By Gareth Vaughan

Some years ago I wrote numerous articles featuring Australian company Toll Holdings. This was when Toll was acquiring New Zealand's struggling rail operator, then known as Tranz Rail.

At the time Toll was on an acquisition binge. In Australia Toll managing director Paul Little was sometimes referred to as a deal junkie. And he even married his investment banker.

If Little was a deal junkie then his counterpart at Chinese company HNA Group is the King Kong of deal junkies.

HNA is the company the Melbourne headquartered ANZ Group announced in January had agreed to pay NZ$660 million for New Zealand's biggest finance company, UDC Finance, which has total assets of about $2.7 billion.

ANZ has said it expects the deal, which needs Reserve Bank and Overseas Investment Office approval, to be completed in the second half of 2017. From HNA, in NZ, we've so far heard nothing.

From the perspective of UDC's 175 staff, its borrower-customers, depositors/investors, and the NZ financial services sector as a whole, just what will HNA bring to the local market?

On its website HNA Group describes itself as a conglomerate founded in 1993.

"It [HNA Group] has created a miracle in the business community over the past two decades, successfully transforming from a traditional aviation enterprise to a conglomerate, and expanding from Hainan Island to the globe," the website says.

That HNA has been on a global acquisition binge is an understatement.

Here's a selection of headlines derived from a Google news search of HNA Group on Friday afternoon;

China's HNA Is Buying a NYC Office Tower for US$2.21 Billion (Or more than US$1,220 per square foot).

Australian office towers anchor AEP deal with HNA Group

HNA Group To Invest In Asiana Parent

HNA Group pays HK$7.44 bn for fourth plot of land at Kai Tak

HNA's Hong Kong-listed unit reports net annual loss of HK$21.9m

China's HNA Group plans to hike Deutsche Bank stake

Going back further, a Bloomberg article from April last year noted;

Will any company that's not had a takeover bid from China's HNA Group over the past year please stand up?

The Bloomberg article concluded;

As we've seen with Anbang Insurance's recent shopping spree for offshore hotels and financial businesses, the usual financial constraints often don't apply when it comes to well-connected Chinese companies following Beijing's push to invest globally. So there's no reason to look a gift horse in the mouth if HNA turns up at your headquarters waving a checkbook. But it might be as well to ask for cash.

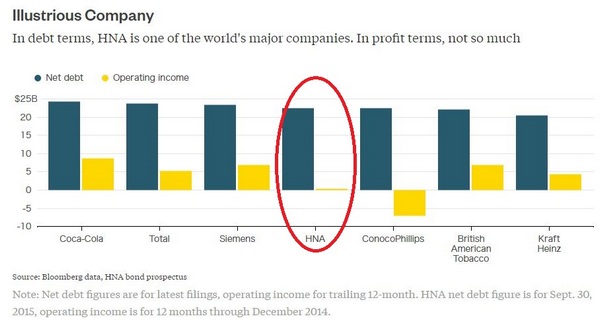

The 'ask for cash' quip stems from HNA's debt position, highlighted in the Bloomberg article by the chart below.

A sinking credit rating

Credit rating agency S&P Global Ratings has detailed that it could potentially downgrade UDC's long-term rating as low as B+ if the sale to HNA Group is completed. S&P currently has UDC at BBB, having already downgraded the finance company from the AA- rating it had, which was equalised with parent ANZ.

The red oval in the table below highlights the 10-notch extent of the possible S&P downgrade. Already UDC has gone from a strong investment grade rating to a low investment grade rating, with the potential to drop to a "junk" rating. This, of course, has implications for UDC's borrowing. Should the firm's debenture programme continue under HNA ownership, depositors should expect significantly higher interest rates to match the much riskier business they're lending money to. (You can see credit ratings explained here).

Some clues

Looking at HNA's group profile, there's an entity called HNA Capital Holding Co. Ltd. It's described as "one of the six cores" of HNA Group. HNA Capital, apparently, provides "comprehensive financial solutions" via its investment banking services, plus "combinations and innovations among diversified financial instruments."

Furthermore, HNA Capital "aims to build itself a world-leading integrated operator in international investment banking and modern financial services industry, undertake the responsibilities of both regional and national economic development, and create a financial consumer market with vast potential."

According to the website HNA Capital's businesses/services include investment banks, leasing, trust, insurance, securities, banking, futures, funds, guarantees, factoring, and small loans.

In a recent interview with Forbes Adam Tan Xiangdong, CEO of the group and chairman of HNA Capital, had the following to say;

We are a 23-year-old company. We have confidence to invest outside of China, and I still think this is a right time to invest, because China has a $3 trillion reserve. Also, the government supports people to go abroad. For our strategy we have airlines and tourist groups. We started from that. Then we have a logistics group and a big financial services sector. We call airlines and tourists people's movement. For logistics, we talk about all the goods movement; for financial services, we talk about capital movements. So for anything related to these three parts of business, we are going to keep moving forward. We have 300,000 employees: 100,000 Chinese, 100,000 Europeans and 50,000 Americans; the other 50,000 are from the rest of the world. So we are an international conglomerate, which happens to have a Chinese origin.

And a recent Reuters article had this to say;

After a spending spree stretching from hotels to electronics distribution in 2016, Chinese conglomerate HNA Group says it is now investing in financial services, betting on asset managers and consumer finance for growth at home and overseas.

The owner of Hainan Airlines Co inked about $20bn in deals last year, snapping up a stake in Hilton Hotels and investing in catering and logistics firms – spending that raised concerns the group was borrowing too heavily and spreading itself too thinly. With more than $100bn in assets, investments this year have included a hedge fund platform, a New Zealand lender and a 3% stake in Deutsche Bank.

The moves reflect a broader push by China into financial services globally as Beijing encourages its corporate sector to expand overseas, although they face increased regulatory scrutiny in the United States and Europe.

Additionally the Reuters article noted some possible attractions for HNA in taking over UDC;

In HNA’s latest deals, it bought a large stake in hedge fund platform SkyBridge Capital from Anthony Scaramucci, a high profile supporter of US President Donald Trump and spent $460mn on New Zealand’s largest non-bank lender UDC Finance.

Two people with knowledge of the matter said HNA is bidding for UK-listed insurer Old Mutual’s $900mn controlling stake in its US asset management business. HNA declined to comment. Both SkyBridge and UDC Finance, which mainly provides car loans and equipment finance, offer stable revenue, while allowing HNA to increase yields by borrowing in the institutional market and lending in the retail market.

The Auckland-based company also boasts a management system that HNA could potentially utilise in China, where consumer finance is blossoming from a low base.

Still HNA’s rapid expansion has prompted concerns it is spreading itself too thinly. “The real risk for HNA is a loss of strategic focus,” said Brock Silvers, founder and managing director of Kaiyuan Capital, a Shanghai-based investment advisory firm. “Their plan to build a financial empire takes a lot of human capital, resources and time.” Carol Yuan, an analyst with Aberdeen Asset Management, said she was concerned with HNA’s debt, which can sit anywhere in the group financial structure and can be issued by any part of the group. “It’s hard to get comfortable around how they manage risks,” Yuan said.

A successful, conservative business

UDC is known for the financing and leasing of plant, vehicles and equipment, mainly to small and medium sized businesses across NZ. Give this, UDC is something of a barometer for the economy, posting a record net profit after tax of $58.5 million for the year to 30 September 2016, a 3% increase on the previous year.

It's also a non-bank deposit taker with $1.46 billion worth of secured deposits outstanding as of December 31, with $2.76 billion worth of assets pledged as collateral against these. As David Hargreaves reported last week, as part of the ANZ-HNA deal, there'll be a meeting for the 13,500 UDC debenture holders to vote on winding up the finance company's existing debenture plan. UDC also currently has a $1.8 billion loan facility with ANZ.

UDC has been around a long time. The company celebrated its 75th anniversary in 2013 noting it "financed the first Masport motor mower and the first commercial Hamilton jet boat," having started life as Financial Services Ltd in 1937.

This longevity, of course, means UDC survived the meltdown of the finance company sector. Then-CEO Chris Cowell told me in 2010 UDC had survived by sticking to its knitting. UDC had not financed any property development, but rather the company, fully owned by ANZ since 1980, had continued to finance plant, equipment and vehicles. Added to that was funding support from ANZ and governance, risk management and liquidity risk forecasting which mirrored its parent, Cowell said.

Now it's proposed that this successful, conservative business, working in the SME heartlands of NZ's economy and borrowing money off ma and pa, will be taken over by a debt-laden Chinese conglomerate behemoth. A key question here is just what will HNA bring to the NZ market as owner of UDC? And how will HNA add to, and improve, UDC?

When a business changes ownership it's always a nervous time for staff, customers and competitors. It's fair to say that with UDC facing such a drastic ownership change, there should be plenty of nervousness swirling around this one.

*This article was first published in our email for paying subscribers early on Monday morning. See here for more details and how to subscribe.

7 Comments

Should the firm's debenture programme continue under HNA ownership, depositors should expect significantly higher interest rates to match the much riskier business they're lending money to.

Should ANZ 30 day term depositors expect more than 50 bps to compensate them for stated credit risk and OBR haircut liabilities?

Furthermore, ANZ O/N deposit rates collapse to 10 bps, which according to the RBNZ represents a seriously large segment of banks' collective national liability base.

That's a scary chart. Over 80% of deposit funding is under one year. Is the Core Funding ratio another deception played on the people of New Zealand by their [potentially libellous word removed, Ed] Reserve Bank?

Under the RBNZ's BS13 (Liquidity Policy) Table 2, overnight on-call deposits of less than $5million contribute 90 cents to the dollar in core funding. It is a ludicrously large weighting, but reflective of the fact that depositors really don't have much choice as to where to put their on-call money given all NZ's banks are like reef fish, all seeking to avoid standing out one from the other.

And what proportion of those deposits have been created by the banking system itself conjuring up "money" by writing mortgages against residential property. In the fiat system everything is mercurial.

As always the sale poses more questions than we have answers for.

HNA is a setup I have never heard of before , but given its claim of size and scale is certainly not some chump change operation

I am left wondering just how the valuation of $660 mln. was arrived at and whether it is fair value for ANZ Shareholders ?

Also , apart from unloading some debt on its Balance sheet what are the benefits for ANZ ?

I assume the $1,8 billion ANZ loan facility is going to be substituted with an Chinese Government / HNA loan facility using the Chinese Government reserves on which they are currently earning Zero or close to Zero ?

The next question is the ownership of HNA , which I assume is a Chinese SOE of sorts.

Who owns HNA ?

A clue is reference to the $3 Trillion in reserves that "China " holds............ thats Government money held in the Central Bank (PBOC) , and does not belong to HNA, and the blurb seems to suggest they have access to this money .

Ignoring turnover , or assets , having 300,000 employees worldwide makes HNA bigger than Citibank and about 90% the size of HSBC by number of employees.

This implies that HNA has serious scale, so who exactly are these people ?

Locally , UDC does asset finance at rates from around 8% to up to 14% ( and while it has onshore funding its cost of Capital is way lower than retail banks as I understand it can source funds offshore )

UDC's lending book is good ( non-performing debt is low ) and loans are often secured by cross-collaterel with other assets , so its a sound business model , and must add substantially to ANZ bottom line .

What is really at play here , is there more to this story?

Are they wanting to downscale their US$ holdings and diversify, or is it something else ?

I have strong suspicions that this is colonization by stealth , and China is not a country you want to have as your master controlling your assets , your banks and financial institutions , or your farms .

They have said there will be no job losses ............. really?

What about natural attrition and ongoing restructuring as is commonplace in big banks ?

Will these folk be replaced with Kiwi's ?

Lets not forget , their minimum wage is nowhere near ours , so relatively well paid NZ back office jobs are going to China , like it or not .

Is this the thin end of the wedge or am I way off the mark ?

@BOATMAN

HNA also just bought Ingram Micro - the world largest technology distributor earlier this year. They are on an acquisition binge....but yes, who are they....really. Is it the Chinese Govt in disguise...?

These companies come along and seem unstopable in their quest to gobble up everything in site. Eventually it all blows up and they crash. E.g. Ariadne, Tyco and a bunch of others.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.