Over the last 150 years or so, numerous innovations have radically changed the way people live. You can tick off the list: electricity, the automobile, refrigeration, television, the Internet. Yet one innovation rarely makes those lists, even though it is just as significant if not more so: retirement.

The idea that people can stop working in their fifties or sixties and then enjoy 20+ years of relative leisure is actually quite new. For most of human history, the vast majority of people worked as long as they were physically able to – and died soon after. Retirement is possible now only because those other 20th-century innovations accelerated the division of labor and lifted us out of subsistence farming and living.

Our inventions often have a dark side that can come to haunt us. They may be applied to wage war… or to create reality TV. Are we going over to the dark side with retirement? Maybe not, but we’re certainly heading in that direction. And there’s nothing wrong with the idea of retirement, of course – the concept is a fabulous invention, helping to extend life and happiness.

But retirement is made possible by a prior life of hard work and careful saving and investment. And the very funds that make retirement possible are dependent on growth of the economy. Without growth, retirement as we have come to know and love it will not work. Retirement will still be possible, of course – just not under the same conditions.

The zero interest rate and now negative interest rate policies of our central banks are gumming up the global retirement machinery. The Federal Reserve and other central banks have spent so many years subsidizing debt and punishing savings that it is now extremely difficult to guarantee future income streams at a reasonable present cost. And future income streams are the very heart and soul of retirement. Without adequate future income streams, retirement as we know it today is off the table.

Whether this sad fact is what the central bankers intended or not, it is indeed a fact, whether you are an individual saver or a trillion-dollar pension fund. Today we’ll examine how we have come to this unhappy point.

When Retirement Was risk-free

Saving money for retirement has never been easy for the average worker, but at least it was feasible if you started early and earned a middle-class living, especially if you had automatic deposits or a business or government guaranteeing you a pension. Plus, the bond market was on your side. Until the year 2000 or so, anyone could lock in risk-free 5% or higher yields in bank certificates of deposit.

Suppose you saved all through your career and accumulated a million dollars. It was a simple matter to put it all in CDs, Treasury bonds, or tax-free muni bonds and generate $50,000 a year in current income. Living costs were lower last century, too. Presumably, you also paid off your mortgage in the course of living the American Dream. Add in Social Security and you could enjoy a comfortable if not extravagant retirement. Your million-dollar principal would remain intact and could go to your children upon your death.

Again, this was relatively easy to do. It didn’t require any financial sophistication or even a brokerage account. The hardest part was saving the million dollars in the first place, but you could get by with much less if you drew down the principal over a 20 or 30-year period (and didn’t outlive the drawdown).

Better yet, you could do this with no risk, just by keeping your money in FDIC-insured banks. You might have to split it between a few different banks to stay within the limits. Some extra paperwork, but easily done. There were plenty of services that would help you distribute your assets over multiple FDIC-insured banks.

It was even simpler if you had an employer or union pension plan to do the work for you. Pension plans pooled people’s money, calculated how much cash they would need to pay benefits in future years, and built portfolios (mainly bonds) to match the liability projections. Government and corporate bonds yielded enough to make the process feasible.

Younger readers may think I just described a fantasy world. I assure you, it was very much a reality not so long ago. Ask your grandparents if you don’t believe me. However, you may find them in a state of shock today because they thought the fantasy would last forever. Indeed, their financial planner probably told them they could count on drawing down 5% of their portfolio per year to live on, because the income from the investments in their portfolio would more than make up for the drawdown.

None of this is possible today. Neither you nor a massive pension plan acting on your behalf can generate enough risk-free income to assure you a comfortable retirement.

Why not? Because our monetary overlords decreed that it should be so. Retirees and their pensions are being sacrificed for what now passes as “the greater good.” Because these very compassionate overlords understand that the most important prerequisite for successful future retirements is economic growth. And they think that an easy monetary environment is the necessary fertilizer for that growth. So, when they dropped rates to zero some years ago, they believed they would soon be able to raise them again – and get people’s retirements back on track – without risking future economic growth. The engine of growth would fire back up, and everything would return to normal.

So much for the brilliant plan. You and I, the expendable foot soldiers in the war to reignite growth, now gaze about, shell-shocked, as the economic battlefield morphs from the Plains of ZIRP to the Valley of NIRP.

Ultra-low rates

In fairness to our central banks, they must balance competing priorities. The Fed’s statutory mandate is to promote “maximum employment and stable prices.” Their primary tools to execute this mandate are the manipulation of the money supply and interest rates. Since 2008 they relied on near-zero interest rates to stimulate economic growth. As I wrote last week, the Fed (and much of the economics profession) sincerely believes that low interest rates will do the job they’re supposed to.

However, the hard evidence of the past few years is that ultra-low rates, combined with quantitative easing, haven’t stimulated much growth. Unemployment has fallen, which is good – but probably not as good as the numbers suggest, because people have gone back to work for lower pay and are now even deeper in debt. Personal income growth has stagnated, as we will see a little later in this letter. So, are we better off now than we were five years ago? The answer is a qualified yes.

But it is not entirely clear, at least to your humble analyst, that the halting economic recovery is the result of low interest rates and not other less manipulable factors such as entrepreneurial initiative and good old muddling through. In fact, an ultra-easy monetary policy may be part of the reason we’ve been stuck with low growth. Witness Japan and Europe. Just saying…

Seriously, no one fully understands how all the moving parts influence each other. Years of ZIRP did help businesses and consumers reduce their debt burdens. ZIRP and multiple rounds of QE have also done wonders for stock prices … but not much for the kind of business expansion that creates jobs and GDP growth.

If year upon year of ultra-low rates were enough to create an economic boom, Japan would be the world’s strongest economy right now. It obviously isn’t – which says something about ZIRP’s efficacy as a stimulus tool.

What isn’t a mystery, however, is that ZIRP has created a massive problem for retirement savers and pension fund managers. NIRP will make their problem worse – and they were already facing other challenges as well.

If we (the US) get negative interest rates for a sustained period, similar to Japan and Europe, it will be because the economy is stuck at no-growth or in contraction. Stock prices will head the other direction: down. It will be the mother of all bear markets. We are getting a little taste of it right now in bank stocks. Look for much worse as the growing impact of NIRP and the threat of NIRP reaches other sectors.

Defined failure

Employer-based retirement plans come in two flavors: defined benefit and defined contribution. A defined-benefit plan is what we usually think of as a pension. You work for employer X, who promises to let you retire at age 60 or 65 with a defined monthly pension payment – so many dollars per month, based on your salary, years of service, etc. You and your employer pay for this plan by contributing cash to it during your working years. (Unless you work for a government entity like a police force or fire department and can retire in your early 40s with full benefits after 20 years, then go to work for another government entity and retire with a second and sometimes even a third defined-benefit retirement plan. Yes, there are numerous instances of this. Not a bad gig if you can get it.)

But will the amount you and your employer contributed be enough to pay that defined benefit for all the years you survive after retirement? The answer necessarily involves guesswork and assumptions about events 20 or 30 years in the future. It also means someone has to be on the hook in case the guesswork is wrong. That’s usually the employer … or taxpayers.

Private-sector employers realized decades ago that carrying pension liabilities on their balance sheets left them at a competitive disadvantage. They removed those liabilities by switching newer workers to defined-contribution plans – the now-familiar 401(k) and similar programs. You and (if you’re lucky) your employer both deposit cash into your 401(k) account. You decide how to invest the money and hopefully do well. More to the point, a defined-contribution plan does not require your employer be on the hook for poor investment results. The one on the hook is you.

Defined-benefit plans now exist mainly in state and local governments, where unionized workers have more influence over management and elected leaders come and go. Politicians, by their nature, often think no further ahead than the next election. Their path of least resistance is to promise workers the moon and let their successors figure out how to pay for it.

Guess what? The future is here, and it turns out the guesswork and assumptions about the future were really, really bad. As in, if you are just about to retire or have only been retired a few years and have a pension, you may be seriously screwed.

Hot potato pensions

I get a creepy déjà vu feeling every time I write about public pensions. I’ve been preaching about them for more than a decade now, and the situation keeps getting worse. Obviously the politicians are ignoring me – and not without reason. Clearly, I underestimated their ability to postpone the inevitable. Nevertheless, I firmly believe a train wreck is coming. The math has never worked well, and now ZIRP/NIRP is making it much worse.

Fixed-income markets are tailor-made for funding future liabilities. Suppose you sign a contract in which you agree to pay your supplier $1 million exactly one year from now. How do you make sure you will have the cash on hand when the time comes?

The most conservative way would be to put $1 million in a lockbox right now, with instructions to open the box and disburse payment on the agreed date.

Back when CD and Treasury bill rates were 5%, you could just buy a series of $100,000 CDs for $1 million. When the time came, you handed over the principal and kept the interest accrued. You covered your obligation and still had $50,000 to use however you wanted.

That is roughly how defined-benefit pensions used to work, with longer time spans and much larger numbers. My example also has an advantage they don’t: certainty on how much cash you will need at maturity and the exact amount the investment will make in the meantime.

A pension plan that covers thousands of retirees can make educated guesstimates as to how long those pensioners will live. Professional actuaries are uncannily good at this when the population is large enough.

The far bigger challenge is to determine the expected rate of return on the pension’s assets.

That number is a hot potato, because it determines how much cash the employer must contribute each year to keep the plan “fully funded.” The laws require the sponsor of a pension plan to maintain a fully funded position. However, they allow a great deal of flexibility in how “fully funded” is defined. Assume higher returns in the future and you can get away with spending less money in the present. Furthermore, because we are dealing with large numbers over long time spans, small changes can make a huge difference.

The state and local officials responsible for these plans want to assume higher returns so they don’t have to raise taxes or cut other spending. So, as politicians often do, they shop around for someone who will give them the answer they want – along with plausible deniability should that answer turn out to be wrong. This is why we have a thriving “pension consultant” industry.

Almost without exception, public pension plans still assume very optimistic future returns. They base those projections on long-run past performance and assume the future will be like the past. CALPERS, the California public employee plan that is the nation’s largest pension, is in the process of reducing its base forecast from 7.75% to 7.5%. Even this tiny change was enormously controversial. Revenue-challenged local officials all over the state looked at the difference it made in their mandatory contributions and flipped out.

I have talked to numerous board members on multiple enormous public pension boards. Many of them would privately like to reduce their projected returns, but they know it is politically impossible to do so. Other simply say, This is what my consultants tell me, so I have to go with their expert opinion, don’t I?”

The return assumptions are a blend of past stock and bond market returns. This is where ZIRP starts to hurt. Bond returns have the advantage of being more predictable than stock returns, but now they are predictably low. Inflation-adjusted returns on Treasury and investment-grade corporate bonds are either zero, below zero, or not far above zero. They are certainly nowhere near the 5% or more that was once common.

If you can’t assume decent bond returns, can you make up the difference with higher stock returns? That’s not easy, either. Today’s behemoth pension funds don’t simply invest in the stock market; to a large extent, they are the stock market. It is mathematically impossible for all or even most of them to achieve above-market returns. They are just too big.

As I often say, long-run stock market returns are a function of economic, population, and productivity growth. Some companies always outperform others; but in the aggregate, stocks can’t outpace the economy in which they operate. If the economy grows slowly, then over the long run stock values will, too.

Growing slowly is exactly what the entire developed world has been doing and appears set to continue doing for years to come. If 2% is the best GDP growth we can hope for, then we are not going to see stock market returns over the next 20 to 30 years at anywhere near the 8% or 10% that many pension trustees assume.

If investment returns aren’t sufficient for pensions to pay the benefits they promised, all the consequences are bad. State and local governments must then implement some combination of higher taxes, spending cuts, or benefit reductions. All three hurt.

The same reality applied if you’re running your own pension. If you don’t save enough and/or fail to achieve your expected returns, you will face some unpleasant choices: work longer, live more frugally, or die sooner.

From frying pan to fire

If ZIRP is bad, NIRP will be far worse for retirement planning. Bond-return assumptions will have to be even lower and potentially below zero. This situation would wreak havoc on every pension fund – but that’s not even the worst part.

Most asset allocations are generally in the ballpark of 60% equities and 40% bonds, so that is the standard portfolio we will be discussing. Other allocations will make some differences but not change the general direction. In other words, “your mileage may vary” – but probably not by much.

In an ideal world – which is the world that pension consultants live in – equities will return 10% nominal, and bonds will return 5%. A 60/40 portfolio blend will then yield an 8% overall return after fees, expenses, and management costs.

It doesn’t require a great deal of head scratching to realize that a negative interest rate environment is going to bring overall bond yields down below 2%. That paltry yield will drop the blended portfolio rate to 1.2%. How long can that low return last? Ask Japan. When we saw the advent of zero interest rates in the US seven years ago, no one thought they would be in place this long. No one.

The reality is that in our mega-debt world, long-term interest rates are going to be low for quite some time. One thing that could change that would be inflation’s charging back against consensus expectations. I don’t think the Fed really makes much of a move until inflation is over 3%. FOMC members would actually like to see 3% inflation for a while, though they will never say that. But then at some point they will have to make a move, and that is going to be exceedingly uncomfortable whenever it happens. But for the nonce, we are in a low interest rate environment.

Phantom stock market

Maybe we could just allocate more to equities? That is one possible solution, but the historical record suggests that might make our task even more challenging! When I start thinking about future possible returns, one of the first phone calls I make is to my friend Ed Easterling of Crestmont Research. He and I have collaborated on numerous papers on market cycles and future returns, most recently “It’s Not Over Until the Fat Lady Goes on a P/E Diet.” His website is a cornucopia of data and analysis. Let’s look at a few of his charts and conclusions.

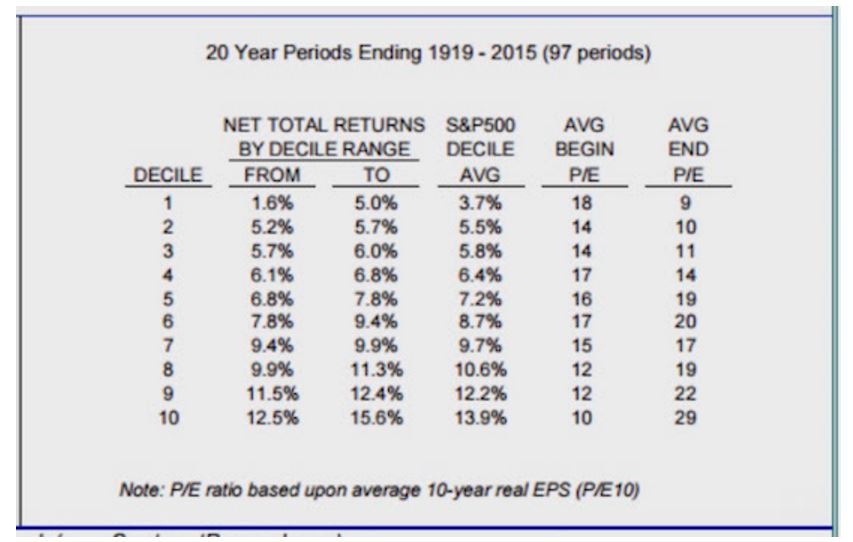

One of the more reliable predictors of future returns is the current price-to-earnings (P/E) level. There are only three sources of stock market growth: EPS growth, dividend yield, and the change in P/E ratios (http://www.crestmontresearch.com/docs/Stock-Waiting-For-Avg.pdf). Where you start from gives you an excellent indication of the range of returns you can expect to get over the following 20 years. For most people, 20 years can be considered the long run.

Today the normalized P/E ratio is 23, which is right up there in the top 10% of historical rankings. Even if you want to quibble and drop the ratio a few notches, it’s still high. And by looking at the chart below, we find that historical returns 20 years on have ranged from 1.6% to 5.0%, with an average of 3.7%.

There is no historical instance of price-to-earnings multiples expanding from where we are today for any sustained length of time. In fact, levels like those we see today have generally indicated a brewing storm – a bear market. That doesn’t mean something new can’t happen this time. There are those who argue that because interest rates are so low, we can expect earnings multiples to continue to rise. Maybe, but for how long and how by how much?

If you take the highest historical return of 5% (from our current P/E) and marry that with the bond returns we discussed earlier, you find your 60/40 portfolio can now be expected to give you 4.2%. And the average historical equities return of 3.7% leaves you with only a 3.5% total return on your investment portfolio!

And the return level makes a huge difference to the eventual success of a pension. As in, a monster difference. Most people don’t realize that most of the money their pension will pay them in 20 or 30 years will come from the growth of the portfolio and not from their actual contributions. As we will see, your contributions might actually amount to as little as 20 or 25% of the total portfolio 20 years from now.

I’m going to start with a modest number, but you can add zeros to your heart’s content. Let’s say you save $1,000 a year for the next 30 years. Your pension consultant tells you that you can make 8%. And if you actually do, you find you have paid in $30,000, but your account has grown to $123,345.87, or over four times your contributions. Not a bad day at the office. You stick that into a 5% CD (bear in mind that we’re talking a fantasy outcome here), and you make $6,000 a year, or about $500 a month. Add a zero and save $10,000 a year for 30 years, and now you’re earning $5,000 a month, which, with a paid-for home and Social Security, provides you a comfortable, if somewhat frugal, lifestyle.

But what if you get only a 6% total return? Well, now you only have $84,801.68 after 30 years. Your 5% CD gets you only $4,000 a year. If you were able to save $10,000 a year, your monthly income would be roughly $3,500. Not bad, but much tighter. But that outcome depends on your being able to get 5% on your bonds or CDs. Do you want to bet your future that interest rates are going to be that much higher in 20 years? Maybe you need to save more.

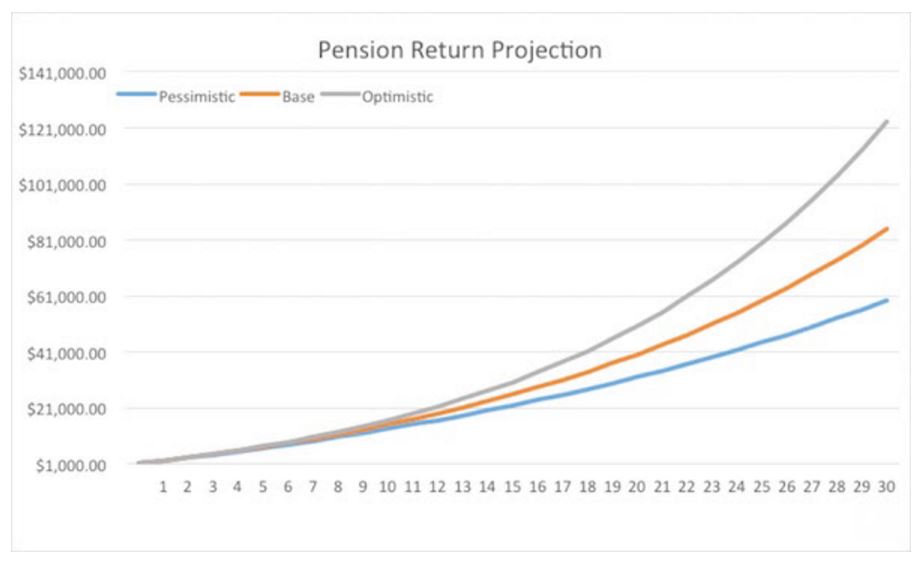

Let’s turn to a little graph that my associate Patrick Watson whipped up for me in Excel. The top, gray line represents the 8% scenario; the middle, orange line is the 6% scenario; and the lower, blue line is the more pessimistic (but maybe realistic) 4% return.

What does that 4% return look like 30 years down the road? Your $30,000 in contributions have not even doubled, leaving you with just $59,328.34. That’s right, you don’t even get a double. And in our far distant future, that 5% CD is only going to give you $250 a month. Or if you save $10,000 a year for 30 years, you’ll be living on $2,500 a month.

But these numbers assume you don’t have to deal with that pesky inflation thing. A mere 2% inflation will guarantee that your money will be cut by about half after 30 years. (So even that $5,000 a month if you really make 8% won’t turn out to be that much of a lifestyle. And God forbid you make only 4%.)

Unicorn CDs

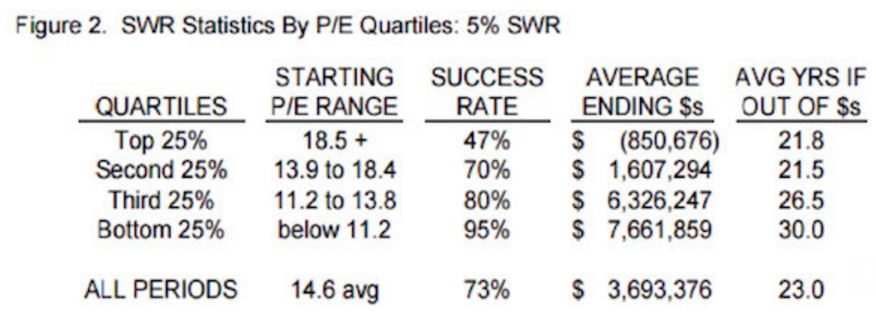

Well, that’s okay, many financial planners will say. You just dip into your principal, and when the market turns around you make it back up. I can’t tell you how many financial plans I’ve seen that assume the safe withdrawal rate (SWR) is 5%. As the table below (from one of Ed’s essays) demonstrates, a 5% withdrawal rate has historically (as in, since 1900) only been safe 47% of the time, and on average you are out of money after 21 years. Hardly safe!

The only way you can be “safe” is to find that magical 5% CD of the future when you’re ready to retire. If the world then happens to look like it does now, though, you’ll just have to keep right on working until things somehow magically recover. I hope that never happens to you, because you could find that your work experience is no longer relevant in an increasingly rapidly changing future.

I also wouldn’t assume that 30 years is a reasonable additional lifespan starting from age 65. With the advances being made in medicine and biotech, your “healthspan” as well as your lifespan are going to increase, and we are going to see many people live well into their hundreds. I think people would be well advised to plan to live a great deal longer than their parents and grandparents did and to budget for retirement accordingly. For most people that means continuing to work. If the thought of working an extra five years at your current job is somehow unpleasant, then my suggestion is that you switch jobs as soon as you can and find something you can tolerate for the longer term.

The same numbers that we applied to individual returns also apply to pension funds. Pension funds are going to wake up in 10 or 15 years, find they are massively underfunded, and look to taxpayers and businesses to re-fund them. Your corporate pension plan that is guaranteed by the Pension Benefit Guarantee Corporation is not as guaranteed as you might think. If the PBGC has to take over your fund, you may be lucky to get 50% of the promised benefits. Before you get too fat and happy, I would read the fine print on that guarantee. Then I would ask the pension plan management exactly what expected return they are planning to get; and when you hear the typical “7½% for the long run (blah blah blah),” start trying to figure out how to work well past your expected retirement age so that you can supplement your pension when it fails.

Then again, maybe your corporation will be there in 20 years when you need it. No need to worry – just assume it will all work out. Everybody else plans that way, and they all tell you everything’s going to be fine – just ask your brother-in-law.

Let’s step away from the unrestrained sarcasm to sum up the facts: Long before 20 years have passed and sometime after the onset of the next bear market, reality will set in, and pension fund managers will begin to plead for increased funding. And that is going to cause all sorts of repercussions. For a government plan, to obtain the needed funds, either taxes will have to go up, or other services and government expenditures will get cut. Either way, it appears that voters are in no mood to tolerate the status quo today. Imagine how much more fractious they’ll be in 20 years, when it’s clear that most people’s pensions are down the drain.

Governmental bubbles

The biggest bubble in the world is the one we live in without being able to see it. It’s the bubble of government promises that government will not be able to fulfill. When it bursts, multiple generations will find their expectations destroyed. The politicians at ground zero had better be saying their prayers and putting their earthly affairs in order, because they aren’t going to last very long after that bubble bursts and reality sets in.

This is a mathematical certainty: hundreds of pensions are seriously underfunded, and many more will be endangered if we have another significant recession. Four percent returns for 10 years in a pension plan portfolio will result in massive future underfunding, even if things eventually get back to “normal.” There is going to have to be significant funding from corporations and taxpayers to make up the shortfall, at precisely the time when that money will be needed to rebuild infrastructure, retrain massive numbers of workers facing employment challenges from an ever-transforming environment, and deal with the fact that there will be more old people living than there are young people being born. This last fact is already the reality in Japan and much of Europe.

Next week we are going to look at what makes the pension challenge even more problematic: the difference between 2% GDP growth and 3% growth over the decades to come is every bit as dramatic as the difference between 4% and 8% portfolio returns. And if we don’t figure out how to get back to 3% GDP growth (and neither of the two leading presidential candidates are offering anything close to a plan that will get us there), the US is going to find itself even deeper in a hole, even as we continue to dig.

------------------------------

* This is a slightly abridged article from Thoughts from the Frontline, John Mauldin's free weekly investment and economic newsletter. It first appeared here and is used by interest.co.nz with permission.

49 Comments

John Mauldin is worth following. He predicted the GFC. I read his book The End Game many years ago and he has been spookily correct. In almost the final chapter he talked about the Australian Housing boom-this was about 5 years ago. He said I would keep going until China got into difficulty and then said it would get v messy. I need to re-read to see exactly what he said.

yet he doesnt see energy at all...

Or the environment for that matter. Though at least he is talking about something other then how the future is all roses.

John Mauldin has hit the nail on the head. His article may be full of american references but it has complete reality. excellent work.

In NZ the Government Super Fund (majority govt employees approaching retirement are in this fund). A couple of years ago there was a short fall of around 1Billion which the tax payer had to pay.

NIRP will make this ongoing liability worse. Thankfully that fund closed to new members 20years ago under Ruth Richardsons watch - aka razor gang.

NIRP will reduce interest earnings and also the tax on these earnings. Thats deflationary and detrimental to govt revenue.

Pension Funds collapse will be catastrophic.

So that will force people to work longer and starve the young of much needed jobs. They will have to bring in an "aged worker" medical check otherwise you could have people who should retire not actually retire.

But it will all be ok - our houses will ALWAYS go up in value. And our interest rates will be low for ever . She'll be right mate. Kiwi's aren't all that bright are they? But they are brighter than the average american I think

Unfortunately the pension collapse in the US has already started. Years of poor returns and young workers not seeing any future in the pension fund aren't contributing. There are some unions that require the contributions but those won't stop the collapse.

There are currently pension funds that have had to cut payments. So there are a number of recent retirees that have suddenly found their income cut. These funds are well managed. The poorly managed funds will abruptly run out of money causing major cash flow problems.

If you look at Japan their pension funds are already financially broken from their ZIRP policy.

So what we are facing is a future with the largest retired population with very little spending money and a rapidly shrinking economy. However what we will experience is people working their entire life until they die with no retirement, but at least the economy will function under those conditions.

So should one take a 5 year holiday from KiwiSaver contributions then, and pay extra on the mortgage instead?

I would, but that is me.

Being self employed I never had kiwisaver, but you get some from the govt, and some from the boss, so it's like a guaranteed return right there. What I didn't like about it was the fact that I can't touch until 65 at the earliest. The money from kiwisaver is going to be worth diddly squat, thats the essence of this article, so you need to put your money where it will maintain its value.

A house will always be worth what a house is worth, and you will always need a roof over your head. What I did was cover the basics, for me a small farm 30ha, and a couple of rentals which net about $230 per week. Once I hit 65 the mortgage on the rentals will be paid and I'll net whatever the rental on two houses is. I know I can live on the rent from two houses, so it's all covered.

You have to be flexible, and somehow need to save up that cash, but we did it for $400k last year.

Make contributions where you are getting contributions from others (employers or government) as they are adding "free" money. I would not put an excess above any other contributions. If you are 15 or more years from retirement it's probably worth keeping the account as is. You will get some benefit from dollar cost averaging if your account is mostly shares as you might pick up some bargains with future gains to be made. Think carefully about any decisions you make with kiwisaver.

If you can put more towards the mortgage. Given that the official inflation rate is 0.1% mortgage principal is just debt, everything you pay off means a real saving in interest payments at this time. The whole idea of low interest rates is to reduce debt but everyone is doing the opposite.

From a financial perspective this article is good. However, like most commentary in the financial world, it misses the essential truth, that it was the INCREASE IN EXTRACTION OF FOSSIL FUELS (especially oil) between 1760 and 2000 that facilitated economic growth and generated the apparent surpluses that permitted early retirement.

As long as there was easily extractable oil, forests to chop down, fish to harvest etc. the global economy could grow at a high rate.

Now none of those preconditions for growth exist: extraction of conventional oil peaked over 2005 to 2008, and the global economy has been increasingly propped up by unconventional oil, which is a lot more expensive to extract.

The nub of the predicament can be summed up in one simple phrase: without energy nothing happens.

The picture looks increasingly grim from here on for anyone dependent on economic growth because there cannot be any significant growth from now on, as the following items indicate.

'While the mainstream media are regularly reporting about artificial islands and militarization in the South China Sea, peaking oil production in this important region of the world and its economic impact is totally ignored.'

http://crudeoilpeak.info/peak-oil-in-the-south-china-sea-part-1

'The red horizontal line is the maximum crude oil production level in May 2005 (the Katrina year). We can see that almost all additional oil produced now above that level is US shale oil. In other words: without US shale oil (which required cheap money from quantitative easing), the world would be in a deep oil crisis.'

http://crudeoilpeak.info/world-outside-us-and-canada-doesnt-produce-mor…

Thus, we see that we will soon be entering a period of severe decline in available energy, with populous nations attempting to increase their consumption dramatically.

The numbers simply do not add up, which is why central banks have been 'pushing on a piece of string' when attempting to stimulate economic growth.

As global extraction of oil declines, so does the global economic system, until some critical point is reached, after which the system rapidly collapses.

Just how far from the collapse point we are is difficult to determine. However, we can be certain that no government will plan for the inevitable collapse because we have a confidence-based system.

In the absence of official planning, individuals need out carry out their own planning.

Pity youngsters who have been promised 'the good life' and are about to have the rug pulled form under their feet.

You said it better than I could.

Not just youngsters I am in my 50s and its blindingly obvious that the odds of my pensions and even OAP beng paid are approaching zero IMHO despite decades of promises.

--edit-- indeed I might have an even bigger reason to be more miffed as I have been lied to by successive Govns and the pension industry. So unlike youngsters ive put money aside for almost 40 years into a ponzi scheme with little hope of any payout, so an utter waste.

That's exactly why I never signed up. A bird in the hand is worth two in the bush, and once your money enters a scheme, it's no longer your money, it's theirs and they care about themselves not you. Though I think you'll still get something out of it.

Thus, we know that the underlying rate of return is near zero in the West. The rate of return falls naturally, due to capital accumulation and market competition. The system is called capitalism because capital accumulates: high income economies are those with the greatest accumulation of capital per worker. The robot assisted worker enjoys a higher income as he is highly productive, partly because the robotics made some of the workers redundant and there are fewer workers to share the profit. All the high income economies have had near zero interest rates for seven years. Interest rates in Europe are even negative. How has the system remained stable for so long?

All economic growth depends on energy gain. It takes energy (drilling the oil well) to gain energy. Unlike our everyday experience whereby energy acquisition and energy expenditure can be balanced, capitalism requires an absolute net energy gain. That gain, by way of energy exchange, takes the form of tools and machines that permit an increase in productivity per work hour. Thus GDP increases, living standards improve and the debts can be repaid. Thus, oil is a strategic capitalistic resource.

US net energy gain production peaked in 1974, to be replaced by production from Saudi Arabia, which made the USA a net importer of oil for the first time. US dependence on foreign oil rose from 26% to 47% between 1985 and 1989 to hit a peak of 60% in 2006. And, tellingly, real wages peaked in 1974, levelled-off and then began to fall for most US workers. Wages have never recovered. (The decline is more severe if you don’t believe government reported inflation figures that don’t count the costof housing.)

http://thesaker.is/capitalism-requires-world-war/

You missed cheap oil and cheap raw materials as these are two of the essential drivers of growth, without these we cannot grow no matter how hard we work.

" Without growth, retirement as we have come to know and love it will not work. Retirement will still be possible, of course – just not under the same conditions.

Yep. We will power down, hence yes pensions and Govn OAP are almost certianly mostly toast. Ergo there will be no retirement for many, I certianly expect to have to work until I am too unwell/dead.

Well that's not good news. But on the up side, you may have a lot of company.

Yeah misery loves company.

If someone can create a cheap net-energy producing fusion reactor we could have more energy than what we would know what to do with. However projects to create viable fusion reactors have been in the works for many decades with no success. Everyone better hope for a technological leap in the next decade.

Actually we dont need fusion, what we would have found good enough is Thorium salt. Sadly the asshole by the name of Nixon killed its development otherwise by now we'd be sitting fairly sweetly IMHO. If we are lucky China may survive long enough (a decade) to get commercial plant up and going and sell the IP to others, which would be funny if it wasnt so desperate. " Everyone better hope for a technological leap in the next decade." indeed.

Thorium reactors would be great but so much more money has been put into fusion. Trying to develop thorium fission reactors at this time would be a very long road.

So the entire thrust of the article is what?

a) we have a problem (oh yippee dee doo I never would have guessed)

b) not enough or even any growth (uh huh)

c) interest rates and profits are non-existent to pay pensions. (really? who would have noticed.)

d) "Why not? Because our monetary overlords decreed that it should be so" no, energy limits decrees it.

e) "This is a mathematical certainty" indeed funny how mathematically you cannot see that the math of exponential growth on a finite planet does not compute.

Yes, the 'infinite growth on a finite planet' aspect would be hilarious if it were not so serious.

Chris Martenson, of 'Crash Course' fame, commented that we have an economic-financial system that assumes the future will always be bigger than the present. Forever. Which is absurd. It followed, as sure and night follows day, that when we hit the wall of resource limits, the economic-financial system also hit the wall.

Professor Albert Bartlett presented a wonderful lecture, 'Arithmetic, Population and Energy', several thousand times....and made almost no impact whatsoever; despite being spot on. He pointed out that the 'really good' annual growth of 7% that people liked to see resulted in doubling every 10 years, and even the 2% growth that most economists describe as disappointing results in doubling every 35 years.

Does anyone seriously think that consumption of oil and other resources 35 years from now will be twice the current rate? Clearly such a notion is absurd because the oil simply does not exist. Nor do other resources essential to the functioning of the global economic system. Yet economists, politicians and central banks persistently aim for 2% (or 2%plus) growth and suggest it will continue for decades. Such notions are truly insane.

The desired growth is apparently 4% which needs 2% more oil per year. Oil supply today is 94? mbpd all up (incl condensates, shale etc) Even the most optimistic oil guy talks about 130mbpd at most 35 years from now and not 190mbpd. However its the reverse, 35 years from now effectively there will be no oil.

So some fag packet math, lets say 94mbpd shrinks to 14mbpd (leaving residual and bio-fuels), 80mbpd disappears, ergo we'll be lucky to have 20% of the GDP/economy in 2050 we have today in real terms but 9billion ppl to feed. Frankly I think my kids / next generation(s) are f*cked, and I have to live with that legacy.

In practice, whatever oil is extracted after around 2025 will be largely used near the point of extraction. Jeffrey Brown highlighted the 'Export Land Model' several years ago: practically every oil-exporting nation has increasing domestic consumption, so the quantity of internationally tradable oil declines much faster than simple geological constraints and energetic constraints to extraction would seem to indicate.

https://en.wikipedia.org/wiki/Export_Land_Model

NZ imports approximately 80% of its oil (I have not seen an exact number recently), and that imported oil could 'vanish overnight' if political factors suddenly turned the wrong way. Under even the most optimistic scenario, NZ is unlikely to be able to import any oil after around 2025. Countries like Spain, Italy, Japan etc. are in a far worse predicament than NZ, and are unlikely to survive in their present forms beyond 2020. Just 5 years away, now.

The well-documented science of oil depletion and the very clear indications of falling supply in the near future do not deter governments from squandering rapidly diminishing resources on infrastructure that is totally dependent on INCREASING oil supply.

By the same token, governments refuse to acknowledge the reality of exponentially increasing sea level rise, and encourage squandering of resources on infrastructure that will be inundated by mid-century at the latest.

40 years of ignoring all the scientific evidence by governments (practically all of this was worked out by 1975) has a huge price, and as you say, the next generation is f*cked

We won't see serious oil shortages until 2100 if then. Sea level rises are going to be minimal. I'll go with JB's thought below. Unimaginable wealth and a glorious future lay ahead.

ah nice troll.

and this opinion on oil by 2100 is based on what data/reality?

"The point is that we are all capable of believing things which we know to be untrue, and then, when we are finally proved wrong, impudently twisting the facts so as to show that we were right. Intellectually, it is possible to carry on this process for an indefinite time: the only check on it is that sooner or later a false belief bumps up against solid reality, usually on a battlefield.

– George Orwell"

Currently by 2100 the sea level projections are ramping up, plus the damage / costs come in faster, exponentially in fact,

http://insideclimatenews.org/news/29022016/flood-damage-sea-level-rise-…

Then there is the small drought problem in the eastern med set to get a lot worse,

http://climate.nasa.gov/news/2408/

So first Syrians flood to Europe, next?

then maybe russia as well,

http://www.npr.org/sections/thesalt/2016/02/21/467413500/for-russian-fa…

Glorious? if you like to revel in death caused by starvation, riots, war, weather, pestilence I guess so.

Well,

I would love to see the evidence for both your assertions; no serious oil shortage till at least 2100 and minimal sea level rises.

I'm no oil expert so I wouldn't argue that point,but I have done a lot of work on climate change and I would certainly question that. What do you regard as 'minimal'? If you accept that seal levels are actually rising,then you presumably accept that this is being caused by thermal expansion and melting land-based glaciers. Since we are well into the current inter-glacier period, to what do you attribute this warming?

For some background on the subject,you might care to peruse Sir Peter Gluckman's report to the government in 2013. Is titled; "New Zealand's changing climate and oceans" and can be found at;

www.pmcsa.org.nz

Read Buffett's latest letter to shareholders - an entirely different take on the future.

Today's crop of youngsters will prosper as never before.

I think I'll run with his view of the world !

Got a URL on that please?

Otherwise his view is on say insurance is he can put up premiums no worries. This is assuming an effective monopoly which if people are so fearful of CC events they buy insurance no matter the cost is kind of true and sick at the same time.

The reality is that costs /payouts due to CC look to rise exponentially and like we see from Chch there were a considerable amount of ppl not insured due to the cost I think we'll find more and more ppl wont have any. Certainly my insurance at $200 a month is noticeable, if it ever comes to eat or pay the insurance I'll choose to eat today thanks.

I think we don't need infinite growth, we just need to live within our means. The growth we have seen since leaving the gold standard is in credit. This growth bought by debt is coming to an end. Imagine a world where there is no credit, just physical money. You would need to save up to buy things. That's where we came from, look how distorted the world is now.

Fundamentally he is talking about the same underlying issues that caused the GFC, the consequences of unrestrained capitalist greed and the fallout. No one will be spared. Pollies the world over have bought into flawed economic theory that failed to account for unrestrained human greed, while it argues for less regulation and more free market. This is not a perfect world, it is a flawed human one. We need laws and regulation to restrain those who think they are more entitled, smarter or better than others. so far the bottom end of society has those, but the top?

Well said, totally agree. Even we keep democracy there will be a huge swing to the "left" as the ppl losing will at some stage be big enough to vote for "something else". If we do not, I think we'll see riots and revolution, so ugly or very ugly. NZ will I hope be fortunate, many other countries with huge populations wont have the first option.

The opposite is true. Big money would have suffered a wipe-out, if central banks had allowed bankrupt banks, states and corporations to go bankrupt by NOT printing money to keep them afloat since the GFC. What governments and central banks are doing is central planning economy instead of letting markets regulate the flows of capital. The results, as always with Socialism, is a declining standard of living for many while a small cast of politicians, functionaries, managers and speculators are reaping the benefits.

Had market forces bankrupted mismanaged economic entities during the GFC, there would have been great suffering at first, but we would now be in year 8 of an economic revival built on a sound basis instead of in year 8 of an on-again-off-again perma-crisis. The demise of speculator banking alone would have driven the best talents back into science and engineering, areas which actually create progress and prosperity. As things stand, young people see that being a JK-type greedy banker pays, as you get loads of money is speculation goes right and loads of taxpayers' money if it goes wrong.

Socialism does not work, face it.

Really nothing works long term.

Just how you think we would have got through not having any banks if they had all gone to the wall mystifies me. I mean just one aspect, how would you get food? and for 4million with no banks operating? let alone the 70million in say the UK on the same land area?

In terms of "year8" look at the only example we have, the Great Depression. From 1929 to 1932 in effect was the collapse so - 3 years there. So by 1937 the world was coming out of the DG sure but that was mostly due to the massive stimulus caused by the run up to WW2.

Some notes,

a) our debt is even greater today than 1929, ergo the fall is likely to be even bigger and far longer. have a look at Steve keen for that info.

b) The US was the greatest oil exporter at the time ie they had abundant resources with which to use to grow we dont this time in fact one of Keynes comments at the time now looks very prophetic.

c) Our economy is even more inter-linked so a stress on one sector will feed into others more quickly, in a mostly unknown and complex manner and bigger.

Why is having rules and regulation Socialism? It is not. There is a balance between the free market and the Government being responsible for everything. What is being demonstrated at the moment is that unregulated markets create greed and imbalance. The declining living standards you refer to are not caused by socialism but by the free marketeers trying to growth their wealth at the expense of their workers. they are artificially growing productivity by driving down wages. This has gone on for years. In effect they are inventing new forms of slavery. A very good example is AFFCO and the Tolley family who seem to feel it is fine to spend $50 mil on a home while they force their work force onto IEAs that are essentially unliveable. The on-going GFC is a consequence of rampant right wing greed. It is past time to bring it back to centre, but probably too late and more likely moving towards a revolution.

So to sum up its case of pensions are buggered, cash them up and?

Prepare to work until you die. Or something I have promoted for some time now. Buy physical assets that will maintain relative value, and provide income. Always buy low.

I suspect though, that if money in the bank is guaranteed to cost money, you can expect to see an even bigger bull run in stocks, even though the underlying companies are spending more money on buybacks, than they are on cap-ex, which means they are going to have some massive debts to pay in the future.

I posted about the wall of corporate debt due, peaking in 2020, bloomberg I think. Yep,

http://www.bloomberg.com/gadfly/articles/2016-02-29/-9-5-trillion-debt-…

Buy a house. At least then you dont depend on a inapt government to provide a roof over your head. Make sure a piece of land with favorable aspect goes with it, so that in the worst case you have a subsistence fall-back. And dont forget to buy some kind of energy system that makes you a bit independent of the inapt government's electricity. If you have kids, invest as much into their education as their brains can take. Oh, and learn programming so that you can create some bs app that provides cash flow on the side.

Unfortunately, this is only half a joke. 1/2 shares (mostly not NZ ones, of course, good dividend payers), 1/4 real estate, 1/10 gold (physical, as insurance) and the rest cash, as the 3% you are getting in NZ are still extraordinary, globally speaking.

But I am sure there will be a part 2 in which he will explain the ultimate investment strategy for retirement.

how do you pay the rates?

My rates have over trebled in 19years....

Thats the problem....need cash flow for that.

Rates will drive older freehold home-owners out of their neighbourhoods.

Really.

Rates on a $2.1 million dollar house in Herne Bay are $6000 p.a.

You telling me these guys will not be able to deal with $500/month rates ($125 p.w.)?

People on the dole pay higher rents than that.

Cry me a river. Sell up and move to a palace in Tauranga if it's such a hardship.

Maybe should have diversified assets before retirement instead of expecting us (the young) to bail them out.

"You poor things"

When considering the use of ZIRP or NIRP and what they are supposed to achieve, what seems to be missing is direction. These policies are supposed to stimulate growth, but providing low or no cost money with no stipulation as to how it is to be used will generally see it wasted. Low cost money invested in property will not stimulate economic growth, but in R&D and local manufacturing it may.

With globalisation the drive to reduce production costs saw many manufacturing jobs exported to places like China. These moves also saw the necessary export of the technology that the manufacturing employed, thus the net outcome exporting what should have been protected capability to a potential competitor, at the expense of local jobs, export income and the flow on economic benefits. A number of companies come to mind here Fonterra at the top of the list.

So the message to the RBNZ should be that if they are to consider ZIRP or NIRP, then they must also specify the used and required outcomes. We should be looking for more than just profits, but capability, and jobs as well.

The idea of low interest rate policies is to take the interest rate pressure off lending. This gives the borrowers a chance to reduce debt load, as they will be able to pay off debts faster.

However today's world the majority of people are financially retarded. Easy credit means they borrow more as interest rates drop instead of reducing debt.

The goal of ZIRP or NIRP is to lend money to companies prop up loss making ventures so they don't collapse. These policies literally lead to running a large portion of companies as a ponzi scheme so that people keep their jobs. Effectively those working at loss making companies are bludgers.

These policies also create a liquidity trap. The central banks can't increase interest rates without putting the economy at risk. Alan Greenspan is the John Law of our generation.

https://en.wikipedia.org/wiki/John_Law_(economist)

Very well said, personally I think there's a whole lot of Mississippi Companies in the tech sector in particular.

I'd also add the (intended?) side effect of NIRP-ZIRP to further inflate asset bubbles, which fools people into thinking everything is fine. This also makes the 'buy some arable land' survival strategy out of reach for most of us.

There are large commodity companies in China and South Korea that are being run like Mississippi Companies. ZIRP lending perpetuates them. Let's hope that all the bubbles in every market don't all pop at the same time.

"The goal of ZIRP or NIRP is to lend money to companies prop up loss making ventures so they don't collapse." to reiterate my point, what kind of companies? A property investment company won't produce any kind of growth, but cheap money could assist a manufacturing company survive a slump, to weather a down turn, find new markets, fix or create new products. All the time supporting or sustaining jobs and growth. Agin it is important how the money is used, direction is an important component.

All of the above comments and general sentiment make my wary of having investments /capital in a bank and I am not happy with the advice that I received to date.

I appreciate that it is a bold question but would someone please be able to suggest /recommend an adviser (more than happy to pay) or who to find one

Thanks

For this I recommend searching for an 'authorised financial adviser'. I do not want to recommend anyone specific as you really need someone who is a good fit with you.

Thanks, dictator will do some more digging and see if I can find someone who I get with

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.