By Mieke Welvaert*

Auckland dictates the market

Auckland dominates about 30% of the New Zealand property market. We expect house prices in Auckland to keep climbing over the next three years, even though Auckland is the most unaffordable region in the country. A considerable undersupply of housing will support Auckland prices which will limit any downside to house price inflation measured at a national level.

Undersupply keeps a floor under Auckland prices

We estimate Auckland’s housing undersupply at 45,000 dwellings. Although Auckland house price growth has been losing speed, the sheer scale of undersupply remains a floor under prices in the region. House prices aren’t expected to fall in Auckland until 2022, when additional construction will begin to offset some of this undersupply.

House prices will fall elsewhere in NZ

House prices are expected to fall by up to 5.0% during 2019 and 2020, as strong residential construction activity brings more houses online in parts of the country outside Auckland.

Property markets around the country have already lost sales momentum and prices are expected to follow. In the September quarter, national sales were only up 2.3% from last year. Property markets such as Tauranga, Wellington, and Queenstown have all reported undersupplies, but sufficient consent growth in the past year, alongside reduced demand from slower population growth, will soon take the heat out of these markets.

But prices will pick up again before long

We expect house prices to hit their trough in the middle of 2020. But more buyers will be drawn back into the market by the second half of 2020 when the Reserve Bank reduces its loan-to-value ratio (LVR) restrictions and lending conditions improve.

At their June 2020 trough, house prices will still be higher than their pre-Global Financial Crisis (GFC) levels in all regions bar the West Coast and perhaps Gisborne. At the same time, prices in Waikato, Bay of Plenty, and Otago will still be around 30% higher than they were in December 2007 (just before the GFC). With house prices expected to hold well above their pre-GFC peak, correction is not the word we’d use to describe how house prices movements in the next few years.

A correction isn’t on the cards

Current conditions simply lack the drivers for a large correction. Although we acknowledge that several property markets in New Zealand are currently overvalued and highly unaffordable, we still find it hard to entertain any large downside in house prices. Slowing population growth will start to alleviate demand pressures, but the New Zealand population is still expected to grow at an above average pace during the next five years. This base of people needing houses will continue to support housing demand.

Interest rates remain low, supporting mortgage financing. Even as interest rates rise, easing of LVRs will help draw more investors into the market from 2020.

Furthermore, the New Zealand economy and employment are still expected to grow at slower, but still comfortable rates, meaning that people will still be earning incomes that they can use to support mortgages. With these underlying conditions in play, alongside Auckland’s massive housing undersupply keeping upward pressure on prices, chances of a substantial correction are slim.

Mieke Welvaert is an economist at Infometrics in Wellington. This article is a re-post from here and is used with permission.

150 Comments

I can smell the fear !

Exactly.....

Scaremongering = "the spreading of frightening or ominous reports or rumours" . Yes, the media did work wonders for property spruiking! On the way up, there was also lots of frightening price gains, ominous reports, dealings and rumours.

It's been such a great run hasn't it? Now, it's time to pay the piper.

Take a shower :-)

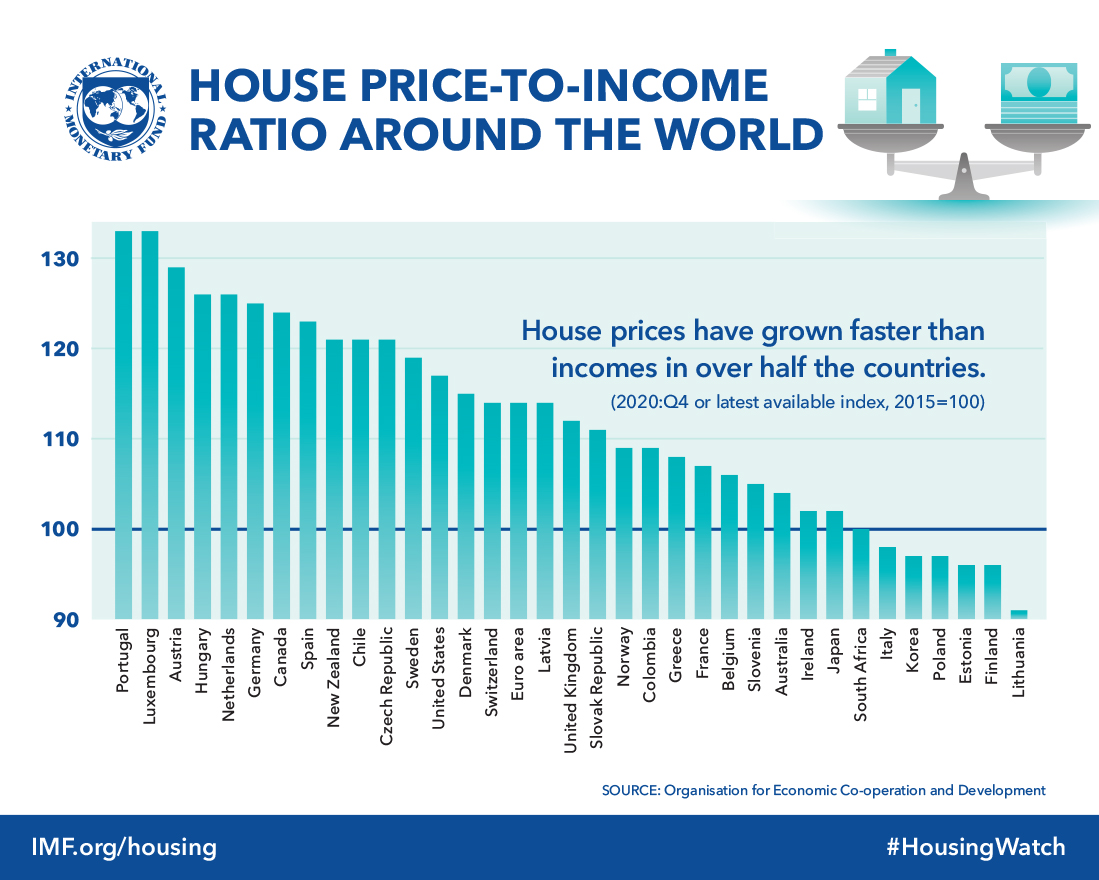

Most unaffordable housing in the world when measure by income to home price ratio. We are long overdue for a correction.

https://www.imf.org/external/research/housing/images/pricetoincome_lg.j…

{kind=link}

Great article, cheers. Agree with pretty much every point.

ha I thought literally the opposite of every point. Upper quartile Auckland is tanking already, (and this needs to happen if the future generation is to have any hope). Lowering LVR's and borrowing costs wont provide a domestic floor for 2 million dollar houses, but it will inflate house prices in the regions.

I agree BLSH.

FHB will be listening to all the uncertainties about the housing market. However, as long as they are buying for long term property ownership and are not over leveraged and be able to absorb interest rate increases down the track, then all will be fine no mater what happens. Their bank has a vested interest to assess whether or not these factors pose a risk.

FHB; there is conflicting views from all and sundry and their is no future certainties but don't put your life on hold. You will be fine!

There is no price floor. It's the price ceiling imposed by the ability to finance that restricts house prices. That is evident by RBNZ loosening the requirements to finance house purchases.

A price floor would be evident if RBNZ or another Government entity was buying houses if the price fell below a certain value.

Thanks for the reminder about no price floor. If the price is what we are willing to pay and the price ceiling the max we can afford then there is no price floor. Even if the land is free and it costs $350k to build there is no price guarantee. I remeber a few years ago falling in love with an advert for a house in Taranaki - I could have traded my delapidated 3-bed house in North Shore for what was effectively a 30s manor house: it was in good condition with tennis coursts and acres of garden and formal driveway and seven bedrooms and red tiled roof with bay windows etc. To build from scratch probably more than the 600k they were asking. But it was in the wrong place - the best house in a village that had died and disappearred. Similar proof of no price floor viewing new houses in a Las Vegas suburb a few years ago - price cuts from 750k US$ to 300k and none selling.

Prices have been increasing so much as interest rates allow.

I just don't see necessary wage growth or continued interest rate decreases in the near to medium future.

I think prices may dip and/or plateau for some time. Corrections can't happen in auckland as population growth means demand is higher than supply.

population growth doesnt necessarily mean houses sell, and thats why inventories are so high and sales volumes still dismal

You may be right too. It is very difficult to guess what is going to happen in a market with so many variables.

I think so many people are waiting to buy houses though, that they will jump in on every price dip thus providing a buffer to a large price correction.

But, that is just a guess on my behalf too. I could be quite wrong and if the price falls fast enough buyers may try to time the bottom.

If NZ was bringing in very wealthy immigrants then prices will stay up (my arrival in 2003 worth about $800,000 meant the first thing I did was buy a house and when settled sold in the UK and bought another). However the 60,000 immigrants arriving last year seems to include plenty of checkout operators, cleaners, fast food operatives, etc and as far as I can surmise they spent their saving to buy their residency.

Articles with more spin than a turbo, Banks lowering rates to the levels of a pancake, comments vanishing into thin air, TTP calling for censorship on the Truth and Reality Merchants, and now the easing on the LVR ?????

Call me a conspiracy theorist , but it looks awfully suspicious that we are getting very near the end of the R.E Party.

No conspiracy, we are indeed at the end of the current RE cycle. Things are gonna stay relatively static (with some fluctuations) for a while, before the next cycle begins. "Yeah but this time it is different" types are hopeful souls who, alas, are likely to get disappointed: the fundamentals (persisting demand, easily accessible credit, construction cost inflation, etc.) are still in place as they have been for decades...

I think the conspiracy Tony is referring to is the imminent property market crash that will wipe 70% off house prices. The crash has began and interest.co.nz, infometrics, RBNZ the banks and Kermit the Frog are all conspiring to fool owners and buyers to ramp up more debt before the apocalypse can no longer be denied.

Unfortunately your "relatively static" comment also lumps you in with the conspirators who are attempting to hide the truth.

This is not the first time, and probably not the last one either, when people predict a “crash” and call their prediction “the truth”. There were many who heeded such predictions, and even based their property buying decisions on such predictions, only to regret it later.

Let’s come back to this discussion in 2021-22 when the next cycle takes off…

Hilarious!

Hi Tony

Sadly we lost control of our banking sector after the GFC and they pumped and pumped a bubble. Now they have a strong grip on everything and articles like this re-enforce how brainwashed the population have become and how little they know about credit! It's like believing in father Christmas, and when you grow up and realise that he's not real it takes a while to fully comprehend.

Nic

Shut up. Nobody’s lost control of the banking sector.

You sound like an egg when you talk about property busts but don’t know the difference between real and nominal prices in NZ. It’s just rambling

Mind your manners lalaland. This is a gentleman's forum.

Have you seen what is happening in Australia and the extent of the fraud that has created their housing bubble? A bubble that is in the early phases of a collapse. Not such a lucky country at this moment in time and as sure as 'eggs is eggs' we'll follow them. Their reserve bank doesn't have a clue how to deal with it either!

It’s a every one forum, not a “gentleman’s” forum. So maybe you sort yourself out. Yeah?

Hi lalaland,

"Rambling" is a very good description......

Many of these people are on a crusade.

Who would want them running NZ's banking sector?!

TTP

Look I’m all for a good bubble burst but there are good arguments and then there are just ramblings. As someone who is actively taking risk in both short and long property markets, I see the latter all the time.

Life is different when you take significant risk against a view. Some know what that’s like, most don’t

I now understand the reason for your current temperament.

Put your views to a test one day. Might be good for you

You and THEM AN are definitely on a crusade, it's transparent.

Conversely, I don't think BuyLowSellHigh is. He's a genuine commenter with a genuine viewpoint.

Yes - a good, solid appraisal from a well respected economics agency (Infometrics).

Note that the article represents very much a mainstream view.

TTP

Ummm, I think instead of flip flopping, Infometrics should have stuck with their initial February 2017 forecast (-12%) and run with it. "NZ house prices look set to fall 12% by 2020 as rates rise and population growth eases"

https://www.interest.co.nz/property/86171/nz-house-prices-look-set-fall…

Agent TTP, Infometrics forecasting is much like yours. It's all over the show. There's little consideration towards expanding global risk. As you've often said yourself, NZ is a global economy, therefore, we have to sometimes swallow the bad as well as enjoy the good.

Hi R-P,

"Agent TTP, Infometrics forecasting is much like yours. It's all over the show."

That's an implausible statement.

You need to understand that reputable economic forecasters (including Infometrics, NZIER, BERL, RBNZ, The Treasury) update their forecasts periodically - as information/data changes and new approaches/insights develop. In this respect, they are similar to other categories of professional forecaster, such as weather forecasters, seismologists and various others whose job it is to predict. Life is rarely a constant.

Forecasts do not (and cannot be expected to) remain the same forever, but are point-in-time outputs of on-going, robust processes.

Forecasting efficacy might best be judged in terms of keeping abreast of changes and measuring them accurately.

TTP

Agent TTP, that said, it doesn't bode well for yours and BLSH's resurgence of NZ house prices in 2021 now does it? It's now okay to flip flop as long as you are paid a salary to do it.

Mainstream view = sheep, blinkers on, uninformed.

This article is nothing more that an indoctrination piece for the masses that is deliberately ignorant

The masses are on this site (clue posts with most thumbs up)

I can assure you the 'masses' don't read interest.co.nz

Yes its the mainstream view but not the view of the majority on here so its going to get flamed.

I would say its more bullish than mainstream

I have to agree unfortunately.. I see only three probable ways house prices will drop

A credit freeze (global)

Job losses (cant pay mortgage)

Immigration falls (no more renters)

Also maybe if the ass dropped out of the NZ dollar might tip things over?

You left out trade war.

Ah true, a war will upset the apple cart..

The assumption Mieke makes is that the present demand for houses in Orc Land will remain at current levels ...

.. any one of a hundred different Black Swans could come crashing through the economic windscreen and shatter that demand in the blink of an eye .... a ratcheting up of interest rates .... the trade war between China & Trumperia spilling over to include other nations or trading blocks .... a worldwide pandemic , a virulent flu .... an outbreak of foot & mouth in the dairy industry .... the alpine earthquake fault line rupturing , as it's overdue to do so ...

Or just a plan old fashioned dose of reality , a'la Hugh Pavletich's Demographia , that houses in the Kiwi Pavlova Paradise are just way too many multiples of expensiveness as a ratio of household income ....

Times like this I wish there was a “like” option

And foot and mouth.

The probability of these events occurring changes over time. Many people assume that the probabilities of these events are static and unchanged over time.

The probability of some of these risks has increased significantly in the last 2-3 years with the US Fed raising interest rates and the ripple effects this has on the global economy, and the global financial system, and hence the NZ financial system. If you are interested, then you only need to read the RBNZ Nov 2018 Financial Stability Report for the risks that they raise there.

Many property owners have maximised their debt levels when the probabilities of an unexpected event has increased significantly. Under current market and financial conditions this is a potentially risky strategy. Would they be able to hold on if any of the above mentioned events occurred? Many might not and could be forced into some type of deleveraging.

Highly leveraged property owners should be positioned to hold on under all economic circumstances, not just favourable market conditions.

Great comment!

The last one is the most likely, initial shocks from a kiwi fall are understated

Hmmm.......some of the most recent headlines...

" 400000 under RV"

"motivated vendor selling below RV"

" All offers considered , Own your own sanctuary"

" Selling 200000 below RV, act now"

" Now selling 200000 below RV"

" Owners have purchased bring all offers"

" Address withheld "

Yes....I do see the upward trend coming soon.

I was disappointed how shallow the thinking is in this article.

A set of random thoughts:

Why do we believe that there is a 45,000 shortfall of houses when rentals are no higher than in Wellington. The 45,000 shortfall figure is based on 2006 ratios of population to houses. However, demand is elastic and prices would need to fall to their 2006 relative prices for there to be demand for a further 45,000 homes

The concept that investors will step in if prices fall - but investors have been chasing capital gains and if they are not available then investors would seek a relatistic return based on income levels. This would imply prices falling significantly to the point they provides (say) a 5% return on investment - which is probably 20-30 below current prices levels.

The reality is that much of auckland business is unsustainable at current prices/rentals. We are already seeing teachers and nurses saying they can't afford to live in Auckland. Therefore, we are likely to see population/industry relocate to the regions.

Supply has been constrained by the previous Auckland District Plan. Greater housing density, coupled with the ability to supply housing at below the median Auckland house price will contribute to increased supply.

All in all a projection of current prices into the future is somewhat heroic

At 5% houses are free so thats incorrect.

The 45K shortfall simply means there is a group of people who cant afford at this level, but as prices fall, demand would be expected to rise quickly.

Certainly nothing implies prices would return to 2006 levels. The sum of inflation, wage gains, rate cuts etc indicate prices should have risen hugely. The shortfall sent property to its affordability limit, and that is not surprising.

Renters will crowd if prices rise too quickly, so rent is a fairly blunt tool to measure housing shortages.

Unsure what you are saying here.

- "At 5% houses are free" - sorry I don't know what you are saying.

- we seem to agree that as prices fall more people will demand houses. However, I argue they need to fall substantially until there is demand for another 45,000.

- and my comment was 'relative to 2006' where I was suggesting that price to income ratio would equate with 2006 levels rather than absolute house prices.

- I agree rentals are a crude tool - but they do equate with income and affordability levels. That is why Shiller and other economists use it as a measure of how much of prices is sustainable and how much is 'bubble'.

At 5% the ownership cost of many rentals is $0.

Housing shortages blunt corrections relative to balanced markets, so the correction should be less serve, not more severe.

Debt to income in 2006 needs to be adjusted for interest rate changes. If you undertake that work youl see house prices are at the peak of the typical range but are likely no where near as stretched as you imagine using something as blunt as a DTI ratio.

The affordability of rentals is less affected by interest rates, where as housing, and in particular rental housing, is massively influenced by interest rates.

In simple terms if you halve interest rates you double the value of investment property but you have no direct impact on rent.

At 5% return the cost of rentals is the original investment. Investments are meant to be above the cost of borrowing to allow for the risks - take away capital gains annd 5% return is low. Commercial property for instance is commonly a 6% return and commercial rentals commonly go up with inflation.

In 2006 the price to income ration was 5.9 - it is now 8.6 (on a consistent measure) so prices could drop 45% before that ratio would be restored.

The ratio of interest rates to investment rates is more complex - if interest rates decline then renting is less attractive than purchasing. I think interest rates are an enabler of bubbles rather than a cause of bubbles.

Total return should be above 5% over a long period of time. So if you get 5% from income alone then you are in a very good place, consider stocks at a yield of half that. Commercial yields slightly better than residential at low values, much better at high values. But commercial is riskier and can not be geared up as aggressively. Both commercial and residential are good investment classes. Both commercial and residential rents/leases rise on average faster than inflation.

DTI has little to do with how much you can pay for a property. You must account for interest rates. The reserve bank has gone to great lengths to study this and it is as proven as it can be, it is borrowing capacity, not income alone, that drives house prices in NZ.

If you think interest rates do not drive prices upwards then you are wrong. Provided you do not have some horrific oversupply then cutting interest rates will drive prices up in NZ.

https://repository.digitalnz.org/system/uploads/record/attachment/424/t…

"In our cointegration framework, we find evidence that disposable income per

household and mortgage interest rates have explanatory power as long run influences

on house prices.

• It is perhaps a little surprising that these two variables – which together reflect

households’ borrowing capacity and which are largely demand-side in flavour –

should by themselves account for long term movements in house prices."

Tired of being polite - you are talking nonsense:

5% is below the return on investments - check your kiwi saver. I think you are stuck in the mindset of capital gains. Even a 5% yield rate doesn't allow for depreciation - replacing roofs, bathrooms

Residential/ commercial rentals don't rise fast than inflation - that would imply that rentals continually became a higher proportion of the revenue generated. Some locations gain as cities grow (effectively becoming more central). However, a lot of retail is currently competing with on-line retail and unable to pay higher rentals.

If borrowing capacity drove house prices then they would have gone up everywhere. Auckland was a bubble - prices went up because people thought prices would go up.

The issue of the supply/oversupply is because of the lag to price increases to supply (and RMA constraints). We are seeing many locations (eg Queenstown) where supply has lagged and prices are therefore likely to reduce when supply catches up. You can build a 150sqm house for $270k - and there is not a big shortage of land in New Zealand

Total return includes capital gain... I am saying that total return should be over 5%, so if income is 5% then you are home and housed because eventually the capital gain will come.

At 5% yield with a 4% interest rate a rental is maintainable without topping up, eventually youd struggle with something like a refit but you are effectively splitting hairs as those costs are so far down the track youd be swimming in capital by then.

Rents and leases rise faster than inflation. Its just a fact. Rent is expected to rise roughly in line with nominal GDP, well above inflation: https://www.interest.co.nz/charts/real-estate/rents-median. Maybe you dont mean inflation?

Property has risen in most locations with decent demographics. Auckland has gone further than borrowing capacity would imply largely due to a housing shortage which added some froth.

Read the RBNZ report on this, i posted it for you.

There is a major shortage of land in Aucklands central suburbs for various reasons but the reality is that there is a land shortage and location matters in any city.

The shortage will be solved one day and that will remove some of the froth from Auckland prices. But its a long way off and over that time fundamentals like wage growth and inflation will have driven prices higher anyway such that the froth loss isnt likely to matter.

...and you should always be polite, or at least try to be funny if you are going to be rude :-p

Can I just say... What a load of tosh!

Can I say bollocks?

Ireland?

... for about the same price as an average " Kiwi Build Ballot Affordable " house in NZ , you can buy a Chateau on an acre or two in Southern France , or in Spain ....

Kiwi real estate prices are treading on as solid a foundation as Bitcoin currently is ....

Mais le château coutera une fortune pour rénover ou même juste pour le maintien annuel

Hi Nic,

You can say whatever you like......

But it won't stop house prices rising over time.

Remember, however, that there are plenty of other good things to enjoy in NZ - aside from real estate.

TTP

"won't stop house prices rising over time" = How long is a piece of string

Hi TTP

'You can say whatever you like...' Really?

How often do your comments get removed? I would suggest that some commentators get edited a lot more than others.

But no one is really arguing that there is substantial downside risk from the current status quo.

The argument is that the risk comes from some significant external shock; the thing that is responsible for the majority of property price corrections, worldwide.

New Zealand's one trick pony economy works extremely well from an endogenous perspective; selling things to each other at increasingly higher prices is a perfect example of this. However almost exclusively downturns in the New Zealand economy and asset base are the result of exogenous factors.

nymad it's like you're saying we shouldn't base a large portion of our economy around property and stop assuming that we are somehow insulated from the rest of the world. Shouldn't we be the Switzerland of the Southern Hemisphere already?

I for one don't hold extreme views on this issue. I think a crash is unlikely, and even a large correction of more than 15-20% *relatively* unlikely (dependant on a large external shock). But I think a moderate correction of 10-20% is likely. Especially if Kiwibuild ramps up, which I think it will do in another 9-12 months

“Current status quo”

No need inset current before status quo as it is implied. We’ll sort out your word salad habits one baby step at a time.

[ Deleted. Argue the issue; there is no need for a sophomoric drive-by smear. Ed ]

What if this issue is that we have biased media corrupting the minds of the masses? Perhaps Donald Trump is right...

This article wouldn't look out of place in Dublin mid-2007. Here is a great collection of other quotes from that period, which I find quite hilarious.

Ben Bernanke Dec 5th, 2010 "I wish I'd been omniscient and seen the crisis coming. One myth that's out there is that what we're doing is printing money. We're not printing money.'

Hmmm, remind me why do we pay these people six figure salaries again?

"We expect house prices in Auckland to keep climbing over the next three years, even though Auckland is the most unaffordable region in the country. A considerable undersupply of housing will support Auckland prices which will limit any downside to house price inflation measured at a national level."

Yes, "the most unaffordable region in the country" will differently go up - makes perfect sense, NOT!

"Interest rates remain low, supporting mortgage financing. Even as interest rates rise, easing of LVRs will help draw more investors into the market from 2020."

Yes, low interest rates, "even as interest rates rise" easing of LVRs will make mortgages more affordable - makes perfect sense, NOT!

"..the New Zealand economy and employment are still expected to grow at slower, but still comfortable rates, meaning that people will still be earning incomes that they can use to support mortgages."

Yes, EVEN IF the New Zealand economy and employment "grow at slower, but still comfortable rates" our already indebted, low wage population will magically be able to service mortgages - makes perfect sense, NOT!

What a ridiculous piece of fluff that article was.

Depends if Labour/NZ First continue to stuff more and more migrants into the place, despite campaigning on stopping it almost immediately. Don't forget cashed-up expats who haven't paid tax here since their university days fleeing if shit goes wrong globally and waltzing into an already stretched market.

NZ's house price will DECLINE only when NZ becomes an undesirable place to live as a whole.

So, would anyone expect NZ to become an undesirable place to live?

It already is.

You have not seen and experienced one yet. So, zip your gob.

What's so great about NZ "as a whole"? It's getting pretty 3rd world up in here! To be honest many 3rd world countries have better housing, roads and dental services. We also have a growing number of 3rd world diseases and statistics.

And just like that your credibility went up in smoke.

Fair call, I'm more referring to 2nd world countries like Thailand, parts of Turkey and some Latin American countries. And no (before anybody asks) I'm NOT comparing NZ to Nicolás Maduro's Venezuela.

Hi Xingmowang,

That's a very pertinent point you make.

Indeed, one of the factors driving our property market is the ever-increasing desirability of NZ on the world-stage.

TTP

No Xing

They decline the minute that buyers realise that they are stepping into a Ponzi scheme that is only held up by increasing mortgage debt and where the last entrants are left naked and touching their toes to receive punishment.

We're very close now, slow declines in some Auckland suburbs. Low sales volumes in others and the pace of bank 'money creation.' slowing. 6 months from now we'll be looking at the market and realising that we had created Ireland 2.0.

Yes, supply and demand are not the whole story, confidence is becoming increasingly relevant as a key driver now in the market. It all ties in to cycle theory and now is the time for a pull back. The Aussie land value cycle investor Phil Anderson reckons now is this time followed by the second stage of the up cycle from 2020 to 2025 approx. His argument is quite convincing. Read this: The Secret Life of Real Estate and Banking by Phillip J. Anderson

Sydney is highly desirable and declining quite a lot.

Flawed argument.

Auckland is losing desirability, mainly due to its unaffordability.

People just don't get it. It is simple. House prices rise if rich who do not need loans, buy more. Or banks lend more to people to pay high prices. If either falters, so will prices. Loans are indeed faltering which is why central bank is attempting mild rescue. Credit in world economy is now retracting, having been given a massive state sponsored boost for 9 years. China is leading this. Prices may not fall much next year in Auckland but will fall at least 15% off top, as did in 2007-11, in 2020, when vendors finally get point that boom prices are not coming back. Past is not a guide to future and things do change. No boost to prices (or indeed sales) will come prior to 2023, as market reverts to demographic driver, not speculative flow. AMAZING that latter is never mentioned by the paid up members of the FIRE economy.... By the way prices are not flat as people pay same for LESS land. About 20% less in Rodney in fact, than in 2015, despite prices up 40% or more in that time. wakey wakey

Hi mikekirk29

As a gentle word of caution, I think you need to be very careful re specific forecasts about falls in property prices......

Forecasts which create the spurious illusion of precision can soon come back to haunt you - as people like Retired-Poppy (and various others here) have found out.

Remember, what you want personally and what actually happens in practice - can be two very different things.

TTP

"What you want personally?" is an assumption on your part.

It is not an illusion of precision. I refer to what happened in 2007-11, as a top to bottom fall of 15% FROM THE TOP. That can mean average in Auckland or median, perhaps for a 3 or 4 bed house with particular land area.

Need to look carefully at who buys what in Auckland and when. Section mania has driven 2018 gains. This is dissipating as Chinese buyers affected by OBB are locked out. Market price has already subsided from peak. I agree with info metrics that price will bottom (as median) in mid-end 2020. But careful study of Auckland SALES for past 15 years especially indicate that 20% rises and falls are consequence of. liquidity and speculative flow into market, esp post China joint WTO and the 2014-15 mania. Very few analyse who buys in Auckland and into what sector. They just use lazy averages and talk about the "market" when they mean price. Price of what and where? Like supermarkets selling less beans in a can and charging same, developers building new builds especially are charging more per square metre of land sold. Thus, in Rodney, amount fo land sold with a 4 bed property has fallen 20% in 3 years. Ditto Silverdale. Meanwhile prices have risen a lot. Commentators on TV etc repeat that "market" has stalled, meaning price rises. Point I made is the this is not true. You get less, for same price, than did year before, and year before that. Land price continues to rise. It is difficult to compare exactly as property price alters at same time. 40% of Auckland sales we are repeatedly told, are to "investors." Note that "investor" is never broken down into speculation and landlord intent of purchase. It is former that drives large increases and declines in sales. Prices are sticky because those who do not have borrowings and do not need to sell when no capital gain available, sit and wait. November sales figures will be greatly different to October and scrutiny of difference will show where in particular. Listings are now falling I notice. Spring bounce will not materialise. Note that EU, USA and China all experienced material declines in house and car sales and stock markets in last 2 months. This is because liquidity is reducing and dollar is making credit harder to renew. Credit contraction or slowing will induce recession next year in USA and China. NZ cannot be unaffected by this.

@mikekirk27 Im not sure i get your point, if you pay the same for less land that means that prices have risen, not fallen. Using your numbers you are saying prices rose since 2015 by ~75%, and a fall of 15% leaves that figure at +49%, so hardly punishing is it. And Auckland dropped 10% not 15%... Maybe you mean with inflation. Because of the way debt and inflation interact you cant just add the price change and inflation together.

Dear Laminar,

crux is that price of land continues to rise, even whilst price of property sold remains static. Hence, each year, you get less for your buck.

Conversely, someone is getting more buck for their land.

Ireland, owing to a shortage of houses - prices rose. Bust came, young workers (many of them construction workers) emigrated en-mass. Vacant houses = rents and house prices collapsed.

Here we are today, NZ containing a workforce more casualized than ever. Many from other countries. How many do you think play a role in the boom/bust construction industry?

There are correlations.

To play the devils advocate - we have sky high immigration still. People still want to live here, just not Kiwis.

China to NZ is a step up. NZ in 2018 to NZ in 2028 is a step down.

agreed:) My point is that it can turn on a dime. Post shock, workers are locked out of construction sites as access to credit is cut off. As a country in denial, the longer we sustain this stratospheric property ponzi, the harder and further we will fall.

I dont think people necesarily want to live here. They dont want to live where they currently are and we are a soft touch, especially if you have anything resembling money in your back pocket or can successfully flip a burger.

"Here we are today, NZ containing a workforce more casualized than ever."

Retired-Poppy - that's a fallacious statement.

The reality is that the labour force has become increasingly regulated!

Occupational licensing has become far more widespread over the last half-century - as any review of the labour market will show.

TTP

You're talking at cross purposes. It seems to me RP is likely talking about underemployment and the gig economy (a la USA), not builders being a bit casual vs regulated.

RickStrauss, precisely :)

Have a quick look at builders as a for instance. Most are paid as contractors, they invoice their,usually, sole employer weekly. Most under the IRDs meaning of contractor are employees.

I would hazard a guess that outside of bigger construction co's 60% plus if builders are in this boat. This trade is extremely casualised. The IRd, Master builders et all turn a blind eye... too hard basket.

RP - I think you'll find in the Ireland situation they had a massive overbuild that crippled them. The only people living in the new build's were Polish workers renting who were doing the building. I believe Australia is suffering from and overbuild of apartments on their East coast which is contributing to their situation,

If there's a glut of cheap apartments in Australia where jobs pay more, where might young Kiwis go and what could that do to demand pressures in NZ? No correlation....?

The future of Auckland is a glorified departure lounge for students and people trying to get NZ citizenship so they can go to Australia.

The establishment will be happy to know she is singing from the same song sheet

Gee this is bad news for the doomsayers on here!

No you won’t agree with her because it is not in your line of hoping is it?

Get on with life and forget about what way the house prices In Auckland are going as it is mind numbing.

If you want to buy and own a home and you are buying well and can afford it, then just do it!

If you aren’t buying at the right price, then others will!

It's not bad news at all. It's just one opinion. Which is probably flawed.

This whole - Auckland is so bad at building houses that house prices can never collapse - is highly flawed. Auckland has inelastic housing supply compared to everywhere, so if demand is high price inflates quickly (which it did) and if demand falls the price falls quick. The underlying demand Infometrics relies upon are relatively wealthy people with transferable skill sets. They wish to acquire property and have a wide variety of options. Property prices in Aussie are falling. Hamilton and Tauranga are growing quickly and offering more good paying jobs. Auckland has no lock on any ongoing demand.

Scarily simplistic article. Noting that she does raise some valid points as to why property may not crash.

Also scarily and worryingly confident. A book I got yesterday called 'Wrong - Why Experts Keep failing us and how to know when not to trust them' (by David. H. Freedman) sets out as one of the giveaways of less trustworthy expert advice is that:

'it's simplistic, universal and definitive'

The points are made to appear valid but are just spin.

1) Auckland is 30% of the market therefore it dictates the market. No that is not the case.

2) Prices will fall everywhere else. No that it not the case either, but if it did then why live in Auckland?

3) Price will pick up before long. That is just a different wording for "house prices always go up". That mantra devastated people in the US during the GFC and they are primed for a second collapse.

4) A correction isn't on the cards. Some metrics indicate that we're neutral. So this could be correct but when things go wrong the metric could change in a matter of days.

There's not any evidence to support the first three points.

Pays to keep it simple Fritz or you get "Paralysis by Analysis" and your left renting for life.

Phew, what a relief!

Reading the author's bio she is a transport economist for infometrics, not a housing economist.

This article just further reinforces my already lowly opinion of economists.

She’s an economist. Very well placed to provide market commentary.

Have you read Taleb?

Does it have pictures of houses in it? If not, perhaps not?

And economists are hardly ever wrong....???

Interest, that's really mean feeding Mieke's (perfectly good) article to the majority of commenters on this site

The front page headline was there just to get a response. They need to have a range of opinion pieces like this, despite lacking any evidence.

Infometrics has made so many incorrect predictions and time will prove that this one is also wrong as well.

I'm sorry Mieke Welvaert but you have no idea.

Out of curiosity, what are some of their incorrect predictions?

In 2016 they were predicting continued growth in the Auckland property market well into 2019 due to supply and demand. Median rising around 5% a year or something like that.

You sure? I know that in 2016 they predicted that “residential building cost inflation will average 5.2%pa over the three years to March 2019” You’re not thinking of this by any chance?

http://www.infometrics.co.nz/homebuilding-reach-time-record-2018/

I'm sure. Tony Alexander was also saying that the Auckland market was going to boom through until 2019.

So why have you still not sent me a link to prove it? Not saying you’ve made it up out of thin air, but it’s beginning to look like you’ve made it up out of thin air...

Hi BLSH - Just in case Adam is busy this evening, here's Tony Alexander talking earlier this year....

https://www.youtube.com/watch?v=HnnmmQb1XO4 - sounds a bit wrong now!! but gotta sell those mortgages.

Here's Tony encouraging the investors to buy into Auckland in 2016... And guess what, many areas started to fall in April 2017.

https://www.youtube.com/watch?v=A-psmZvMT3M

And here's Kenny Rogers... Just because I like the song! The Gambler!

Cheers Nic, Im familiar with what Tony Alexander has said, but Adam made a very specific claim about an Infometrics prediction, which is what I’m asking him to show proof of. He says he’s sure, and all Infometrics predictions/commentary is published online, so I’m sure a link will be forthcoming. I’m sure he’s not full of it and didn’t simply pull those figures out of thin air.

Hi BLSH

That information is provided here in their 3rd Feb 2017 forecast of a 12% fall in prices... bit of a change of tune today now that the falls have actually started wouldn't you say?

Nic, your link suggests the exact opposite of Adam's claim. Adam's claim was about a 5% growth prediction, your link relates to a 12% correction prediction.

This is their prediction for the end of 2020, so time will tell. It’s not actually even a prediction, they just say that there is “scope” for a 12% correction. Not sure if this is still their outlook. This is a possibility of course, but it’s not going to happen. Their timing about the bottom of the market isn’t far off though.

Adam made a specific claim about a supposed prediction that Infometrics made in 2016 about what prices would be doing through 2019. The prediction Adam refers to claims growth of 5% through to 2019 - this is totally unrelated to the prediction you refer to above, which states that there is scope for a 12% correction.

Do you think maybe Adam was slightly off on his recollection? Maybe he didn’t have the link right in front of him. You’re quite anal retentive aren’t you?

He didn’t like the opinions expressed in this article, so decided to discredit the author by claiming that Infometrics has been wrong in the past so shouldn’t be listened to now. I don’t think he had any particular incorrect prediction in mind when he said this, so when I asked him for an example he made one up. Gloomies do this all the time (make stats up to support their world view), so I’m just holding him to account.

Nic’s link suggests the opposite of Adam’s claim.

Will take it all back if he can just post a link of course.

I always find interesting that people actually listen to these so called economists that happen to be judge and party.

Sorry guys, was out slightly with my dates. Here is the link I was referring to. Will try track the Tony link down soon when i get a chance. http://www.infometrics.co.nz/where-are-house-prices-going-to-go/

Thanks, so you'll acknowledge that the Infometrics prediction was very accurate? Its actually amazing how well they forecast Auckland house price growth from the date of their prediction in Dec 2015.

https://imgur.com/gallery/8JYOf8R

First red line is date of Infometrics prediction. Second red line is current date. Infometrics prediction (lower graph) matches what actually happened (upper graph) remarkably well.

BLSH, think global.

The graph point you made is incorrect. That aside, growth dropped off massively to almost 0 after 2016 in the Auckland market. The median price peaked in March 2017 and then down and bumped along from there. In their chart they predicted at least 5% growth to 3% yearly growth through until 2018 which hasn't happened.

No forecast is ever perfect, but they came as close as can be reasonably expected - look at the graphs again, they nailed it. Got the peak almost perfect. They had growth falling below 5% around mid 2017 and zero by mid/late 2018. Pretty close to what happened. You claimed they said 5% “well into 2019”.

She'll be 'right, eh? Unless she turns out to be a turkey, just ready for Christmas. Markets are risky, they have periods of small changes where statistics are helpful, and periods of chaos where statistics are misleading. Just like the weather, there are a lot more 100 year downpours than there jolly well ought to be.

Started reading the extraordinary Benoit Mandelbrot:

https://www.amazon.com/Misbehavior-Markets-Fractal-Financial-Turbulence…

Scarmongering......... NO Reality.

Day by Day auction is failing unless vendor drops the price.

So called experts / Media trying to prove otherwise but will not help.

It's an arrogant and naive article in it's outright dismissal of alternative scenarios and outcomes.

As I say higher up, opinions that are this definitive are to be suspicious of.

As per this article - House price will never fall in Auckland irrespective of what happens world over.

Reality is otherwise.

False propoganda / news / article.

This headline is frankly negligent. Given the similarities between nz, and Australia how can one possibly say that our housing market is immune to a crash. Sydney, Melbourne and a number of other Australian cities have been in free fall. Investors have left the market. And now anecdotally baby boomers who hold negatively geared investment property are trying to bail too. Nz shares so many features with Australia that to say that this couldn’t happen here is absurd.

Life cycle according to economists:

2010-2016 - Denial: Real estate prices will always go up.

2017-2018 - Bargaining : The market is slowing down -> Prices have flattened up -> We see a small dip but it will not last (now)

2019-? - Acceptance: We should have seen the signs before. These are are regular economic cycles.

And they still get paid for doing their job.

B21 see any parallels to the Bitcoin fiasco?

It's not the first nor the last time we will be seeing a bubble, It's just hilarious (and sad) to see how economists repeat the same patterns over the years again and again.

2019-? Capitulation

“People still want to live in NZ just not Kiwis” spot on. And how sad is that.

My observation is thst increasingly it's people from the third world. Anything is better than there, or so they tell me

“People still want to live in NZ just not Kiwis” spot on. And how sad is that.

I think it is a reasonable article, and is a more probable scenario than the "crash" most commentators here seem to be expecting.

She Expects prices to fall by 5% into mid 2020 and then strengthen.. ( NZ aggregate prices )

She suggests that the fundamentals will keep a "floor" on downward price pressure, in Auck.

In regards to Auckland, she does not see a decline in prices till 2022 as new supply finally impacts prices.

She says:..."Current conditions simply lack the drivers for a large correction. Although we acknowledge that several property markets in New Zealand are currently overvalued and highly unaffordable, we still find it hard to entertain any large downside in house prices. "

Makes sense to me..

ps.. some people have been calling for a "crash" for a while now... As far as I can tell, the stresses and fears that might lead to a deep downturn in prices are not there... ie. the actual microeconomic drivers, and not, so much, the macro - world views.

Scaremongering about a housing correction - Many who have been enjoying speculation and so called boom under national will believe and support - Just like National whose believed that rising House Price to extreme is good crisis (Housing crisis was good - For Whom ?).

Current situation is different and housing market will correct - to what extend once can argue (Already have seen correction of 10% Plus in many places) but to say will not fall - more than the opinion is wishful thinking of all those whose party is over for the moment.

Definitely bookmarking this post. Pretty sure it won't age well. Interesting there is no mention whatsoever of what's going on in Australia and how the will impact the market here. Sydney just hit -8% over the past year alone. There were similar articles to this before and during the beginning of it there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.