By Terry Baucher*

Capital gains tax is the New Zealand equivalent of the Irish Border in Brexit: An intractable issue which politicians have kicked endlessly down the road without resolution. Until now. Perhaps.

The Tax Working Group’s interim report released in September follows this pattern of deferring the dreaded day.

Rather than make an outright recommendation, the interim report instead explains the policy reasons for increasing the taxation of capital and wealth before reviewing two main alternatives; broadening the taxation of realised capital gains from classes of assets not already taxed (the CGT approach), or taxing on a deemed return basis, the risk-free rate of return method.

What the TWG isn’t proposing is a separate capital gains tax regime encompassing the taxation of all gains and replacing the present rather ad-hoc approach. This is an important point which seems to have been drowned out by all the noise around the issue. The TWG is recommending a “targeted” approach to tax asset classes which are not currently fully taxed. Existing regimes such as those for financial arrangements and foreign investment funds (FIF) will remain.

This is an extension of the incremental approach to taxing capital gains which has been in place for the past 50 years. What makes the TWG’s suggestions radical is that it should effectively result in comprehensive taxation of almost all capital gains. The suggested approach should also be legislatively easier to introduce as it would not require a complete rewrite of the existing legislation.

The TWG has decided to follow the example of Canada and South Africa and adopt a “valuation-day” basis under which all the gains from the date of introduction will be taxed. The TWG rejected the Australian approach of exempting assets acquired prior to introduction of CGT as encouraging “lock-in” or the retention of assets in order to defer realising a tax liability.

A valuation-day basis does require obtaining market valuations of assets held on the date of introduction. Much has been made of the compliance costs involved in obtaining market valuations of assets with the view that these costs would be a deal-breaker.

Although such an approach would indeed be prohibitively costly, other jurisdictions which introduced valuation day CGTs have managed to resolve the compliance issue. The TWG noted the Canadian approach where the taxpayer’s cost in an asset acquired prior to the introduction of CGT could be the median of either actual cost, the value on valuation day or the sale price.

Another option would be to allow taxpayers to pro-rate the gain or loss on a time basis. This was one method allowed by South Africa after it introduced its valuation day basis CGT on 1 October 2001.

In short, adopting a pragmatic approach can resolve the valuation issue without imposing unreasonable compliance costs. (It might also require banging a few heads at Inland Revenue which too often circumscribes promising initiatives such as the Accounting Income Method with overstated fears of potential tax avoidance).

Other key features of the TWG’s proposals are that the net gains will be taxed at a person’s marginal income tax rate, no concession will be made for inflation and capital losses will generally be able to be offset against other income. In some circumstances, such as death, the gain could be “rolled-over” and only taxed on ultimate disposal. All up the proposals are estimated to potentially raise close to an additional $6 billion of tax over the first ten years.

But fitting a CGT into the existing patchwork has its issues. The “tax, tax, exempt” (TTE) approach applicable to investment vehicles such as KiwiSaver funds and other portfolio investment entities (PIEs) creates issues around aligning their tax treatment with that of individuals. This was an issue seized on by the New Zealand stock exchange (NZX) and the Securities Industry Association (SIA) in their submission to the TWG.

An answer to the problem identified by the NZX and SIA might be to tax Australasian shares using the FIF regime fair dividend rate (FDR) methodology. In this regard the TWG noted that the current 5% FDR rate was set in 2007 and may now be too high. It is considering whether that should change and whether the present comparative value option available for individuals and trusts should be removed. Alternatively, overseas shares currently subject to FDR could instead be subject to CGT, a move which would raise an estimated $680 million over ten years.

The alternative to a CGT, the risk-free rate of return method (RFRM), was proposed by the McLeod Tax Review in 2001 and adopted for the FIF regime introduced in April 2007. Its attraction is more predictable cash flows for the government and the issue of “lock-in” doesn’t arise. However, it also has issues around valuing assets, taxpayers may not have the cash flow to meet tax liabilities (an existing problem with the FIF regime), and how would it tie in with the availability of interest deductions. Intriguingly, RFRM is seen by some as a better tax solution for addressing housing inequality.

On housing, the TWG’s terms of reference exclude taxing the family home but the interim report raises the issue of whether an exception should be made for “very expensive homes” defined as worth more than $5 million. The suggestion is that imposing an upper limit should act as a deterrent to owner-occupiers over-investing in their property. It will be interesting to see if that suggestion makes it into the final report.

A largely unremarked feature of the TWG’s work is the greater attention given to the implications of the tax system for Māori. This is in marked contrast to previous tax working groups. Māori submitters were overwhelmingly opposed to a land tax, so a policy backed by the last tax working group in 2010 has this time been rejected.

Māori concerns about how a land tax would operate would be equally applicable to the RFRM alternative.

The TWG’s interim report also identified the potential implications of a CGT on Māori freehold land and assets held by post settlement governance entities as requiring further analysis. If a CGT is introduced then a possible exemption for such assets might be one outcome.

The issues the TWG identified for expanding the scope of capital taxation centre on the longer-term sustainability of the tax system in the face of growing fiscal pressures from an ageing population and the fairness and integrity of the tax system. As the interim report notes;

“Taxing capital income that is currently untaxed is likely to provide a significant and growing revenue base for the future. Such gains are the single largest source of

income that other countries tax and that New Zealand largely does not. …The lack of a general tax on realised capital gains is likely to be one of the biggest reasons for horizontal inequities in the tax system. People with the same amount of

income are being taxed at different rates depending on the source of the income.”

Against this background my belief is that despite the reservations of several of its members, the TWG’s final report will recommend the introduction of a realisation-based CGT.

However, it may also suggest that its implementation is deferred by a year until 1 April 2022 to allow time for further consultation. We will be hearing a lot more speculation about CGT for a while yet.

This is my last column for 2018, my thanks to David and Gareth for their support and to all my readers and commenters, thank you for your engagement. Have a great Christmas and see you in 2019.

*Terry Baucher is a tax consultant and director of Baucher Consulting Limited a specialist tax consultancy. He is the co-author with Deborah Russell MP of Tax and Fairness published in 2017 by Bridget Williams Books.

60 Comments

If you're not going to tax the family home, then it follows that those who don't own should have a tax free investment threshold. Otherwise the tax bias to housing continues

If we want to keep this bias, then fine, but let's be honest and admit it's real. Admit it to the renter classes and see what they do with their vote....never!

Rastus, I understand your argument that renters and homeowners must be treated the same from a tax perspective. However, is it the only place that "bias" exists? tax is paid by those who can afford it. Consequently a considerable number of people do not pay any net tax (i.e. tax paid less direct tax credits is a negative number for many). If you are such a purist, then surely this is also a "bias"?

I dont mind to include family home in the capital gain scheme (if that is realisation based system). if you do that, then you will have to allow the house owners to deduct costs such as interest paid, insurance, rates, maintenance etc. as well as other costs such as agent and lawyer fees from the sales proceeds. I bet that in a flat market, many households wont be making much "gains" (after taking into account associated costs). Only people who have bought their houses with their own money (little or no mortgage) are likely to be making significant capital gains

Not sure I'm actually arguing for it. Tax is too complex and intertwined for me to make that call. But, peoples need to accept that renters get no deduction for rent paid, but home ownership gives you that break.

The owning classes, more so landlords, need to acknowledge that renters are not on a level playing field re ownership & tax.

I'd have thought that there would be an annual threshold as it's just not going to be economic to collect otherwise. Maybe the answer is a nominal threshold or allowance rather than specific exclusions? (e.g. the "family home")

There are many people who want to own a home but never will be able to because of their circumstances.....too many children, never able to save because they are a low income earner etc.

There are many people who do not want to own a home

There are many people who want to own a home but will never be make the sacrifices that are required to achieve this.

You are proposing that renters should essentially get a tax break. Low income earners are already well supported through working for families, state housing and housing supplements. Therefore you must be saying that those that choose to not own, or are unable to make sacrifices to enable them to buy a home should get this subsidy.

Here we go again ......

Our practice will make a fortune out of the implementation of this type of tax , doing all manner of business and asset valuations and giving advice to our clients

Lets not forget that CGT is simply a resentment tax , which extremely complex to implement , is highly disruptive, realizes very little in actual collection and does incredible damage to those who are trying to accumulate assets for their retirement .

Its premised on the twin fallacies that because we dont have this tax , house prices have climbed out of control and we are all sitting on huge capital assets that have made us " rich"

It destroys inter-generational wealth , its a disincentive to capital formation .

Its just plain stupid

I agree. It is a stupid tax. No one with any sense can deny that.

However, you people really need to understand tax a lot better.

Sure, it affects the accumulation of wealth. But why should anyone be subsidising your accumulation of wealth in the first place - what an uneven tax playing field does in the first place.

"It destroys inter-generational wealth , its a disincentive to capital formation."

What do you mean by "It destroys inter-generational wealth"?

How is a realignment of intergenerational wealth at all bad? Ya know, it is good when the younger generation can afford to live in productive areas. Because, well, they need to pay for the old ones..

Yes. It will have an impact on capital stock. Which is another reason why it is a terrible tax.

However, with supposedly smart people unable to reconcile deemed rate of return or land taxation, it is that we are left with.

Maybe it's not a case of "understanding tax a lot better" and maybe those other options are just rubbish as well.

Why are people subsidizing my accumulation of wealth, the money earn't to pay for it was taxed, at the end of the day I started with a house, paid to upkeep that property, and I ended with a house, what real wealth did I gain. Yes if you are in business of buying and selling houses to make a profit then yes you should be taxed, I think that is how the laws is technically law, but it needs to be better defined. I would suggest negative gearing is one indicator, if you are never paying anything off but simply buying more properties based on that equity you are clearly using that equity as profit.

The problem is people see having a house worth millions of dollars as a good thing, its not, I still just a place to live, if it is worth $1 or a million. But if houses cost millions of dollars then the people around me have to be paid enough for them to have a place to live (rent or buy) so all my costs go up. I also worry that my children or grandchildren won't be able to afford somewhere to live. I am no longer saving for retirement but to have a place where my children can live. I would be happy if my house price halved tomorrow. Even if I had a mortgage say I owed half a million, I would still owe half a million, and the bank would not reposes as long as I kept paying it off. The only people that make real money on high house prices are property speculators and banks.

Capital gains will not reduce house prices because the you only charge it on profit, you just make less profit. Build more houses we don't have enough houses for people to live in.

hmmm. I'm not sure on a few points.

"Its premised on the twin fallacies that because we dont have this tax , house prices have climbed out of control and we are all sitting on huge capital assets that have made us " rich""

- It's not the biggest reason for house price growth but it is definately part of the equation, and those with assets have been advantaged over those without (again, a lack of a cap gains tax is not the be all and end all but it is part of asset inflation.)

"It destroys inter-generational wealth , its a disincentive to capital formation."

- Is it a disincentive? It's a disincentive to realise the gain which would encourage less speculation and more focus on what an asset can actually produce. I don't think that's a terrible thing.

CGT definately has it's drawbacks, as you say it's complex to implement for example. If they could reduce income tax due to implementing it I think that would be a mostly positive thing overall.

Boatman right on the money. Instead of a Capital gains tax, lets collect the tax which are currently exempt from paying tax Charities that are just fronts for people to earn a living, Foundations like wise and the benefits from Racism type policies.There is no incentive to save for your retirement. Spend it today or this Govt will take it off you. Let us not forget that New Zealand was in a recession in 2007 before the GFC and no medals for who was the Minister of Finance at that time. He he is again with his Ideological ideas. National Spent 9 years getting New Zealand back on track and a stable Economy Sure they still had a lot of work to do. But this Govt is just blowing all the hard work down the drain. People want to be rewarded for their endeavor not wards of the State collection Beneficiary payment all their life.

Having lived in a country with capital gain tax I can tell you one of the first reactions, don't sell. In California CG tax can be as high as %40. You don't sell your house unless you have another one to buy or already purchased. I have a friend with three houses in the bay area, Kiwi, done well but he can never sell, he would get hammered and being a non resident extra hard with CG tax, I think %11 extra for non-residents.

I have talked to farmers desperate to buy a farm before they get caught by the tax after selling to developers and it got down to just buy a farm any darn place will do we have 3 months till we lose %40 of our capital.

The worse thing is CG taxes are giving the wrong signal, watch the rich get out of it and the middle class get hammered.

Deemed rate of return based on values will fix that. It will also prevent land banking and return farms to affordability levels for new young farmers.

I don't know if the lenders to the sector are going to vote for that

Im sure many here will be pleased to hear that I’m off to Australia for good if this country ever ends up “taxing on a deemed return basis, the risk-free rate of return method.”

What was it Muldoon said about people like you?

I hear there are some real bargains emerging in Melbourne and Sydney, fill your boots.

You know Aussie has a Capital Gains Tax, don't you! And if we here in NZ are their 'test case' ( which we seem to be on all manner of things, being so much smaller and all) it's just a hop and a skip to them also enacting what you are trying to escape!

The Australians have a capital gains tax, but it is not based on "a deemed return basis, the risk-free rate of return method.” Look into it.

The opinion pieces are rolling out with all sorts of misinformation, and scaremongering. I do agree with Boatie that it is a resentment tax, but with a big BUT. Property investment is largely a business built on capital gains and i feel that should be taxed on the capital gain, when it is realised, either by a sale or by borrowing against (the costs of that borrowing should not be tax exempt).

However i am concerned that Cullen is an ideologue, and is blinded by ideology rather than a balanced perspective, that allows ordinary people to get ahead as well as business's to function.

Plus i always understood that no matter how long you had a property any captial gain achieved when sold was always taxable? Is this true? If so why hasn't it been done?

No you did not necessarily have to pay tax on capital gains from realised from property. The law thus far has been very "loose", it is based upon your intention at the time of purchase. i.e. in the past, if you bought a house with the intention to keep it long term but your circumstances changed after 1 year, you wouldn't pay tax on any gain. You could do this once and get away with it but the IRD would come knocking on your door if there was a history of such dealings. Still, a very elastic rule

Tax is an "arbitrary imposition", ( for want of better words ). Tax is not really based on any kind of economic rationale, it is based on the "will of the govt".

Using arguments like Capital gains is a double tax , or an envy tax, is pointless in this context. (GST is a double tax on income. )

Using logic that presumes pretend income that is untaxed and therefore justifies taxing it, is also pointless, and takes one down the "rabbit hole" ...as the idea of imputed earnings can be applied to anything.

Attached is an article about Capital gains tax in USA... Its worth reading.

The better argument is not about "double tax" but about the material effects of having the tax, in relation to the total tax on a sector. Fairness, equitable, distortions/effects ..etc are the tests that might determine if a tax is a good idea....or not.

eg.. NOT allowing a depreciation component on income earnt from savings is unfair.

Taxing inflation component of a Capital Gain is unfair.

It is the total tax on Business that is important, and it is the mix of those taxes that really determine the material incentives and effects. ( eg.. pursuing income over Capital gain )

ie. Corporate tax rate + dividend tax + Capital gains tax. = total tax

USA has a Capital gains tax... this article is worth reading

http://www.taxhistory.org/www/features.nsf/Articles/0C43B0D6D127333E8525...

Agree with the "double Tax" perspective. Don't forget that the concept of GST was to replace income tax in totality with GST which is in effect a consumption tax. Of course the politicians screwed us, by keeping both - again!

The Australian CGT system is simple and neutral and indexed for inflation - it doesn't collect a lot of tax - it was/is easy to understand and accepted by the people

The TWG proposals are so complicated (and, with a background in taxation) I have difficulty understanding them - so best of luck with selling the stuff outlined above by Baucher to the great-unwashed - the Cullen proposals are doomed to fail

Governments and the IRD have been unable to enforce the existing legislation for decades - so the solution is - lets design another scheme and see how that goes

Best of luck

My understanding is the Australian CGT has not been indexed since 1996. However I agree with your sentiment; Cullen seems determined to tax people who own things and give it to people who don't.

There is also another factor; the ringfencing/investor changes haven't played out yet and won't until March 2020, when investors who were claiming losses gain no appreciable benefit from a rental in the face of little to no accruing gains. This is not something that NZ has ever had to deal with before; I would rather see how that plays out before we even bother with this sort of discussion.

Cullen seems determined to tax people who own things and give it to people who don't.

There's plenty of Superannuates who own things.

Nzdan, what is your point!!!!.

so simple .. that you do not actually understand it. Inflation indexing has long been removed.

I'd add, to what I say above......as an example.

I have friends in farming...

When my father was a farmer he farmed for income.

My generation ( my mates who are farmers) told me they were in 2 businesses . One was "farming " and the other was real estate ( Capital gains ).

Their way of avoiding paying too much income tax was to borrow and buy more land.

This all made sense to me.

One on the unintended consequences was high farm prices, low returns on investment and a sector with a debt burden.

One only has to look at the marginal productive value of a hectare of land versus the marginal cost to see that this is definitely the case.

The only business farmers are in these days is the business of farming tax free capital gain.

Correct. The trading income is to cover the cost of ownership. The real profit comes at sell-up - hence the problem we have with farm succession. A terrible way of managing a key industry where new, young,bright and progressive people with skin in the game are essential.

I think Maori will sink this one. It will fly with enough people with an exemption on the family home to pacify the masses. Any exemption offered to Maori so that land they are sitting on doesn't place a tax burden on them won't be accepted by the masses. And it would be just too divisive. What government would want that on their hands?

Hamish, won't be a problem for this Govt. Let's Do this.

Great earner for accountants and lawyers. Unintended consequences, unforeseen consequences, subtle destruction of society by disincentivising capital accumulation. How to set us argueing amongst ourselves, all because Michael Cullen and company caused house prices to income levels to surge. Talk about the fox running the hen house.

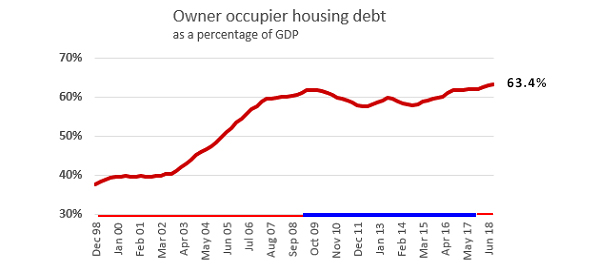

https://www.interest.co.nz/property/97275/yes-housing-debt-growing-perh…

https://www.interest.co.nz/sites/default/files/embedded_images/housing-…

{kind=link}

RogerW. Fox is right. His recent comment that 'we are not supposed to be looking at inheritance taxes but a majority of my colleagues on the TWG "appear" to have a found a way around that' was about as slippery as they come. My translation: 'we've specifically been instructed to not look at these two taxes but I know better and have decided to expend taxpayer money to do what I want but I'll spin it as some members going, you know, ahem, a bit rogue, like, sort of , cough, without my knowledge'.

Any enaction of CGT under this govt will be horrendously inefficient, because they will write in exclusions for various clients/voters of theirs. It has to be on everything including the family home or not at all.

A better option would be: a universal property/land tax at 5-10x current local body rates, with option to accrue it against the property title if no cash to pay it (for pensioners etc)

Another sensible option would be ending deductability of interest payments from income for tax purposes, as it represents and huge and unwarranted subsidy on property investment.

Wow. At 10x local body rates that would be more than our home has apparently increased in value in the 11 years we've been living in it. Even at 5x that's over 50% you want to tax us. Are you open to haggling?

Was it Roger Douglas and his flat tax rate,if so ,come back Roger all is forgiven.

I don't see that Terry B is thinking like a politician.

My prediction FWIW is that the attraction of the regular cash-flow from the RFRM method, and the ease of the tweaks to the deemed rate (regulations, in effect from lunchtime tomorrow....) will prove irresistible.

So RFRM, an easily changed deemed rate, and a wide definition of 'assets' - that definition itself easily changed - by Regulation, naturally - will win out.

We'll be the Social Lab-rats once again - get on that there treadmill and start pacing, all youse rich pricks....

I know, let's follow France....

Waymad. I suspect your prediction is correct that RFRM will prove to be the least worse option for the coalition but it still leaves the issue of affordability for high asset/low cashflow entities. The impact on farmland values would be significant and the opposition has already identified the political vulnerability through the Bach being dragged into a RFRM net. Peters asset rich heartland constituency would be heavily affected. Enjoy your treadmill fantasy but stock up on the antidepressants for the letdown.

Thx for yer kind response, but be sure that I am in no way invested in any particular outcome. I know politicians too well to expect anything but Yet Another Cash Grab, despite the lofty sentiments that will undoubtedly be wheeled out to support it.

I don't see why a capital gains tax needs to be complicated.

2018 buy an asset for 100k.

2025 sell an asset for 150k.

20% tax on gains = 10k.

No inflation adjusted, no write downs, no kick backs. Just a straight line approach.

Do it for all assets including family home, shares, any asset sold for over $X amount. Dividends or income from shares / rent is taxed at the nominal rate for the person/company who owns them.

2018 buy an asset for 100k (20k deposit, 80k mortgage) First Home Buyer.

2018 - 2040 pay down the mortgage from taxable income

2050 - sell asset for 500k (average house price)

20% tax on gains = 80k

After selling an average house for $500k, the person now has $420k to spend on buying another "average house" worth $500k.

TM, indeed you do not see "why a capital gains tax is complicated"

TrappedM. You make it sound simple which it is for most listed companies but I'm guessing you haven't had much exposure to buying or selling privately owned SME's. For these entities wide variations in formal valuations can be achieved though manipulation of various factors considered in the valuation process. Valuation of larger businesses is a complex and contentious exercise, a reality that CGT advocates such as Cullen and Rashbrooke are well aware.

MiddleMan, can you please explain more?

I am interpreting your comment that the SME value can be manipulated when sold and thus not easy to calculate CGT? The value only matters when its sold. If i sell a SME for $20mil then that's the value that we need to base the CGT off, just like share price fluctuation. It is a little mirky when you build a business from $0 to $20mil and then you get taxed off the full value (will think about this further).

One example is a personality centred business where the value is influenced by the extent of the incumbent proprietors ongoing presence. Equity can be extracted from a business through various and more tax efficient vehicles than a single hit at marginal rate CGT payment to the taxman at time of sale.

The vicious scraps over business valuations in divorce scenarios provide some insight into how contentious and variable valuations can be.

Would your point not be moot? If the value is based on a person(s) then if those people leave with the business sale then the sale value should reflect this. If the person(s) stay in the business then again the value will reflect this. You have to put a $ value on the business at time of sale, and that $ should be taxed. The value is based on all tangible and intangible factors of the business position. Divorce will always be messy but should not complicate the process that much as long as one party in the divorce keeps the business.

To which one can add plenty of variations:

- Goodwill and other intangibles. Flip a coin...

- Assets just marooned via ongoing technology changes (e.g. patterns and molds invalidated by 3-D printing)

- Instructions to the valuer: in the old days of Gifting, valuers would be told to low-ball it...

- Legal challenges with the attendant costs and time delays which alter both the timing and value of any sale e.g. a messy liquidation of a business' major debtor in the middle of a sale process - Debtors are Assets, remember

- Assets which aren't on the books at all - asset registers, unless ruthlessly physically audited, are quite unreliable beasts

Sorry if I am confused but I don't see how this matters in the end. If any of your points above alter the sale price then the % of CGT paid is also altered. If someone is willing to pay more due to good will then extra tax. If you are gifting at a low price or $0 then the tax reflects the final price. If assets are marooned then the final sale price will be lower or the business will have to write down their valuation. Either way CGT is paid on what someone is willing to pay for the business at the specific time of transaction.

TM, your comments apply only to a Realised regime. I and others are exploring the plentiful glitches apparent in an Unrealised (Deemed/valued, think-of-a-number-and-tax-it) scheme.

So it matters not whether there are buyers, sellers, timing or other issues. On VA (value-Assets) day, the deemed value is all that matters, and the comparison with Last FY's equivalent.

So defining what 'asset' means, having a List of the assets thereby caught, and a valuation for each that will withstand IRD's stern gaze, is the essence here. No sale. Just a valued list.....

The appeal of the RFRM approach to always-cash-hungry pollies is easy to spot....

OK. So capital gain is to be treated as income. the CGT will raise $6.6bn over 10 years. So that will be factored into spending plans and of course, being revenue neutral, income tax will be cut accordingly. So we have the mother of all crashes, ie 1986, 2008, and the capital gain is gone. So how will the govt of the day fill the shortfall - by borrowing of course. And will the person who sells at a loss get a tax credit?

If on valuation d-day, an asset is factored in at $100,000, then sells after a crash for $70,000, can the new owner get an effective $30,000 tax free when the asset price rises? And of course, many capital gains look much slimmed when inflation is factored in.

I might retrain as a tax practitioner. Business is sure to boom.

Waymad. Yes, lots of ways to skin the same cat. Skilled minds are already at work in contemplation. Three aspects in respect of CGT on businesses are certain - complexity, cost and avoidance for those who can. While mum and dad are helpless as their kiwi saver accounts are raided, the family bach is pillaged and part of the grandparents house is confiscated by the state when they die. The socialists rail against inequity while creating a CGT system that will deliver just that.

Certainly, there will be no new investment from the middle-income folk. Where is the incentive to do that?

With no incentive to save and invest, then people will just convert to a consumption only economy, with no growth whatsoever, and no retirement savings or investment returns.

The CGT should work the following way:

1) apply to all properties including the home

2) be scaled back over time, i e, 100% tax within 1st year, 90% if sold between 1 & 2 years after purchase, 80% 2-3 with tax decreasing by 10% for every additional year held until there's no CGT to pay after 10 years.

This will naturally discourage speculation without hurting home owners and will be easy to police as there are no exclusions

The plan is to to continue devalueing the currency to create the illusion of capital gains, thus destroying the property owning classes. Result, all assets owned by either incompetent bureaucrats and politicians or ruthless overseas corporations. A La France.

CGT won't float with the 5% or so who are reluctant Labour voters. So Labour won't be around to implement it.

SMEs, the lifeblood of this economy, are already treading water and this will simply be the last act before the decline of this economy really gathers pace. With a large percentage of people holding their life savings in businesses (backed by property collateral), commercial and/or residential property, this will be a confidence killer of epic proportions. While the socialists might cheer this on and say “so what if the next generation doesn’t inherit anything, it will make everyone more equal”, the reality will be significantly lower standards of living for everyone. Employment levels will plummet as SMEs stop taking on staff or even downscale. As Roger has stated, we are heading down the same disastrous path as France and other failed socialist states. The only growth employment areas will be tax experts, govt employees and consultants and other such productive types...

SHOW ME which IWI or Maori Trust will EVER agree to having its assets taxed on the basis of a "deemed rate of return "

It will sink all the trusts in one tax year

Its going to lead to a showdown between Maori and the Government if this ever happens

Agree with Boatman. This will never happen as an across the board tax. Labour would loose the next election by a landslide, and it would be immediately repealed under urgency if it had not already been defeated in the house. I suspect the CGT boat will be pushed out with the residential speculators as its primary target. How would you target that you ask - simple - any residential asset that has claimed any degree of tax loss finds that this applies.

One adds a key quote from the TWG interim report "With your contribution and mine, the people will prosper". Says it all really.

Read appendix B. https://taxworkinggroup.govt.nz/sites/default/files/2018-09/twg-interim…

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.