By Alan Shields*

The fight over 'main-bank' customers is heating up as lenders try to eke out every possible advantage over their rivals. Now the battleground is clearer: statistics show if a bank can acquire and retain customers in their mid-20s and 30s it will undoubtedly win the main-bank war.

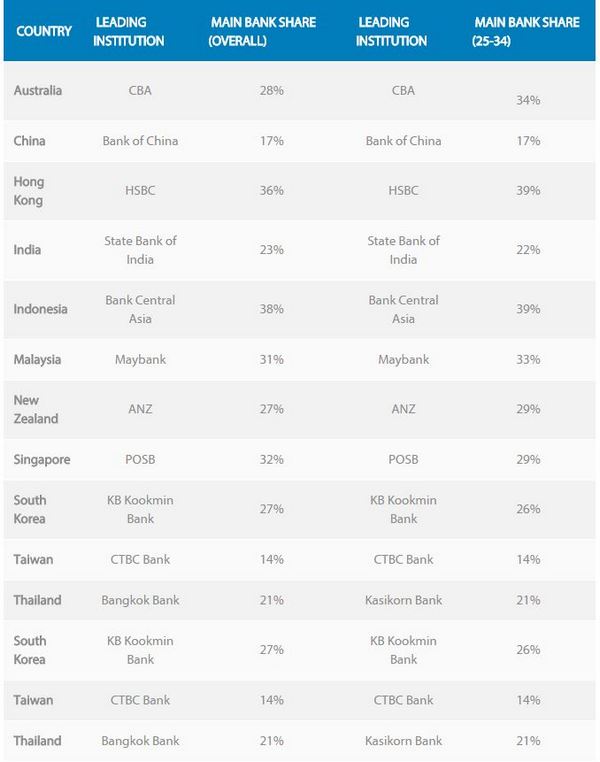

An RFi Group study on Global Retail Banking shows banks with the largest share of the 25 to 34 age segment are, in every country studied, the banks which end up having the largest main bank share of the whole market.

Customers describe their 'main bank' as their most important financial institution and on average hold more products and have longer relationships than non-main bank customers.

From a total sample of over 40,000 consumer interviews globally, the report took into account the opinions of 22,000 banking customers from 11 APAC markets – Australia, China, Hong Kong, India, Indonesia, Korea, Malaysia, New Zealand, Singapore, Taiwan, and Thailand.

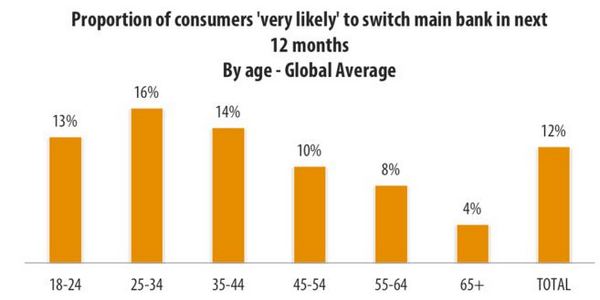

In past studies RFi has always been fascinated by the fact almost nobody across the globe switches their main bank after the age of 34 – in fact, around the world, more than 90% of all main bank switchers do so before they reach the age of 35.

The reasons behind this often lies in life stage changes such as buying/moving home, moving/starting work and getting into or out of a relationship, all of which in turn often require a rethink of banking arrangements.

So from a main bank perspective, this (18 to 34 years) is an absolutely critical time for both acquisition, but perhaps importantly, retention and it is on the latter that we would like to focus.

This switching is reflected in both past switching behaviour and in future switching intent. Likelihood to switch main bank accelerates and peaks in the 25 to 34 segment globally and it is in this age group that proactive retention should therefore be focused.

In fact, 16% of 25 to 34 year olds globally are very likely to switch their main bank in the next 12 months, compared to an average switching intention of 12%.

In addition, across the Asian markets, very few of the large incumbent banks have been able to increase their share of the 25 to 34 segment in recent years. Three notable exceptions to this have been ANZ and CBA in the Australian market and HSBC in the Hong Kong market.

In the case of these three banks, success has been driven by a combination of specific acquisition campaigns focussed on the younger demographic segments, a focus on customer experience and importantly, a focus on digital engagement.

Get digital

Indeed, in attempting to retain the 25 to 34 segment, the importance of digital engagement should not be underestimated.

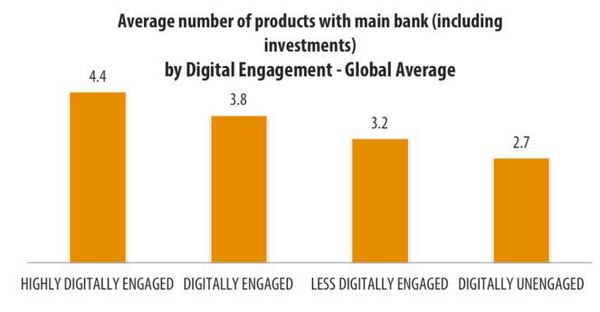

RFi Group found that this age group was the most likely to be 'highly digitally engaged' (determined by using mobile or tablet banking more than once a week) and that if they could be kept engaged, then they offered enormous opportunity for main bank product cross-sell.

In fact, a highly digitally engaged consumer has 4.4 unique products with their main bank, compared to just 2.7 for a non-digitally engaged consumer.

The caveat on this digital engagement is that highly digitally engaged consumers are the least sticky of all customers despite their increased product holdings.

Indeed, any bank looking to drive digital engagement needs to understand that once they embark on the initiative, they must continuously adapt and improve their digital proposition so as not to fall behind the competition.

---------------------------------------------

*Alan Shields is managing director of RFi Advisory. This article first appeared on ANZ's BlueNotes website here and is used with permission.

5 Comments

What about the marketing technique of offering free overdrafts to tertiary students, then once they graduate then charge them 20% interest? This helps 'lock-in' the customer, as they defer paying off the overdraft in their early career and stay as a customer.

I can but assume that this would peeve a customer enough to make them leave, but if all banks do it then I guess it doesnt matter.

Perhaps if banks offered new graduates with a package that reduced their overdraft costs, consolidated debt, & maybe even dealt with/consolidated their student loan debt, & gave advice for their financial future. Student loans must be having a huge drag effect on the economy generally, & delaying household formation etc.

When I look at my kids in their 20s, student debt, consumer debt, cost of city living - they are 10 years behind being able to buy a house or get their heads above water.

I had one of these and they are quite a good trap, a lot of students have them, I used mine for travel. However you get a year out of Uni interest free to pay it back, which I just managed, but I know a lot of people who still have them and those people haven't switched banks...

almost nobody switches their main bank after 34? Because they only do it at key life events. Isn't buying your first home a key life event when someone will switch banks to get the best offer?

The idea that most people will have bought their own home by 34 is rather wishful with current 10/1 price/income medians in auckland, and the rest of that country ain't exactly cheap.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.