gold coin less pure by degrading or adulterating its substance, as if the dollar were old Roman coins that had less and less silver content over time.

Numerous conversations about "money printing" or "how are we going to pay for it?" have an implied basis in gold standard thinking. Like somehow we're going to run out or be forced to go cap in hand around the world looking for generous donors.

With any luck the surge in interest in fiat currency -- which again, we have to thank crypto for -- gets us to think more deeply about it and how currencies whose value is rooted in law and public convention have different characteristics than what came before, and what's come after.

3) 'The ugliest and most despairing column I have ever written.'

Our old mate Bernard Hickey is feeling very downbeat about the housing market, even by his standards. He describes this article for The Spinoff as "the ugliest and most despairing column I have ever written." (I did joke to David Chaston that's quite a high threshold!)

It's a look at the New Zealand housing market since he returned from overseas in 2004, covering the almost continuous price rises and dashed hopes of meaningful change. He concludes that young people without parents able to help them with a sizeable deposit, or who don't marry into wealth, have no home ownership hope and should move to Australia.

Those parents still renting and those just graduating into Covid without assets should move now. Giving up hope seems a capitulation. It is. But sometimes discretion is the better part of valour. Sometimes there is no hope. Move to Australia and you’ll find wages are 30-40% higher and rents have fallen $50-100 in the last year.

I write this as the Wellington City Council is debating whether to gut its spatial plan to ensure fewer houses are built to avoid altering the views of those who own homes close to the centre of town. It is hopeless in my experience of covering this debate for nearly 20 years. Get out while you still can.

At the end of May the median house price was $820,000, up 30% in a year and not slowing down despite the government’s actions in November and March to address supply and demand, again without any real intent to lower prices. And the median rent was $550 a week, up $150 a week since the election of the Labour-led government.

These prices are predicated on home buyers being able to handle mortgage rates of at least 6%, which is the affordability threshold set by bank lending managers. Any shift lower in that affordability threshold towards 4%, which is likely as interest rates stay below that for several more years, would justify house prices rising another 50% in the next couple of years.

4) Living with COVID-19, long-term.

In Singapore's Straits Times an article by some of the country's government ministers looks at living something resembling a pre-2020 life even though COVID-19 is likely to be with us for the long-term. They point out that COVID-19 may never go away, continue to mutate and likely become endemic like influenza.

The article's by trade and Industry Minister Gan Kim Yong, Finance Minister Lawrence Wong and Health Minister Ong Ye Kung who co-chair Singapore's COVID-19 multi-ministry task force. We're likely to start hearing similar messages from New Zealand authorities as vaccination rates ramp up here, and we evolve from our elimination strategy.

With vaccination, testing, treatment and social responsibility, it may mean that in the near future, when someone gets Covid-19, our response can be very different from now.

The new norm can perhaps look like this:

First, an infected person can recover at home, because with vaccination the symptoms will be mostly mild. With others around the infected person also vaccinated, the risk of transmission will be low. We will worry less about the healthcare system being overwhelmed.

Second, there may not be a need to conduct massive contact tracing and quarantining of people each time we discover an infection. People can get themselves tested regularly using a variety of fast and easy tests. If positive, they can confirm with a PCR test and then isolate themselves.

Third, instead of monitoring Covid-19 infection numbers every day, we will focus on the outcomes: how many fall very sick, how many in the intensive care unit, how many need to be intubated for oxygen, and so on. This is like how we now monitor influenza.

Fourth, we can progressively ease our safe management rules and resume large gatherings as well at major events, like the National Day Parade or New Year Countdown. Businesses will have certainty that their operations will not be disrupted.

Fifth, we will be able to travel again, at least to countries that have also controlled the virus and turned it into an endemic norm. We will recognise each other's vaccination certificates. Travellers, especially those vaccinated, can get themselves tested before departure and be exempted from quarantine with a negative test upon arrival.

5) A cricket tragic celebrates.

As a cricket tragic I've been basking in the Black Caps' victory in the World Test Championship Final this week. For anyone who doesn't know, they beat both a strong Indian team and the fickle English "summer" weather. I've been devouring plenty of articles on the game, and cricket in general. Here I'm linking to two especially enjoyable ones.

The first one, by Jarrod Kimber of ESPN's Cricinfo, runs through the colourful history of New Zealand test cricket as perennial underdogs given little thought by the game's superpowers. Below is a flavour of the article, which nicely encapsulates just how momentous this victory is.

There is a story I found when John R. Reid died. It was written on some long-forgotten cricket forum or blog, and it was about Reid's preparation for a tour to England when he was captain of New Zealand.

Reid worked at a service station, and to warm-up before the tour, he asked for volunteers to come down and bowl to him in the local nets. One of those was a young boy, around 12, who tried his hardest to help Reid. The pitch they had on offer was concrete. Reid was going up against the great England cricketers in an era they dominated, with kids bowling to him on a concrete wicket.

There is amateur, there is graft, but New Zealand weren't playing the same sport as England at that point.

The second article, by The Guardian's Andy Bull, is a colourful celebration of just what a crazy and unique game cricket, especially test cricket, is.

When the ICC designed this new competition, the final was supposed to be a week-long celebration of Test match cricket. And, even though the match was relocated from Lord’s to a ground built in a retail park off the motorway near Southampton, even though the social distancing measures meant the crowd was restricted to around 4,000 a day, even though two entire days of play were washed out by rain, even though the conditions were so difficult that only two batsmen managed to scrape past 50 runs in the entire game, it seems to me that they succeeded admirably. It felt one for the connoisseurs, all those of us who have already been converted.

Because Test cricket is awkward, irritating, and silly. It has languors, it can be baffling one minute, boring the next, and brilliantly compelling the third, and it does last an unreasonable amount of time, and demand an unfeasible amount of attention. Which is why its rhythms are entirely unlike anything else in all of sport.

And despite that, it all turned out perfectly, on one long, enthralling last day’s play, ending on a beautiful late afternoon, with New Zealand’s two greatest batsmen grinding away against one of the finest all-around bowling attacks ever put together, trying to find the final 30 runs their team needed for victory.

The World Test Championship has just been won by a team who can’t even really afford to play the game. Unless they happen to be playing India, the New Zealand Cricket board actually loses money on most of the Test matches it hosts. Like I say, nothing about this game really makes much sense.

(This article, from Greg Baum of The Age is nice too).

Above: Ross Taylor & Kane Williamson enjoy their moment of victory. Photo: Alex Davidson/Getty Images.

Kyle Jamieson receiving the player of the match award in bare feet was an extremely Kiwi moment.

— Jarrod Gilbert (@JarrodGilbertNZ) June 23, 2021

23 Comments

"Numerous conversations about "money printing" or "how are we going to pay for it?" have an implied basis in gold standard thinking. Like somehow we're going to run out or be forced to go cap in hand around the world looking for generous donors."

Exactly. Our constraints are real resources - people, skills, natural resources, energy, infrastructure - NOT how many dollars the Govt has spent into existence.

Our constraints are real resources - people, skills, natural resources, energy, infrastructure - NOT how many dollars the Govt has spent into existence.

This comes from the MMT spiel. My question is that how does fiat maintain a 'store of value' property if the supply can be endlessly expanded? It doesn't make any sense, despite how many resources you think justify it as an SOV for your currency. People might point to the yen as an example. At the end of the day, Japan lives within its means, despite QE. It's the difference between broad and base money. People and firms are paying down debt, not taking on more like the bubblicious Anglosphere countries.

Not sure what "MMT spiel" is - I am just acknowledging the reality of post-gold standard fiat money systems.

The 'store of value' is simply a promise from a sovereign Government that the IOU that you hold as cash in your hand or as numbers in your bank account will be honoured.

Japan lives within its *resource* means, which was my point. The Govt debt level in Japan (200% of GDP?) is just a number. Who cares?

Govt Bonds are just IOUs that pay a bit of interest. So, QE is just swapping IOUs that don't pay interest (newly created cash) for IOUs that pay a bit of interest (previously sold bonds). Bond sales are the same in reverse. Govt 'debt' does not really change either way.

The whole thing is a charade to create the illusion that Govt money is finite somehow - like Govts have to take money off rich people to spend on the voting public. Ridiculous really.

What you're saying follows the MMT dogma about being 'constrained by resources', which doesn't make sense to me. What is the relationship with fiat currency? My issue is that fiat currency is a store of value because it's exchanged for labor, so the attitude is that it's just an IOU also doesn't make much sense.

I think we probably agree in the main. The value of fiat currency in a country is determined by its equivalence to real resources - $23 will buy you an hour of unskilled labour and about half an hour of skilled labour for example in NZ. What allows people and companies to sell and buy labour, and trade what they earn or make for other things though, is a Govt supported currency that acts as a safe and stable intermediary (Govt backed IOUs for people to swap with each other).

Government spending is of course constrained by real resources. For example, if Govt decided to put solar panels on all houses in NZ tomorrow, this would cause unwelcome inflation on solar panels, panel fitters, etc. When the MMT folk say that Govt spending is constrained by real resources, I think they are talking about examples like this - i.e. where too much Govt spending on supply-constrained stuff causes inflation.

Labour is so little of 'work done' as to be inconsequential. Complete noise.

What we've done is claim a portional right to the extract/consume/excrete resource stream (and the energy which does the work). Lawyers have claimed a bigger portion than cleaners - house speculators currently think they have claimed a portion bigger than both. Problem is, there isn't enough left to cover the bets.

Doesn't matter where your bet was fiat, crypto, even cash; if there's more bets than underwrite, the chips are about to get worth a lot less. But issuing more bets hasn't 'stimulated' 'the economy' because of the same restriction. So we can see inflation, but not interest-rate rises. And despite the hype, we're not seeing real growth (You can watch that by watching energy-use - too easy). So I'm guessing deflation in the longer term. Permanent.

None of the IOU's make sense at this stage. We can take the banks out of the picture, they're just parasitic. Govt. issuance is fine; but it needs to pass the underwrite test too. Same with bitcoin. And they all come down to faith and belief.

None of the IOU's make sense at this stage. We can take the banks out of the picture, they're just parasitic. Govt. issuance is fine; but it needs to pass the underwrite test too. Same with bitcoin. And they all come down to faith and belief.

Now this I can grasp better. But do people really understand how expansion of money dilutes the value of currency? This is why I refer to what one's labor can be exchanged for. So if we take the price of housing (which is really just banks lending money into existence), this has to impact the value of labor for young people. More hours need to be exchanged for shelter, whether it's rent or mortgage payments.

Bitcoin is different. Sure, it needs faith and belief. I would suspect that most people think it doesn't have any or limited value. It's underwritten by the integrity of its blockchain and energy required to sustain it. And most attractively, it's deflationary as opposed to inflationary.

Is the supply really being expanded? It depends on whether you think lending money is expanding supply. I personally don’t; if someone lends me money I don’t think I’m any richer. If the supply of money was genuinely increasing then we would see CPI inflation.

Is income tracking money supply expansion? No. The CPI is a construct that doesn't represent the cost of living for an individual or household.

An article here that explains why government spending is not inflationary, tax and savings. http://www.matchesinthedark.uk/spending-chains-sankey-diagrams/

JC, the understanding of what supports the value of a currency should be discussed mush more often and in much more detail. Before the gold standard was dropped, the total amount of money in any system was constrained, and this would have been a major part, but not all, of it's value. It's the other parts of that equation which dominate now; the quality of government and their economic policies, the ability to get a return when investing in that currency, the spending power of that currency, it's popularity (therefore demand) are all a part of the equation. But the total amount available will still be in there too, just at a much reduced weighting.

So i agree with Weisenthal that thinking is still constrained by pre-1971 concepts. We, including our politicians, continue to think of Government spending as 'debt', when it shouldn't be. BUT Government's must also be careful, as their spending should be targeted to items that are designed to create value, or necessarily preserve it.

That video on Twitter just nailed the slogan re housing in NZ.

Sure did - I love how the women never even glanced at the little girl as she walked away as too busy getting high fives from her mates. Reminds me of boomers when they outbid FHB at auctions.

I was thinking what a real NZ version of Monopoly would be like. I reckon it would go like this: there are four players, Boomer, GenX, Millennial, and Gen Z. The player designated Boomer goes first, and gets to make one complete trip round the board buying as many properties as they can. Once they have passed go, the Gen X player may start, but the prices of all the properties on the board double, and the rents increase by 50%. You get $20 extra dollars for passing Go. Every time the Boomer passes go, these increases are applied again, and a new player may start. Oh, and if a player wishes to buy property, but does not have enough actual cash, they may borrow from the bank up to 60% of the current value of their properties.

3. The entire resource consent system allows councils to impede residential development. They opt to do so because financially it makes sense for them to limit development. We could easily remove those constraints and the building boom would push our economy along nicely.

5. If you're a cricket fan I recommend Jarrod Kimbers YouTube: https://youtu.be/pSMu3y0PJMQ

Yes, an interesting article from Bernard Hickey - here's another one worth reading;

https://thespinoff.co.nz/business/18-06-2021/bernard-hickey-our-empires…

One would think that in most advanced countries, these properties would be condemned. We ought to bring in a regime regarding house condition much like that to do with vehicle condition;

https://www.drivingtests.co.nz/resources/notices-ordering-a-vehicle-off….

Otherwise we'll never get the amount of demolition and re-build needed.

Eliminating retail banks would cut competition for services.

Offering a basic public banking service with mortgage rates at OCR + 2% and dividends for people with deposit accounts, would mean cheaper rates for borrowers, better returns for savers, and less profits for rich shareholders. Win. Win. Win.

Bernard is 100% right.

Nice cricket inclusion, I am a cricket tragic too. Very sleep deprived...

The standard price now for a standard family home on a section in an average suburb in NZ is $1 million.

Cheers for the cricket piece.

New Zealand has shown how to revive Test Match Popularity.

Reduce Matches to 3 days.

They can be won in 3 days.

Central Banks need Main Street Banks to rule over. So, they will give the share of CBDC operation to them. Private sector will have to be on its toes with constant innovation to run a parallel Crypto network to compete and undermine the CBDC system. Wonder how the Public will take to that confusion ?

May be China will provide the lead in this field and that will shift the power base of monetary practices to the East. A Bretton Woods in China perhaps ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.