Today's Top 10 is a guest post from Shamubeel Eaqub, principal economist at the New Zealand Institute of Economic Research.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 10 yourself, contact gareth.vaughan@interest.co.nz.

See all previous Top 10s here.

1. Expensive but buy them anyway.

Stock markets are very expensive, but the quote from Robert Shiller neatly sums up the confusion.

...Shiller says, people are right to invest in U.S. stocks. “I’ve been talking down US stocks because of their high valuation, but I would invest something in US stocks,” says Shiller. “It’s been an amazing run and looks like something that can’t keep going indefinitely, but it might continue for several more years,” he says, adding that no one knows when it will end and it “might end very badly.”

In a CNBC interview, IIF suggests as the US Federal Reserve gets closer to raising rates, more emerging markets will face capital flight.

Investors withdrew $9.3 billion from emerging market funds in the week to June 11, according to funds tracker EPFR, the most since 2008 – the height of the global financial crisis. The bulk, or $7.1 billion, was pulled out of Chinese equity funds. Meanwhile, global emerging market funds saw $829 million of outflows and Latin America funds lost $442 million.

A combination of factors have led to heightened outflows, say analysts, including a stronger U.S. dollar, expensive valuations on emerging market assets and a rise in developed-government bond yields, which has dulled risk appetite.

3. A virtual tour of North Korea.

A really interesting piece of photojournalism on NY Times. It gives a fascinating look at the economy by omission. My favourite was:

“Pyongyang at dawn from across the Taedong River. Towering above the city is the 105-story Ryugyong Hotel, under construction since 1987.”

4. Why do we like the idea of owning a home?

Few people ask what is it about home ownership that is so important to our culture. An interesting piece in The Conversation by our cousins across the ditch is worth a read.

The appeal of owning a home seems deeply embedded in the psyche of Australians. Yet psychologically, it is not clear the home ownership dream is entirely rational. Achieving the dream may not be all we might have hoped, and chasing it may even do damage.

After discussing the pluses and minuses, the author closes with:

In any case, the walls and roof within which we live do not make the home. While we may justify our dreams with reasons, the truth of the home ownership dream is probably closer to the heart than the head.

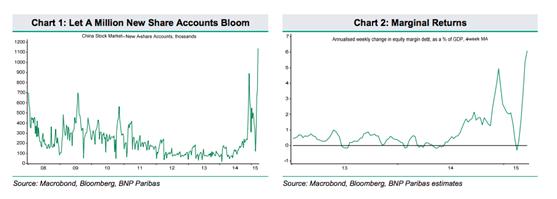

5. Betting on stocks for profits in China.

What could possibly go wrong when businesses are betting on the stock market to boost profits?

The WSJ reports that:

“Chinese companies are turning to an unlikely source for profits in the soft economy: the country’s red-hot stock markets.

Take Dong Jun, who earlier this year shut down his factory making lighting equipment and electrical wiring and let go some 100 workers. The 50-year-old comes to the plant in the eastern city of Yancheng almost daily, but spends his time trading stocks on behalf of his company, YanwuKeda Electric Co.

“Manufacturing is a very hard business these days,” said Mr. Dong, chairman of the company. “I want to make some money from the stock market and use the profits to restart my manufacturing business later, when the economy turns for the better.”

Two charts from BNP Paribus on FTAlpaville are staggering: a huge surge in new accounts and margin lending.

6. Time to talk about road pricing seriously.

The Australians are beginning the conversation on road pricing. It is fraught. But the status quo is unsustainable.

“The idea of motorists paying for the roads they use beyond tolls, fuel excise or registration fees has taken hold in Australia. A user-pays system might replace existing fees with charges based on motorists' actual use of roads. New technologies would allow charges to be applied at different rates during peak periods in the same way we pay for the use of telecommunications or electricity networks.”

“A user-pays system is necessary to reduce congestion on our roads and improve productivity into the future. We must have a debate over how, not if, we should implement a road user-pays system. But chances are political debates will send the user-pays idea down a rabbit hole before it even begins.”

Auckland needs to have the same conversation. Our congestion is bad and getting worse. The politics and ‘pub test’ will be roadblocks.

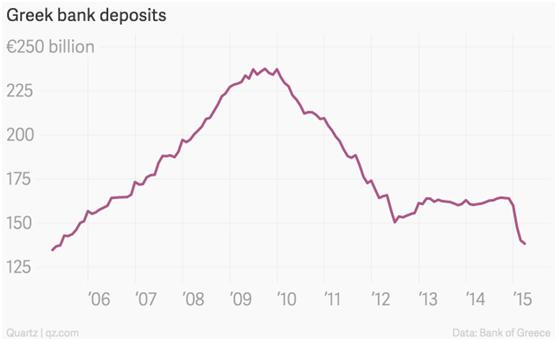

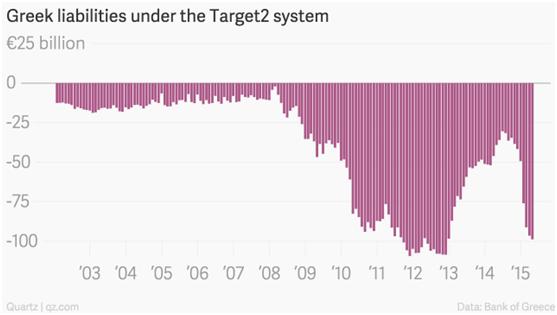

7. The Greek tragedy in two charts.

The Greek crisis continues to escalate. Quartz had a neat post looking at the two key charts to describe the Greek tragedy: bank deposits are fleeing (again) and the ECB (rest of Europe) is propping up the Greek banking system.

“Withdrawals have accelerated in recent months as people worry about the possibility that their euros could be re-denominated into rapidly depreciating drachma in the event that Greece has to exit the euro zone.”

“Greek banks have been constantly borrowing from the ECB.”

“And with time running out, the rhetoric running between the Greek government and its creditors suggests that once again Greece’s fate will be depend on the ability to agree to a last-minute deal.”

8. Should NZ borrow to invest?

A new IMF paper suggests NZ has lots of headroom for public debt. Should NZ capitalise on this headroom and borrow at current very low interest rates to fast-track projects that are already in the pipeline?

The critical paragraph for NZ is:

“Where countries retain ample fiscal space, governments should not pursue policies aimed at paying down the debt, instead allowing the debt ratio to decline through growth and “opportunistic” revenues, living with the debt otherwise.

The reason is that the deadweight loss associated with inherited public debt represents a sunk cost— so, abstracting from rollover risk, there is little purpose in paying it down by raising taxes or cutting productive government spending (of course if there is scope to cut unproductive spending this should be pursued).

Distorting your economy to deliberately pay down the debt only adds to the burden of the debt, rather than reducing it. When fiscal space is limited, incurring this cost is likely to be normatively desirable given the crisis-insurance benefit.

When space is ample—which cannot be established through some mechanical rule but will generally require judgments based on stress testing fiscal balance sheets to withstand extreme shocks—the distortive cost of paying down the debt is likely to exceed the crisis-insurance benefit.”

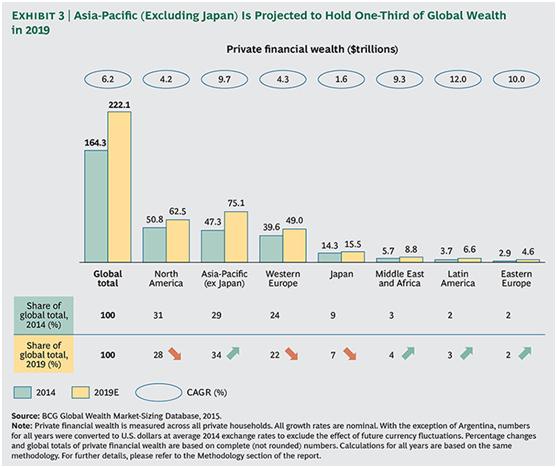

9. Asia is richer than Europe.

Strong performance by stocks has boosted wealth, and newly created wealth by entrepreneurs of mid sized companies, according to a study by BCG. As the region gets wealthier, they will be opportunities for our exports and tourism. They will also want to buy (some of) our assets.

The Economist Free exchange blogs;

“For the first time in modern history, Asia is now richer than Europe. And it is catching up with North America too; by 2019 the region’s wealth is expected to reach $75 trillion compared to $73 trillion in North America. And although America is still the country with by far the most millionaires in the world, of the 2m new millionaire households created last year 62% are from Asia-Pacific. China is the main driver here; it will account for 70% of Asia’s growth between now and 2019, predicts BCG, and by 2021 it will overtake America as the world’s wealthiest nation.”

There is always a but:

“But although Asia is now richer than Europe, individual Asians are not. Once wealth (including life and pension assets) is broken down per household a different picture emerges: whereas European households now have $220,000 in wealth and America’s $370,000, China still has a long way to go with its $72,000 (as does Asia-Pacific as a whole with $54,000). Convergence is certainly conditional.”

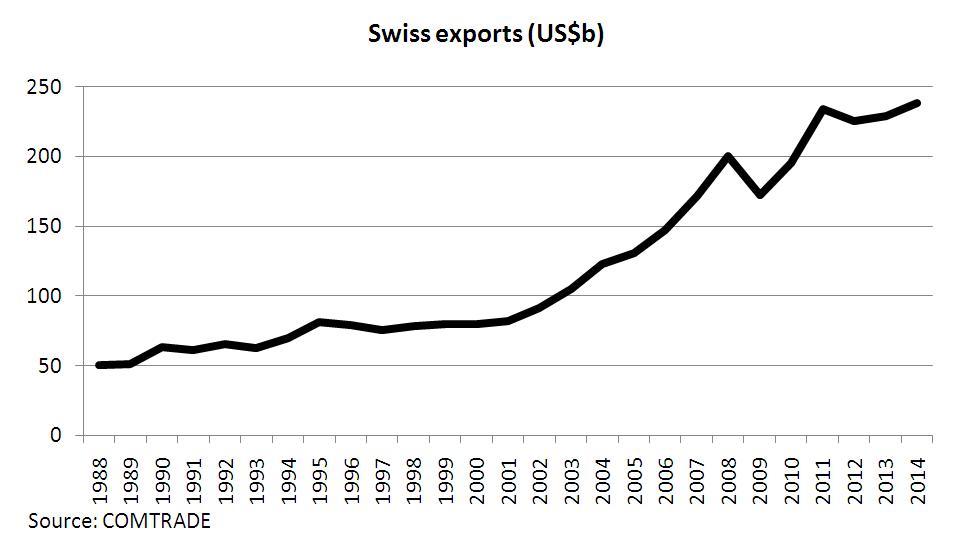

10. Strong franc doesn't dismay Swiss business leaders.

Swiss wages are high and the currency has been appreciating for a long period. Yet, its export sector has been remarkably resilient.

Der Spiegel draws parallels of the Swiss experience to Germany:

“Anyone who delves into the mysteries of the Swiss economy will soon stumble across a number of similarities to West Germany. Back in the days of the deutsche mark, when German companies were constantly struggling with its rising value, they optimized domestic production, made sure to avoid too steep a hike in wages and shifted parts of the manufacturing process abroad.”

They go on to talk about flexible labour markets, low unit labour costs and massive R&D. Some lessons for NZ perhaps.

34 Comments

#8 What's an 'opportunistic' revenue?

I have no idea, but I assume it can only be undemocratic and regressive in nature.

The underlying tenet of the IMF proposal involves covert default by advocating debt financing growth at a greater rate than the interest cost to do so.

From a macro view, a sovereign can inflate away the debt if the average interest rate on the debt falls below the growth in nominal GDP. (It doesn’t matter whether it’s volume growth or inflation driving GDP.) This is how the public-sector deleveraging after World War II was accomplished. Exhibit 3 shows that th eaverage interest rate on public debt in the US was below the nominal GDP growth rate. Read more

I thought the same and wondered whether they gave Greece this same advice around the year 2000.

I assume its tax by the back door, like increasing fees on say passports, user pays sort of thing? Demanding an un-realistic return from SOEs?

Another way of saying "opportunity cost" ?

No, of course it's not another way of saying "opportunity cost" and why anybody should think this remark witty or clever enough to earn an up-tick I cannot fathom.

An opportunity cost is income foregone as a result of not taking an opportunity. Thus, for example, suppose you inherit a Van Gogh painting. Would you be willing to sell it to me for $5? After all, it didn't cost you anything, so you'll make a whole $5 profit on the transaction.

The reason you probably won't agree to this (although I'd love to do business with you if you would) is that by selling it to me for $5 you miss out on the $several million that you could earn by selling on the art market. Even though you don't have any less actual money than you did before, you incur an opportunity cost.

Same goes if you don't sell it to me, but keep it on your wall instead. This is not a costless choice, it is a choice that involves foregoing the money you could make by selling it. That's an opportunity cost.

Whatever "opportunistic revenue" means, there is no way it can be read to mean anything like the same thing as an opportunity cost.

although I'd love to do business with you if you would

Hmmm - a character I had dealings with in a past life in London.

Well, I read the document - and here is the context of 'opportunistic' revenues:

... for countries that have ample fiscal space (clearly in the green zone), the benefit of reducing debt (by deliberately running overall surpluses) is unlikely to exceed the cost of the necessary

distortionary taxation.

In such cases, debt-to-GDP ratios should be reduced organically, through output growth, or

opportunistically, when less distortionary sources of revenue such as privatization receipts or

royalties are available. Within the confines of the formal model, there are two such sources of

short-run inelastic revenue: income from initial holdings of public debt and income from the

initial stock of private capital. Both of these sources will be inelastic in the short run, but highly

elastic in the longer run (because agents can choose to save less in the form of government

bonds or private capital when they expect the income to be taxed heavily).

Since there is no explicit tax on the income from government bonds here, the “taxation” takes

the form of very low—perhaps negative—real interest rates in the initial period. In a monetary

model with sticky prices, this could be achieved by cutting nominal interest rates—as indeed has

been the case in advanced economies since the global financial crisis where policy rates have

been at historic lows and have even flirted with the zero-bound. Within the confines of the “real”

model presented here, low real interest rates must be engineered by cutting taxes on the more

elastic tax base (labor), giving a fillip to output and consumption in the initial period, and thus

reducing the rate of return payable on the inherited debt.

A similar phenomenon occurs when there is the possibility of taxing capital income. In the initial

periods, when the capital stock is fixed (that is, before it depreciates), capital income is inelastic

and its taxation largely non-distortionary. Accordingly, the optimal fiscal program calls for heavy

taxation to reduce public debt. Very quickly, however, the private capital stock becomes highly

elastic (the anticipation of taxation will lead to lower investment) and the optimal tax rate on

capital falls to zero.14 In an economy with an initially inelastic source of revenue, the government

should opportunistically pay down some of the inherited debt; the greater the inherited debt, the

larger the amount paid down through such taxation.

Sorry about the formatting. Can anyone interpret this?

One just has to wonder who the intended victims would be in New Zealand, since 67% of NZDMO public debt is owned offshore and private bond issuance is not a hugely favoured source of business finance since savings are primarily directed to the residential mortgage market.

Why on earth would New Zealand borrow for infrastructure when it can print the money. Why pay interest to someone when you have the solution in your own hands. If you are frightened by inflation then increase taxes for incomes over, say, a $100K until it is paid back. That would not be necessary but it would satisfy those who are frightened about inflation.

um how about the Weimar Republic , https://en.wikipedia.org/wiki/Hyperinflation_in_the_Weimar_Republic

as to why not?

or can you explain why we wouldnt end up like Zimbabwe?

"pay it back"? if its paid back its not printing, its debt or "borrowing".

Why do you think hammering the ppl above $100k would stop inflation? proportionally they dont spend their income on goods in the CPI but invest 'excess" income which isnt then inflationary in terms of CPI or core inflation.

Just as an aside what you would do is hammer some single income family households with one good bread winner who's partner stays home with kids earning say $105k and not where both ppl were working say earning $90k each ie earning even more combined with no kids! How is this fair?

On top of that once we get inflation (assuming all else being equal for now) you would mercilessly hammer "well off" individuals to stop it.

You "idea" seems very confused, indeed ill thought out, punitive on those who wouldn't be responsible for the resulting outcome and are without any evidence of it even being workable!

steven, the Weimer Republic isn't a fair or relevant comparison to Patricia's proposal, because according to Hjalmar Schacht, the currency commissioner of the Weimer Republic and one of the founders of the Bretton Woods system and Bank of International Settlements (Central Bank of Central Banks), the Reichsbank (German Central Bank), was a public-private partnership between the private banking industry and the government during that period, which the Allied Powers, insisted be run according to free market principles. Not only the Central Bank, but private banks were allowed to issue public currency (notes and coins) in volumes, which drove the down value of the Reichmark against the dollar.

" The great German hyperinflation of 1922-23 is one of the most widely cited examples by those who insist that private bankers, not governments, should control the money system. What is practically unknown about that sordid affair is that it occurred under control of a privately owned and controlled central bank.

The Reichsbank had a form of private ownership, but with public control; the president and directors being officials of the German government, appointed by the emperor, for life. There was a sharing of the revenue of the central bank between the private shareholders and the government. Unfortunately, the League of Nations experts delegated to guide the economic recovery of Germany wanted a more free market orientation for the German central bank.9"

http://www.wintersonnenwende.com/scriptorium/english/archives/articles/…

In fact in the 1930s, the First Labour government deployed a highly successful programme of funding public infrastructure and housing, through direct, low interest credit from the Reserve Bank of New Zealand, with negligible inflation relative to that experienced by similarly structured economies of that period.

"The Government's opponents never tired of inquiring, “Where will the money come from?”; the Government's answers were never explicit, but in fact a good deal of the money came from State credit created by the Reserve Bank. This institution, by an Act of 1936, had become a fully governmental body; where these expensive programmes could not be financed out of current revenue or overseas funds, the Government simply borrowed from its own bank. Neither the housing programme nor the guaranteed price could have been financed without such credit. "

http://www.teara.govt.nz/en/1966/history-settlement-and-development/pag…

2 things, a) are you really saying patrica is talking sense? because I see nothing to justify her position.

b) I am not trying to change the system "the Weimer Republic" is in some ways a poor example on the other as a massive printing example its not bad. Labour in the 1930s borrowed? not printed? Lets also consider that the 1930s was a time of the Great depression with zero inflation or deflation and a broke country and I did try and hint at "all else being being equal".

Read the second with interest but I cant see how you read into it what I cant seem to see there, ie its a A4 page of generalisties, though positve ones.

For instance though " the long and losing battle against inflation from the war years into the peace" is of note.

and,

"Hard on the heels of the victory came tribulation. Thanks in part to public works construction 8><----- in part to the unsympathetic attitude shown by London financiers to some £16 million of debt shortly falling due, things looked ominous in 1939" Looks more like borrowing than printing to me.

Virtually every country which has experienced high inflation has had sanctions imposed against it. It is a shortage of goods that causes inflation. As only 3% of all money is created by the Government, the rest by the Banks, don't you think Steven that there is a lot of leeway. Steven, the current economic system does not work. I think that anything would be better than what we have now. Continually rejecting every alternative is really just being negative. There has to be a better way. What was achieved in this country from around 1935 to 1975 created a wonderful place where my parents and grandparents saw hope for their children and grandchildren. What is being done now and to our children and grandchildren is

nothing short of criminal.

You are raising quite separate issues here.

I dont understand your sanctions comment, context?

a) Shortage of goods doesnt create inflation in a complex large economy, as usually substitution can take

place as ppl have no more money to pay the extra, unless they also have more money.

Excess money certianly can except in the aero bound trap, and this is well documented/tested.

b) Banks create money as loans which when it is repaid disappears from the economy, ergo that isnt printing.

and no I dont think there is a lot of leeway. The UK Labour Govn's of the 1970s tried such an experiment,

it failed.

c) The current economy / financial system has worked until excessive deregulation allowed greed etc to take over which helped make it dis-functional. On top of that our globalised, industrial economy is based on a grow for ever model using cheap and abundant fossil energy, this is no longer the case and hence why its really

broken.

d) "negative" well any hodge podge of ill thought out ideas of "lets print" isnt a solution and indeed has been tried frequently enough with bad results that should be studied, not ignored.

e) 1935 to 1975 was done with debt, that broke NZ, so its un-sustainable.

f) children and grandchildren, simple, over-population is a significant part of the problem, previous generations simply had too many kids. we ae past peak oil, approaching peak minerals have climate change coming and that is all down to us as humans and we have inflicted this on our children and grand children.

blame yourself.

Good that the First Labour Govt's state credit creation is mentioned. If all resources are there for the work, inflation will not be created, ie labour and materials. they did it on a small scale in any event. The proof of this is the massive multi-trillion QE that has certainly not created systemic inflation apart from a few isolated asset bubbles.

#4 Owning a home? try these on for size; compulsory saving -generally the money one puts in is preserved while rent is a bottomless pit with little to offer, more control over living -less at the whim of some landlord who likely doesn't give a damn about what you can afford or if you consider the house you're renting is your home.

#6 Cost of roads - a good first step would be for the Government to make transport cmpanies pay their true fair share of the costs they create for those maintaining our infrastructure. Governments have successively and repeatedly refused to make truckies pay the full cost of their presence on the roads, yet they have passed legislation allowing the size of truck to increase, thus increasing the wear and tear and damage to roads. Roads in NZ are spec'd to accomodate the trucks, and most if not all the damage is done by them, but is is the common private vehicles and public who pay for them. If they did this Kiwi rail would become more competitive, private vehicle cost would significantly reduce, and climate impacts may be positively reduced.

#4 the standard befuddled reasoning that has given rise to the current irrationality. It completely omits all the costs associated with ownership which are, same as rent, tipped into the bottomless pit and do not contribute at all to "compulsory savings". By good the fortune of timing alone capital gain is all that makes your point viable. Imagine if capital gain was nil, then do your sums again and ponder on the result. Then factor in the opportunity cost of not investing your equity elsewhere and an honest person may begin to admit that ownership is just an emotional crutch, not a (not so) clever investment device.

Compulsory savings v paying rent in a zero capital gains environment - paying mortgage/rent and rates insurance etc if you are in your own home at the end of the day you still have your asset. Every time you pay an instalment on the mortgage you own a little more of it. Paying rent means you make those same payments and perhaps more in many instances for nothing more than a roof over your head for the next week! The sums are very simple when not clouded by the BS some "economists" apply. The average kiwi simply cannot put the money that they would put into a house into some other money making scheme to offset the downside of owning your own home. If that was the case the first home buyers would never buy a home after saving a deposit and realising that they can be safer not owning a home. While there are risks in owning a home they are far less than renting.

I will admit that the risks of buying in Auckland at the moment are significant, especially if the market collapses (and I hope it does, as it is madness at the moment) but if you choose to live almost anywhere else in the country the answer is obvious. Businesses should consider relocating out of Jaffaville as their employees would gain a significant improvement in lifestyle almost anywhere else, and the business would benefit from improve productivity, loyalty and lower costs.

That's a false dichotomy though. It's perfectly possible to save in ways other than buying property and paying mortages (and at the rate many pay their mortgages, it's not even a particularly efficient way of saving!)

If you do the calculations then it streangely can work out for your first house, mostly because it stop "leakage" due rent cost, and "locks in" the purchase price target. Otherwise you tend to find inflation usually increase prices (including houses) faster than you wages go up and certainly faster than most peoples' disposable income.

I am interest to hear you other proposals though.

The homeowner always wins long term. Because people are not perfectly rational, and will do anything to make their mortgage payment. Most salary/wage earners do not invest other than KiwiSaver or small term deposits.

Also investments outside of homeownership or KS can be clawed back - Sure you can topup the mortgage but most home owners people achieve a mortgage free home at the end (although recent article discusses more over 50s 60s with sizable mortgages.)

it would be interesting to see the stats there, most of the baby boomers I suspect were mortgage free by their 50's meaning they could put a little away to augment their pension. with todays level of mortgages either you will put off having kids or be paying late into your 50's or early 60's

Yes, a 65 yr old with a 300+k mortgage will be a growing phenomenon in future.

The other advantage for homeowners is: they can always sell and rent for a season.

The renter does not usually have the choice of immediately purchasing for a season unless they have considerable savings (difficult/unusual for a wage/salary earner).

" Government to make transport cmpanies pay their true fair share of the costs they create for those maintaining our infrastructure." Amen to that. Can it happen with this government? Don't hold you breath.

a good first step would be for the Government to make transport cmpanies pay their true fair share of the costs they create for those maintaining our infrastructure.

Road Transport operators might disagree with you.

While heavy trucks make up less than 2.5% of all the vehicles on the road, the RUCs they pay provide about 43% of the money needed to maintain the country’s roads, improve existing routes and build new ones.

http://www.rtfnz.co.nz/transport-facts/paying-for-roads

I'd estimate their contribution to road wear and tear at about 98% or more. Simple physics, wieght and dynamic loading and impact.

It doesn't really matter how you estimate it Bender.....if the trucking companies have to pay increases in RUC then they are all going to have to pass those costs on....so everything you buy will cost you more....just about everything that I can think of arrives on truck from somewhere....

Exactly.

Road damage increases in proportion to the 4th power of vehicle weight. In the case of many-wheeled heavy vehicles this effect is moderated somewhat by increased road contact footprint, but nevertheless it's hugely significant.

Exactly.

Road damage increases in proportion to the 4th power of vehicle weight. In the case of multi-wheel heavy vehicles the effect is moderated somewhat in comparison to cars because of road contact footprint, but nevertheless it's hugely significant.

The heavy trucks also only use a small portion of the roads.

But the small users do use petrol and do pay quite a large tax donation through that in GST and various levies and duty.

#6

Congested roads, record immigration, do you t hink there is any correlation? Well Duh!

Next we will be talking about congested schools, congested hospitals, congested courts - and we will all still be talking about it as the PM for Parnell rides off into the sunset with his work done here. Its all about supply - NOT!

#4. What an odd article. Because people 'preferred' the idea of owning where they, 'preferred' must be suspect in relation to some 'rational' decision. But what was supposedly rational was not explained.

There are lots of practical benefits to owning. 'Security' for example is a preference and a feeling but also practical. for example recall the multiple stories here on interest.co about multiple unwelcome relocations.

As for economics. Think of a low income tenant. Explain to me how is it cheaper to have the landlord organise somebody else to drive 15km to come in to change a tap washer. Rather than an owner occupier simply doing it.

#6 If technology allows us to charge individuals based on actual times and roads traveled, then we could also apply this to individuals on PT transport as well to increase efficiency?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.