The following article is the second chapter from Progressive thinking, ten perspectives on housing, a Public Service Association (PSA) publication. Interest.co.nz is publishing all 10 chapters from different authors on various aspects of housing.

By John Tookey*

Housing in New Zealand is in trouble in so many ways. Quality, cost and sustainability all have roles in the discourse. The critical issue, both locally and nationally, is the Auckland affordability crisis creating economic instability.

How did we get here and where next? The culprits have all been paraded before the demos - builders overcharging, lack of competition in materials, foreign investors, property speculators. Everything up to and including “A big boy did it and ran away”. So why this mess?

Technology

In 1965, Intel co-founder Gordon Moore noticed the number of transistors per square inch on integrated circuits doubled annually, whilst the price reduced. The eponymous “Moore’s Law” has become our benchmark expectation for product performance ever since. The phone or computer you use gets ever more capable, and our performance expectations grow in lockstep. Your phone now does email, photography, storage and route finding with GPS.

By contrast, what has been happening in the building industry over the last 50 years? Not much. Houses are built as they were, using the same materials, trades and taking the same amount of time.

Construction productivity flatlines at $34/hr added value compared to a national average of $48/hr, with innovation 10 per cent below the national average. Consequently building new is growing in expense, irrespective of economies of scale. We build approximately 7,200 dwellings per annum against demand of 14,000 per annum for the next 30 years.

The only way to meet housing needs would be to double labour productivity through innovation, or double our total workforce in house building. Since we do not have a transient labour force of skilled workers as in Europe, productivity through technology is where we need to invest.

Housing types

‘Affordable’ houses are more expensive to build pro rata than larger properties. Typically, affordable homes are two or more storeys and attached rather than detached.

The scaffolding and other technical requirements (thank you Health and Safety Act 2016!) lead to a cost of around $3,400/m2. Conversely large single storey houses are $2,000/m2. The result? Affordable homes are affordable to the end purchaser, not the builder in the value chain.

Why would a builder build lower margin housing for the public good if not compelled to do so? New homebuyers tend to specify the largest possible house on their section in order to incorporate the maximum residual value for themselves.

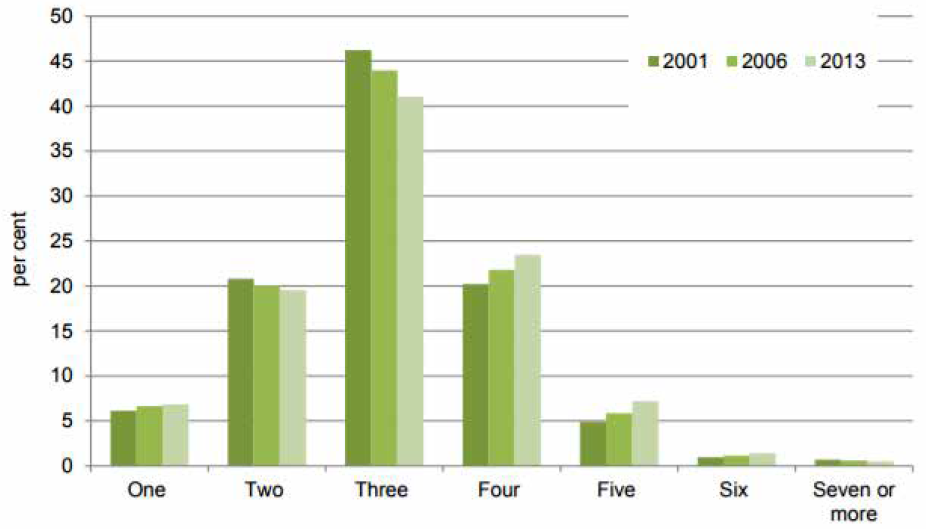

Thus we see census trends in house building showing increases in four to five bedroom properties being constructed, while affordable two to three bed units are in decline (Figure 1). In short, the market is driving the wrong outputs at the wrong end of the market.

Special Housing Areas (SHA) fail to change these trends, with standalone sections developed first and affordable housing developed last. Indeed, 56 per cent of SHAs have been de-established.

Fragility

Our housing industry is literally a cottage industry: 98.5 per cent are single person, ephemeral companies subsisting from invoice to invoice, using credit lines to stay liquid.

Their risk profile requires spreading their effort over several projects simultaneously to maintain turnover.

This industry corpus increases production scale without recruiting more tradies and increasing their risk – hence costs climb with demand. They are inefficiently organised with poor bargaining power compared to group builders.

Figure 1: Bedrooms per dwelling in Auckland 2001-2013 (StatsNZ, Census 2013).

Most therefore fear the boom-bust cycle. Altruism for homebuyers is inconsequential amongst their priorities. Builders take only the work they can manage to limit exposure to the ‘bust’ cycle, thinking in terms of three to five years until the downturn – but indicators are already appearing.

Land

Land supply is core to unaffordability, but the assumption that more land being released and consented more cheaply and rapidly equals more housing more quickly is fundamentally flawed.

This is only true if industry capacity is scalable to demand and the market operates perfectly. ‘Material availability’ doesn’t automatically deliver higher production rates. Land improvement/preparation capacity is as constrained as housebuilding.

Doubling available land will not double the number of land developers or their capacity. Imagine a car producer received an additional million tonnes of sheet steel at their factory at zero cost. Will more cars be produced? No.

A more likely scenario is optimised production to factory capacity, retaining the current selling price, margin and brand value. The problem is exacerbated because before land is ready for housebuilding, costly infrastructure, drainage and improvement is required - consequently it is a tough, cash-intensive, industry to enter. Once again we expect industry to absorb the cost and risk of delivering societal needs when increasing production forces down sale prices for all producers. Is it reasonable to expect markets to deliver societal needs then be shocked when they function in their own interests?

The future

Einstein said: “We will not solve the problem by using the same reasoning that created the problem”. By contrast, current government thinking on land availability is the equivalent of Captain Blackadder anticipating the plan for the next offensive: “It’s the same plan as last time and the seventeen times before that.”

Blackadder economics from government will not cut it this time. Land release and Special Housing Areas (SHAs) are not solving affordability issues since social outcomes are not compelled through ‘use it or lose it’ clauses, or incentivised through additional profit.

Compulsion (or profit motivation) in land development is required if we take affordability seriously. We need incentives to use prefabrication to increase productivity.

Why not specifically fast-track consenting for prefabricated housing? Why not make consents zero cost for two to three bedroom housing and double or triple current rates for four to five bed housing?

If this is a national crisis, why not create a national prefabrication plant producing inexpensive kit-set housing with preapproved building consent for generic designs?

How about incentivising landlords to sell off their buy-to-let investment properties? Imagine a scheme where landlords agree to divest their portfolio so they can place their capital gain tax free into KiwiSaver - provided they commit to not owning directly or indirectly investment property in the future.

Imagine genuine state housing (not mortgage assistance schemes) delivering the two to three bedroom housing we need, rather than expecting industry to deliver this category of homes with lower profits and higher risk?

Ultimately government should accept the seriousness of affordability. Blackadder economics and wishful thinking will not magically change what is and is not profitable for the housing industry to build.

We are at a tipping point for the New Zealand economy. The electorate knows it. The question for government is whether laissez-faire ideology or pragmatic intervention will win the debate.

Either way, decisive action is required now.

-----------------------------------

*Professor John Tookey is Director CUBE-NZ, at Auckland University of Technology’s School of Engineering.

Note: The views expressed in Progressive thinking, ten perspectives on housing belong to the authors and do not necessarily represent the view of PSA members or the organisation.

56 Comments

NZ can free up as many sections as it likes. There are 3 billion people on our doorstep ready to arrive and/or buy a house.

Free trade, free immigration, free property buying, = NZ is highly prized, so property shortages and hyperinflation of property will continue regardless of a few more sections rolled out.

As long as government only talks about supply ignoring demand side their will be no solution. Supply and Demand both have to be tackled and for that any solution may be possible only with change of government.

A Capital gains tax is a very strong incentive not to build more dwellings or make other capital improvements. This is despite it being easy to avoid.

CGT only applies to profit. First you have to make a profit and if you make a big profit you can smile as you pay it. Not like my son paying income tax on the $150 per day he is earning - has to pay it even if it means no new clothes and cheaper food. As you say fairly easy to avoid and also very marginal as to the amount it raises. Just not worth worrying about.

Based on this logic, income tax is a strong incentive not to work

"We are at a tipping point for the New Zealand economy. The electorate knows it.

No, it doesn't!!!!

What The electorate knows is that:

1) Lower phone prices is good

2) Lower petrol prices is good

3) Lower taxes is good, and

3)Higher property prices is good

The electorate has been brain-washed and until it gets hurt, it won't know anything other....

3)Higher property prices is good

Disclaimer: If you were born at the right time. Your mileage may vary.

Quite right. I recall my parents agonizing for months over buying a specific replacement home. It was going to cost them.....$17,000....and they would need a $7,000 mortgage to fund it. Seems quaint now, but they made the move, and I recall them having 'buyer's remorse' for some time after. Now, of course, it would probably be worth $1.7 m, and yet any buyer today wouldn't blink twice at lashing out the asking price and feeling elated that "they own (more) property!"

Today, people buy a $1,000 phone and get Buyers remorse ( "It does the same thing as my last phone!") or a new $3,000 computer ( ditto) yet have no emotional or economic fear of expending $X on a house because 'property always goes up'. It has and it may. But I recall one of the founders of Billabong (surf wear) being laughed at when he sold his stake for $7.50 per share and it then went up further. Last I saw Billabong was worth 44 cents..... All things come to an end. Irrationality being the main one....

All things come to an end. Irrationality being the main one..

Not according to behavioral economists such as Daniel Kahneman (Nobel prize winner and important thinker on asset bubbles). Irrationality is pervasive.

Emotions rule over rational decision making most of the time. Even when people think they're being rational; for example investing in property because recent history shows it's the best investment over time, that decision is not really rational. It's actually dictated by emotional gratification.

I find your comment very confused. In the 1st part you show how property goes up, then you talk about consumer goods and you finish by saying "all things come to an end". What's the point you're trying to make ?

There are far too many supply constraints in NZ for any government to roll out a major house building programme.

After taking a breather, house prices are set to increase again - especially well-located houses in densely populated areas, such as the inner-city suburbs of Wellington and Auckland.

NZ is an increasingly popular place to reside, internationally. (Demographic indicators provide a very good clue here.) Notably, the upswing of 2014-16 had structural origins: it was not merely a cyclical event.

"There are far too many supply constraints in NZ for any government to roll out a major house building programme."

Rubbish.

Any government could fix that, if they had the balls.

The moment you added another supplier into the fold, watch Fletchers' materials lead drop like a stone.

Houses aren't difficult to build. We just make them difficult to build for some retarded reason. Sure, we need land, but there is plenty of that in Tauranga and Hamilton.

"Notably, the upswing of 2014-16 had structural origins" - what were these 'structural origins'?

Hi nymad,

Skilled labour in the building trades is in desperately short supply in many parts of NZ - and there's no easy or quick fix for any government.

Get real nymad - your head is in the sand.

Also, if you don't know the difference between cyclical and structural factors/origins in investment, then you know less than the average high school pupil learning economics or accountancy. Go read any textbook on investment. It's very basic (and important) stuff!

My question was

"What were these 'structural origins'?

Tell us some of the structural factors as we can all be as enlightened as you. As everyone here knows, you are so great at supporting your comments/arguments, so I just want some supporting justification.

As an economist, I'd like to control for some of these structural factors in my models - given you know so much about the subject of econometrics, the reasoning for this will be evident.

As for the supply shortage of skilled labor, that's a creation of our own failing.

The only demand we have is for cheap labor due to the issues with materials supply and implicit cost. i.e. the inefficiency in materials supply means we have to increase the human capital. You know a standard Cobb-Douglas function, right?

Reduce the lead time of materials production (easy, as our suppliers aren't running at capacity), introduce innovation in the building sector, and reduce implicit taxation - the result of thatis we will see demand for cheap labor decrease significantly, along with the associated increase in overall productivity.

That is an easy fix. It's called stimulating competition in the market.

hi Nymad,

There's no point showing off about your knowledge when the evidence suggests you actually know very little.

Go and read a book on investment principles/analysis and that way you will become better informed. Go find out about the difference between cyclical/structural. Go find out about supply constraints in labour markets - and labour mobility/flexibility across the short & long runs etc. Then read the empirical literature as well - including the international studies.

Just as good information is a prerequisite for efficient markets, it's also a pre-requisite for meaningful debate. (If you really are an economist, you should know about this.)

Okay seeing as you are still oblivious to the key point, I'll quote myself again.

"My question was

"What were these 'structural origins'?

Tell us some of the structural factors as we can all be as enlightened as you. As everyone here knows, you are so great at supporting your comments/arguments, so I just want some supporting justification."

And, I'll quote you currently

"Just as good information is a prerequisite for efficient markets, it's also a pre-requisite for meaningful debate."

If you can't answer my simple question, it seems you can't even take your own advice...

Structural/cyclical phenomena in property markets/analysis has been dealt with umpteen times in this blog - and you've been here long enough to know about it. Plus, there are a multitude of other sources on the subject.

Go read the previous contributions here - and the literature (both theoretical and empirical) elsewhere. No point in talking with you further, until you've got yourself up to speed.

If you have done the research, it should be really easy for you to just tell me a couple of factors.

That's all I want.

An answer to my original question.

Oh somad nymad.

nymad has no clue what he's talking about

You don't know what you're talking about nymad

You can troll all you like Yvil, it's not going to make house prices magically rise again any time soon or even in the next few years.

You're absolutely right tothepoint. Here's the latest Market Update in Auckland! as you can see, there are no issues with achieving high house prices especially if your suburb is near the CBD.

https://www.youtube.com/watch?v=ao9X9Cd7_Nk

Hi DGZ,

Thanks for that - but I take anything produced by a real estate agency with a grain of salt (as I'm sure you do also). When material such as this comes from an independent source, it has much more credibility in my eyes.

But I'm not saying B & F is wrong/misleading/deceptive etc. It's just that I feel I can't be sure, because there's an obvious conflict of interest with real estate agencies, who I find will put a positive spin on almost anything in order to promote sales - and their commission. (They seldom say anything that's not in their own best interests.)

What I can say is that I know several people who are looking for houses (not apartments) in Auckland Central right now - and they all say the same thing: good houses are few and far between. They're finding house-hunting to be arduous and unrewarding at the moment - and are very vocal about it! Of course, my comments in this paragraph are purely anecdotal - but they do sort of align with what B & T is saying.

Anyway, if prices do come crashing down in spring/summer, I'll be in with a grin. Would love to find a bargain in Ponsonby.......

Thank you for your insight tothepoint.

Here's a Freemans Bay villa for you, and a DGZ paradise for me:

http://www.trademe.co.nz/property/residential-property-for-sale/auction…

http://www.trademe.co.nz/Browse/Listing.aspx?id=1399841762

Hi DGZ,

Thanks for the links.

That Freemans Bay place looks gorgeous!

Hot location too.

How much do you reckon it will sell for?

Thanks again.

I think around $1,550,000. All the best!

I live in Ponsonby, that Freeman's Bay house is a $2 million house all day

Yeah, the CV is 1.63M so should fetch around 2.1M.

"Einstein said: “We will not solve the problem by using the same reasoning that created the problem”." Exactly, and the comments above illustrate the same old thinking that has created the problem!

Our Governments, irrespective of colour, are too wedded to the globalisation - free market model economic theory, and refuse to accept that the only answer left is regulation. Regulating rental prices, regulating against foreign buyers, regulating against land banking and so on. BUT balance is required, too much regulation also adds to cost - the effects of the H&S Act is one example.

None of the parties seems to understand all this so nothing will happen thus as we are always doing what we have always done, we will always get what we have always got!

It's actually the ruling powers' fear of change and the fear of going against the grain. Most of them are little more than people tied to a managerial mindset. Dime a dozen with the chutzpah to put themselives up for election. They're not really leaders in the sense of forming vision. Adam Curtis explores this in depth.

Completely disagree with the conclusion on land supply. Doubling the amount of land available DOES reduce the price of land, even if the capacity to build and develop does not exist.

The whole point of land banking is being able to drip feed supply and your buyer having very few options available to them. If the urban rural boundary is removed, and a land banker digs their heels in, a buyer/developer can simply say fine, we'll go another 1km out from the city or another 1km sideways and leave the land banker to it. It removes the scarcity completely.

That's not really what they were saying.

They are saying that doubling land availability doesn't double land development, which is logical.

Imagine a car producer received an additional million tonnes of sheet steel at their factory at zero cost. Will more cars be produced? No. A more likely scenario is optimised production to factory capacity, retaining the current selling price, margin and brand value.

No, their car example suggests the car retains it's selling price. Using this analogy, if you have double the steel available, the price of steel is lower, and the cost of each car is lower. Even if the same number of cars are being produced.

Exactly....Production isn't increased by increased supply when constraints are binding.

This is what they are arguing.

They do complicate it with an example of a good that isn't priced at the margin.

Thing is, it is possible to increase the capacity to build, and it doesn't have to require offering residency as a bribe.

I would like to ask those who comment on interest whether they are expecting a recession or not?

If not, why are you not expecting one?

If so, whether you think this should be an important consideration for what you do with your money in the short/medium term?

If you look at this treasury graph, showing a recession in NZ occurring at regular intervals, between every 6-10 years since the 1960's it would seem reasonable to assume we would be expecting a recession any time now. If/when one arrives, how will this affect migration? How will this affect house building productivity? Land availability won't much change, but with the veritable butt tonne of household debt NZ is swimming in, surely this will affect housing inventory and supply/demand?

http://www.treasury.govt.nz/economy/mei/nov13/03.htm/mei-nov13-09.gif

{kind=link}

I think we have a high chance of recession next year; the reversal of high private debt growth will be the catalyst. We have had an economy juiced up on world record immigration and a 30 thousand million injection from private debt growth; with sliding house prices expect that to shrink. With rising unemployment there will be less inward immigration (unless the rest of the world is even worse!) and it would be political suicide to allow it regardless of pre election positions. A worldwide recession triggered by Chinas (and Aussie's own) debt bubble would impact Australia so maybe more returning kiwis but clearly debt growth representing one dollar in nine and running at triple the nominal growth in the economy is not remotely sustainable.

I don't think the question is whether or not there will be a recession, as one will happen eventually. The real question is how resilient Joe Average Kiwi is when one occurs. Going by the amount of private debt tied up in housing, I'd say not very. If NZ had an Ireland-esque recession/depression imagine what it would do to the country.

Not a recession - a crash. Things will go up (ie "growth will be pursued at all costs") until something gives & then it gets ugly... the future can not and will not be a repeat of past trends ...

https://medium.com/insurge-intelligence/whats-really-driving-the-global…

Not a recession - a crash. Things will go up (ie "growth will be pursued at all costs") until something gives & then it gets ugly... the future can not and will not be a repeat of past trends ...

Yes, that is what happens in most crisis. People are blind to what actually occurs and there is no shame in that. Regardless, the ruling powers and the media will explain what happened and frame the reasons for the event occurring with their own narrative. The sheeple, on the whole, will accept that narrative as the underlying reality. They will then play down periods of exuberance (like we've been seeing on an unprecedented scale) using why now is different to the past (NZ is or was not exposed to instability to the same extent as other countries) while at the same time explaining now by the past (house price inflation has been seen in the past, therefore it is "normal").

The reality is that the ruling powers are bricking themselves and doing their best to appear that they're comfortable in their own skin. If you used a facial recognition tool to read the emotions of Bill English and Amy Adams, you'd get the picture. Steven Joyce does the best outward experience, but that means he either is blind to the myriad of obvious risks or either stupid. I don't think he's stupid.

There will only be a recession if there is a change in government

Recession or not. Yes - recession. a. Housing bubble leading to the inevitable - which has already started. And the subsequent shrink in spending due to the negative wealth effect.

Also financial markets also are well topped out with unsustainable PE ratios. Same outcome.

We are sitting right on the boarder of recession at the moment. Its not a question of whether to expect one but more of how can we avoid one!

Two quarters of negative GDP/ CAPITA have just occurred.

Some would say we are in recession already.

Recessions are good in that they pave the way for purging trash from the market place.

Good old-fashioned market discipline is the best/quickest way of sorting the wheat from the chaff.

Property is an excellent asset to have in a recession (provided any debt is manageable) because although it can fall in price, it always bounces back.

PSA - j-accuse of Plagiarism. Of an admittedly damn fine idea:

Why not specifically fast-track consenting for prefabricated housing? Why not make consents zero cost for two to three bedroom housing and double or triple current rates for four to five bed housing?

If this is a national crisis, why not create a national prefabrication plant producing inexpensive kit-set housing with preapproved building consent for generic designs?

My extensive blog history http://waymad.blogspot.co.nz/search/label/Housing

The fast-track consenting is already here - 'MultiProof' - it just needs take-up: https://www.building.govt.nz/building-code-compliance/product-assurance…

..consents zero cost.. good luck with getting cash-strapped TLA's to budge on That one. They have splurged on so many 'four well-beings' fluff categories, which now cannot be walked back without severe electoral consequence (i.e. getting tipped out on their arses), that any non-Rates-Revenue-Required activity fees are their only electorally safe way of jacking up their incomes.

a National Prefabrication plant - er- yes, but only if it's staffed by non-unionised Robots and lotsa clever software. Otherwise it's the Railway Workshops or the State Mines all over again - perfect hostages to stroppy unions with zero comprehension of the Wider Good. No offence meant, of course, PSA members....but History is a Stern Mistress.

"We build approximately 7,200 dwellings per annum against demand of 14,000 per annum for the next 30 years." Where was this 14,000 per annum for the next 30yrs figure dreamt up? More flawed analysis based on flawed assumptions by another academic body with no real world knowledge. A rise in interest rates will tank the market and 2,000 houses pa might end up being too many. All these academics are still advocating more QE even after it has failed for the last 10-12 yrs in Europe and Japan, yet these clowns keep steering the Titanic towards the iceberg.

I profoundly disagree with this article, right from the opening statement saying "With NZ at a tipping point..."

Lots of very interesting comments , NZ may or may not be at a tipping point but if history/economic cycle follows its course the global economies have existed on booms and busts . Mostly created by allowing house inflation to get out of control which infers housing is the greater cause of our problems .

Ludwig

You may have any opinion you like of academic credibility or otherwise. However this is not the ramblings of some left wing academic with no real world experience. The policy points made in the original piece (full report is called "The mess we are in" found here https://thepolicyobservatory.aut.ac.nz/__data/assets/pdf_file/0005/7508…) and this truncated version have citations associated with them. Editors and publishers take them out because they become 'overly academic' and therefore not accessible to the public. As a result everything becomes 'pie in the sky' by commentators such as yourself. The 13000-14000 per year figure is actually from the Auckland housing accord - copy available here http://temp.aucklandcouncil.govt.nz/sitecollectiondocuments/aboutcounci…. Generally it is taken is a true figure of the shortfall in housing provision and is quoted widely such as http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=11874620 and here http://www.stuff.co.nz/business/89336116/NZ-needs-60-000-more-homes-ANZ… for example.

The issue we have with regard to current shortfalls and the numbers quoted, as well as the years over which we will have to deliver the extra, is related to trying to get on parity between supply and demand to stabilise the situation. In other words we have to build more than the annual needs in order to make good on the shortfall last year..... and the twenty+ years before.

Good article John. It seems there are a number of attempts to build pre-fab housing. The next govt need to incentivise these guys. Pre-approved consents, transparent subsidies, assistance with supply of cheap loans. Policy around council consenting process. It can be done!

I dont know about incentivising Landlords to sell their properties though. I dont think it would work for most. Most long term investors want the long term cashflow for retirement reasons.

Incentivising landlords to sell properties is not the same as compelling sales (or compulsory acquisition for that matter). It is actually about providing choices and freeing up capital invested in properties for other purposes (such as retirement) whilst taking the heat out of the market too.

Tookey says that 'building' is the same as it was 50 years ago - sorry, thats plain wrong. 50 years ago building standards in NZ were world class. That could have - and should have - been maintained, but in the late 1990's building regulations were discarded along with proper oversight of quality, good old-fashioned know-how, suitability of materials and ethical behaviour. And so the rot began. Labour continued the stupidity, - nine years in power with Helen Clark calling the ever-worsening building/leaky problems a 'beat-up'! End result; further waves of leaky, structurally unsound buildings thrown up by shonky developers, with yet another generation of buyers losing years of savings while government stands by quoting 'market forces'....

National has just enjoyed another nine-year tenure, and the problem has worsened. Shonky structural steel and rubbish concrete quality has added more headaches. Structural unsoundness now, not just leaky homes, no wonder HNZ has sold off so many houses - they are a liability, not an asset. But now homelessness is common, misery illness and suicide rates are skyrocketing, and NZ is at third world status. Almost 20 years of willfull blindness of poor standards by all parties. Such huge emphasis on making money and having a 'surplus', but so little understanding of the need for warm dry homes, schools and businesses. Meanwhile it's all about new multi-million dollar new stadiums and what a great little nation we are. Whoever we vote in in September - please get the basics right this time.

Minor point, but as far as I was aware NZH has not had any stock affected by leaking issues. (As I understood it, they had their own internal design/architecture team and built to their own standards.) They've typically sold off stock when a government with that ideology has been in power, and likewise built stock up when a government with that ideology has been in power.

Agree we had much more government focus on affordable homes over most of NZ's history than in these last few decades.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.