By Bernard Hickey

Just imagine if more people saved more of their money, and all at the same time. And then imagine what would happen if at the same time hardly anyone invested in businesses or infrastructure that created new jobs or products or services.

It seems far fetched, but bear with me because a version of this is happening globally at the moment, and possibly for quite a while yet.

Firstly, spending on goods and services would fall as more money was put in the bank and a dangerous spiral lower in economic activity, business investment and employment would begin. Essentially, that is the story of how a recession starts.

Secondly, interest rates would fall as banks wouldn't need to keep interest rates high to bring in the deposits they needed and they would lower their lending rates to encourage investors to proceed with their plans.

Ultimately, that is how the market for savings and investment works. The 'price' of money shifts to a new lower equilibrium that allows savings to be matched with investment in such a way as to ensure all the resources in the economy are being used to their maximum potential to create goods and services.

That's been the theory about how financial and banking systems are supposed to work as an automatic stabiliser for an economy..

But many thinkers about global economics and finance are beginning to wonder if some deep-seated factors are skewing the way people are saving and investing in a way that is pushing interest rates ever lower and pushing the prices ever higher of the safest type of assets that generate regular cash returns.

It's called the global savings glut theory and it's been around since 2005 when US central banker Ben Bernanke started talking about it. The theory was that some types of savers, such as those in the Middle East and China, 'over-saved' and were pumping those savings into assets perceived to be safe such as US Treasury bonds. That in turn drove down long term interest rates and helped fuel the US housing boom of the mid-2000s. Back then the glut was caused by surplus cash from sky-rocketing oil prices and China's huge trade surpluses.

Things have moved on since then thanks to the Global Financial Crisis and the savings glut is now an entrenched feature of the financial landscape. The thinking has evolved to include the effects of ageing populations in Europe and North America, the effects of increased income and wealth inequality, the nervousness (still) that many savers have because of the 2008/09 crisis, and the surprisingly small amount of money businesses need to invest in new products and services.

Firstly, ageing savers become more conservative as they get closer to retirement. That means they're much more likely to put those savings into a bank or a bond than into a risky start up company or new venture. The 'pig in the python' of the baby boomers nearing retirement is pushing lots more money into term deposit accounts and Government bonds.

Secondly, when more income goes to the very wealthy they struggle to spend it all and they put it into banks and other low-risk assets such as property and bonds. The more unequal the spread of income, the bigger the 'dead' cashpile gets.

Thirdly, the world's biggest corporates are sitting on enormous cashpiles because they don't have to invest much to grow their businesses. Just five companies -- Apple, Google, Microsoft, Pfizer and Cisco -- are sitting on almost US$500 billion of cash earning virtually 0%. The top 50 US companies are sitting on over US$1.1 trillion. They don't need lots of money to build new factories or invest new technologies. All they need to do is employ a few smart coders to code a few apps and the 'profit' share of national income going to companies is higher than ever.

This glut is most pronounced in the Northern Hemisphere, but it's becoming more evident here. It seems counter-intuitive to say for a country with the sixth highest debt to disposable income ratios in the OECD, but some New Zealanders are saving much, much more.

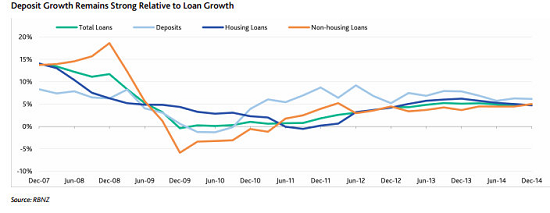

Reserve Bank figures show household term deposits have more than doubled to NZ$144 billion since the beginning of the financial crisis in 2007/08. The collapse of finance companies scared many savers into the arms of the banks, but the impending retirement of many baby boomers is also pumping up these savings.

Meanwhile, over the same time, bank lending to businesses in New Zealand has risen just 19% to NZ$85 billion and businesses have built up their own 'cash piles' in term deposits by 54% to NZ$73 billion.

All this has meant the banks have been flush with cash and have been able to reduce their term deposit rates, particularly after 2013 when the banks had 'filled up' their quotas for local savings to meet Reserve Bank requirements.

This is great news in many ways. New Zealand banks don't need to borrow so much from overseas to fund their lending in New Zealand. That has made our banks safer, although it has also helped make them much more profitable. Shareholders and the Reserve Bank are happy about that because some of those profits have been diverted into capital reserves, which gives the banks bigger buffers in the event of a downturn.

But this savings glut has also helped pump up the prices of assets seen as safer by older savers and dragged interest rates lower. That means property prices and the prices of shares that produce regular and high dividends are at record highs because more conservative savers want these types of assets and banks are keen to lend against these assets.

But will it last? These global trends of ageing population, more inequality, cheap technology and fear of riskier investments are not going away any time soon. Some associate this savings glut with 'secular stagnation', which is where global economic growth rates gradually slow to much lower levels for much longer.

Either way, it means these very low interest rates, 'low-flation', rising property prices and a drought of new business investment could be with us for a while yet and those expecting a natural rebound in interest rates may be scratching their heads for a while longer.

-----------------

A version of this article has also appeared in the Herald on Sunday. It is here with permission.

34 Comments

It's called the global savings glut theory and it's been around since 2005 when US central banker Ben Bernanke started talking about it. The theory was that some types of savers, such as those in the Middle East and China, 'over-saved' and were pumping those savings into assets perceived to be safe such as US Treasury bonds. That in turn drove down long term interest rates and helped fuel the US housing boom of the mid-2000s. Back then the glut was caused by surplus cash from sky-rocketing oil prices and China's huge trade surpluses.

God help me? I thought the Bank of England discredited this self serving nonsense once and for all last year.

"Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits" … "In normal times, the central bank does not fix the amount of money in circulation, nor is central bank money 'multiplied up' into more loans and deposits." Read more

In realty Chinese vendor USD export receipts which represented US resident debt fueled retail purchases were exchanged for unsterilised PBOC printed Yuan.

Quite right Stephen. An easy way to think of it is that savings deposits (credit) are the inevitable result of debt. You can't have debt rising at double digit rates for decades without a corresponding increase in deposits and this "money" cannot be spent away. That would just transfer the credit to someone else, usually overseas in NZs case. If the credit does contract the economy crashes.

We are trapped in a monetary system that will certainly collapse and the faster debt increases the sooner that will happen. Lovely!

The theory is sound - it just doesn't apply when the banks all work off leveraged (margin) borrowing anyway.

Banks have had to pad their nests a little thicker with the new regulations, so they've been soaking up "cash" holdings

And as you say, the TWI affecting global currency USD/Yuan/Euro is more of a factor than naked "glut" will ever be.

And the paradox is - lower interest rates make people save! The lower rates go, or are perceived to be going, the longer people will lock-in their term deposits for; tying up the cash in the glut ( if one believes there is such a thing!). What is the course of action in falling rate environment? Borrow short and lend long. Arguably, until interest rates rise the accumulation of saving, and hence less spending, will continue. Will that exacerbate the coming deflationary global environment? Yes! Lower interest rates are the problem, not the solution....

(PS: I suggest that the cost of money isn't going to be the problem, but access to it might be. "As Credit conditions begin to tighten more generally... perceived wealth will evaporate, M&A appeal will disappear and this bastion of Credit growth and spending will succumb to new realities."

http://tinyurl.com/pahuu2v

Nonetheless, one has to ask where is the NZ savings glut located given the RBNZ claims the book is matched?

A review of Gibson's Paradox might constitute a welcome diversion at this juncture.

A mistake made by central bankers is to believe that the price of money is its interest rate, instead of the reciprocal of the price of the products for which it is exchanged. Interest rates are money's time preference, which in free markets broadly reflects the average time preference of all the individual goods bought with money. The problem with monetarism is that it ignores this temporal aspect of exchange. Read more

The money people seem to be under the impression that they are the center of the universe on a steady state rock, and the word goes up or down around them.

The gibson shows that the future value, is Chaotic relationship, ie its future behaviour is derived not only from a function of what the market state will be in t+1, and t+2, periods in the future, but are also dependent on what factors were t-1, t-2,... ago.

eg what our commitments/contracts were two quarters ago, affects what our behaves will be in two periods from now.

AND it's not just one line of price that sets the market behaviour, it's not a two-body model. Availability of labour and consequential wage (it takes time for a specialist population to migrate to value jobs). Cost of oil and gold , which are dependent on sentiment and very much tied to forward contracts and options give extra constraint lines on the graph of "interest vs spending"

yes, there is no "glut". Just not so many people borrowing even at _momentarily_ low interest rates. That means _investment_ money is finding few homes, as people look at the revenue they'll get from expansion and see a poor forecast. Better to delevrage (ie "save") and not borrow (ie "save") which leaves investors (ie "savers") in a bit of a spot..... which given the media report shows us who is driving politicians and media... the people between the "savers" and the "borrowers".

I think we will look back and wish there was even more of a savings/investment glut as most of the recent investment in NZ (dairy related) has been fundamentally wasted.

In dairy there are 2 main distinct markets, domestic liquid milk and international powder. As we know from the supermarkets the former is not very volatile. In most other countries the domestic market is 95% of the business which is why farmers in those countries are not under so much stress. They have a reliable income from liquid milk to fall back on.

In NZ it is the other way round 95% of the market is powder. We can't survive an extended period of low powder prices or risk being forced out of the business. So even though we may be the lowest cost producer at any time our business mix is fundamentally fragile. At some point, even if it isn't this time, there will be an extended period of low prices and the majority of dairy farmers will be forced out.

Fonterra and the Government should have identified this market dynamic and managed the risk by limiting the amount of powder we produce. However, because of short term greed we have encouraged farmers to borrow and invest in prodigious amounts. All wasted.

(David Stockman) "There's no reversing the artificially inflated bubbles created by the Federal Reserve. I think what we are seeing is the beginning evidence that the central bank-driven credit economy is over and we are in a new era. It's a huge disaster waiting to happen... the world economy, including the U.S., is heading into what is clearly going to be an epochal deflation to the likes of what we have never experienced in modern time."

http://www.cnbc.com/2015/08/07/stocks-are-a-disaster-waiting-to-happen-…

Fortunately, readers seem to have tired of the relentless conspiracy theories and apocalyptic world view of Daniel Ivandjiiski ("Tyler Durden") at ZeroHedge. Moving on to a new prophet in the even worse David Stockman is not a good move folks. Nor Lee Adler (WallStreet Examiner). These views rarely contribute to understanding. Basically they are trying to sell gold or a return to the Gold Standard and a mythical stable point back in history. They kind of support the second part of the fools' thesis " ... fool some of the people all of the time ..."

Fortunately, readers seem to have tired of the relentless conspiracy theories and apocalyptic world view of Daniel Ivandjiiski ("Tyler Durden") at ZeroHedge.

Nonetheless, the irrefutable concentration of factual content contained within this site is second to none.You would do well to match the quality of global wholesale money basics.

There is a difference between data and opinions. The former is indeed a fact, the latter is fantasy. So while I agree the data/facts they un-earth can be good, what they write about them is rubbish, yet IMHO you seem to not differentiate the 2.

While I mostly agree I do think they highlight the data quite well, its just their straight jacketed, hyper-inflationista Austrian fantasy that gets a bit wearing to read.

What amazes me is that after 8 years they still are selling the same old same old script of how they think the economy will end ie Govn incompetence has brought us to this and not private greed.

Steven - I cant believe you said

"What amazes me is that after 8 years they still are selling the same old same old script of how they think the economy will end"

You have been doing exactly the same with your "Peek Oil"

So there. Consider yourselves chastised (by Chaston).

Sorry David, can't agree, I read the "even worse" David Stockman regularly. Well written with some juicy exposure of some of the appalling behaviour that goes on in the world of finance. Haven't heard a peep in the MSM on Goldman Sachs theft of Billions from the Danish people and hiring of their former PM and their head of Nato to help sweep it under the carpet. We need to know this stuff.

http://davidstockmanscontracorner.com/the-danes-and-the-vampire-squid-h…

His warnings on excess credit growth, asset bubbles and deflation appear to be the coming reality; a check of his writings might just turn out to be a very smart choice.

Examples of derivatives’ potential to cause far-wider economic harm

went further than LTCM. The problem, as always, came with bets

more or less recklessly placed against the unexpected, those positions

swollen with buckets of debt. Things went bad for LTCM when Russia

defaulted on its sovereign debt repayments, triggering a market slide

that left LTCM’s positions deep under water. Another version of the

unexpected struck the gold market in September 1999, when European

central banks announced plans to coordinate sales of their reserves.

The news put an immediate floor under gold prices, making bets on

further falls suddenly far riskier than previously. At the same time, the

central banks curbed their physical gold lending, a critical part of the

derivatives merry-go-round, making the placing of bets much pricier.

So far so straightforward: central banks had changed their reserves

policy, reversing downward price pressures just as many miners and

other gold fans had begged them to do for years.

The problem, which took a few days to emerge, was that the ensuing

price spike ripped the heart from the Ashanti Goldfields Corporation,

one of Ghana’s most valuable hard-currency assets. The mining house,

20 percent owned by the Ghana government, was listed in London,

New York and Accra. It was the continent’s biggest gold producer

outside South Africa, its Obuasi mine in Ghana boasting proven and

Fraudcast News

98

probable gold reserves of around 20 million ounces. It also held gold

exploration properties in Tanzania, Guinea, Mali, Niger, Senegal,

Zimbabwe, Eritrea and Ethiopia.52

Gold prices surging from $269 into the $320s an ounce within the

trading week should have delighted any mine management, or so you’d

have thought. Not so for Ashanti, whose chief executive Sam Jonah

later admitted only to “recklessness” in the extent of the bets his

company had placed on falling gold prices. Not content with simply

hedging prices a few months ahead to insure current operating costs,

Ashanti had turned from being mainly a miner to an out-and-out gold

speculator. Jonah’s company looked like it would sink under a mound

of gold-based derivatives turned toxic by the price reverse. Had its 17

bank counterparties called in the $270 million in cash they were due as

guarantees on failed bets totalling $570 million, it certainly would have

done. But as those banks knew only too well, forcing Ashanti to pay

out on its bets would have fired gold prices through the roof. The

miner would have had to buy the physical gold required to close out its

positions, endangering other miners with similar positions and

probably some bankers and hedge funds in the process.53

It was echoes of LTCM once more albeit in a different country and a

different part of the global financial system. The banks involved again

got to call a market “time out” to limit the spread of damage from

deals they themselves had arranged. Goldman Sachs was once more in

the thick of it directly, on both sides of the Ashanti rescue in fact and

in advisory relationships with central banks involved in the pact that

sparked the price spike.

Goldman was not only the corporate adviser to Ashanti. It was also the

mine company’s biggest hedge counterparty thanks to contracts written

by its commodity arm J. Aron, a trader on Goldman’s account. So the

investment bank earned fees advising Ashanti on its massive

speculative hedge, in commission from selling the miner a stack of

toxic derivatives and from profits made trading the market. Banks

operate so-called “Chinese Walls” separating potentially conflicting

Fear and greed correspondent

99

activities. It beggars belief that all those interests could have been kept

apart, not least given the market turmoil.54

Goldman profited once more from being a major beneficiary of the

rescue it led. The operation landed the bank and its fellow

counterparties the rights to the equivalent of Ashanti shares worth

$4.75 apiece, less than half their value just days earlier. In return for

potentially owning 15% of Ashanti, the banks granted the mining

house a three-year waiver on calling in their right to cash deposits. It

was expensive insurance for Ashanti given that by the time the deal

was struck gold was back at $292 an ounce, meaning no cash deposits

would have been due under its existing arrangements.

Once the dust settled, questions remained about how Goldman’s

commodities arm had traded the market for the duration and what

information its traders had known when. Not least of them was a

heavy trade Aron made on October 5, before the waiver was agreed.56

The rotten smell didn’t spread far given the story’s complexity and the

gold market’s niche status. Ashanti counterparties all got a share of the

carve up, with Goldman getting bumper servings despite having given

the company such awful advice. Far more important for the market

was that the rescuers had quietly defused a potential rocket under gold

prices. That might have proved disastrous for their own derivatives

positions, either directly or through additional counterparty risks from

other clients who’d also bet on lower prices. Goldman reportedly kept

the Bank of England, the supposed bullion market regulator, up to

speed on the Ashanti rescue. That would suggest the regulator wasn’t

much bothered by the investment bank’s multiple roles. You could

almost imagine their nods and winks that client pillage and market

manipulation were dandy, just as long as it was done in an orderly and

discreet fashion.

Goldman and the other counterparty banks came out on top, as did

Sam Jonah. Ashanti’s minority shareholders were well and truly

mugged while ordinary Ghanaians lost a great chunk of their national

wealth. Holders of physical gold, having sat through years of falling

Fraudcast News

100

prices caused by derivatives-driven sales, also lost out on higher prices.

The sorry tale concluded in 2004 when AngloGold bought Ashanti for

the equivalent of $1.4 billion, or $10.89 per Ashanti share, down from

an all-time peak more than double that.57

Jonah joined AngloGold’s board, his lawyers eventually settling out of

court a US class action accusing him of deceiving investors over the

state of Ashanti’s hedging. The $15 million settlement filing listed the

hurdles, potential costs and risks of failure in the way of securing

anything more substantial. That pitiful sum, just $0.15 per share

equivalent after legal and administration costs, was more than other

minority holders got, not to mention ordinary Ghanaians.58

David C i think you should not call people "Conspiracy Theorist". In doing so you are showing a side of you that is one of a "Bully"

Conspiracy Theorist

A contemptuous term used primarily by the main stream media to slander anyone who questions their monopoly on truth.

Even though he has done his own research and has concluded that the official account of events is either lacking or inaccurate, he is still a conspiracy theorist because he does not believe what the main stream media proclaims to be the truth.

by TruthWaves July 31, 2009

Anyone who has a different opinion can be called a "Conspiracy Theorist" and is a term used for the sole purpose of discrediting a person with an alternative opinion, rather that explaing where, why or how the alternative opinion is wrong.

The term is used by people who are resorting to bully tacktics to further their own view. And as we all know a bully is a person with a personality disorder.

Well I agree with DC, having read a few of the articles frankly yes "Conspiracy Theorist" about sums up the quality of the opinion / rant coming from Zerohedge and Stockman's corner just to name 2. ie its always the Govn's fault, not the greedies making money by damaging or even destroying the system and then whine when their returns dont meet their expectations, but no its always the Govn..

.

Interesting article there from David Stockman BW.

Here's my take on it.... there has been quite a bit of discussion on the internet as to whether the world will head into deflation (due to saturated debt levels) or whether it will head into hyper-inflation (due to world-wide money printing).

What is apparent is this, the more money is printed, the more money there is and that money needs to find a home. Its a worldwide phenomonen. Inactive money means low interest rates. If there was less money around, interest rates would be higher.

Technology also has a part to play as effeciencies are naturally deflationary and that is a good form of deflation.

So how has the money entered NZ? Bank borrowing to inflate housing is a big one - easy lines of credit. John Key's $60Billion govt borrowing is another. Wow I can't believe he has done that and the media haven't challenged him on that, and the voters don't care cause it doesn't impact on them "today". And then there is the inflow of money from overseas investment and immigration.

The key equation is: The value of Money = the value of resources in the real economy.

Another theory banded about the internet is: 97% of all money is funded from Debt.

Therefore, in a deflationary environment, debt becomes more burdensome and encourages a cash is king approach - money outside the financial system.

At this point in time I see a strange paradox myself... an increasing world money supply and deflation. This is possibly a strong precursor of a worldwide crash caused by falling demand which in itself is caused by oversaturated debt levels.

Therefore, assuming this crash does happen, what is likely to happen? More money printing US style worldwide to sure up the financial system? that in itself can go on forever but the end result must mean a fall in the value of each single dollar's purchasing power as every new dollar is printed.

The symptom of what we have now is because the crash should have been allowed to happen 7 years ago and allow the reset of the financial system. Until the system does reset, we will likely have continued deflation followed by more money printing.

the productive economy is what will decay in this process, more job will go and more and more govts will default.

I think the whole money go-round will continue on for a while yet until you start to see a wave of governments default on their debt and then the music will stop and the reset will finally happen.

The whole system needs to be rehaulled. A system where money is created only through debt is a system designed to fail.

Look at american history - they have not always had the federal reserve - they have had very successful times where money was printed by the govt, free of debt. John F Kennedy would have returned to that policy if he had not been assassinated first.

If you create 1 dollar debt free and you spend it on 1 dollar of new infrastructure, you create 1 dollar of new value which does not rob value from all the other dollars in the money supply.

Such an approach could do wonders for the canterbury rebuild? The secret is not to get greedy as govts do and print too much that then causes inflationary pressures.

The result of the current situation is that someone else has already printed that money and they want interest on it and so it robs us all of interest on our own dollars, while at the same time pushing up the value of the one thing we must have for security - a home which you own.

What is wrong which govt printing money to "build a new house/" If it is done in such large volumes, economies of scale is reached and the per unit cost should actually fall.

Thats my take on it, in the mean time I will hope that the crash does come so i can buy a "cheaper" house which I can call home without having to be in debt for 30yrs to a bank

"an increasing world money supply and deflation"

a) try Keynes for that explanation.

b) Consider the effect of energy in our globalised, industrialised economy.

The outcome of lack of energy will be a shrinking global economy and it will do so from now until its done, the only Q is how fast is it going to be. Welcome the Greatest Depression, aka the 1930s on Steroids.

and if the govt was to print its own money to build houses, it could sell them or mortgage them out to those that can not afford to buy a house, in effect acting like a bank. When the money is repaid, it is theoretically removed from the money supply and hence the whole process of inject and remove money from the money supply should not be inflationary while at the same time adding true value and a higher standard of living for those that need quality housing - insulated and warm - imagine the flow on effects to the health system - less sickness

Does that mean that by Government printing money there will be an automatic move against the exchange rate which will discourage overseas buying of farms / houses /businesses as the buyers will then know they will be selling later into a depreciated dollar?

Bring it on.

This govt wants no part of such thinking or policy. Sell the assets, not build more of them, especially state houses. "For the common good" is anathema to them.

The problem is it wont be removed. The biggest predictor of inflation is ppls expectation of it. On the other hand 10year Govn bonds are in the 3~4% range so we can borrow extremely cheaply and that will be removed.

you can't tell me the banks don't create it out of thin air. this is why we are in the situation we are in... worldwide too.... and who ends up with the asset when you can't pay them the interest on the money they didnt have to begin with??? But you would rather stick with the current failed system would you? Look at american history and you will see it HAS succeeded in the past. Not completely a stupid greenie policy and the right wing neo-fascists would have you believe

They don't need lots of money to build new factories or invest new technologies. All they need to do is employ a few smart coders to code a few apps and the 'profit' share of national income going to companies is higher than ever.

Interesting. Not to mention 3D printing and other disruptive technologies that will reduce the number of future workers required.

I predict that in the near future, outsourcing to 2nd and 3rd world countries will be too 'expensive'. No point in paying an Indian call centre when you can have a basically free local A.I call centre.

The next 20 years is going to be very exciting. For some people.

This article is very interesting...

http://www.theguardian.com/business/2015/aug/01/fears-for-chinese-econo…

in particular is this quote...

{Quote} "But to the extent that Chinese policymakers are forced to dip into their foreign currency war chest to support growth – and particularly if a less export-oriented growth strategy means that it stops racking up the vast trade surpluses that have helped it to accumulate these huge reserves – the ripples will be felt in markets around the world. Simon Derrick, head of market strategy at investment firm BNY Mellon, says there are signs that is already happening. He says reserves have already been trimmed by about 7.5%, from just under $4tn at the end of June 2014, to $3.69tn by the end of June this year. Along with other emerging economies that piled up reserves to avoid a repeat of the late 1990s Asian financial crisis, China’s massive buying power in debt markets was one of the pressures keeping interest rates low across the developed world in the runup to 2008. Derrick believes this shift away from accumulating new reserves could have contributed to the drift upwards in US bond yields, and the downward pressure on a slew of currencies in recent months, including the euro, and the Canadian and Australian dollars. “Suddenly, you don’t have the same support that you’ve had for the past 15 years, which is why you’ve seen so much volatility,” he says. And as the Fed prepares the ground for a rate rise, Derrick argues that the absence of Chinese buying power in financial markets could mean the impact of that decision is amplified, with borrowing costs rising steeply in the US and emerging markets. “If there is to be a move higher in interest rates across the board, maybe it will be sharper than perhaps you might have expected maybe five years ago.” Other countries have ample low-cost labour ready to move into manufacturing as Chinese real wages rise, so it may be through higher borrowing costs, rather than a dearth of cheap toys or T-shirts, where the west will feel the impact of China’s changing economy most keenly." {End Quote}

Note the word "believes"

Yes Debt bubble not savings glut.

This is why interest rates are driving to zero and below just to boost the lending.

Does anyone know what will happen when negative interest rates kick in around the world will this be the end of money or just the end of cash?

huh? cash is king in deflation its buys more and in effect its tax free income (well not GST free), the only Q is how long before the Govn devalues and prints new notes making your stash worthless.

If you look at the war chests of major US corps they are sitting on huge piles of $s and not spending, why? because no one is buying. So yes its a debt bubble not a savings glut.

"It's called the global savings glut theory and it's been around since 2005 when US central banker Ben Bernanke started talking about it."

Hmm its cover well along with a lot of other 'modern ' theory' etc in a Text book by Stewart and Mc Farlane from around the early 70s.. and from memory they even refer way further back than that.

I believe they where Kiwi Professors out of NZ universities

steven I agree - the point of all my posts really - a debt bubble.

This so called savings glut is only there because the money was printed.

World demand is falling off a cliff because people cant afford to take on more debt to "inflate" GDP further.

Its insanity to think banks have the real financial power to create money out of thin air and then charge interest for it. Governments should have that right and no-one else.

It is actually possible to design a financial system where each dollar is not backed by an equal dollar debt creation. Under that system money "serves" the people instead of the current system where people are enslaved by debt. Modern slavery.

Unfortunately, my purist thoughts will never occur. Maybe it will if a reset happens but I doubt that too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.