Content sourced from the World Gold Council

Investors have embraced gold in 2020 as a key portfolio hedging strategy. Looking ahead, expectations for a faster recovery (V-shaped) from COVID-19 are shifting towards slower recovery (U-shaped), or potential setbacks from additional waves of infections (W-shaped). Regardless of the recovery type, the pandemic will likely have a lasting effect on asset allocation. It will also continue to reinforce the role of gold as a strategic asset.

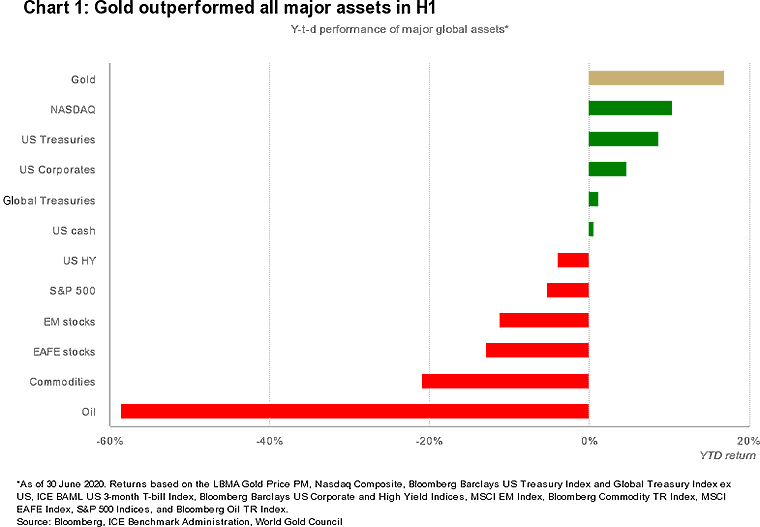

Gold had a remarkable performance in the first half of 2020, increasing by 16.8% in US-dollar terms and significantly outperforming all other major asset classes. By the end of June, the LBMA Gold Price PM was trading close to US$1,770/oz, a level not seen since 2012, and gold prices were reaching record or near-record highs in all other major currencies.

Though equity markets around the world rebounded sharply from their Q1 lows, the high level of uncertainty surrounding the COVID-19 pandemic and the ultra-low interest rate environment supported strong flight-to-quality flows. Like money market and high-quality bond funds, gold benefited from investors’ need to reduce risk, with the recognition of gold as a hedge further underscored by the record inflows seen in gold-backed ETFs.

Economic recovery may come in various shapes

The COVID-19 pandemic is having a devastating effect on the global economy. The IMF is currently projecting a 4.9% contraction in global growth in 2020, with high levels of unemployment and wealth destruction.

There is a growing consensus that a swift V-shaped recovery is morphing into a slower U-shape recovery or, more likely, the possibility that a recovery in H2 is short lived as recurring waves of infections set the global economy back, resulting in W-shaped recovery.

For investors, this is not only keeping uncertainty levels high, but may also have a long-lasting impact on their portfolio performance. Against this backdrop, we believe that gold can be a valuable asset: it can help investors diversify risks and may positively contribute to improving risk-adjusted returns.

Table 1: The gold price is near or above record high across key currencies

Gold price and y-t-d return in key currencies*

|

|

Y-t-d return | Current price | Record high† | Date† | |

| USD | (oz) | 0.167 | 1768 | 1895 | May 9, 2011 |

| EUR | (oz) | 0.167 | 1574 | 1604 | May 15, 2020 |

| JPY | (g) | 0.159 | 6133 | 6538 | Jan 21, 1980 |

| GBP | (oz) | 0.251 | 1431 | 1444 | June 29, 2020 |

| CAD | (oz) | 0.226 | 2408 | 2443 | April 16, 2020 |

| CHF | (oz) | 0.142 | 1675 | 1688 | May 19, 2020 |

| INR | (10g) | 0.235 | 42921 | 43069 | June 22, 2020 |

| RMB | (g) | 0.185 | 402 | 403 | June 29, 2020 |

| TRY | (oz) | 0.345 | 12120 | 12178 | May 7, 2020 |

| RUB | (g) | 0.339 | 4051 | 4184 | April 22, 2020 |

| ZAR | (g) | 0.45 | 988 | 1060 | April 23, 2020 |

| AUD | (oz) | 0.192 | 2568 | 2741 | April 16, 2020 |

*As of 30 June 2020. Based on the LBMA Gold Price PM in local currencies: US dollar (USD), euro (EUR), Japanese yen (JPY), Pound sterling (GBP), Canadian dollar (CAD), Swiss franc (CHF), Indian rupee (INR), Chinese yuan (RMB), Turkish lira (TRY), Russian ruble (RUB), South African rand (ZAR), and Australian dollar (AUD).

†Prices and dates in bold correspond to record highs occurring during H1 2020.

Source: Bloomberg, ICE Benchmark Administration, World Gold Council

COVID-19 is upending asset allocation

In response to the pandemic, central banks around the world have aggressively cut rates and/or expanded asset purchasing programmes to stabilise and stimulate their economies. However, these actions are leading to several unintended consequences on asset performance:

In addition, widespread fiscal stimuli and ballooning government debt levels are raising concerns about a long-term run up of inflation, or significant erosion of the value of fiat currencies. Deflation, however, is seen as the more likely risk in the near term.

As these dynamics heighten risk and lead to the possibility of ever lower returns than expected, we believe that gold can play an increasingly relevant role in investor portfolios.

Equities are getting (very) expensive and could see sharp pullbacks

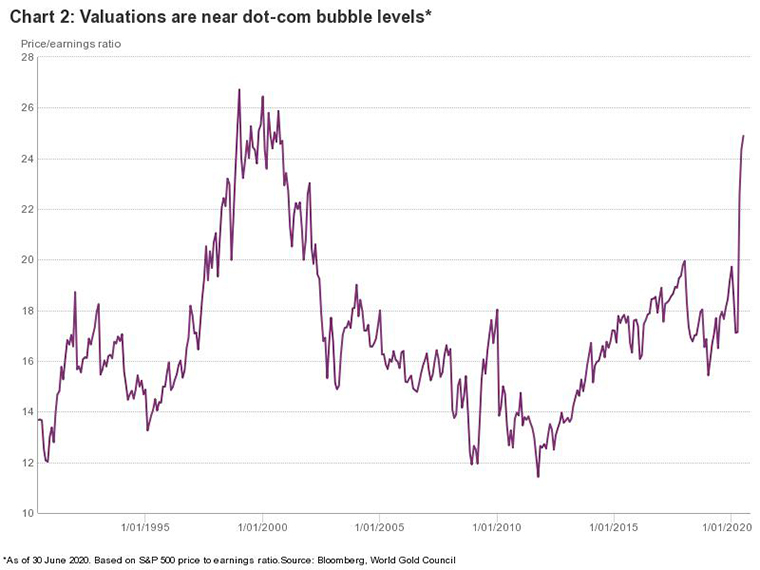

Global equities were on a virtually uninterrupted one-way trend for more than a decade. The COVID-19 pandemic changed that, resulting in a significant pullback, with all major equity indices dropping by more than 30% during the first quarter. However, equities have recovered sharply since – especially tech stocks. But stock prices do not appear fully supported by company fundamentals or the overall state of the economy.

This has often been referred to as the Wall Street vs. Main Street divide. In the US, for example, price-to-earnings ratios have jumped to levels not seen since the dot-com bubble in the span of a few months.

Valuations are near dot-com bubble levels*

And while many investors are looking to take advantage of the positive price trend, there is growing concern that such frothy valuations may result in a significant pullback, especially if the economy experiences a setback from a second wave of infections. Gold’s effectiveness as a hedge may help mitigate risks associated with equity volatility.

Bonds may offer only limited protection

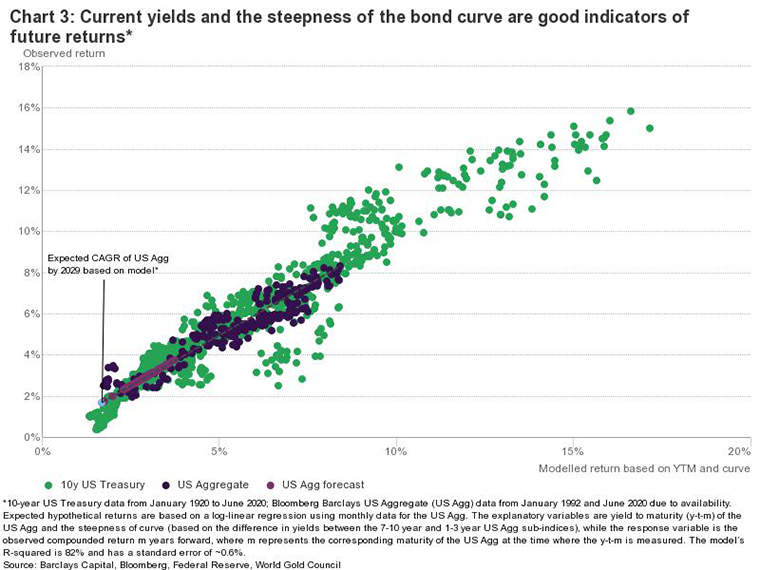

The low rate environment has also pushed investors to increase the level of risk in their portfolios via buying longer-term bonds, lower-quality bonds, or simply replacing bonds with even riskier assets, such as stocks or alternative investments.

Going forward, we do not believe investors will achieve the same bond returns they have seen over the past few decades. Our analysis suggests that investors may see an average compounded annual return of less than 2% (±1%) in US bonds over the next decade.

This could prove particularly challenging for pension funds, as many are still required to deliver annual returns between 7% and 9%. Lower rates increase pressure on the ability to match their liabilities and limit the effectiveness of bonds in reducing risk.

In this context, investors may consider gold as a viable substitute for part of their bond exposure.

Chart 3: Current yields and the steepness of the bond curve are good indicators of future returns*

Stagflation, disinflation, deflation?

While it is fairly evident that lower interest rates and asset purchasing programs are impacting asset price valuations, it is less clear what effect expansionary monetary and fiscal policies will have on inflation. Some believe that quantitative easing and increasing debt levels are inherently inflationary and that, sooner or later, consumer prices will spiral out of control even if economic growth remains subdued (ie, stagflation). Others, however, point out that previous – albeit not as aggressive – quantitative easing measures have not resulted in rampant inflation (at least not yet).

An additional camp points to the Japanese experience and predicts that deflation may happen first. In fact, there are some indications that this is starting to happen already. For example, while the price of necessities spiked during the lockdown in China, consumer price inflation has fallen from 5.2% in February to 2.5% in June. And some economists predict outright deflation by the end of the year.

Gold has historically protected investors against extreme inflation. In years when inflation was higher than 3% gold’s price increased 15% on average. Notably too, research by Oxford Economics shows that gold should do well in periods of deflation. Such periods are characterised by low interest rates and high financial stress, all of which tend to foster demand for gold.

Gold investment will likely offset weak consumption

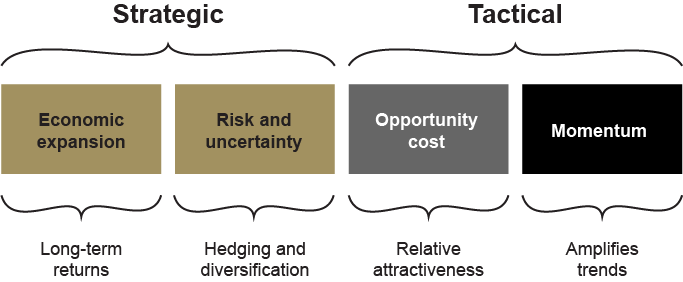

Gold’s behaviour can be explained by four broad sets of drivers:

In the current global economic environment, three of the four drivers are supportive of investment demand for gold, namely:

Conversely, an economic contraction will likely result in lower demand for gold in the form of jewellery, technology or long-term savings. This is particularly evident in key gold markets such as China or India.

Historically, investment demand during periods of financial stress has offset weakness in consumer demand and we believe that 2020 will be no exception. However, gold’s future performance may depend on the speed and shape of the recovery

This article is a re-post from here.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Great to see an article on gold. Good on ya interest.co !

As The Lark said, great to see Gold in the (relatively) main stream media :)

Although with the large spreads on physical gold, as well as the storage hassle and me being younger, I think I will stick to Bitcoin. Being able to take it anywhere in world with me and having the time to ride out the volatility (which is asymmetrically to the upside) is a better R:R than gold for me. Not to mention the ease of exchange.

0.5% spread too much for you?

https://www.perthmint.com/metalprices.aspx

BTC ease of exchange.

LOL.

BTC is relatively easy to exchange. Depends what platform you're exchanging on.

To eliminate counterparty risk you need to have physical possession. Morris and Watson in Auckland are currently trading spot +/- 2% for 1 kg amounts. https://morrisandwatson.com/live-price-lists/?currency=nzd I like the idea of the Perth mint and their gold token cryptocurrency but if you cant pick it up then it's just paper wealth. I dont know why anyone's mentioning BTC here, you might as well talk about seashells.

PMGOLD and tokens are fully redeemable for physical. https://www.perthmint.com/storage/perth-mint-gold-asx.html

Seashells were previously used as currency. As for BTC, its properties have a lot in common with gold. If you don't trust it, fine.

pmgold isn't redeemable in New Zealand right? I'm sure it's better than an ETF but your gold is effectively stranded in Australia. You cant take large amounts of gold through the airport either. Regarding bitcoin, it's got more in common with fiat currency that with gold. Bitcoin's backed by faith and faith alone. Bitcoin has zero intrinsic value. It's a certainty that BTC will go the way of seashells ie zero value.

Bit more that that if i want to hold it myself. shipping alone is pretty expensive.

Hell yea, I can buy it and have it in my custody in less than 10-15 min, and sell it just as fast.

Although with the large spreads on physical gold, as well as the storage hassle and me being younger, I think I will stick to Bitcoin. Being able to take it anywhere in world with me and having the time to ride out the volatility (which is asymmetrically to the upside) is a better R:R than gold for me. Not to mention the ease of exchange.

No reason not to hold both. Mike Novogratz has recently suggested investors hold both. I prefer to hold more gold than Bitcoin.

Why not both? In my experience BTC and physical gold are both very straightforward to exchange in NZ. Both are a good inflation hedge, especially if you can't reach the property ladder.

Silver has far more upside potential than gold....its severely underpriced relative to gold.

Samsung have just developed a prototype solid state silver-carbon anode battery with a far higher energy density than the current state of the art lithium ion. https://www.youtube.com/watch?v=TAFk-CebHWA

You can hold all 4. BTC, physical gold, silver and crypto gold. The crypto gold can take a bit of research, PAXG stores at brinks, really easy exchange. DGX is held in Singapore, there is also Kinesis, UK, and Aurus, also UK.

I also agree with comments regards silver, the most undervalued asset of all assets. Today everyone can see that all markets are manipulated, yet the precious metals market is one of the most highly manipulated. The good news is, the manipulators, being the comex in New York, and the lbma in london, are under massive pressure, and have been all year.

The Comex has been forced to deliver record amounts of physical gold and silver, and this is making the metals market look extremely interesting at the moment. I can thoroughly recommend these are worth looking into, GATA, (gold anti trust), have loads of info, and some great links.

GATA is relevant but they go far down the rabbit hole that it looks like conspiracism to most. It's not.

Eventually the manipulators will run out of physical gold, or a change in inflation expectations leads to price surges that even governments cannot control. There is an endgame. Understanding the manipulation, particularly the short selling, is necessary if you want to understand the gold price.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.