By Gareth Vaughan

Dear Steven Joyce (Economic Development Minister) and David Smol (Ministry of Economic Development chief executive),

I'm writing to you to draw to your attention to what, in my opinion, is a serious problem for this country. I also want to highlight an example of bureaucratic buck passing that is occurring on your watch.

This week I contacted the Ministry of Economic Development (MED) with questions about an entity registered through MED's Companies Office as City Savings Institution Ltd and operating through a website as City Savings Bank. This entity, with a small office on Auckland's Queen Street, is seeking to raise money overseas and claims to be regulated by the Reserve Bank and New Zealand government when it isn't.

Following our story the Reserve Bank issued a warning notice about City Savings "Bank", which incidentally has now dropped use of the word "bank" from its name on its website. The Reserve Bank warning says: "This company is not licenced or prudentially supervised by the Reserve Bank of New Zealand or any other New Zealand authority. It is not authorised to provide banking services or take deposits."

Having rubber stamped City Savings Institution's registration as both a company and financial service provider, what I specifically wanted to know from MED was whether it was aware of this entity's activities and was MED taking any action against it?

I have to say the response I got, via an MED spokesman, left me fuming:

The Companies Office have looked into the circumstances of the City Savings Institution Ltd (CSIL), which appears to be trading as the “City Savings Bank”. Our enquiries indicate that CSIL has been properly registered as a New Zealand company and as a financial services provider.

CSIL and (its general manager) Simon Virgo appear to be appropriately registered as financial service providers, as they have a place of business in New Zealand and provide financial services, which are the two threshold requirements for registration under the Financial Service Providers (Registration and Dispute Resolution) Act 2008.

The Companies Office, as the operator of the register of financial services providers, takes steps to ensure that all providers have an actual place of business in New Zealand so that its staff and those of other regulators, such as the Financial Markets Authority (FMA) and the Reserve Bank, have access to records and employees should the need arise.

The use by a company of the word “bank” in its trading name is an issue for the Reserve Bank. The Companies Office does not allow companies to register the word “bank” or similar terms in their company names, unless those companies have been authorised by the Reserve Bank.

Pressed further that it was City Savings Institution's activities post its registration as a company and financial services provider that was the issue rather than whether it was properly registered or not, the spokesman came back with:

As discussed, City Savings Institution Ltd and Simon Virgo appear to be properly registered and operating within the requirements of the Companies Act and Financial Service Providers (Registration and Dispute Resolution) Act. You would need to refer questions on laws administered by other agencies to those respective agencies.

Now, I understand MED runs the company register, but doesn't actually monitor what companies do once registered. But not even a "we are concerned the activities of this company might bring New Zealand's good reputation into disrepute and will assist our fellow regulators, in any way we can, if they want to look into it?"

Effectively this answer is telling me that MED will rubber stamp company and financial service provider applications for almost anyone with a pulse and who stumps up the required fee. And what happens once they're regulated? "Not our problem."

Has it crossed your mind that having one arm of government registering companies and others overseeing them once they're registered may not be the best option?

'The classic modus operandus of a Ponzi scheme'

You're no doubt familiar with the activities of New Zealand registered company SP Trading, extensively covered by Fairfax's Mike Field. Just to remind you, SP Trading was involved in the charter of a plane intercepted at Bangkok airport - having come from North Korea - with a cargo of weapons aboard. You should also recall a cabinet paper last year highlighted "a New Zealand registered company with its effective base in Panama (that) recently committed a significant tax fraud in the United Kingdom."

And you should be aware of an entity called First Capital Savings & Loan Ltd. Incorporated in New Zealand in February 2007, it purportedly traded foreign currency on behalf of investors in a pooled investment programme primarily raising money from US investors. The Securities and Exchange Commission (SEC) charged this company and its director Jeffery Lowrance with running a US$21 million Ponzi scheme last July, saying it had ripped off hundreds of investors.

The SEC says in reality after transferring investors' money to an off-shore account, Lowrance and First Capital Savings & Loan secretly diverted investor funds to pay fake returns to other, earlier investors in the "classic modus operandus of a Ponzi scheme." The SEC says Lowrance also secretly diverted investor funds to pay himself - despite failing to earn a profit for his investors - and to fund a start-up alternative newspaper, USA Tomorrow, which ran articles and advertisements promoting a limited government ideology. See the full SEC complaint here. And here's an SEC press release saying Lowrance was arrested in Peru after fleeing there.

You'll also be familiar with the similarly named New Zealand International Savings & Loan Ltd, given Green Party co-leader Russel Norman questioned then Commerce Minister Simon Power about this entity in Parliament last year after a Naked Capitalism blog described MED as "clueless" and highlighted the inadequacies of our companies registration system.

You should also know the World Bank and International Finance Corporation rank New Zealand the easiest, of 183 countries surveyed, in which to start a business, pointing out a company can be registered by the Companies Office in just one day. The Companies Office itself notes that "starting a company online (incorporating) is as simple as reserving your company name (NZ$10.22), completing the incorporation application (NZ$153.33) and returning your signed consent forms."

Every company must have at least one director, with only the under 18s, undischarged bankrupts, and the broad brush sounding anyone "otherwise prohibited" from directing, promoting, participating in the management of a company under any statutory provisions, not eligible.

Reserve Bank's headache & what about John Key's funds hub?

MED's rubber stamp company registration process is posing particular problems for the Reserve Bank.

Last year Power said the Reserve Bank believed about 1,000 shell companies incorporated in New Zealand over three years had been used to carry out banking activities free of regulatory oversight and "many" seemed to be undertaking fraudulent activities. Furthermore, Power said 143 New Zealand registered companies were implicated, over a four year period, in criminal activities overseas such as smuggling, money laundering and tax fraud with New Zealand Police and the Customs Service receiving 134 enquiries about them.

Following Power's revelations a Reserve Bank spokeswoman told interest.co.nz the Reserve Bank had prevented "many" frauds occurring overseas through the financial activities of New Zealand registered companies and, with Companies Office assistance, had got a "significant" number of companies expunged from the Companies Register.

Thus it seems fair to assume City Savings "Bank" is the tip of a very large iceberg. The mind boggles at how many of these entities may be out there, given there's likely to be plenty the Reserve Bank isn't yet aware of. If you don't believe me take a look at the Reserve Bank's other warnings, posted on its website here, or just read on. And whilst doing so, ask yourself what all this means for Prime Minister John Key's dream of New Zealand becoming an international financial funds management hub.

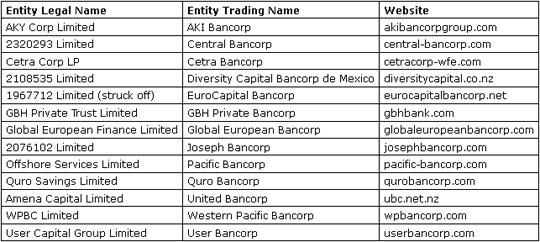

In one warning notice alone (see below) last July the Reserve Bank outed 13 dodgy entities (see below).

'New Zealand a premium 'onshore' jurisdiction, providing more benefits than traditional 'offshore' jurisdictions'

Another company the Reserve Bank has issued a warning on is Swiss Financial Corp. On its website Swiss Financial Corp claims it has been formed in New Zealand, which it describes as one of the most politically and economically stable countries in the world, as an offshore banking financial institution subject to the laws and banking regulations.

"This means that in any country, Switzerland and Greece including, it operates as (an) offshore banking company offering the advantages that a national institution can not expose," it adds.

Swiss Financial Corp notes it's "registered on the New Zealand MED" under the number 2211403. It says its banking activities are regulated, but not limited, by a range of acts including the Reserve Bank of New Zealand Act and Securities Act. It suggests New Zealand could be an "attractive secure jurisdiction" for new structures and for re-domiciling existing structures.

"New Zealand is a premium 'onshore' jurisdiction, providing more benefits than traditional 'offshore' jurisdictions and is not blacklisted by any country or authority in the world and does not have tax haven connotations. It gains additional credibility by being a member of the OECD and is not part of the EU, and is not influenced by the EU Saving Tax Directive," Swiss Financial Corp's website says.

It goes on to say that New Zealand has been providing foreign trusts for several years.

"These English types of trusts when settled by an offshore resident, and where income is sourced outside New Zealand, provide tax free income to the trust and the beneficiaries. Private Trustee Companies are generally used, which provides the settler some direct or indirect involvement in the trustee's operation. These trusts are also asset security and secession structures."

On the Companies Office website Swiss Financial Corp gives its registered office and address for service as Trustees Executors - level 5, 10 Customhouse Quay, Wellington. But it says this will change to 106/23 Edwin Street, Mt Eden, Auckland from March 26. Its sole director is a Renzo Pillon of Zurich, and sole shareholder Paysage Inc of Delaware, USA.

Robert Groover of Woodstock

Another company the Reserve Bank has warned of is Bantec Financial Group, which gives its registered office and address for service as 40b Esk Street, Parkvale, Tauranga. Its directors are listed as Anthony Gelonesi of Sydney and the scarcely believable Robert Henley Groover of Woodstock, USA. (That said a Google search did turn up a man by that name in Woodstock, Georgia, as opposed to the Woodstock in New York State where the famous music festival was held, so perhaps this is a real person).

Others outed by the Reserve Bank - in recent times - include Elite Bank Group which is not authorised to use the name "bank" or to provide banking and financial services as claimed on its website. Then there's Windsor Savings Limited trading as Windsor Bancorp, Alfix Group Limited, Caya Capital Markets NZ Ltd and their associated trading names the Options Bank and BursaMarkets, complete with websites in Arabic and owned by a Belize domiciled company.

Now, let me pause here to emphasise that all these so-called banks or finance companies are still operating despite the Reserve Bank warnings.

So what are you going to do about it?

Mr Joyce, we know your government does actually realise there is a problem. So that is a start.

Power, who is now the head of Westpac's Private Bank, introduced the Companies and Limited Partnerships Amendment Bill to Parliament last October in what he described as a move to tighten rules around company directors and company registration to protect New Zealand's reputation as one of the best and most trusted places in the world to do business, given this reputation was threatened by overseas interests using New Zealand-registered shell companies to undertake criminal activity.

Power has been succeeded as Commerce Minister by Craig Foss, whose spokeswoman told me this week the Bill is still awaiting its first reading. Once it has had the first reading, the Bill will then be referred to a select committee, with the select committee process likely to take about six months. So it's clearly not a government priority.

And even if passed, will this Bill make much difference?

I'm told not because it has limited application and is largely symbolic.

What it will do is make each company, and limited partnership, have at least one person who lives in New Zealand legally responsible for the entity's administrative affairs. He or she will have responsibility (along with the other relevant people) if the entity fails to comply with its reporting and record-keeping obligations. But with further reading the Bill actually talks about New Zealand registered companies having a resident agent "if they do not have a director who lives in New Zealand or in an enforcement country" where New Zealand judgments with regulatory regime criminal fines can be imposed.

All this really means is that the authorities should be able to find someone to sue and/or prosecute if they have evidence of a serious crime. It won't actually stop another SP Trading registering in New Zealand and shipping arms around the world.

Powers to act

Now, the Reserve Bank, FMA and even the Commerce Commission, do have powers to act in these situations. The Reserve Bank can move against an individual or entity that's claiming to be a banker or New Zealand registered bank when they aren't. Potential penalties for an individual, if convicted, include up to 12 months jail and a NZ$100,000 fine and a NZ$1 million fine for a body corporate.

The FMA can also potentially act if someone says they're regulated by a regulator and they aren't, and against general misleading conduct, through either the Securities Markets Act and the Fair Trading Act, with the later something the Commerce Commission could even move under. In the case of City Savings "Bank" the Reserve Bank says it's continuing to make enquiries and will take action as appropriate, and interest.co.nz understands the FMA is also making enquiries.

Look, I accept there are trade-offs as to what our assorted regulators must prioritise and that for each of these rogue overseas entities there are plenty of legitimate registered companies getting on, perfectly legally, with their daily business.

New 'super ministry' offers an opportunity

But as you, Mr Joyce and Mr Smol, move towards the government's new "super ministry" combining the MED, the Department of Labour, the Ministry of Science and Innovation, and the Department of Building and Housing into the new Ministry of Business, Innovation and Employment, can you please take some time to look at this issue of dodgy overseas entities abusing our rubber stamp company registration process by bringing New Zealand's good international reputation into disrepute through activities that, frankly, could amount to anything? We simply don't know what a lot of these companies are really doing.

Perhaps a small team within the new ministry could be established to comb, semi regularly, through the Companies Register and Google, and red flag anything that looks dodgy or smells fishy and then probe them further, stripping them of their New Zealand company registration if good reason is found to do so? I mean doesn't a New Zealand company registering itself as Swiss Financial Corp sound dodgy to you?

And perhaps you also need to make it a little harder for people to register companies, because let's face it, the current process is like a piece of Swiss cheese only with holes big enough for one of Air New Zealand's Dreamliners to fly through, once they arrive in 2014. You may also want to consider that with a couple of articles like the Naked Capitalism one in higher profile publications we'll be a laughing stock, if we're not already in some quarters.

Because at the end of the day if New Zealand loses this good international reputation we have, as a small country at the bottom of the world, the damage could be irreparable.

Yours sincerely,

Gareth Vaughan

Banking & Finance Editor

Interest.co.nz

(Update adds details of First Capital Savings & Loan Ltd, including link to SEC charges).

This article was first published in our email for paid subscribers this morning. See here for more details and to subscribe.

8 Comments

Great piece Gareth. Maybe we can get MF Global to open up here.

But don't worry too much, the market will sort it out :-)

Hey GBH I see up there in that table you have been designated a "dodgy entity"

........ curses ! ...... they've rumbled me ........have I got time to activate some judicious shredding of several wine-box loads of superfluous documents ? ........

..... ahhh , purely in the interests of recycling ....... clean & green me ...... yup ..

Who the Sam Hill was it that set up the MED , in the first instance ? ....... and what actually do they do , in the real world , actually ...... Minister ?

NZers have suffered at the hands of this 'hands off' regulator for years. Here today, gone tomorrow, back the next with a name change... not to mention the complex structures so easily contrived. Is there any way to find out what the total number of currently registered companies and trusts we have on that register? That would be fascinating - and that's only one metric associated with that register that would be interesting.

Look what happens in the space of two days .. appears to be stupidity rather than hands off regulation

Here is a breath-taking (new) expose of the ACC. It's getting worse.

http://www.stuff.co.nz/national/health/6633165/ACC-tries-to-plug-another-breach

You need to read the finer detail of the article to see the cascading series of disasters.

And a construction company fixing leaky school buildings going broke

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=10794390

Can't the government do anything right.?

"Last year Power said the Reserve Bank believed about 1,000 shell companies incorporated in New Zealand over three years had been used to carry out banking activities free of regulatory oversight and "many" seemed to be undertaking fraudulent activities."

Here's an idea, let's make NZ a financial services hub? Easy as. I bet no one has thought of that.

FYI, I've added a paragraph on an NZ registered company accused by the SEC of running a US$21 million Ponzi Scheme, and a link to the SEC's complaint.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.