By Bernard Hickey

Should we all celebrate?

Or sink into a great depression?

Or run for the nearest bunker?

It's hard to know how to react to this week's declaration by Quotable Value and Homes.co.nz that Auckland's average house value rose to over NZ$1 million in August.

Auckland's home-owners should in theory be celebrating their good fortune and be voting for more of the same. Anyone who invested just over NZ$53,000 of their own money in 2011 to buy an average Auckland house with a 90% mortgage would now be sitting on tax-free capital gains of NZ$485,000.

Indeed, some are celebrating. New car sales are at record highs and spending in Auckland's cafes, bars and restaurants is growing at double-digit rates. But it's not the sort of go-for-broke debt-fuelled spending binge like the one we saw from 2002 to 2007 when mortgage lending grew at an annual rate of 15%. Mortgage debt grew 9% in the last year and most people think it has peaked at that rate, given the Reserve Bank's latest restrictions on low deposit lending and a limit on debt to income multiples expected next year.

Most Aucklanders don't believe the manna from the great housing gods in the heavens is real enough to go withdrawing from their household ATMs, which is why the lending growth is relatively subdued.

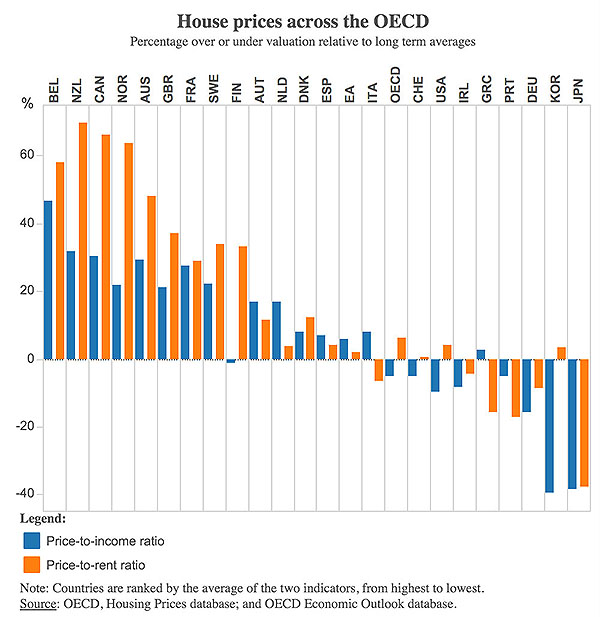

They also can feel in their bones that house prices at 10 times incomes are hyperventilated, if not downright over-valued. New Zealand's house price to income multiple is the second most expensive relative to long run averages in the OECD (behind Belgium), and is the most expensive relative to rents in the OECD. That over-valuation has grown more than any other country in the OECD over the last six years. This is not the sort of world champion tag we want.

The $1 million milestone is clearly a moment of despair for those young Aucklanders aspiring to own a home and start a family, particularly those ones whose parents were also renters. The combination of the price rises and the new LVR rules mean they face decades of saving for a deposit, let along being able to afford to borrow the hundreds and hundreds of thousands dollars needed to buy a home. All they can hope for is to win Lotto or to marry into a rich family.

Another response is to hunker down and prepare for an implosion, which means saving madly to repay debt ahead of the housing market end-times and to diversify into other types of assets. This isn't so much a celebration as a preparing for the party to be shut down.

There are two other ways to think about the magic million number. Firstly, there is the Stockholm Syndrome response where the hostage starts to identify and sympathise with the hostage taker. The home owner knows they're being forced against their will to stick with the over-valued asset, but they also think any attempts to end the siege only risk harming both hostage and kidnapper. Our political debate over housing affordability has appeared a lot like a hostage crisis lately, often boiling down to: 'Nobody moves or the home equity gets it!'

Secondly, there is the pass the parcel approach, which is best played with The Wiggles' 'Hot potato, hot potato' blaring in the background. If you really think that one day the music will stop and you don't want to be holding the bad loan parcel when it does, then the best approach is to flick-pass the parcel as fast as you can and then hope the music stops for someone else. You could even sit a few rounds out of the game.

That's what a few of the banks are now doing. ANZ CEO David Hisco said in July he thought the Auckland housing market was 'over-cooked' and he called on banks to tighten their lending criteria. He even called for the Reserve Bank to force rental property investors to have a 60% deposit.

"The current situation will see ANZ implement even tougher criteria for investment loans as house price inflation spreads from Auckland to other regions," Hisco said.

And the nation's biggest bank has been true to his word since then. It stopped lending to landlords wanting to buy apartments and house-and-land packages off the plan. Developers and brokers also report ANZ and other banks have pulled back from lending to developers in Auckland in recent weeks. The Reserve Bank also noted this week that some banks were being more restrictive than even the latest Reserve Bank restrictions on low deposit lending. The Australian banks know the words and actions for 'Hot potato, Hot potato' by heart.

Bizarrely, I have even heard cabinet ministers worry about the valuations for houses on the Government's balance sheet. The Government owns houses (or more importantly the land under them) worth NZ$19 billion at current prices. The implied worry is that if the Government built a lot more with these inflated prices, then it would face big (paper) losses on that housing equity if there was a correction. This is, of course, ludicrous thinking. Auckland desperately needs more houses and the only player with a big enough balance sheet and a long enough investment horizon to ride out the quarterly ebbs and flows of the housing market is the Government.

The risk is that the developers and banks, who are beholden to much tighter funding requirements and have to report quarterly to impatient and anxious shareholders, choose to step back from lending to build the tens of thousands of houses that Auckland needs over the next five years.

There is one step the Government could take to circumvent this game of pass the parcel. It could restrict its KiwiSaver HomeStart grants to new homes. That would guarantee developers and their bankers that there was a pipeline of funding and demand for their more affordable apartments and townhouses, given the Reserve Bank's LVR rules don't apply to new builds. If the banks and the Reserve Bank are determined to stop landlords from funding all these new homes, then the least the Government could do is step up to ensure they help first home buyers fund these homes.

Now is not the time to give in to the hostage takers' demands. Let's take the long term view and use the Crown's balance sheet to negotiate our way out by funding and building those homes that will be there for many decades and housing cycles to come.

A version of this article also appears in the Herald on Sunday. It is here with permission.

59 Comments

Why should KiwiSaver be allowed to be used as a housing subsidy at all? It simply enriches vendors, inflates house prices and robs the young of their retirement savings.

This is also yet another article that suggests that the government should do things. As we are all now fully aware, this government categorically refuses to do things.

It's unlikely this housing party will end. New Zealand is special (needs).

$1.5 mil, here we come. In 6 months ?

Maybe a bit longer but yes, I expect so.

I agree, and I also see how subsidies work and just who exactly they subsidize, but it will be very difficult to unpick WFF and accommodation top ups, as it will in future be to unpick the issues that dipping into Kiwisaver funds will turn up. Approach with caution.

You are 100 % correct , Mr X ... it is the height of insanity to allow our Kiwisaver retirement funds to be channeled into further inflating the biggest residential housing bubble this country has ever seen ...

... when the bubble bursts , there'll be a massive loss on the retirement nest eggs , further burdening future taxpayers , to pick up the superannuation tab for their forbears , Gen $Million ...

... absolutely barking mad !

That is why it is too big to fail. It will be left to tax payers to mop up the mess. Potentially it will be very costly. First we had the leaky building crisis, now we have this costly bubble that has been allowed to get out of hand. Don't we ever learn with NZ houses.

People need to realise that Kiwisaver is not a savings account, it is a form of tax, it is designed to pump up the share market and you you are not allowed to touch "your own savings" until you turn 65. But if you would like to pump some of your Kiwisaver into the housing market and yes you are more than welcomed to do so! Hurry and join Kiwisaver!

it is designed to pump up the share market

Really? I think you overestimate the impact. NZ's $35b in Kiwisaver only represents 0.04% of the global $85T equity market capitalisation It is actually less than this as a large % of Kiwisaver money is in bonds or cash.

The point here is that if it's applied to new builds only it should increase supply which is good for the market. The only problem with that is what is shutting out investors from scooping up the extra supply. It's a good idea in principle but may not play out as expected. This doesn't affect kiwisaver savings, as the article references homestart grant and not kiwisaver first home withdrawl.

Correct everyone who can make a difference is playing passing the parcel with hope that music does not stop at them but does not realise that music has to stop at one time and is only a question of When and not If.

No pointing in debating housing crisis as no one is serioulsy interested in controĺing it and will happen by itself and than all so called experts will be heard saying : We warned. We said so. We knew it. We told what goes up comes down. Ecenomy ......

If seriously interested one Golden bullet (no silver bullet many says) tax all non resident foreign buyers atleast for few years to start with like Vancouver and intially the market may correct slightly but in the long run will stabilise.

Question is who will bite the bulllet

nzkl - totally agree. The pollies aren't at all serious in addressing the issue. SHAs and planning reform are smokescreens. No amount of SHAs and planning liberalisation will get on top of this issue now (different story if it had been don 7-10 years ago) because of the lack of construction capacity, and the fact that a decent proportion of land owners are just landbanking / speculating

Totally agree that if this was being treated seriously we'd be seeing the Vancouver approach.

Land Bankers are government made

Land Bankers are not born that way

There is no course you can do to learn how to land bank

Land Bankers are "made"

This time round it is the government actions that has made them

Allowing property to escalate 100% in the last 3 years

With mortgage debt (=money) at 9% YoY growth and plenty of foreign money juicing the market we would expect the economy to be growing like crazy. Mortgage debt is now about equal to total national annual output (turnover or GDP) at $240,000,000,000 so a 9% increase there is also 9% increase of debt to GDP. But wait, there's more; household debt is only half the picture. Agriculture, Government and business debt are also (coincidentally) about $240billion. The total debt to GDP ratio is climbing much more rapidly than the 9% increase in household debt implies with the other sectors contributing another 5% of debt to GDP growth for a total of about 14%.

Set alongside our very modest GDP, even lower GDP/capita and sub 1% inflation, credit growth of this magnitude is unsustainable and dangerous. The RBNZ should be raising rates I would have thought.

You forget Student debt of 16Billion, which the RBNZ states should be itemized under household debt but somehow is forgotten..

Yes, and loans to beneficiaries. These are down as an asset in the Government books. LOL

What, so banks are belatedly showing a bit of rationality and caution, and trying to pull back from feeding this beast by raising requirements, so shit, we need to scrape up another bucket of fuel to throw on the fire, what to do, what to do? Hey, let's put people's retirement savings on the sacrificial pyre!

What will be the quality of new houses/apartments being built in a hurry ?

Will they stand the 50 years test ?

First home buyers buying a new house? Madness.

By definition, the house must be crappy or in a crappy location or both.

Thousands of state houses were built in the 50s in a hurry by tradespeope who were rushed through their apprentiship. They were more solid than the homes built in the 90s and on.

These state houses are still up and not leaking etc.

Finance Ready

This morning, ZB's "The Resident Builder" described the case of a person (in Auckland) who had all the designs for a new house, consents obtained, ready to go, but cannot find a builder

Hey, if you need to borrow a big heap 'o money to fund something the banks are spooked by, set up a fund and invite investments. You could call it a Finance Company. And there's a bunch of experienced finance company administrators about due to get out of jail who have all the skills necessary to run it, and Richie McCaw probably has time on his hands and would be happy to front the TV ads.

this is the banks problem kakapo. no one else to blame this time. the $10b losses in 2008-2011 will all be on the bank balance sheets now

There are two other ways to think about the magic million number. Firstly, there is the Stockholm Syndrome response where the hostage starts to identify and sympathise with the hostage taker......

The hostage taker can be none other than the RBNZ.

As noted earlier in a response to a BNZ analyst's claim:

If the RBNZ remains committed, as it appears, to trying to soon return CPI inflation to target (2%), it will have little choice but to keep cutting the OCR. Our core view remains for the RBNZ to cut in November and February, taking the OCR to a cyclical trough of 1.50%.

.Hence the RBNZ will trigger a financially unstable residential property market bubble event. Should the citizens stand idly by, while a government entity driven by nothing more than an ideological set of underpinnings proceeds to decimate our society?

A financial security is nothing but a claim to some future set of cash flows. The actual "wealth" is embodied in those future cash flows and the value-added production that generates them. Every security that is issued has to be held by someone until that security is retired. So elevating the current price that investors pay for a given set of future cash flows simply brings forward investment returns that would have otherwise been earned later, leaving little but poorly-compensated risk on the table for the future. Read more

No wonder Mr Hisco is nervous about his bank's prime assets in the form of interest gathering residential mortgages collaterialised by overvalued wooden boxes.

Bring it on!

In Auckland the price is based on the potential in the land. The actual house itself is worth very little.

Life intimating art:

There was an interesting article in the Listener recently which described how Singapore brought down its house prices. Apart from using its Housing and Development Board to ramp up the construction and sale of units it limited mortgages to 35 years, it tightened loan to value ratios to 50% for those with one housing loan and 40% for those with two or more loans. Debt to income limits were also imposed. Stamp duty of 16% was imposed on those who sold a property within one year of purchase and those buying second and subsequent properties paid duties of 7% and 10% respectively with foreign buyers paying paying 15% stamp duty. Apparently after peaking in 2013 prices have fallen for 11 consecutive quarters and are 9.4 % lower than in 2013. The aim was not to crash the market. Our do nothing Government and RB are obviously wanting to crash the market.

Imagine the revenue we are losing in NZ by not imposing such levies..

All accurate but some points to note:

The Housing and Development Board is (generally) in charge of public housing. Foreigners (i.e. excluding permanent residents) are not entitled to purchase these. The bulk of Singapore's housing stock lies in public housing. The slowdown is much heavier in private housing which is open to all (but various duties will apply). Try to see what 1 million New Zealand dollars get you in Singapore in terms of private housing; you may find that you get value for money here.

NZ does not (1) have public housing (HNZ houses do not really count because they are nowhere the scale), (2) have the manpower capacity to undertake the building of high rises at relatively cheap costs (Indian/Bangladeshi/Chinese migrant workers anyone?) and (3) have the political will of the existing ruling and extremely dominant political party (or should I say, capacity) to undertake such construction without undergoing extensive consultation (see for e.g. the Auckland Unitary Plan that took 3 years to "finalise"). Such political will includes compulsory acquisition of land by the government at market prices.

In short, the markets are pretty different in terms of capacity, political will and the type of housing. I cannot see how NZ can ramp up capacity at the scale that Singapore can. Taxes can only go that far.

The point I was trying to make was Singapore DID something that actually worked and did not just tinker round the edges as our RB and Govt have done. Singapore's aim was 'to skew the incentives that reduced the demand for property'. While not everything that one country does suits another, some of what Singapore has done would suit NZ. For instance limiting the term of the mortgage, the debt to income ratio and I would put stamp duty for all but first home buyers as well as really really limiting interest only mortgages. New Zealand does not need a crash and unless Govt/RB does somethingt that is what will happen

Just to add on this topic, Singapore's HDB public housing are all

1) 99 year lease hold

2) Generally highrise (a lot 30+ storeys)

3) They are not as cheap as you think,

I just can't see Kiwi's buying into this concept of a house, at least in the near future. There has to be a big change of mindset to be able to roll out something like this on scale that Singapore did.

Exactly, KiwiSaver being used for buying a house is just another example of how we incentivise buying a house over all other forms of investment. All it has really done imo is inflate houses even more as all KiwiSaver people are competing against one another to buy the same house.

The government should give direct subsidy to FHBs and not through Kiwisaver, which is supposed to be for retirement saving. We got it all wrong, aye.

Yes. Land value is a completely elastic product.

At what point would high house prices cause Auckland to be a failed city? If another town in the north island suddenly had some industry and required a lot semi skilled labour what is to stop all the people living in car moving there for the chance to live in a house? What is so great about Auckland that people are willing/want to become debt slaves to live there? If average house prices hit $1.5mil you would be better off living in another part of the country and flying into Auckland every day.

From residential to investment to speculative, the progression of Auckland housing is very scary. Tax and raising the barrier for speculative activity (if not completely stopping it) is the only way. But there is absolutely no political, administrative or regulatory will for that.

To duplicate the facilities in Auckland in another place in North Island is not easy. There was a chance after the big quake in Christchurch to build a brand new city elsewhere, but that is gone now. It is back to square one there, with uncertainty about another big one always in the background.

May be outsourcing to China or the US will get us a brand new city which can rival Auckland in 10/15 years ?

If you had to save and pay 100 percent cash for a million dollar shack in Auckland, who would use their own money to do this, unless they knew they could get a good return on that money with capital gain and/or rent? many are in fact using cheap borrowing to do it, the Price for the house seems to be irrelevent, as long as they can afford to make the monthly payments. Banks are lending, because they say that if they don't lend, then another bank will, even though they are uncomfortable with the current housing market situation. It does show all the signs of a slow car crash.

The government has the power to fix this going forward tomorrow. But they appear to be spinning it out for the election. So they will come out with policies next year, by which time it will only be worse, and the average house price in Auckland will likely be 1.1 million.

Wait for the bubble to burst guys !! ... listen to BH , he is an expert -- who rarely gets it wrong ! ..... enjoy your weekend with this:

http://m.nzherald.co.nz/personal-finance/news/article.cfm?c_id=12&objec…

Wow hahaha~ Someone has proven to be the biggest white elephant in town! ...but wait he's no longer in town in Auckland, he's now a Wellingtonian trying to solve the so called Auckland housing crisis! Shameful.

Interesting to see that most of those who commented then are now absent on this site. Different times, different folks, different strokes, aye.

Maybe different "Smoke" too !!

Good one.

mmm, just like you have never been wrong in the past with any of your wacky comments.

I have never been a public commentator who has followers , sitting on TV panels ( as If) and have a website to promote biased political views and acts as an expert !!.... I just put my views and if wrong will say so ... not the end of the world ..... after all why are you so pissed off ??.. is BH your friend or role model?

Read the comments on his article in 2010 and see what people think of him and his predictions lol ... I wonder who believes those who cry Wolf every second day other than chicken littles !!

It has only continued because a useless, not working for NZ govt refuses to acknowledge the amount of or doing anything about, foreign money. I put it to you that if our housing "bubble" were due only to money rightfully in NZ, then it would have burst long ago, and given Hickey was probably basing his predictions on how things went in the past, he would have been right if things had gone the same way they had in the past.

BH wrote that article in good faith and with no intention of it being used as financial advice. Sure he was wrong about the forecast, but it wasn't some hastily constructed piece with little basis. You make it sound as if he has somehow wronged a nation by reporting facts and his logical conclusions to them.

I'm not pissed off, I just think its funny how you spurt out all the biased, slapstick, uninformed, and largely illogical stuff that you do and then attack someone who has taken the time to prepare and justify their words.

Given the information available "at that time" it was a valid "high probability" call

What he could never have anticipated was the 5 Federal Reserve spending spree packages

"I'm not pissed off, I just think its funny how you spurt out all the biased, slapstick, uninformed, and largely illogical stuff that you do and then attack someone who has taken the time to prepare and justify their words."

taken the time to prepare and justify their words.....but who is wrong. And badly wrong, and continues to be wrong. But he will be right one day...as they say, even a broken clock is right twice a day.

Sure, he hasn't been correct yet.

His premise still remains, however. That is, housing prices are unsustainable relative to the real wealth of Aucklanders.

Anyone who denies this is just plainly stupid. The moment immigration is turned off or overnight rates rise we will see a lagged correction in the market. There just is not enough liquidity to sustain it without these facilitators.

"Sure, he hasn't been correct yet.

His premise still remains, however. That is, housing prices are unsustainable relative to the real wealth of Aucklanders.

Anyone who denies this is just plainly stupid. The moment immigration is turned off or overnight rates rise we will see a lagged correction in the market. There just is not enough liquidity to sustain it without these facilitators."

OK. You can continue to be right and wait. When property prices correct 50%, be there to buy them all? Or is the correction still insufficient?

Yet ?? Haha, yeah he will get it right one day ... just like lotto have to be in to win I suppose!! , one day!! ....

The problem is not with the work he's done and data available at the time - the issue is with reading , interpreting and forecasting using that data using some COMMON SENSE instead of wishful thinking.

... He had never got it right for the last 10 years and he just does NOT want to back up the truck because apparently he has a certain ideology and reads a lot of text books and selective stats and his bias is very obvious ( just like his other mates) ....

Common sense dictates that market should NOT be allowed to drop beyond a reasonable amount ( maybe 10 - 15% from here) because that HURTS everyone ... and it ALSO dictates that Housing prices should NOT be allowed to run away like they did in the last 3 years ( because of continued demand in the next 2 years) for the same reason - this rate of rise needs to be slowed down to say 1 - 5% Max pa until supply catches up or the world economy ( not the Government !!) allows interest rates to move up again .... and it looks like that will happen slowly in the next 2 years. So here is the tough balance that the Gov ( Any Government !!) has to keep and work hard in using all the tools it has -

No one can close the immigration tap in this shonky world economy ... even Labour is just calling to slow it down a bit ( just playing with numbers to be seen as opposition) !! That is Common sense too ..... at the moment!!

So don't get pissed off from contrarian opinions mate.

as I said before : I am entitled to MINE as you are to YOURS .. time will prove us right or wrong ---

Perhaps it is only continued ShonKey immigration intensity that prevented the BH prediction or something of the same trend materialising.

Then of course there is the ShonKey soft or nil money laundering policies.

There is nothing more certain about any forecast than the ultimate result will be wrong.

Auckland mortgage debt has risen 550 percent in past 15 years.14 percent per annum. Thankfully we have low interest rates, and the RBNZ has not introduced DTI yet.

The situation regarding runaway house prices in Auckland is much worse than the OECD data suggests. Why? It completely neglects the quality aspect.

An average house in nothern continental Europe for example comes with a basement made of steel reinforced concrete, centralized heating, triple glazed windows and properly isolated brick walls. The expected lifespan of the building structure is well over a 100 years.

Comparing the wooden, leaky, drafty shacks marketed to us as "dream homes" in New Zealand to modern buildings elsewhere in the world is not even a case of comparing apples and oranges. It's more like comparing a bicycle to a top of the line BMW and suggesting the bike should cost more because it's made in New Zealand...

"It's more like comparing a bicycle to a top of the line BMW and suggesting the bike should cost more because it's made in New Zealand..."

Sounds like lots of stuff here actually.

Super Mario,

From my own limited experience,I can only agree wholeheartedly with your comments.I retired here from Scotland in 2003. Every house I owned there from 1969 on,had double brick cavity walls,proper insulation,central heating and double glazing and these were not flash mansions,just ordinary houses. I had never heard of leaky homes till I got here. My younger son and family have a home in Meadowbank built in the 70s. It's now 'worth' approx. $1.40m and they have already replaced the leaky deck and will soon replace the entire roof.Indeed, they are going to knock most of it down and rebuild.

The standard of building in NZ is a bloody disgrace and don't get me started on estate agents. Why are Kiwis prepared to put up with this crap?

I appreciate that interest.co.nz now go on record and say we are 2nd highest in OECD income to debt, as what they were saying before was all countries which was total BS as OECD is only 20 countries...

You too are wrong... OECD is 35 member countries

I appreciate that interest.co.nz now go on record and say we are 2nd highest in OECD income to debt, as what they were saying before was all countries which was total BS as OECD is only 35 countries...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.