By Andrew Bascand*

Sometimes perception doesn't bear the truth. Facts are ignored and experts unheeded or discounted as they are deemed too close to the issues. In reality the prickly issues are well known.

Market sentiment can swing wildly, and you need to ask questions of experts face to face to find reality. This week in our most recent trip to see analysts and financial companies in Sydney, we were struck by several inside views.

Australia is not in a recession. Far from it. There is a degree of moderate optimism, tempered by the need for reform on a number of fronts. Business is still focused on cost, but productivity and technology investment are more important than cutting employment.

Perth and some mining towns are seeing both income and house price deflation. Elsewhere trends in the housing sector remain at worst benign. If anything, rents in Sydney and Melbourne continue to rise and unemployment is falling. These conditions are not conducive to a major deterioration in impairments.

Specific loan concerns have been highlighted in the media. Dairy sector risk has been quantified, and resource and energy sector exposures are still largely investment grade. These issues may have an impact on the next few quarter’s impairment levels, but all seem controlled and well within reasonable provisioning. Perhaps there may be a little complacency around the potential for further waves of economic or commodity price weakness, but loan to value ratios in housing and institutional lending are relatively low. Perhaps Australian executives were a little concerned with more recent NZ dairy price weakness and stress tests, but there is certainly a very calm approach in dealing with investor concerns about these issues.

The agenda for the banking system to hold even more capital is softening. Australian banks already sit in the top quartile of global capital ratios. The banks we spoke with said that the regulator (APRA) is more focused on risk weights for lending, on lending classification by risk and general lending criteria. There is a growing perception that higher capital requirements will only result in a further rise in both mortgage and business interest rates as banks seek to maintain a reasonable return on equity.

Over the next 2-3 years, risk weights for lending may rise further. Floors for overall portfolio risk weights are being discussed globally. However, taking the lead from the UK, there is a general perception that total banking system capital is already at a high level, and the conversation needs to move on to consider liquidity, risk weighting classifications and lending practices.

When questioned on more general lending practices, the banks said that recent media concerns had led to a further check on their controls. They said that all lending practices were tightened further in 2014. Investor loans in particular had significant controls and were now much less that 10% of lending. Interest only loans had higher interest rates, and all borrowing was subject to a 7% plus (7.0-7.6%) rate stress test.

Given the noise around a widespread Ponzi scheme (which we have already discounted), we asked more direct questions about lending practices. Directors and senior executives of the banks confirmed that original bank statements are viewed to check borrowers’ income and expenditure. New mortgage applications were also reviewed in Australia and New Zealand, not offshore as suggested by some news media. The regulator continues to be highly focused on auditing lending practices.

Turning to wealth management, the banks remain divided about how best to approach the sector. Advice practices have been generally weak, and both Commonwealth Bank and ANZ were widely reported in the press for weaknesses in some life insurance processes last week. National Australia Bank has sold its life business and more formally separated itself from its private bank, JB Were. ANZ also made several changes last week to their wealth management reporting lines. It seems that banks are keen to distribute life, general insurance and wealth products, but seem generally less enamoured with operating these businesses. In part this reflects both the capital intensity of insurance and the regulatory and consumer challenges facing the wealth management and investment advice environment in Australia.

The superannuation industry has navigated its way through a significant reform agenda. Wealth management advice is increasingly focused on the post-retirement income generating years. Annuities remain a significant focus as part of the solution. In addition, self-managed super, My Super and Robo advice are impacting on margins.

Financial technology disruption remains a general risk for incumbents. However, some of the banks are ironically leading the charge with their own disruption. Consumers in Australia and NZ are already highly penetrated with bank led ‘fintech’ solutions. Wealth management is more exposed to Robo advice disruption.

A more general discussion with each institution on longer term technology disruption around blockchain and quantum computing yielded little insight. All the banks have joint working groups on improving the payments system to ward off a disruptive social media based change in the payments system. Imagine a giant spreadsheet with everyone's ‘ledger’ instantaneously connecting. That apparently is the future. The cost base of the Australian banking system is an astonishing $40 billion a year. Blockchain technology could significantly lower costs and so the prize is worth the investment. However, conceptual beta trial implementation is still years away. Expect lots of talk about blockchain and quantum computing over the coming years.

Overall this week we asked lots of prickly questions of banks and other financial companies. It isn't clear that anything is broken. In fact higher capital, stronger lending practices and senior executives thinking about technology suggests a very healthy financial system. Much of the outlook depends on the bigger trends in the Australian economy and commodity prices. However, we generally heard honest responses to our questions, and while the recent recovery in share prices leaves less upside, we liked the expression that right now it is probably better to ‘hug the cactus’.

----------------------

*Andrew Bascand is managing director at Harbour Asset Management.

5 Comments

May the term Ponzi scheme, applied to the property market, be forever eradicated from comments sections.

This bit from the Bank resilience pdf seems reassuring:

What if house prices did fall? Banks must stress test their portfolios. For instance, CBA’s risk

statement says that if house prices fall 30%, and unemployment doubles (to 12%) then CBA’s

models suggest about $3.75bn of losses, ie a bit more than 1/3rd of forecast 2016 profits.

You going to pile into CBA shares? With thei reassurance, you're possibly onto a winner.

I'm not that reassured! It's just that a doubling of unemployment and a massive drop in house prices combined with billions in losses still had them making a handsome profit.

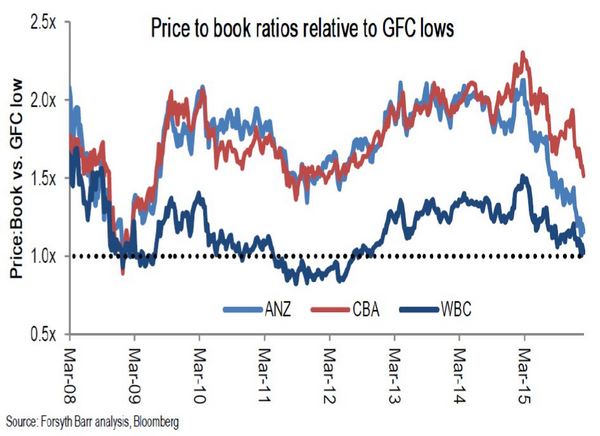

The deteriorating Aussie bank price to book ratios are not encouraging.

Gross disagrees with commentators such as Barron's who argue that the selloff in bank stocks has created an opportunity. He urges investors to shun the "tantalizing apple" of bank stocks with low price-to-book ratios – Bank of America Corp.'s (BAC) is just 0.6, Citigroup Inc.'s (C) 0.61 – since he expects the sector's future return on equity to resemble utilities'. Read more

So a bank with only a 10% stake in all their assets is regarded as safe and yet their own customers with the same scenario in a house are regarded by said bank as a risk a likely requires mortgage insurance. The only difference is the bank has a more diversified income stream.

If the asset ledger becomes impaired by 30% the bank will fall into negative equity just as said homeowner would. To make matters worse, the bank will have some opaque, OBS derivatives in place to protect against asset impairment.

Hidden behind the bank's rosy impairment outcome is likely to be the hope that they can quickly recapitalise before negative equity comes home to roost.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.