By David Chaston

Last Thursday's release of fourth quarter GDP data has all been focused on the +0.6% rise in real terms. This was below economists' expectations who had expected a +0.8% rise.

For most readers that is 'just numbers', with little to link it to everyday life.

But there are links, and because they are generally positive, there is little news-value for those involved in the partisanship and the blood-sport of politics.

For the rest of us, we should try to understand the other 'real'. For economists and statisticians, 'real' means after inflation is removed.

But for me, 'real' means how it is affecting our wallets, our savings, and our inequality issues.

Governments that want to spend more need to tax or borrow more. In the end that can only come from the productive sector in a transfer of wealth.

But business wants consumers to have rising purchasing power, so a first analysis of the GDP result should start with how much wages are of total overall economic activity.

And here the news is pretty good.

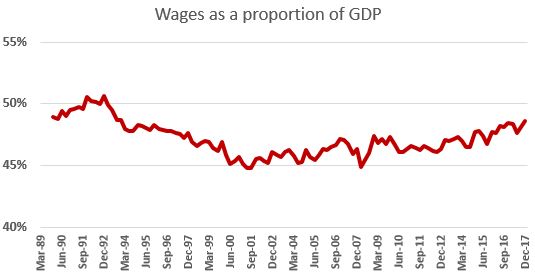

On an annualised basis, wages (code for personal income from work) now represent the highest proportion of national income in 25 years. It's a generational high, and has been rising consistently since 2010 and rising its fastest in that period over the past four years.

All data in all charts are sourced from Statistics NZ, or the summaries published by the RBNZ.

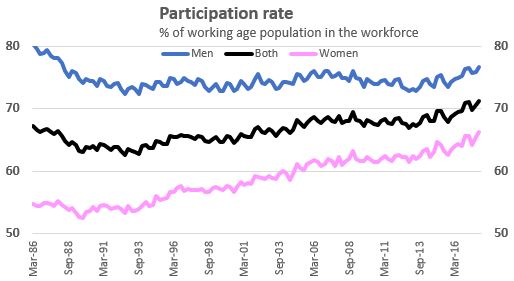

One reason is that more people are in work than ever before. Employment at December 2017 was an all-time high of 2.62 million people, up +3.7% in one year and up almost a fifth in ten years. To put that in perspective, the working aged population only grew +16.5% in the same period, so there have been real in-work gains. More people are being paid more for more work.

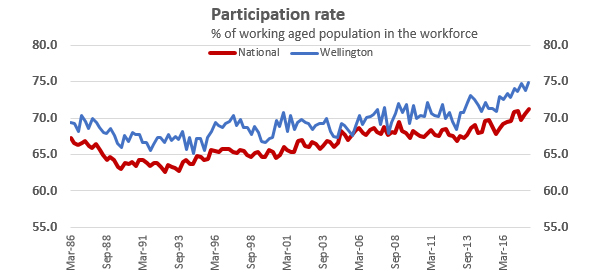

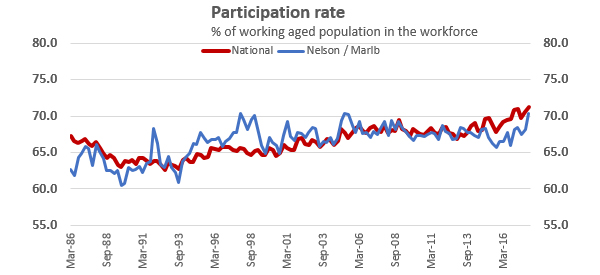

And in turn, that is because we have a very high participation rate. It is rare for a developed country to have a participation rate over 70% and New Zealand is one of those rare cases. Our's is over 71% and the highest it has been since modern records for this metric started in 1986.

So more people are working and pay is rising faster than inflation, together resulting in a larger claim by workers on national GDP.

Behind this improvements in rising participation is a long-term and relentless rise of women in the workplace, and a transition from part-time to full-time work. This has had a powerful impact on household wages and budgets. It is a trend that started in 1989, going from 56% to 66% over that quarter century. But it still has a long way to run to match the male participation rate of 77%.

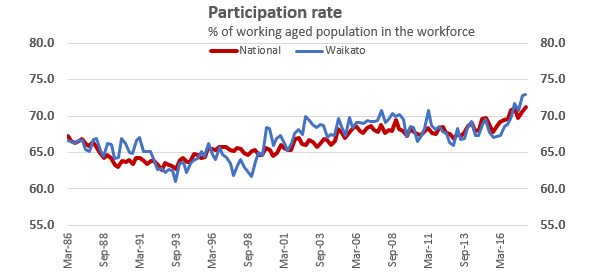

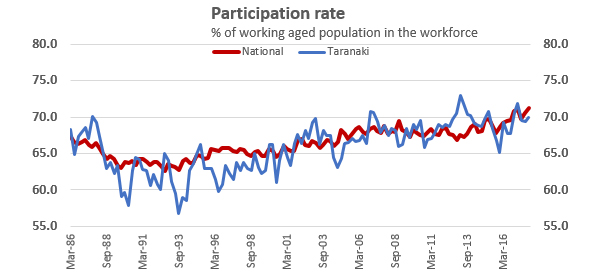

But there is something else at work as well. Participation rates, while rising overall, have drawn in new people working in the regions even as participation rates in the main centres rises too.

Participation at such high levels comes with an inescapable fact - the latest workers joining the workforce are likely to be the least productive, or the hardest to make fully productive. Ministry of Business, Innovation & Employment (MBIE) job ad data shows that we have high demand for unskilled and semi-skilled work. There are not enough people available to fill all these types of positions where skill standards are not high. It is unlikely that these types of jobs are adding proportionately higher output or productivity.

Some critics see the low rise in per capita GDP as evidence we are not on the right track. But there may be an overlooked and simple explanation.

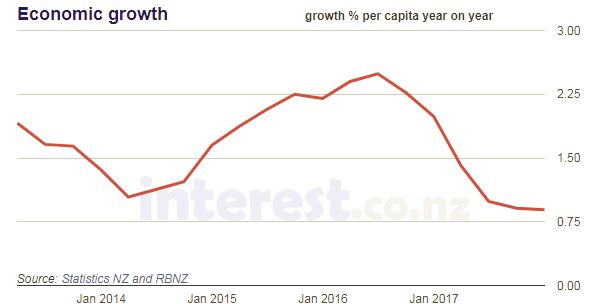

First, here is the recent growth record of GDP per capita:

It is pretty anemic. In the year to December 2017 it grew just +0.8%. That is far below the +2.0% it grew in the year to 2016 and the +2.2% it grew in the year to 2015. Note that it only grew by +1.3% in 2013 and +1.7% in 2014.

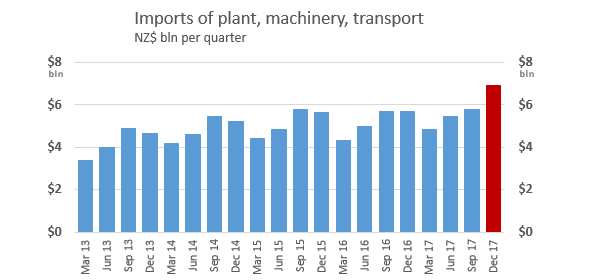

But the years it was high, imports of machinery were low, and when machinery imports were low, GDP-per-capita rises.

In the year to December 2017, this machinery import rate was +11.0% higher than in 2016. In the year to December 2015, it grew just +4.8%.

That is just the way GDP is calculated:

Household spending plus Government spending plus Investment plus Exports minus Imports = GDP

Imports of productivity increasing goods reduces GDP in the short-term.

We should expect GDP-per-capita to rise again over the next year or two based on the surge in recent capital goods import levels.

What this all means

There are two takeaways here. First, in its current state our economy is nearing full practical employment and each additional worker added won't be adding much more to output. To get more people participating in our economy will take us into unusual territory among any OECD economy. In my view, unless we start adding new high-output workers from outside the country (immigrants), we cannot reasonably expect the current type of economy to grow much faster than it is.

High participaction with a rising share of wages-to-GDP is not a story you hear often, and goes some way to understanding why New Zealand's inequality levels are relatively low (as measured by its stable Gini scores).

And secondly, businesses will need to invest at their current higher levels over a long-term basis in productivity-related equipment if the 'current state of the economy' is to be changed to a future, higher productive state. That will require those investments to be 'worth it', meaning our market size will probably need to grow, and market returns need to be seen as likely (otherwise, why would you take the risk?). That outlook will require positive support by policy makers, and stumbles will undermine it quickly.

11 Comments

thank you DC. It's good to see that the share of GDP that New Zealanders get in their pocket is rising. After all what is the point of driving up New Zealand's GDP (it's only an acronym) if it don't benefit us New Zealanders (we are the inhabitants).

Yes - Business will need to invest in higher productive assets and move from our culture of under investment. Any government will need to have structures that support it

The approach of the previous government to grow GDP by bringing in low wage immigrants, and thus depressing incomes overall was a disaster, and the main reason I didn't vote for them.

I like your analysis David, but I differ in the conclusions.

What we have in New Zealand is that very rare thing; things working well.

The way wages work is that the more profitable businesses in a region can afford higher wages. They can therefore poach workers from the next layer of business down. The next layer will have workers with good skills who can be upskilled in the more profitable business. This process repeats down the skill ladder, with each business poaching the more skilled workers from the layer below it.

Also the more profitable business can afford to install machinery to replace their own lower skilled workers.

So at full employment you get a virtuous circle working, with more profitable businesses continually upskilling their own workers, poaching workers from less profitable firms and installing machinery to free up their own lower skilled workers. These freed up lower skilled workers provide replacement workers for the next level down.

In a successful local economy this becomes a really powerful thing as it results in an eco system of skill sets which support each other. Think engineering workers in and around Port Nelson. They mend ships. They mend oil rigs. They need a tiered range of related skill sets and can afford to upskill their workforce.

This powerful process of self improvement can be de-stabilised if lots of cheap labour can be shipped in from outside the region. The incentive for training and upskilling is reduced and you endanger the self reinforcing effect. You get a low wage, high labour content economy. Think grape growing.

Keep in mind that our "full employment" is in the environment of very low interest rates..

That is going to change... especially long term interest rates.

Will be interesting to see how our economy copes with higher interest rates...

my view is ... Not so well.. ( Maybe very low growth or even a mild recession heading our way .?? )

Your concerns are perfectly valid, but I am beginning to think the danger is less than it has been historically. Higher interest rates can be forced upon us, as they have been in the past, or they can come about naturally as a result of competition for funding from profitable businesses. The effects of the two are very different.

If higher interest rates come about naturally as options expand then savers have more choices, they can choose between say, a Fletchers bond, an Auckland airport bond or an ANZ term deposit. Interest rate rises are a function of the profitability of the economy increasing. In this case they go up more or less in line with our ability to afford them.

If interest rate rises are imposed from overseas then they are determined by events over which we have no control. This has been our historical experience. However, low government debt levels free us from one of the main reasons why this happened. A crucial historic vulnerability has been dealt with, and those who went through that carry the scars to prove it.

So, what does the next period of difficulty look like? High household debt means we are very exposed to mortgage interest rate rises and thus to mistakes by the RBNZ. Usually the RBNZ does too much, too late. They fail to raise interest rates in a timely manner and then rush around in a panic when inflation gets ahead of them. They tried not to follow this path in 2014, when Auckland house prices started taking off, but were forced to stop when no inflation in day to day costs was evident and the interest rate rises started to slow things down. They have therefore had to watch the stupidity caused by low interest rates overseas on New Zealand house prices.

I think we are starting to see inflation arising quietly in commodity prices worldwide. So far its the key industrial metals, copper, zinc, nickel, cobalt, tin and so forth that have been going up. The big one, oil, was last to fall and will probably be last to rise, and its current cheapness masks the rise in commodity inflation that I think is taking place.

Roger ... I think the forces are different, in regards to short term, md. term and long term % rates.

My concern is with where long term rates go as Central Banks step back.. ( keep in mind, the GFC was the first time, in my lifetime , where Central banks directly influenced long term rates )

My guess is that as long term rates rise around the world, it will have an affect here.. eg.. %rates on fixed term mortgages, Govt borrowing, Corporate bonds...etc

Mervyn King says that :

Short term interest rates are controlled by Central Banks,

Medium term interest rates are infuenced by "mkt expectations" ( eg. inflation/deflation, risk .etc ),

Long term interest rates are influenced by the forces of supply and demand.

With Medium term rates, traditionally, Central Banks try to influence mkt expectations ( forward guidance etc ) but have no real influence on Long term interest rates

QE was all about controlling long term interest rates, lowering them . ( As Bernanke says in his book ).

Unwinding QE will allow Longterm rates to move to the mkt forces of supply and demand... Will be interesting to see if Long term rates rise..., and by how much ??

Thanks Roelof,

Yes, I'm trying to figure out what happens next. This chart seems to be telling me something:

https://fred.stlouisfed.org/series/USD12MD156N

I think it means that the world economy is picking up. That productive enterprises are competing for funds and this is pulling interest rates up. That demand for copper is going up because it is being put to good use. That the positive, productive forces are gaining the upper hand. The trouble is, that is also what I want to believe, being a fundamentally optimistic chap who thinks that by and large people are pretty good at sorting things out in their own lives, if they are allowed to do so by those who worship power over others, be they thieves, socialists, militarists or misguided bankers and intellectuals.

I tend to parrot what Ray Dalio says... He says we are in the "goldilocks phase", of the business cycle... I agree ( I think we have past that in NZ, and are kinda in the latter stage )

https://www.reuters.com/article/us-hedgefunds-dalio/bridgewaters-dalio-…

I've added the fed funds rate to your chart

https://fred.stlouisfed.org/graph/fredgraph.png?g=j8hn

{kind=link}

roger , You might be interested in this..

https://www.linkedin.com/pulse/its-all-classic-main-questions-timing-wh…

Thanks Roelof, that is a good link.

Ray Dalio is someone I take seriously.

roger - Ray Dalio's new book is worth reading if you haven't already

and the magic bullet is still more immigrants recommended.?

We need a new recipe.

When the current wave of immigrants have the housing they need built and the displaced NZers are housed and the infrastructure has caught up with the population growth, what then?

Davids new boost of immigrants are going to do what exactly? Build more houses and infrastructure? Are they going to make farm land more productive? Catch more fish or plant more forests?

Imagine if NZ had its current productivity with 1/2 as many people. They would all have a great lifestyle.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.