By Bernard Hickey

This chart courtesy of the Reserve Bank encapsulates the huge challenge New Zealand's economy faces over the next three years.

It shows how many houses would be built if the current targets from the Auckland Accord and the Canterbury rebuild were met in an 'unconstrained' scenario and the rest of the country carried on per usual.

It's worth unpacking what this means and how important it is because this forecast is central to everything in the economy and in politics through the middle of this decade.

The Reserve Bank would love for this extra housing supply to help offset some of the extra demand surging into the housing market from migration, population growth and record low interest rates.

Such a building boom would help them keep interest rates low for longer, and therefore take some of the pressure of the ever-rising currency, thus reducing some of the 'headwinds' it talks about for the export sector.

The economy would love it because it will help drive GDP growth at 3-4% per annum over the next half decade or so, putting us at or near the top of the growth league tables in the developed world.

The Government would love all of those things to happen -- slowing house price inflation, less unaffordable housing, low interest rates for longer and the strong economic, jobs and wages growth that would go with it.

Reserve Bank Governor Deputy Governor Grant Spencer was openly sceptical in his speech last month about how easy it would be to achieve the scenario pictured in this chart.

He worried rightly that all of this would be happening at the same time as a massive commercial rebuild in Canterbury and that the building level would need to be 9% higher than it ever got at the height of the 2003/04 building boom.

He said it was likely to create price pressures that could spill over into wider inflation.

The unspoken next step is of course that such inflation would force the bank to put up interest rates.

Aside from the sheer construction logistics of such an unprecedented house building boom being able to take place at the same time as the biggest commercial CBD build in our history, it's worth looking at the financial logistics.

The Reserve Bank is saying almost 100,000 new houses would be built in the next three years under the existing government plans. Including all the council funded infrastructure around them, this would cost about NZ$50 billion. So who will pay for them? How will they be funded? Can it be done without another household debt explosion? Will the Reserve Bank itself restrict credit in such a way as to stop the boom happening?

This is the conundrum at the heart of the economy right now: will the Reserve Bank allow another increase in household leverage to fund this building boom?

A slow start and a hiccup

This week's events in the building market and the banking system have shone some bright light on this conundrum for central bankers, politicians and home builders alike.

Thursday's building consent figures for September appeared to confirm a slowing of the consenting growth seen earlier in the year, just at a time when everyone was expecting it to be picking up going into the October 3 signing of the Auckland Housing Accord and a ramping up of building activity in Christchurch.

ASB economist Christina Leung said the slowing trend was a concern.

"There have been recent anecdotes from building companies that the restrictions on high-LVR lending, which took effect on the 1st October, are discouraging house-building demand," she said. "Building companies are reporting concerns amongst some households that if a top-up in mortgage borrowing is needed should unexpected additional building costs be incurred once the building project commenced, then there is the risk of the mortgage hitting the 80% LVR threshold and impacting projects.

Westpac Economist Michael Gordon said the consents in Auckland remained worryingly subdued. "While the number of consents in September was up 7% on the same time last year, the pace has slowed markedly in recent months," he said.

Then on Thursday BNZ CEO Andrew Thorburn told me BNZ had completely stopped issuing new approvals for high LVR loans. He said the conversion rates for the pre-approvals BNZ issued before the August 20 announcement of the high LVR limit were much higher than expected. This had forced BNZ to cancel about 150 approvals and stop issuing new ones altogether while the bank slowed its 'run rate' to meet the 10% limit for high LVR loans as a proportion of total average mortgage flow over the first six months. He also noted sub-80% lending was also slower than expected. ASB has also cancelled many more of its high LVR pre-approvals and Westpac has cancelled significantly less than a third of its high LVR pre-approvals. ANZ has yet to cancel pre-approvals.

On Wednesday home builder GJ Gardiner was reported in the NZ Herald as saying it had lost 24 deals to build new homes because of the speed limit. The Registered Master Builders Federation (RMBF) repeated that it expected the high LVR speed limit would reduce the number of new builds by about 15% or 3,000 in the first year.

RBNZ, Key more confident

The Reserve Bank itself and Prime Minister John Key are more confident the speed limit won't slow down new building much, or at all. Key flatly rejected the talk from the RMBF that it was affecting new building, pointing to a rise in weekly consents he was seeing from Auckland since October 1.

Governor Graeme Wheeler said in this Radio NZ interview broadcast on Monday that the bank didn't see a strong case yet for exempting loans for new builds from its speed limit. He pointed out that the sharp rise in the value of existing housing above the cost of new housing was making it more attractive to build. The bank itself estimated the limit could reduce consents by 60-80 or 2-5% a month.

Wheeler is not the only one pointing to the conventional theory that people will opt to build when it's cheaper than buying existing homes.

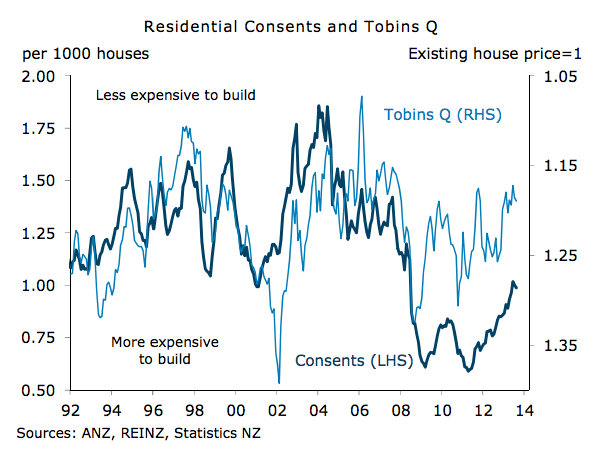

ANZ's economists produced this nifty chart showing the 'Tobins Q' -- the ratio between market price of an existing house and its replacement value -- and housing consents.

This would suggest we're about to experience a surge in building consents.

Ability to borrow?

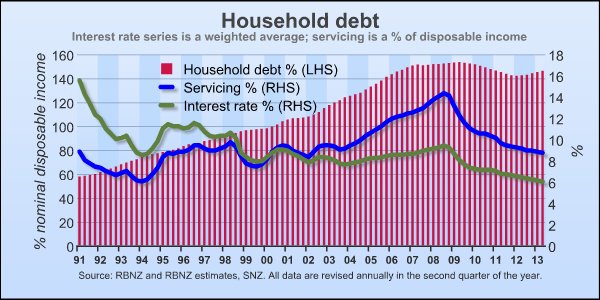

But there is one thing markedly different now than when we last saw a rise in the Tobins Q and building consents. Back in 2000-2002 New Zealand's household debt to disposable income ratio was around 100%. The subsequent borrowing binge through 2002 to 2007 increased that ratio to about 150% of disposable income, as this Reserve Bank chart shows. It fell a bit from 2008 to 2012, but has since started rising again.

The bank itself has warned repeatedly in recent months it's concerned about this renewed rise in household indebtedness. It's one of the justifications for its high LVR speed limit.

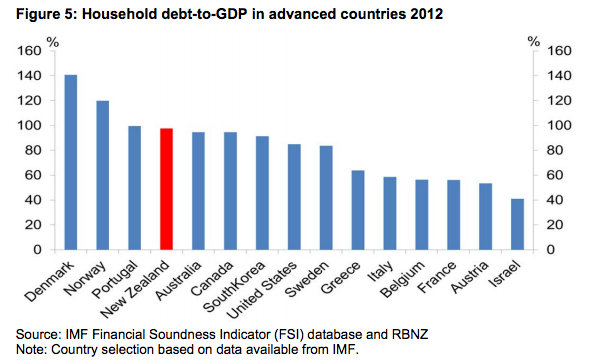

The bank's regulatory impact statement on the speed limit even has this excellent chart comparing New Zealand's household debt to GDP ratio with other countries.

It shows New Zealand's ratio sitting at just below 100% of GDP.

That's a problematic level, according to those who have studied the long term effects of indebtedness for countries, particularly household, corporate or government debt. The Bank for International Settlments (BIS) said in this 2010 study that household debt tends to drag on economic growth once it gets over 85% of GDP. New Zealand's is near 100%.

So it again begs the question: how will households fund this NZ$50 billion building boom in three years?

Not all debt

To be fair to the Government and the Reserve Bank, not all of that money will come from increased household debt. Perhaps a fifth of that will come from insurance payouts and perhaps the same again from various governments and corporate funds as local governments borrow, some developers borrow and some corporates invest their own equity.

Some will come from accumulated household savings. There is about NZ$120 billion stashed away in term deposits and another NZ$16 billion in KiwiSaver, some of which will be drawn down to take advantage of the Government's first home buyer subsidy of up to NZ$10,000 per couple.

Some of that NZ$50 billion will be able to come without increasing indebtedness as debt can grow in line with incomes, although at current growth rates that's about NZ$10 billion worth of growth over three years.

On that back of the envelope that leaves households about NZ$15 billion short of the NZ$50 billion they would need. To achieve the planned and hoped-for ramping up of house building the Reserve Bank is going to have to tolerate a further increase in an already dangerously high level of household indebtedness.

Or someone else is going to have to fund the building.

The Labour and Green Opposition are proposing that a good chunk of it come from the Government, which does have a much greater capacity to borrow, with its net debt currently well under 30% of GDP.

Your view?

(Corrected to make clear Grant Spencer is the Deputy Governor, not the Governor)

51 Comments

Kiwibank, Kiwiassure, Kiwihouse - watch this space !

Why not just buy one of the ghost cities in China - the homes are already there....

removes the development/construction risk...

Call it Kiwiland, part themeworld, part dairy centre

a little bigger than Hamilton, a little smaller than Christchurch...

.

I know, let's subcontract a Chinese company to build a few extra cities for us, we don't seem to be very good at it ourselves. This would have the following advantages:

No need to train people in old fashioned skills like housebuilding, they can learn hairdressing and game software development instead.

Lots of new houses. So we can bulldoze the old ones and put up high rises in their place where people can retire to.

We can get the Chinese government to lend us the money for no cost and no repayment.

What could possibly go wrong?

If .... we build this amount of new homes -- not a chance we dont havethe skilled craftsman and tradies to build what we need at the moment - Approached three builders in Auckland last month - two said sorry not even looking at pricing work till january the other said he might be abel to start late February!

thats before we get into the RMA issues - The level of debt wont be roadblock to the building - its a non issue - its the tradies that will limit the building

You're correct, there needs to be action to plug the gap; eg pre-manufactured homes from Canada (which the Japanese already buy like hot cakes); and migrant workers.

If the legal framework is there for "housing supply", the free market will make it happen. Entrepreneurs will make it happen.

I suggest NZ could play "housing catch-up" for years yet, and there would be a boost to the economy, affordable housing would attract Kiwis back, affordable land would attract businesses and create more employment.

An NZ economy modelled on Houston, which was about our population in year 2000, would be a really smart thing to have in this day and age. I see no reason we couldn't have a similar boom in population, construction, employment, and economic growth.

On the migrant worker issue I don't think it's necessary to import labour, because I understand that there's plenty of tradies in the provinces doin make-do work after they were cast off when the Federal Reserve/RBNZ hiked interest rates in 2007 and the big building companies abandoned their projects. They won't relocate until contractors can provide steady employment at fair wages. Subcontractors are stuck between the anvil of cheap local governments and hammer of major contractors who between them are the biggest employers and insist on driving down their wages as much as they can get away with. Is it any wonder wehave a chronic labour shortage where its needed most? Added to this is a flawed RBNZ which exacerbates the already cyclic nature of the construction industry's activity.Something that Wheeler's embrace of macroprudential controls is a tacit admission of.

So it again begs the question: how will households fund this NZ$50 billion building boom in three years?

Not all debt

To be fair to the Government and the Reserve Bank, not all of that money will come from increased household debt. Perhaps a fifth of that will come from insurance payouts and perhaps the same again from various governments and corporate funds as local governments borrow, some developers borrow and some corporates invest their own equity.

Some will come from accumulated household savings. There is about NZ$120 billion stashed away in term deposits and another NZ$16 billion in KiwiSaver, some of which will be drawn down to take advantage of the Government's first home buyer subsidy of up to NZ$10,000 per couple.

Pray tell which bank assets are currently servicing the interest rate demands of the term deposit liabilities? Exisiting mortgages - no? New foreign wholesale debt will be called upon to meet further borrowing needs in the immediate future given self financing growth is not a feature in abundance across the NZ economic landscape.

"self financing growth"

What a curious old fashioned concept. Why save when you can borrow and party, party, party? Sorry, I just can't tell if I'm being ironic or sarcastic.

Is it the Government's direct responsibility to find houses for it's citizens?

Perhaps we could bring Rob Muldoon back who would stop all foreign buyers of property other than those who have permanent residency, cap mortgage rates at 6%, govt purchase 1000s of sections, put the unemployed into building social housing, remove the "accommodation supplement" which distorts the housing market towards landlords, also one of Rob Mulddons greatest ideas was the Home Ownership bank account which got a lot of us into our first homes (dedicated account which had to be used for a house plus allowed a tax rebate each year of saving). Sorry - can't do, too interventionist.

Where are the "low cost" suburbs with new sections? This always used to be the starting ground for FHBs. Now it seems to be unacceptable to develop suburbs with cheap sections - noone wishes to risk their families there? OR is it commercially impossible? City councils could get cheap secions rolled out in greenfields developments as they used to.

The last bit of your comment, about the acceptability of developing suburbs with cheap sections, is where you hit the nail on the head.

THIS is why it is impossible to develop suburbs with cheap sections now:

http://www.nzherald.co.nz/anne-gibson/news/article.cfm?a_id=39&objectid=10887742

It would be a peice of piss to develop a suburb with cheap sections if Nick Smith had the cojones to rubber-stamp developments on farmland that some developer with a conscience had bought legally outside the UGB for $30,000 per acre.

http://www.productivity.govt.nz/sites/default/files/research-note-mar-13-auckland-mul.pdf

Sort the NIMBY's out. Neurotic Individuals malfeasant beguiling yackers.

Set Building consent costs. $1000.00 is about all the work should cost.

Read up on Hugh's advice - it will bring the final cost down.

If people see that the Government is serious about building people will show up to build.

Yet more socialising the costs but keeping the profits private, funny how the right / libertarian wingers are so happy as long as someone else pays. $1000? lol, clueless is all I can say. So what you are saying is in effect, get the existing rate payers to cough up the difference rather than the person who wants it. So little old ladies on a fixed pension pay more for a service a wage earner on far higher $s should pay for.

I odnt see that as fair myself.

So easy way to solve it though, or at least get a true/fair cost, open it to tender by private entities.

So The council would charge a flat fee for say 2 hours at the beginning to open a file and 2 hours work at the end to close the file and archive it. So make sure its a section that can be built on and that there is a registered private entity overseaing it all. At the end go through a check sheet to make sure the standards are crossed off and that the entity has a 10 year insurance policy in place.

Though note the last time I used the council and a structural engineer the private structural engineers inspection costs were $100 an hour V $85.

regards

Steven, you never, never, never, never, never learn, do you, no matter how many times it is spelled out to you.

What would happen if we put a $100,000 tax on new cars "to pay for the roads" instead of petrol taxes you pay as you go?

Suddenly all used cars would be something like $100,000 more expensive too, as a windfall gain to the existing owners of all of them, and everyone who bought their first car from then on would be paying the equivalent of the "road tax" even on a used car, only the money wouldn't be going towards roads.

Hopefully you don't have to have it spelled out how this also applies to houses, but at least I am sure everyone else following this discussion will "get it".

Our ancestors who opted for "pay as you go" were not fools. It is our generation that are. Not just fools, knaves as well.

NOW Mr Hickey decides to ask "how do we pay for these new houses and infrastructure"....!

I would ask him, where have you been all these years as young Kiwis have been taking on $50 billion of excess debt already, for NOTHING...???? Just a contribution to a Baby Boomers Benefit Ponzi scheme.

Very good post PB. I was reminded of the necessity when explaining anything to explain it like your telling a 5 year old.

You correctly identified a very key component of value-adding by bureaucracy to a product. Far too many people do not understand this. Our ancestors were certainly not foolish and knew the diffference between real positive value addition and negative value additions.

No, Its pretty obvious you are incapable of understanding I dont agree or will take on blind faith with your libertarian/right wing/austrian point of view which I regards as faulty logic or not downright lies to further your viewpoint at any cost.

I understand total cost of ownership, and that paradgym shifts have occured that make this discussion moot, obviously you do not.

regards

The system you describe has been legal since 1981. The last of the private certifiers quietly shut up shop after the 2004 amendments to the Building Act made it too expensive and risky for them.

Yep and thats the point Im trying to make. If it could truely be done for $1000 on a new house, of even $5k and a good profit they would be all over it, or at least cherry picking the nice easy ones aka ACC v private insurance.

They are not, instead the rate payer is left holding the risk for no gain.

regards

The only way to get the cost down is to revoke all the mandatory steps that the 2004 amendments added. No-one can get a consent to CCC stage for $1000 when there are 16 mandatory inspections. Doesn't matter who does it.

Agreed on all risk and no gain for councils which is why I continue to advocate taking building control out of councils and folding it into DBH. It's not like there has been any local control over building standards since 1981.

Kumbel - I think the question people need to ask is: Should Councils be making a profit on the services that they provide?

Councils costs:

Building inspection (labour component for site visits)

Cost of travel - vehicle including kilometers.

Office Administration costs including other Labour used.

Overheads.

BRANZ Levies.

How much profit is the Councl making off the Building consents process?

I cannot possibly support any type of profit from a bureaucracy that directly impacts upon housing prices or for that fact any other type of Goods and Services. These profit margins act like a subsidy.

Now Steven has written his usual BS and constantly confuses what costs are being Socialised. The fact of the matter is house prices are being increased to all existing owners by the Council charges that include a profit margin to the Council.

This is not correct. It is my expectation and I'll repeat it today, what Ive said over many months, my expectation is the costs are what are charged for with no profit.

So I dont agree a rate payer should subsidize a new build and I dont expect that a new build fee supports an existing ratepayer, that is nto fair in either case.

regards

In theory they would be in breach of Local Government Act 2002 150 (4) if they did make a profit (especially on purpose):

The fees prescribed under subsection (1) must not provide for the local authority to recover more than the reasonable costs incurred by the local authority for the matter for which the fee is charged.

Steven - the profit margin on Council charges is the problem. How much money is generated in profits from the new builds and is this how Councils are funding their obligations to the leaky building fiasco?

Hi, Do you have actial proof please?

Im not aware councils have a profit margin on consents, or at least my expectation is they should not. So if it costs $7500 to do a consent, well that is what they should be charging give or take a little.

Now if indeed they are charging $10k, or 15k then that is wrong and they should be slapped over it. This could and should happen on 2 levels. Councilors those who we vote in should be monitoring these costs and there should be a legal avenue for a 3rd party to challenge and see true costs in the last instance in court if needbe.

I have no idea on the leaky homes mess. Though note its the private entities / businesses that have run away from their moral if not legal obligations leaving the rate payer to fund the loss. Moral hazard that one, I'd just leave the leaky home owner and builder/supplier responsible, it was their work and decision.

regards

Sort the NIMBY's out. Neurotic Individuals malfeasant beguiling yackers.

Set Building consent costs. $1000.00 is about all the work should cost.

Read up on Hugh's advice - it will bring the final cost down.

If people see that the Government is serious about building people will show up to build.

They will do the wrong thing Hugh, its just an inevitability.

its going to collapse,' hit the wall', 'tip over',run aground.

http://thearchdruidreport.blogspot.fr/2011/01/onset-of-catabolic-collapse.html

Never ask an economissed.

Ask Kevin McCloud. At least he can build a career on the rise and rise of Grand Designs.

Ask yer Insurance Company and Bank if renting out is legal or folly. (Maybe they encourage it here).

Over priced Insurance to re-build, over priced houses. Nuff said.

Bernard,

As I have noted on this site for many years, the government can simply spend these new funds directly into circulation or even take an interest free loan from the RB (as the first Labour government did in 1936). The only requirement is that the money supply expansion be managed (i.e. private credit restricted as with the LVR restrictions).

I'm not sure we have the capacity to build that many houses but certainly funding should not be a major issue if the government builds the houses and then on-sells them. Alonsgide a major sorting out of the overpriced building supply chain and increased land availability, this should help to reduce new housing costs quite substantially.

Was Fletchers fortunes built on building State houses? I thought it was, The government did not actually build them- it paid firms like Fletchers to build them.

Government controls the process by funding it but anyone can do the actual building. The goal is to get scale and therefore cheaper build costs. It's open to competition and, from what I've heard over the last few years, there is no shortage of ideas on how to build better but cheaper.

See also:

http://www.thebubblebubble.com/

http://www.thebubblebubble.com/european-housing-bubble/

It always needs to be noted, though, that cities with elastic supply of housing do not have house price bubbles. Even if they are a minority and the vast majority are bubbling, they are still "holding out like a little Gaulish Village".

Great piece on China. The person interviewed is right on the money. China is reminding me more and more of Japan in the 1980s. It was Japan this, Japan that. Everyone said Japan was the future with all the business opportunities. You couldn't go wrong in Japan. I see the same claims about China today. I remember Japanese being major foreign investors in NZ back then, along with making up a huge chunk of the tourist numbers etc. China has followed the same pattern. It remains to be seen if they follow the same fate.........

We could follow the Oz example?

Australian dreams of prosperity were built on the wealth trinity – a good well-paying job, a nice house and comfortable retirement financed by superannuation. Unfortunately this has now become an illusion. Australians are now members of the ‘precariat’, the precariously employed proletariat.

Globalisation’s combination of off-shoring and relentless technological change has reduced job security and income for all but a select few. Housing was seen as an Australian birth right and retirement nest egg leading to massive over-investment in real estate. Now lower housing affordability and reliance on housing prices has undermined this pillar of the Australian prosperity.

As for superannuation, unrealistic expectations, poor returns and investment losses mean that the golden years of retirement funded by super have vanished. How did the great Australian dream come to this?

http://fodi.sydneyoperahouse.com/the-australian-dream-is-over

or as audio:

http://www.abc.net.au/radionational/programs/sundayextra/

(roll down toThe Australian Dream is Over)

Will impact CPI, will impact CPI. It's a bit obscure but the inevitable rise in contracting rates due to high pressure to develop flows through to rates via asset revaluations and depreciation charges. Whether you live in Karori or Kaitangata your rates will go up just because we are building quickly in Auckland and Christchurch regardless of what's happening locally.

What is the point of borrowing all this money overseas to build house s and infrastructure for a bunch of immigrants when most of our exports are created by a handful of farmers.

Chris-M see my comment at the end of this article. The trick is to be able to build houses as cheaply as possible so you don't have to go into so much debt, while having an economic model that allows you to diversify and expand your exports.

It is a trick that we clearly have not even begun to master, so why persist doing damage to our ecconomy until we know what we are doing?

The next generation of new-home buyers are going to borrow foreign cash anyway. Better that debt-money goes into the local economies making real things (houses), than funding the babyboomer's extravagant overseas holiday's (and the Banks' bottom lines).

And if we reinstate affordable housing, by cutting back on land inflation and false taxes, they won't need to borrow so much in the first place, of course.

You assume those savings get back totally to the buyer and not get retained by the developer/builder.

Since it seems the above have a great ability to get the last penny out of people Id suggest changing the system would do little more than add more profits to the above.

PS real things are not houses, think of it as an overhead not a good.

regards

Wish we could borrow foreign money for this kind of thing, there are rates in the sub 2% in the US

Yes it must be great to borrow at sub 2% rates.

Irecall watching an interview on Trackside with Lance O'sullivan our former top jockey and he said that when he borrowed to buy his first farm he got the money fom Germany.

This is what a lot of wealthy people do but it doesn't seem to be available to the common people.

error

The tax and rates must pay for all the infrustructure.

The funds well be reinbursed in time once poeple start buying the houses and paying rates.

Question is how do we reduce that infrastructure and cost of infrastructure. Those that make decisions on spending/implimenting have personal, professional and politicial interest in putting in as much infrastructure as they can.

Because of the economic structure in NZ that becomes very expensive so those buying houses and trying to pay rates find themselves with increasingly harder burden. And the hard burden of a landowner(landlord) by necessity gets passed to renters and those saving for a property of their own. Notice that few of those savers are old enough or economically or professional established enough to fit into the first paragraph decision makers..... Nor do they, as individuals, have capital or influence enough to disuade those decision makers (and often have poor education and end up demanding more infrastructure, thus making their own hurdles higher.)

This contrasts to what is required as any kind of enterprise start-up. An enterprise startup requires (1) establish a target market (2) research some possible solutions (3) generate demand (4) venture low levels of capital to build solutions (5) gain profits to grow enterprise (6) analyse effective solutions (7) reject those that aren't sustainable (8) repeat.

Many NZ operations and all central and local political organisations try to run the system backwards thus are very hit and miss. Which is why such a high failure rate exists in business...and why we have such high bailout costs covering central and local government problems.

Keep it simple Cowboy.

There never has been or well be cheap Infrastucture.

Economies of scale and competitive tendering well help.

The increase in the number of rate payers well devide the burden, reducing cost.

The checking process mentioned well help; polticians are controled by the voters (the majority?).

Business is ruled by profit. Borrowing has pushed property beyond what the majority can afford.

Government needs to step in and bring prices back in line and "reduce foriegn debt".

Government have done this many time with particular note the world wars, where there was no economic progress, just degrees of losing.

Taxing the rich for a while would help. Those whove done well out of the economy (those who own several houses and cars and make $300K plus a year) Either those who have made it themselves or inherited.

Having spent some years here in NZ and the UK doing "infrastructure" Id say you were very wrong. My experience is its usually hard to get the customer in NZ to pay for a solution that meets the needs or what they have asked for let alone make it bigger than needed. Also as a professional engineer its my job (or was) to show the customer their options ie different and cheaper methods or even an extra size allowance if I thought it was probably going to be needed, I'd then let the customer decide but under guidence. On top of that I often got the work by showing the customer that by employing me I could save them money.

Also consider that extra work you would benefit from in an upgrade, put in too big a pipe and, well there is no upgrade fees.

Now if you wanted to reduce the infrastructure needs www.earthship.com shows a fairly radical (by NZ standards) but well tested alternative. But many NZ customers just want another cheap and nasty MacMansion.

"sustainable" one over abused use of word IMHO.

Using recycled building materials -tyres and mud well definately bring down the cost of housing :) And why not - easy to add on an extension or even demolish.

Now all we need to do is bring down land costs to 100K for a 300m2 section.

And thats easy the Gov and Council can pay up front front infrustructure which can be paid back in time.

I like it - one gets sick of the our typical house design - bring back the Hippies!

Sound fair enough

"But there is one thing markedly different now than when we last saw a rise in the Tobins Q and building consents. Back in 2000-2002 New Zealand's household debt to disposable income ratio was around 100%. The subsequent borrowing binge through 2002 to 2007 increased that ratio to about 150% of disposable income, as this Reserve Bank chart shows. It fell a bit from 2008 to 2012, but has since started rising again."

This is the "elephant in the room" in my view. Either we all receive stratospheric wage increases to service the extra debt or there needs to be a correction in land values and construction costs. If neither of these, then stagnation will prevail.

One can rule out the wage increases. If that was the case Ethopia would be flush totday. No ones going to help those individuals who've dug themselves into hole.

Novice investors thinking that property is the be all and end all of all investment. Paying well beyond what the locals can afford is wrong for NZ going forward.

Its a necessity that the Government gaurantee affordable, quality housing in order for NZ Socioty-communities and economy to flourish in the right way.

The real estate industry bias geared to pushing prices up so individuals can walk away with maximum profit. Through selfish un ethical methods such as constraining supply and media "hyped gold rush stories.

Combine a cocktail of easy accesible money and lowest interest rates ever does not bode well.

The excessive cost of building, to house just a few.

But, it may keep the wolf from the door.

Over rated yes. Over blown, yes. Necessary, probably.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.