There is a widely held view, especially among armchair analysts, that New Zealand households are loading up on housing debt.

It is a reasonable conclusion to come to if you look at the monthly data released by the RBNZ.

In the year to September (all the data in the piece will be based on quarterly data), total housing debt rose to $254.8 bln (RBNZ C5). That is a rise of $14.4 bln in a year or almost +6.0%. Total mortgage debt never seems to reduce.

$254.8 bln represents 88% of GDP.

And +6.0% growth in mortgage debt is far higher than the growth in household incomes. The RBNZ has recently released data (C21) that shows these up +4.7% (the RBNZ definition of household disposable income is before taxes and includes interest earnings).

So yes, mortgage liabilities are growing faster than household incomes.

But I believe using these gross measures can lead to superficial conclusions.

Firstly, we know that we are consenting about +30,000 new dwellings each year. These dwellings take about two years to build, so those new builds in the past year are those consented two years ago, or about +28,000 annually.

And a check of Statistics NZ dwelling data confirms that. Our dwelling inventory is growing at the rate of +1.5% per year or 27,400 per year. But that same data allows us to separate out the growth in owner-occupied dwellings from rented dwellings.

This separation is important because residential renting is a business activity. Households involved in that are involved in a business and the liabilities for that are those of the business even if they are unincorporated..

Just focusing on owner-occupied housing, we are able to calculate that the average loan on this housing stock is only $185,200. Of course, many households will have no mortgage liabilities, and many recently formed households will have substanbtially higher housing loans. But the average loan size has only been growing by +$9,650 per year. In the nine years to 2017 that growth averaged +$5,000 per year per home owning household. In the nine years to 2008 that growth averaged a remarkable +$6,600 on much smaller balances.

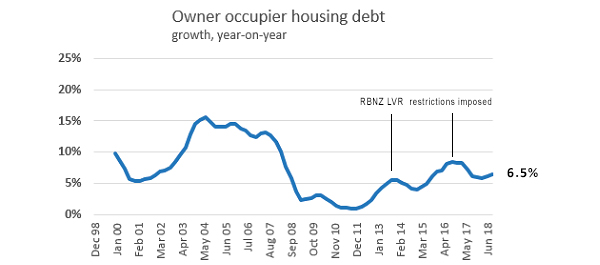

The same year to September 2018, on a per owner-occupied house, mortgage debt rose +6.5% pa while after-tax take-home pay rose $1,827 or +2.2%.

So it is a fair conclusion to say that households are taking on more housing debt in the current cycle even if those overall debt levels are relatively low and even if their rising incomes could pay off that increased debt in only 5 years. Again, these are averages but not a spooky levels.

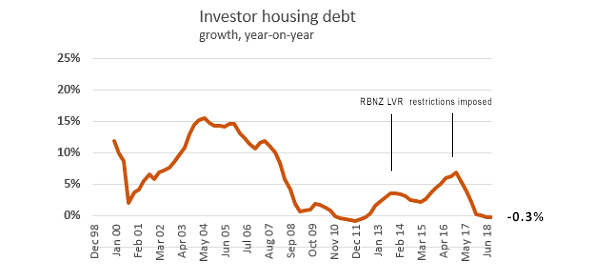

We can also do this same analysis for rental properties. These are typically a lower quartile properties. After adjusting for the growth in the number of properties for rent, the loan amount per property is actually very stable, unchanged at an average of $109,500 per property.

This lack of growth is a direct result from the application of LVR policies.

But rents (3 br house) grew by $1,040 in the year to September.

Capital gains may have ended for many investors and they have definitely been restrained from taking on more debt. But their investments are turning to recovering yield after a long period where it has been head-scratchingly low. However, they may have to suffer an extended period where yields creep out of the basement while they reap no capital gains. They have the RBNZ's LVR credit tightening to thank for that position.

At least interest rates are unusually low.

For most investors, in fact most owner-occupiers, their average debt levels are not high by any standard. Credit ratings agencies - and Fitch is that latest to say it - don't see special pressures here like they do in Australia. And tighter credit assessments flowing from both New Zealand regulator actions (FMA and RBNZ), self-imposed responsible lending codes, and as importantly, the Hayne Commission pall that hangs over all Australian-owned banks, will all work to ration the lending impulses of banks to only those with the best financial situation.

Unless, that is, you are buying a new build. The rules and restrictions, especially around the LVRs (deposit levels) required are far looser here, by regulatory design. The KiwiSaver piggy bank for many now has balances well in excess of $30,000 and certainly enough for at least a 5% deposit on a first 'home' - KiwiBuild townhouses if you are lucky, but apartments if you are not. Banks, supported by the Government-backed Welcome Home Loan program will be ready to lend on that.

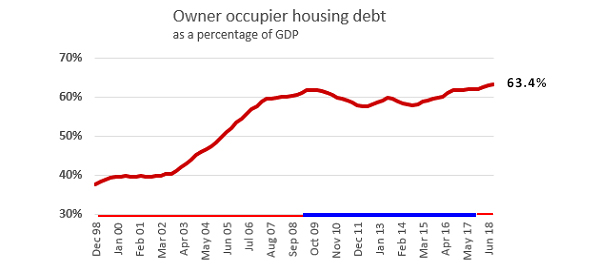

Housing debt by owner-occupiers is only $185.4 bln or just 63% of GDP and that is far less than armchair analysts assume. Even more interesting is that what really juiced it up to this level actually happened more than 15 years ago - the raising of the margial income tax rate to 39% which unleashed the impulse to find a tax shelter. The genie was then out of the bottle and we live with the consequences even now.

42 Comments

Total Mortgage Value divided by Total Number of Households?

What about Total Mortgage Value / Total Number of Mortgaged Households?

Home Owners and Landlords with no mortgage are not a financial liability so they shouldn't be counted in the data.

Very good point.

Another question (apologies if this has been answered elsewhere): what about unused lines of credit? Do the aggregate debt statistics reported in this article take into account flexi loans' borrowing limits, or just the debit on those credit lines on a particular date? I've often wondered whether there is data on NZ credit lines securitized by real estate. I would think that fluctuations in flexible credit lines and the percentage of the debit limit utilized could be an interesting number to track. It would also be interesting to know if many property investors fund purchases with these lines (e.g. what is flexible credit lines' share of total mortgage debt?), perhaps switching them to fixed term on settlement of the silent purchase agreement. I know some who use their flexi lines as an upper bound on what they will bid unconditionally at auction. Therefore, changes in untapped credit lines could give some information about latent demand among investors at auctions. Thanks,

DC

The problem for armchair analysts is a lack of data on how the debt is concentrated.

As the percentage of households that are owner occupied has reduced over the last few decades has that meant owner occupied debt to GDP may have actually been growing more than it appears?

My main challenge would be, if the situation really is as benign as suggested, why are such a high proportion of loans made at DTI ratios above 5 and above 6?

In Australia it's not the "battlers" with mortgages who are seen as being the highest risk it's actually the more affluent young households who have leveraged good incomes to the max.

I'm not even sure to what extent the RBNZ would have the necessary data on debt concentration? The banks are perhaps the only entities who would have a good handle on it.

"My main challenge would be, if the situation really is as benign as suggested, why are such a high proportion of loans made at DTI ratios above 5 and above 6?"

Fair enough. But you are right, we don't have any data like that (or the number of properties with mortgages). So we are left with what we do have.

And that includes C35 which gives the overall total of what repayments are, and C21 which gives total household disposable incomes. If you adjust the C35 data down to just the household elements (excluding the investor stuff), you get that they repaid principal and interest in the past year of $21.0 bln. And that is only 12% of household disposable incomes. That is very low indeed and is another sign this risk is quite benign right now. (And even if you included all those rental business mortgage repayments+interest, it would only rise to 16.4%. So in a worst case scenario, it's not too bad either.)

Yes, you will always be able to find anecdotes of folks in stress. And there will be more of them among those who took out a mortgage obligation in the past five years. But even among these, the chances are those in stress are the outliers. And in five years, most of them won't be in the stress group.)

C35 has Schedule Repayments (even the RBNZ doesn’t call it Principal and Interest Repayments, which it isn’t!) of $4.3 billon and Full Repayment of $9.2 billion. I find it odd that Full Repayment would be so much higher than Scheduled, but there you go (transferring lenders and paying out the existing one?) Other Excess Payments of $3.6 billion. So I can’t see Household Element being as high as $21 billion?

average NZ mortgage is around $400,000. Higher in Auckland. The concentration of debt is the concern and the credit impulse needs to continue to grow at 6% or more next year. What happens if the increase in the number of sellers (which we will see after Christmas) is not met by a similar enthusiasm for debt?

Answer. Sydney 2.0

Would be interested in your souce for "average NZ mortgage" as $400,000.

And I thought your "increase in the number of sellers" was going to happen before Christmas. ?

Impartiality be gone! David joins team Spruiker.

What David appears to be saying but can't quite bring himself to actually spell out, is that his analysis shows that It was Labour wot dun it. National promised hand on heart to fix the housing problem and failed dismally. So now, in a deliciously ironic twist, those who were not yet earning taxable income under Clark and Cullen have voted Labour back in "to fix the housing problem". C'est la vie.

To be fair, I thought socialism had more promise when I was younger. Now I suspect it encourages self delusion about the real causes of social problems. In short, it encourages those in office to accept simplistic analysis at face value, and so they stop digging deeper into the problem. So the causes are left unidentified and the rot continues.

In this way Labour tend to penalise the behaviour that the structural incentives encourage. Whereas the Labour philosophy brands itself as non-authoritarian, this is a delusion. Labour philosophy, in it's present form (not in its self help society origins) is based on the idea that people are basically devious and need keeping in line. So once a group who can be blamed is identified they legislate punishment and delude themselves into thinking they have solved the problem.

A better way would be to identify the incentives that create the perverse outcomes and change them. In this case a system based on government promotion of asset price inflation leads to unequal outcomes. Gosh, who would have thought?

https://finance-commerce.com/2018/10/paul-volcker-whats-wrong-with-the-…

Great article David.

I believe both the left and right are authoritarian in many ways - any restriction could be considered authoritarian. While I would like to think people would act like decent human beings and cooperate, I'm cynical enough to recognise that humans are a rapacious lot and no amount of PC indoctrination will change that. The current political climate I think just amply shows our true human nature / rant mode off.

Overall I think we just don't have enough information to really know what is happening out there regarding people's finances - the banks may have a better idea but I still think they will be hoping and praying that everything is all right and that people will be able to continue and pay their mortgage.

Of course both left and right can be authoritarian just as they can both be libertarian. The political spectrum is not linear, it looks more like a graph. Right and left should only be looked at in economic terms, left representing the collective, right the individual, then on the up and down you have authoritarianism at one end and libertarianism at bottom. Go to the www.politicalcompass.org you can do the test to see where you sit, but it is interesting to see how we can structure mixed economies with aspects of both socialism and capitalism, which I am absolutely convinced is the right thing to strive for. As for the authoritarian v libertarian one of the first things I worked out was that the left-lib quarter was most probably where the person we think of as Jesus Christ would fit most comfortably, while in the authoritarian right corner is where you find conservatives as we think of them here in the west, who tend to be the group that purport to worship him - oh the irony of that one. I came to the conclusion that he would have fit there, as lib-left would work really well if we lived by the do unto others mantra.

I guess I was trying to figure out the reason Labour often seem to lose the plot and achieve the opposite outcome to the one they desire. Both parties have their weaknesses and I was ignoring National as they are not in power now and it looks like it was Labour policy that stuffed up the housing market. As David alludes, Cullen set out to reduce inequality (presumably) with his punitive tax rates on "rich pricks" as he put it. Result, more inequality! How does that happen? Clarke and Cullen were both competent politicians, they kept NZ out of the main Iraq invasion force, they sorted out the government books, and yet they appear to have caused a widened rift in our society that so far resists a solution. If we understood how that happened we might be better able to solve the problem.

Probably quite simply because we had gone down the neo-lib track and it isn't easy for them even to turn it all around. They were still operating in days of if you mentioned the word "union" you got your mouth washed out with soap. It has only really been since we found out that Helen Kelly was terminally ill and how she subsequently went about her life after that, that we began again to think they might have some relevance. The solution lies in some socialistic policies and that one we are still grappling with. We had them before, we need them again.

It is, after all, the voting public that decide much of this, this government is constrained from full on sorting things by narrow margins and NZF.

The younger generation, should they become politically active will have much effect, as it is them who are being the worst affected, especially with the rise of robotics and technology, and I do not buy that will be plenty of work as this evolves, there won't be, not much that is long term, full time and not on a contract basis.

Having said that, there are very rough waters ahead, as we do not seem to be able to agree on if we have serious problems, leave alone how we fix them (climate change, pollution, you name it).

The Labour party is not socialist by any stretch of imagination. Given Ardern’s Blairist credentials and merely looking at the Labour script all the way back to the 1980’s it never ceases to amuse me how utterly contrived and artless so much of the Labour rhetoric has

been yet there are die hard supporters, bless em, who patiently abide a level of false ingenuousness and rather pedestrian outcomes (at least in terms of any meaningful socialist or left leaning agenda) on which their support is predicated.

You might be onto something there. They still seem to cling to Stalinist ideas about the economy; Blairite ideas about imposing "democratic" solutions on countries that regard those ideas as Western Colonial Oppression; and seek to impose anything goes, Cultural Marxist, anti-Christian concepts on all. They also seem to reject the idea of the sovereign nation state, the cornerstone of democracy, instead supporting a dangerous globalist agenda to impose global agreements on all. All of those are in opposition to the self help and co-operative movements that gave life to the Labour movement. Why, why, why?

Roger, to the dismal record of Unintended Consequences that Labour hath wrought, one can add the two below, to the ruinous 39% 'rich pricks' Cullen tax of yore:

- The stupid squared decision in 2002-3 to set the housing inflation fire a'burning via the wholesale introduction of a Welcome Home Loan price floor nationally. All of a sudden shacks worth peanuts (in my case $47K) were re-priced literally overnight with a '1' in front. Universal Pricing signal....

- The Sandra Lee amendment to the LG Act, which introduced the 'four well-beings' to TLA's. Who responded to the Social and Cultural spend possibilities as one would expect: with huge enthusiasm, little to zero competence, and using OPM via rates to plug the fiscal gaps which, whodathunk, emerged soon thereafter. Any chart from 2002 onwards showing inflation-adjusted rates will point one way - towards the top right, and at a swingeingly steep angle. A warning to all who pay rates: Bill 48/1, before the current crew, seeks to reinstate the Four Wellbeings in all their glory......

We never learn, it seems....

As capitalism (as its name infers) relies on growth, it is not really the system that will get us through a desperately needed time of down-sizing, in both our population and resource use.

How can you possibly say that? Capitalism is always flawed, it is always sub optimal. That is because it is an evolutionary system. The centrally planned systems of resource allocation and population depletion of the likes of Mao, Stalin, the Nazi Party, Pol Pot, Cuba, Venezuala and North Korea are much more scary.

"it encourages those in office to accept simplistic analysis at face value" - funny, I always think that of right wing. For example, the right wing solution to crime is always more jail time - regardless of the fact it hasn't worked in any other country. The right wing solution to Auckland's congestion problems is to build more roads - I don't think that has ever worked before either. The right wing deny climate change even though almost every academic says it is happening.

By the way it is quite possible that all that debt racked up under Labour was due to pay increases - people now had the money to upgrade their houses, they felt safe in their jobs, life was pretty good during those 9 years.

It's half hearted analysis like this that lead to the GFC. Debt is at all time high, and when Mr. Simpleton reads this they think life is still good. Let's take on more debt

David can we get an analysis on retirement savings. Both mine and my partners parents have all savings in the house. I would like to know if this is common or not. Low mortgage amounts avg across all households is great, but how is savings as well for retirement. If they are banking on high prices to pay for retirement.....

RBNZ C22 has a household asset item that covers this. It shows that insurance equity and superannuation funds now total $100.9 bln which would be regarded as 'retirement funds.

In addition households have another $73 bln in 'investment fund shares', plus another $71.3 bln in unlisted shares, plus another $177.1 bln in bank deposits (which may or may not be available in retirement). That doesn't include a further $326.7 bln in investments in unincorprated businesses.

All up, household financial assets (not including housing) total $890 bln. That is far, far higher than what they owe for housing ($254 bln at most, although a good portion of that is a business liability, so it is more like $185 bln as a household liability).

Thank you for your response David. Very very helpful

Another question for retirement is the type of lifestyle your parents are going to have. If they have a house with no mortgage and superannuation then they could live on this. They may want to downsize or get a reverse mortgage to cash out and have a higher standard of living. It would be helpful if they had some other liquid financial assets to try to maintain their current lifestyle.

" The regulatiory restrictions are doing their job well " so what does the RB do - Change them

Houston, we don't have a problem. Bad news for DGM/armchair analysts.

Agree with you skudiv

I do read postings talking of corrections of 30% plus in the housing market and reference being made to collapses at the start of the GFC USA (the sub-prime fiasco), Ireland and Spain with the claim that the same may likely happen here. While there is some risk of a correction in NZ being compounded by banks having to "foreclose" in some instances, we seem to be well regulated and not in the same precarious situation as the above examples (and seemingly, currently including Australia).

Having said that, if I was a FHB - or a homeowner with high debt levels - I would be taking the current window of opportunity with historically low interest rates to be paying down debt as quickly as possible as in the medium to longer terms it will be more about increasing rather than falling mortgage interest rates.

Interest rates will only rise if inflation rises, and if inflation rises it reduces the 'real' mortgage value, currently even interest only mortgages are being reduced by 2% just because of inflation. This is great power of inflation it eats away at debt while you do nothing. I'd love a period of hyperinflation like they had in the 80's, so many people I know were set up for life by being in debt and holding onto their assets.

Don't quite agree with you here skudiv; "Interest rates will only rise if inflation rises".

It is all to do with factors such as bank's ability to borrow money to lend and this includes influences such as the OCR.

Fortunately NZ banks' funding are just over 70% (up 10% over past decade) domestic and just under 30% offshore (refer link below).

While only 30% is offshore, there is upward pressure on international interest rates as US has finished with QE and a tightening of money supply, so global interest rates - including US - are climbing higher and this could have a significant impact on the international sourced funds. I would also be looking at events in the Eurozone with increasing risk there and consequently increasing global interest rates.

Domestic funding. Well as one with some cash investments, these are frustrating low and it would seem in inflationary periods they could also continue to be frustrating low while there continues to be adequate source of cash funds such as through KS.

As for domestic inflation - well RBNZ will be endeavouring to keep that at current levels so it should not be a significant contributor.

https://www.interest.co.nz/news/86326/we-look-detail-where-banks-source…

DGM's just look at the debt total and start waving their arms in the air and start calling it a Ponzi scheme. The data you really need to drill down to is the data you will never get however and what really matters is your total income vs your outstanding debt. Its simply your ability to be able to repay it and cope with increased rates, which is what the bank should be doing (and has been doing) as it can only be done on a case by case basis. If you ability to repay is still there at 7% interest rates then you should be okay for years to come regardless of the debt "Total".

But as you say we don't have access to that information so neither side can make any judgement as we simply don't really know......

DGM's just look at the debt total and start waving their arms in the air and start calling it a Ponzi scheme.

1. DGMs look at total debt and says scary ponzi scheme

2. Now that we separate owner-occupied debt and realise its not too scary

3. What if we take the non-owner occupied part alone, will the debt not be far more scary than DGMs initially painted ?

DC, the problem I have here is you are taking averages is, a) a decent number of homes have no mortgage/debt. Those that do however have the FHB contingent that carries a high debt level in a housing bubble. ie burst that bubble and then its a lot of negative equity. b) With leverage in play it doesnt take a huge % of FHBers going into negative equity to pose a risk to the banks?

Then there are the "landlords" who have significant debt and who it seems the banks target when things go adrift rather sharply.

My concern is I dont see a linear event/decline but something that can accelerate out of control.

Agreed. Landlords with significant debt should be handled differently and tracked in an semi isolated way for reporting and management of risk.

According to Census 2013:

Of those households who owned their home and specified whether they made mortgage payments, 56.4 percent (398,373 house holds) made mortgage payments in 2013. This was very similar to 2006 (56.5 percent or 405,267 households).

http://archive.stats.govt.nz/census/2013-census/profile-and-summary-rep…

In 2013 there were 1,065,000 Owner Occupied households, so 37% of these said in the census they made mortgage payments. There are now 1,091,000 Owner Occupied households, so around 405,000 with a mortgage if you assume the same percentages. Investor lending is roughly 20% of total lending, 80% of $254 billion = $200 billion for FHB + Owner Occupied.

$200B divided by 405,000 = $493,000.

Also note, in 2013 there were an estimated 1,065,000 Owner Occupied households. March 2018 estimated 1,091.000. Increase of 2.5% in 5 years. Yet mortgage debt is increasing by 6.5% P.A (37% compounded over the 5 years?).

I was going to guess the average Mortgage would be $500K. This is exactly twice what I started off with, however interest rates are now HALF what I was repaying at 8.6% and I was doing it on a single crap income so whats the problem ? nothing has changed. Totally doable and a couple both on good money can smash it.

You forget that the repayment part is much larger:

- Monthly payment on $250k over 25 years at 8.6% = $2030

- Monthly payment on $500k over 25 years at 4.3% = $2723

So interest is the same but you need about $700/month more to repay the capital.

Correct, the serviceability costs have barely changed. Your deposit requirements would have been exactly half though, and your bank savings rates would have been almost double?

How long did it take you to save for your deposit? Double it, and then work out what that equates to in additional market rent every year.

Did you have a student loan taking 10% out of your pay?

And if we assume that an average mortgage is 20years, and factor in that those who purchased ten years ago a) purchased at 10 year ago prices, and have paid ~1/3rd of the mortgage down, it becomes very obvious that the risk is concentrated in those that purchased recently, and those that leveraged up to buy more property. So for every couple in their 40s or 50s that has a <$50k mortgage there is someone out there with a million dollar plus mortgage to bring that average back to $493k.

The tax loss on income had got out of hand and was seen as a way (correct or not) for the casual investor to feel they were gaming the tax department, especially after Cullens envy tax on income to .39 cents. That coupled with cheap money, and overseas speculation driving capital appreciation, made this the go to retirement saving option. This has rightly or wrongly created a distortion, and has not been unique to NZ.

At least this govt has done something to attempt to level the playing field, unlike the Nat's who refused to accept that this was even remotely an issue. Sad. Anyhow, will see it all play out over the next 24 months.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.