By David Chaston

There are reports that already more than 500,000 Kiwis are on the emergency government wage subsidy scheme. And the Ministry of Social Development (MSD) is facing a huge increase in unemployment claims.

At the end of December 2019 there were 112,000 people in the workforce without a job plus another 90,000 in part-time jobs looking for more work. 147,464 were on the JobSeeker benefit, or 4.9% of the labour force.

When the end of March labour force data is released on May 6, these levels will be very much higher and of course they will have probably grown again sharply in April too.

The main feature of the rise is that the newly unemployed were employed previously. They had jobs, and income, and probably consumer debt. And that may well be very different to the 2019 cohort without jobs and on benefits - those probably had little access to consumer debt.

So we are expecting a very sharp rise in consumer debt stress.

The Government has an agreement with banks on how mortgage debt stress should be handled. It is likely that homeowners will actively work to mitigate their mortgage debt issues.

But credit card and personal loan debt will be the first place we are likely to see real household debt stress. And it could explode as fast as job losses.

Making things worse will be Buy-Now, Pay-Later (BNPL) schemes. They have been allowed to mushroom without regulatory oversight so how much is at risk here is unknown.

But these BNPL schemes work via a credit card settlement system. So we will be closely watching credit card debt data. And personal loan debt levels.

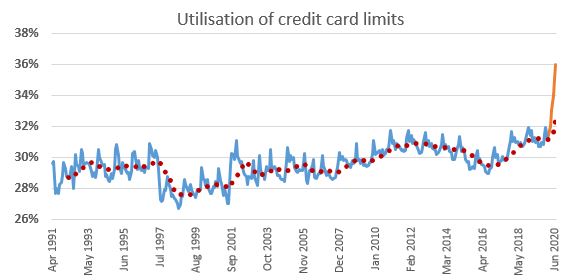

Banks have approved $23.4 bln in credit card limits covering $7.4 bln in actual credit card balances outstanding at the end of February. BNPL schemes fall due to credit cards on a two-weekly payment basis, either in four payments (like AfterPay) or ten payments (like Genoapay).

With sharply increased job and income losses, we expect to see card holders letting their credit card balances rise sharply, not only to settle BNPL debt but also just make household living purchases.

Even though we don't have any specific data yet, we would not be surprised if credit card balances alone ballooned by an extra +$1 bln by June 30. It could prove an under guess.

Source: RBNZ C12. The orange data are our projections.

Such a shift would be unprecedented. In the Global Financial Crisis the long run credit card utilisation rate (the red dots) rose from about 29% of the overall credit limits to 31%. Improving prosperity saw that gradually fall back to about 29% until the end of 2017 and then it has risen to a record level in the past two years. But that is likely to be completely eclipsed in the next few months as sudden, severe household budget stress bites very hard.

One of the ironies of the rise in BNPL was that "millennials didn't like debt and the interest that came with it". But these schemes suggested you could still get stuff on credit without having a financial interest rate penalty to pay. It has of course been too good to be true. These bills become due now as default payment systems will kick in. It will hurt.

And worse, having had BNPL debt will be a black mark on your credit history. Banks will not look kindly on a surge of these obligations appearing on their books. In fact, it will be very easy for them to identify these flows and their accumulation - and to insist that household budgets are changed to deal with unpaid obligations as a priority. Watch Trade Me sales activity as some people are forced to liquidate 'stuff' to resolve this unsecured personal debt surge.

Expect no help from the buy-now-pay-later schemes themselves as they will be fighting for their very survival as retail throughput dives. You can see more on the buy now pay later sector here.

54 Comments

What might be more telling is to ask what the number of applications for benefits are, they probably only have a very limited number of staff so looking at the queue length may be more telling.

Out of a job, but having to wait 3 weeks for Winz to process your application.

First 50 callers are mailed out a laptop, VOIP headset and an employment contract to deal with added demand?

A temporary UBI, although unfair, would solve this issue.

I'm inclined to agree but politically it seems taboo to extend welfare to taxpayers in a time of hardship.

Australia and USA have just done it... any ideas why it would be so taboo in NZ?

Sqishy - The wage subsidy and other Govt handouts may be welcome but I consider them Helicopter Money - Hong Kong did it first and openly by giving all HK$10,000. Most western countries have similar schemes.

There will be all sorts of other debt as well. Car loans spring to mind.

I doubt that the status associated with the new Audi SUV or the new Ford Ranger Ute will be of such importance over the next few years.

Good one Uninterested =)

I very painful time for narcissists no doubt LMFAO

Just read some stats about car loans in the US. ~90% of new cars are bought with borrowed money! On average, the buyer has $4000 deposit on a $40000 car. Let that sink in. People with $4k in their pockets buy $40k cars...

Subprime auto loans??

Of course some of those people could have afforded to buy the $40k car with cash, but why use cash when credit is so cheap? Better to put the extra $36k into the stock market instead. Oops, not 2019.

It's not always cheap. When I bought my Ranger in 2015, Ford offered 9% finance when the banks were offering 3%!! If they'd offered 1.5 or even 2% I might have taken them up on it.

US has always been about car payments in a way NZ never has. Although more folk in recent years here, I think, than in the past, have been using finance.

In the UK as well, they even have dated registration plates and a rediculous testing standard to try to try to encourage sales of new vehicles. Environmentally it always seemed a bit dubious to me, particularly "cash for clunkers" where many people where incentivised to scrap perfectly good cars.

Yes has surprised me the last 5 years or so to see how many young Mums are driving the kids around in a late model Range Rover (especially North Shore of Auckland?). I'm left thinking how the hell did they finance that? Then I remember we're probably in a property bubble.

Return of the White-Van Man.

Interesting Scenario - If it happens

Retirees realising 'they don't have enough', and start selling their assets to support their lifestyles?

Of course!

That's what savings are for.

The problem for many Western societies and Australasia in particular is that much of those saving is tied up in hard assets - property. And when they all realise that they need to sell ; all at once ( after this shock?) it could get nasty.

Exactly right bw, the same thing happened after CHC equakes, no cash-flow, it was all tied up in the house, and subsequent insurance battles. Hopefully some people learnt to keep some cash aside for the next rainy day (of course this will be more like 18 month thunderstorm)

I was working in banking during the 1987 crash and months later all these flash cars started to appear on the market

Of course the values dropped considerably

Also a lot of leased vehicles went on the market after they were returned to the lease companies

How many flash Mercedes Utes have you seen being driven by newly established tradesmen in the last year or so

It won’t be pretty

Late model low mileage ex-rental Corollas and Rav4s will be flooding the market soon too.

Motorcycles as well, it's like high end sports cars it's a heavily cyclical market.

I'm willing to make a donation but I see you have to have a credit card (or I presume, a debit card) to make a donation.

Dahhhh? I'm in a positon to make a donation because I DON'T POSSESS A CREDIT CARD !!!!!!!!

And I don't intend to change the habits of a life-time, and acquire one now.

So, Interest.co, if you email me your bank account number I will pay my donation by internet banking, thank you.

Incidentally, I note that a couple of close millennium relatives are phoning me up for the first time in years telling me tales of woe that really come back to their lack of savings. Unusual times!

Get a debit card. Life is too hard without one.

Beanie. I've never found it so. I do have an eftpos card. Obviously, the banks have sold you on the idea, nice marketing banks.

I wonder how humans have survived for 500,000 years without credit cards.

How does a credit card cure a tiny virus! Do you lick it or what?

My visa debit card is accepted anywhere a normal visa credit card is, so can be used for online purchases while still giving you the protection of being able to request a reversal if it all goes wrong.

The same card operates eftpos when you select that option. It costs $10 a year I think, and no more incurring interest when you forget the monthly payment because it never goes into debt.

Thanks for the street wisdom ;)

The popular dispute concerning so called Boomers overlooks the fact that credit cards didn’t become readily available until the mid 1980s. Up until then reliance was on HP, lay by etc. Those generations up until the age of say thirty had little opportunity to incur personal debt as it was simply not available until Rogernomics lifted the lid and the availability of credit simply got strapped to a rocket.The problem for the generations born say 1960 onwards is that they have been able to help themselves to credit and often the banks have overtly encouraged that. Many today look at what they have without any thought as to whether it was bought with money earned or money borrowed, they cannot distinguish the difference. Comes squeeze time and the stark reality of that comes home to roost.

What hits me is that the March figures will be released on May 6. This is an out of date 20th Century govt in a new millennium. We should have March 2020 numbers by April 6 not May 6. We have the technology. Do we have the right people? In fact, I'd go further & say that all govt data should be available within 5 working days of the the stats period ending. This is now what we expect Jacinda.

PS: Watching OneNEWS (One Views) the other night show Norwegian & American unemployment stats for the week ending Friday 27 March a day after that period concluded. No sign of any NZ data available. Good cover TVNZ? Not. Poor governance covered by poor media.

Most competent businesses at the more organised end of town (that does exclude a Lot of SME's....) manage to close their books within 3-5 working days of month-end. To be sure, there might be some accruals which are essentially educated guesses in those numbers. But mostly hard and timely data is much preferable to having exquisite data months down the track.

Gubmints are notoriously clueless about such things, and the reason is very simple: their Departments, staff and reputations don't ride on having decent, timely data. The old saw is 'Good enough for Gubmint work'.....

You have heard of the large number of Wellington government workers, all working from home. But working from home with No Laptops.

It's a joke amongst the our Wellington betters that gets a laugh.

More so than the Health Minister, that just gets a shrug from same....

A couple in our immediate family have senior govt jobs. Their living room is set up with two desks (one borrowed from me) upon which are multiple VDUs patched into their respective departmental systems. It looks like a mini dealer trading room. Phone and video conferencing meetings often start quite early and sometimes extend into the evening. They seem to be flat out and declare themselves to be operating more efficiently than under BAU, especially without the regular red eye flights.

I work in IT and working twice as efficiently from home than I do at work

Consumer debt crisis imminent..

Another thing that is imminent :

https://www.ccn.com/a-1-3-trillion-u-s-housing-market-crash-is-imminent…

This scenario of skyrocketing utilisation of credit limits will be great news to the banks.

Looking forward to this.

I'm after a late model mountain bike, the sort that retail for $10k previously. Way above my level of riding but oh so nice and should start appearing on TM soon.

redcoats. How about also a snazzy SUV to hang the bike on the back of. The soon to flood the market tsunami of late model rentals will provide good buying opportunities.

Car and RV Rental company liquidations. Now there’s a true tsunami of worthless assets to flood the market.

Quite fancy an RV now that can't travel internationally.

Nah it's ok. I'm of simply wants, just a mountain bike for me , fits well in my 29 year old bighorn.

Bighorn.

Never was there a more self-aware naming of a truck.

Cool truck though, in fairness. I'd like one.

Great time to upgrade my vehicle fleet....I want a helicopter!

Had an interesting conversation with a coworker a couple of weeks ago. She asked me what would happen in a financial crisis. I mentioned that if a bank goes down, people might lose their savings. She said "lol it's a good thing I don't have any savings"...

Then I said that many people will lose their jobs, mostly real estate agents and car dealers. She asked why, I told her nobody wants to / can buy a new car in a recession. Then she said that's awesome, cars will be cheaper then and she was looking to buy a new car anyway, because she wants a jet ski and her current car isn't big enough to tow it.

Basically living paycheck to paycheck, zero savings and she's looking to buy a jet ski and a new car...... And she's actually not a dummy! Just financially illiterate.

No, thats a dummy!!

I remember living in the Goldfields in WA Australia when mining took a hit and their were a lot of redundancies ,quite shocked to see couples who were earning between 10 to 17 a month have to sell all these toys to pay for a relocation costs,i thought some of these well educated people had it together..

Average rents were 600-1000 a week ,they just blew their money on holidays ,junk,booze and partying,i spoke to my accountant who said that their were clients who earn a 160,000 a year and had no assets or savings, i think we need to let the dust settle a bit ;but,ive got a gut feeling it wont be pretty ,we will soon see within 6 months whether those that appeared wealthy post corona virus were financially stable.

Recently i had a conversation with a mate in Adelaide ,he has an associate who was just brought out of retirement to help businesses in trouble ,he spoke to a lot of these people and said lets look at your expenses ,ok lets trade the BMW for a corolla etc ,most told him to piss off.

I say 6 months coz a lot of people will do anything in their power to maintain the status-quo.

I'm guessing there's going to be a big transfer of wealth from creditor to debtor in the P2P space. Nobody has mentioned those looming defaults yet.

Wait until Moodys down grade us then Sparks will fly

Also credit cards are great I have never paid interest in my life and never will.

In fact I have over a $1000-00 of free petrol and a bottle of Jack Daniels IN LAST 12 MONTHS from credit card -take note Streetwise

Not to mention the number of tradesmen who have bought Ford Rangers and the suitable boat to go with it , all on the drip .

The boat will be the first to be listed on Trade me

exactly right, contractors and sub-contractors are just about to bear the brunt, and all the financed utes and boats will be first to flood the market. then as house prices start to slide the decision has to be made as to whether to exit and protect your deposit or let it evaporate. huge housing crash on the way!

Oh but the latest was the delve into airbnb. Buy the house by the sea or lake as they werent a million bucks anymore after the gfc. Airbnb it. Taupo rife with this. First back into the rental market will be ok. Those that miss that boat. Not so much.

Great stuff have not owned a boat for a while. Too Expensive. Could now be more affordable

If there is a repeat of a large bank failure like 2008 (there probably should be) then this has just really started. If not and the print-a-thon continues we just bail out and reward the stupidly in debt, but save our Banking overlords.

Go long. Or go short, now is the time to role the dice...

Those perky RE agents who rushed in to sign up new leases on that Maserati and Porsche Macan must be laughing with tears now...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.