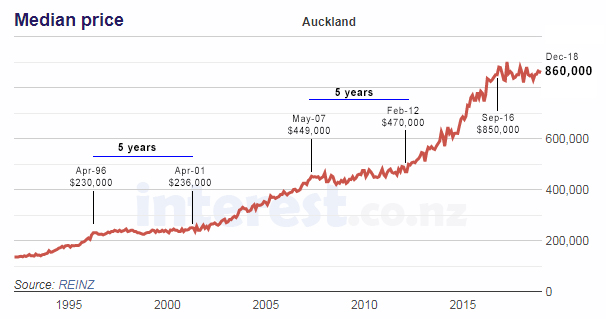

The Auckland housing markets are clearly in a funk.

House prices in the City of Sales are little changed at the end of 2018 from what they were in September 2016.

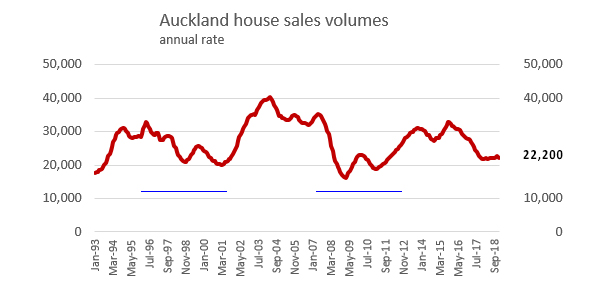

Sales volumes are unusually low.

And the commentary around the state of the market is no longer upbeat.

But we have had flat periods before. So what do earlier flat periods tell us? What does history suggest?

Firstly, these market pauses last a long time. The last two lasted five years.

And that suggests that we are not even halfway through this one. In fact, history suggests there may be another three years of low sales volumes and no price gains.

Secondly, previous flat periods have tended to coincide with economic recessions. But the current flat period has come when economic growth and overall prosperity has been very positive.

It is unusual for the New Zealand housing market to be in the doldrums in good economic times. There seems little doubt affordability limits have been reached.

Thirdly, it is unusual for the Queen City to have run out of wind when the rest of the country isn't suffering the same effects (Canterbury excepted).

The run up in price between 2001 and 2007 was 90% while the run up in price between 2012 and 2016 was 80%. It takes incomes a long time to catch up, and income gains in the past five years haven't been strong.

And fourthly, we are in a phase of more active public policy changes, which are mostly aimed at the Auckland housing market. The foreign buyer limits are just the latest, which included the LVR restrictions, Auckland's Unitary Plan rezoning to free up greenfield and brownfield development, the Special Housing Areas of the National Government (which are now starting to bear fruit), and the KiwiBuild and enhanced Housing NZ programs of the new Labour Government. All these are changing the supply/demand balance.

This additional supply perhaps suggests that the current period where it is hard to sell a house, and even harder to expect capital gains from housing, may last even longer than five years this time, perhaps extending out well into 2023 to 2025.

89 Comments

"But the current flat period has come when economic growth and overall prosperity has been very positive"

yes, but this growth has been based on ultra low interest, an abundance of credit and huge immigration. ie. unsustainable factors, not anything of substance.

"David Chaston says thanks to affordability limits being reached"

Correct and this affordability has been reached because foreign buyer has been removed out of the market otherwise for money laundering - their is no limit and as far as local average Kiwi were concerned, affordability limit has been reached long time ago.

Also the affect of new money laundering will know after few months.

Why is it hard to accept that Foreign buyer ban is having its affect ( Forign buyers were very active despite denial by national government and ifs supporters) anbd hopefully the money laundering act will add to the ban.

By march the result will be out.

Did anyone notice the significant price change in Queenstown?

Apparently asking prices have fallen 18.9%. Not sure if this is a function of higher priced properties being taken off the market, or sold and no new listings of higher priced properties.

https://www.newshub.co.nz/home/money/2018/12/prices-plummet-in-queensto…

Except they got the stats wrong on the immigration numbers. Read how they bungled it.

Think NZ not as a country, but a place where rich people from all over the world would like to have a house or two to stay or invest.

Why ?

Indeed, I've got no interest in living in a rich person's playground

Because we have too many politicians who seem willing to be bought by foreign interests?

And what aspiring imperial powers have not wanted to own land around the globe?

"Housing bust spreads across global markets"

https://www.macrobusiness.com.au/2019/01/housing-bust-spreads-across-gl…

Yes I cant think of anything better than the country of my birth being used as a late night ''booty call'' for those wanting to get their ill gotten gains out of their home nation..

Truly aspirational

Indeed. Fortunately that door is closing/closed to be strengthened with new anti laundering rules. If I wanted to live in overcrowded place I can simply move overseas where that is the case. Fortunately a majority of NZ voted for this to stop and the current Govt implemented it. National in denial and still claiming it was impossible to achieve..

What an absolute load of bollocks.

I understand what you're trying to say, but I think that's a very insensitive remark. How would you feel if someone tells you not to see your own country as a country, but only as a piece of land with houses on it? Every country has its own unique heritage and culture. For NZ, being traditional a farming & agricultural country, the heritage is in the wildlife, wild flora, natural landscape & slow pace of life that it wants to preserve. Unfortunately, most immigrants do not understand this and see NZ as just another big city with its people interested only in generating wealth.

I'd change

"... Unfortunately, most immigrants do not understand this and see NZ as just another big city with its people interested only in generating wealth... "

to

"Unfortunately, most immigrants and urban born NZers do not understand this and see NZ as just another big city with its people interested only in generating wealth. "

I'd change

"NZ as just another big city with its people interested only in generating wealth."

to

"Auckland as just another hick town with its people interested only in speculating wealth. "

Sod them, I say, houses are needed for people, here.

It is a fine point you make there PA.

Xingping

I wanted freehold property in China but the CCP don’t allow it

Chinese nationals often abuse the over generosity of countries like NZ

The CCP calculated they can increase their influence over a countries politics by allowing its nationals to buy properties & businesses in host countries

Seems to be working well

This seems like a good way to encourage a backlash of nationalist populism. Perhaps Kiwis will eventually tire of being a servant class for the world's rich.

would be interesting to compare the debt level in all the three 5-year plateau period

And where any considerable downward interest rate movements occurred along the tail end of those 5 year plateau periods.

Yes, as Sam Hunt once said "We're just a big country town" at the end of the day. One of the real issues we have is that we've stopped respecting our leaders. This seems to the case right across the western cultures. Some would say that's because they stopped respecting us/the people, and it would hard to argue against that, to be sure, however from my angle, we've stopped producing good leaders in our education systems and families which is today starting to hurt us. Struth, when you look at the current batch, both in power and in business, there's not much to look up too, is there? Or, is it the fact that the left have been undermining the hierarchical structures on which our culture was founded? Mmm. Like most things, it's usually a bit of both.

Absolutely, we've stopped respecting our leaders because they've treated us with disdain and contempt for decades. Unfortunately for our "leaders", the digital age has meant the carpet, under which their dirty deeds have traditionally been swept, is thinner and covers much less area. The public have never been smarter and politicians have failed to realise that we know what they say and do aren't anyways truthful and ethical. We have long memories.

At these "must go" low bargain prices Auckland will soon be inundated from those returning from the over priced regions...

Get in quick - these prices won't last long!

So which economists see this as the "soft landing " of which they speak so often

Never fear

JPMorgan’s Jamie Dimon says

https://www.usatoday.com/story/money/2019/01/15/government-shutdown-jam…

Do you believe him ?

All thanks to past national government for turning entire NZ- Auckland in particular to casino for the rich and foreign buyers - Heaven to park unofficial money (Money Laundering).

Now it is hard for anyone to deny that the boom is over, so will have to accept atleast that the market is slow (To maintain ones creditability) but still being careful with words to suggest will be flat (Avoiding the word FALL) but in reality when it is hard to sell - the price has to and will fall as their will be many who will have to sell for one reason or the other and will not be able to wait for few years SO…can argue the percentage of fall but not …...

Many who have bought in the last stage of the housing boom for a quick buck and are not able to hold for long will have to come out and book the lose (Can try to minimize the lose) but at this stage are hoping that may be now, the market will pick up and it is this hope that is preventing them from selling so IF the market does not pick up in first quarter of 2019 will be very bad news for many.

Softness = Falling Market

The Australian deniers liked to use the term "negative sideways movement" LOL

One can close one eyes to reality and deny but when it will hit (Unable to deny anymore) will hit harder so best to accept and act accordingly.

All thanks to Len Brown (Lab) and Phil Goff (Lab) at Auckland Council for making the city a land-banking paradise, speculators could buy any junk property sit on their backside for years and make gains. Unfortunately there has turned out to not be an endless supply of speculative investors (as if any other outcome was possible) and gains have stalled. Which is why Auckland is screwed up in relation to the rest of the country.

Affordability limits passed the mark many years ago. JK promised to resolve the housing "crisis" after the 02-07 boom that pushed people out of the market, particularly at 9% interest. Back then from memory it was 5-6 x income, now 9-10 x (off the top of my head). https://data.oecd.org/price/housing-prices.htm

NZ 2nd most unaffordable country vs incomes, Canada No 1 & Australia No 3. Both basket cases for similar reasons. What a mess, the implications have hardly started, flat house prices should be the least of our concerns.

I know "everyone does it" but it is just a nonsense to compare incomes to house prices. Virtually no-one buys a house with [saved] cash, certainly FHB's hardly ever do. The proper stress test is the proportion take-home-pay to make a mortgage payment (and more specifically the mortgage payment for a first home). That is the real measure of affordability.

The house-price-to-[gross]-income measure (median multiple) is just junk clickbait.

So what you are saying is that affordability is tied to the interest rate, as long as they stay low or get dropped to near zero then NZ houses are affordable to everyone. Lets hope the RBNZ hurries up and drops the rate to keep this ship afloat.

Correct,

As accounting 101 teaches, we need to compare income with expenses (and assets with liabilities), not income with liabilities. Unfortunately DTI is a measure which also proposes such ill comparisons ("D"ebt = Liability with "I"ncome)

That's neat if mortgages are lent with 0% deposits, but they're not. And incomes drive the ability of people in the market to come up with a deposit.

And the longer people need to save for a deposit the more dead money rent they end up paying (instead of contributing towards a mortgage) if they’re not fortunate enough to have parents to freeload off like we did.

You can't entirely discount the psychological factor of having to sign up for a debt that is 10 years of your gross income. (Yay for being jointly and severally liable!)

There is a simple way to reduce your liability here Pragmatist... Polygamy.

s/reduce/increase

What is nonsense is your refusal to understand the underlying issue that income to house prices highlights.

The ability to make a mortgage payment on the day you buy your home has no bearing on your ability to continue being able to make that payment over the life of the mortgage, and you become more vulnerable to the amount of any residue debt the greater your ratio to borrowing versus income is, ie income to house price.

And you know there is a direct correlation between house price medium income ratios and restriction zoning policies. IE more restrictive zoning higher house prices to incomes ratios.

High prices to income ratios are indicative of dysfunction council policies and they have been the red flag that has highlighted what we are starting to go through now with the topping out of housing affordability.

After all who wouldn't want a house a 3 to 4 x income rather than 6 to 9 x income? Other jurisdictions do.

"And you know there is a direct correlation between house price medium income ratios and restriction zoning policies. IE more restrictive zoning higher house prices to incomes ratios"

Can you justify/back up that statement ?

The real benifactor to David’s measure of “the proportion of take home pay to service a mortgage” is of course the banks. We are now paying back much greater sums over long periods, yes at lower interest rates however the interest paid over time is more than it was with lower price to income measures. So more of our production goes to the banks due to not addressing systemic failures in our banking and political systems. Not great in my opinion.

It’s fine if interest rates stay this low for the next 30 years. But what if they don’t? It’s great for the banks, max out their lending at record low interest rates then tweak the rates upwards.

Interest rates can’t rise in any significant way due to the price to income ratio. If affordability is maxed out now at current rates a rate hike would lead to a downturn which potentially is worse for the banks than anyone - hence the bailouts of banks around the world. Our banking system isn’t made to handle downturns and contractions, they are inherently reliant on growth with only a small buffer for downturns.

I can’t see how rates can rise in any serious way without a recession. My guess is rates will drop at the first sign of real trouble and we will then keep increasing the total value of mortgages with our enhanced “affordability” until we max that out too. Rinse and repeat until that no longer works and we have a real disaster.

So delaying the inevitable?

I always want to hear different points of view so if you’ve got one please let me know but in short, yes.

Should interest rates need to be raised, the government/Kiwibank could offer to take on 1 existing owner occupied mortgage per individual/couple that are deemed to enter undue hardship at, I dunno, let's say 5% p.a over 10 years. A bit like the State Advances Loans in the 50's. Issue bonds against them if they must.

Have it restricted to mortgages taken out in the last 2, 3, whatever years that they deem suitable. That way if the whole thing goes tits up, people might lose their investment properties but can potentially keep the family home.

Hmm, interesting. I’m not 100% sure it would work as if we got to that stage where that was necessary, higher interest rates would mean more money disappearing from the economy through debt repayments and there would be lower to negative debt growth due to decreased affordability and subsequently less new mortgages.

As another commentator points out often (either c.s or bw?), either we need increased private debt or increased public debt to keep our system going. This is why I dislike the monetary system we use so much as we are forced into ever increasing debt loads just to keep from going into recession which ironically makes a recession more likely.

I fully agree with you Whitay that interest rates can't rise significantly for fear of precipitating a recession, I have been saying that over the last 3 years, back when all and sundry were predicting interest rate to rise back to "normal levels"

What you say is true with regards to the USA, EU, China and Japan - big economic powerhouses. However the small unattached country of Iceland did not have the backstop of a multi-trillion plus economy to fall back on and so something else happened. When talking about New Zealand it pays to remember that we are a small unattached country.

Your right, Iceland did what no one else did. They let the banks fail, they actually jailed some bankers and bailed out there citizens instead. They went through some pain but two years later they returned to growth and are growing much faster than the other Nordic countries/most countries around the world.

I really hope NZ follows suit when we are forced to. I don’t know if we will however seeing how OBR legislation has been passed etc.

It will be interesting. Will Jacinda bail out the Aussie banks?

Gosh, I agree 100% again, and I stated before that it was wrong for governments to bail out large companies and banks with working people's money. Yes there would have been many lay-offs and a deep recession, but the world would be in a much better place now. Also it sends such a wrong message, now banks and all companies that are "too big to fail" know that Joe Bloggs will bail them out via the governments

Then why do overseas reserve banks impose debt to income ratios then? Obviously its an important determinant of judging how much a household can affordably borrow.

Banks don't impose DTI's, they compare a client's income with their expenses and their assets with their liabilities, which is exactly correct.

Your overly simplified view that currently serviceability is the only measure of "affordability" is bizarrely naïve and shortsighted.

You are ignoring the requirement to save for a deposit. As prices rise in relation to income, saving for a deposit gets harder and pushes more first home buyers into high LVR mortgages (increasing systemic risk).

With low rates, below historical averages, and high levels of debt it creates further systemic risk of rates rising in the future.

Both of these make House price to income relevant (but not the only factor) to the overall picture of affordability.

Our Housing Minister agrees, he is spending taxpayer $billions to subsidise house prices and keep the bubble going. The aim is support the prices at the bottom end of the market above $600,000, which will mean the average house price can remain high.

DC,

And I thought you talked sense.of course the multiple of price to income matters. If the multiple was much lower,say 5 times net income then the mortgage would remove a much smaller percentage of that income.

In a properly functioning market then even 5 times net income would be on the high side. Prices in Auckland are insane and I know that as my son and his wife paid $2m for perfectly ok bungalow in Meadowbank,which in no way reflects its real value.

""NZ 2nd most unaffordable country vs incomes, Canada No 1 & Australia No 3."" Am I right in thinking the 3 countries with the highest legal immigration per capita? Coincidence?

I understand what you're saying about a "prolonged housing market funk" but I think this time it's not going to be like that, the bubble is just too big and has gone on too long. It's similar in Australia (same loose lending banks and low interest rates for 10 years), and Sydney has just dropped 10% with the decline accelerating into 2019, dropping over 1% a month now. I'd like to think it's just going to be flat for a long period in a "soft landing" but I really don't think so this time...

Many central Auckland suburbs have taken a hit - if you purchased an average priced home in the double grammar zone 12 to 18 months ago and want to sell it today you will take a $100k to $200k hit or possibly more! The chinese buyers have disappeared.

and all the FHB were scared into buying a house with their Kiwisaver and mummy and daddys money from all the " if you don't buy now you never will" MSM fear mongering.

I know quite a few that are very nervous currently...

absolutely, although I'm renting in the eastern suburbs all the chatter on the streets and in the schools and on the sports field sidelines is that it's dropped away

Please do not use the C.. word or will be termed as racist (Though is a reality)

David might be right - flatness for years.

However, there's a few 'ifs, buts, maybes'

- what if there is a global financial crisis?

- does that send prices crashing, or....

- would the OCR be cut and cut, limiting the damage?

Overall I think prices probably WILL be flat for a few years, although I'm still sticking by my prediction of a 3-5% fall in Auckland this year - followed by flatness.

What would happen to your house prices if Kiwis ever quit reassuring each other that New Zealand is the best country on Earth?

it's a curious habit isn't it. Inferiority complex?

It's certainly a lovely country, but there's lots of other lovely countries too. As a country we've got lots of strengths but also lots of weaknesses. It's a matter of taste or priority what weight you put on those different things.

I think it is some sort of curiously misplaced nationalism. I agree, there are many other places that are at least the equal of here.

Some leadership with vision and a plan past the next 3 year election cycle could improve things here, greatly.

"What would happened ....." Nothing.

What would happen if foreign buyers were convinced that New Zealand is no longer the best country on Earth to stash their money outside the prying eyes of your home country? Now that might have an impact.

Imagine what a tax information sharing agreement with China would do?

You mean like the law National put in place 3 years ago to force foreign buyers to have a NZ bank account and a NZ IRD number?

If softness streches even for few months market will fall and if it lasts for years, do not see how it will not fall.

As interest rates are very low, resistance will be strong but fall it will be.

If house prices do continue to drop in Auckland it will have a huge effect on the economy going forward.

If this happens the Coalition government will not be campaigning for a capital gains tax as people will see that this COL can not run a country.

If the economy tanks then yes they are gone but they are gone anyway.

Kiiwibore gone!

Pike River entry gone!

Immigration reduction gone

Business under pressure. Gone

Winston. Under 5 per cent . Gone

You certainly have a warped view of what is happening in this country.

The housing (and debt) bubble has taken a lot longer to inflate than the past year. It was always going to burst. Yes, the current govt will get the blame because most voters really don't know what the real story is: years and years of loose lending and very low interest rates, and a housing bubble that was denied for years and actually encouraged. It was never going to go on forever. Bubbles NEVER end with a soft landing.

Is the Pike river re-entry not happening anymore? I must have missed it, thought it was all on towards the end of 2018?

There was something about it in the news the other day.. trying to flood the mine with gas again maybe? Hopefully they come to there senses and just build a bloody statue somewhere and let the bodies rest in peace before somebody else ends up dead.

Least this COL managed to do what National failed to and Ban Foreign Citizens from buying NZ Property. National did nothing to reduce Demand and simply spun stuff about Supply.

"Income to House prices" is a good general measure and should be used along side the "Take Home pay to Mortgage payments". Calling one clickbait is a little strange considering the other one ignores the need for a deposit and the debt taken on board.

No harm in quoting both measures, and you will probably find Auckland is high in both considering the interest rates in NZ.

A 25% fall in transaction volumes Dec 2018 compared to December 2017 would suggest the idea of a 'flat market' is unlikely. January and February will be very interesting indeed. is it time to bring out all the cheerleaders to keep the debt stacking going?

Where are Ecobird and Double GZ these days? We haven't had a 'foreign commentator' ban on interest have we?

I think they have both retired hurt. Not sure they will be able to continue this innings. Very sad.

If they retire now, they are exiting near peak market and will have made a killing. We should be happy for them.

Yes and the usual RE industry spruikers are noticeably subdued, they probably know a dip is happening

Affordability limits are irrelevant, David Chaston is a hopeless optimist. Auckland property has risen to exploit capital gains and now those capital gains have vanished. Without capital gains Auckland property is about 40-50% over priced. Maintaining flatness at this level will be very difficult in even good economic conditions.

Unaha-closp you are 100% correct - without capital gains Auckland property is over priced and need correction which will happen.

The housing market having a little breather for now. Renting is dead money, money in the bank earning very little after tax and Stock Markets are very volatile. With low rates will be around for a long time and cheaper money access, than quality properties will always seek good demand. Immigration running around net 60k p.a then they need somewhere to live. The market is a buying opportunity now the heat is out of it.

It'll be different to Sydney and Melbourne, right? Even though NZ always follows.

Please admit that the replacing of owner occupiers with rentiers is much of the problem that results in desperate buyers being prepared to pay too much (interest rates or not) and who will take far too many years out of their life to become mortgage free.

Also admit that there are too many landlords many of them having substantial capital and with a lack of communication skills to be involved in the workforce directly and that means they have no other way of earning an income other than as property investors.

Are you suggesting that The Man 2 epitomizes Landlords? I wonder how much of the "substantial" capital you're referring to is equity recycled with a bit of interest only juice?

I've heard that real property investors don't put any of their own money in. They leverage equity in an existing property to scrape together a deposit; borrow the rest on interest only; outbid First Home Buyers on entry level DIY properties then rent them back to the First Home Buyers as is. But it's okay because they're providing a Public Service so I've been told.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.