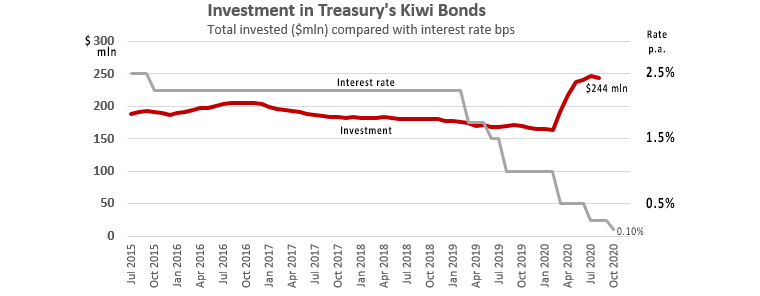

The interest rate offered by Treasury for their Kiwi Bond product has been cut sharply today (Monday). This is the third cut so far this year, effectively reducing the rates for these bonds by -80% or more in that period.

The perspective of today's change compared with rates that did apply over the last year, are:

| Maturity | 19-Jun-19 | 16-Aug-19 | 23-Mar-20 | 13-July-20 | change | New Rate |

| Term | p.a. | p.a. | p.a. | p.a. | p.a. | |

| 6 months | 1.50% | 1.00% | 0.50% | 0.25% | ( 0.15% ) | 0.10% |

| 12 months | 1.50% | 1.00% | 0.50% | 0.25% | ( 0.15% ) | 0.10% |

| 2 years | 1.50% | 1.00% | 0.75% | 0.50% | ( 0.30% ) | 0.20% |

| 4 years | 1.50% | 1.00% | 0.75% | 0.50% | ( 0.30% ) | 0.20% |

For retail investors, the rates for Kiwi Bonds are an effective risk-free return benchmark.

And they give an indication of where term deposit rate offers by banks may go when the Government rolls out its promised Deposit Guarantee.

These offers are also well below the current rate of inflation.

But they are higher than what wholesale investors bid in Treasury tenders for bonds of an equivalent duration. But as there is no effective secondary market, there is no easy way to sell these bonds and take the capital gain as yields fall. Holding them to maturity or "redeeming" early are the only options.

Kiwi Bonds are the main product available to individual investors from the Government. Kiwi Bonds are offered directly to the New Zealand public, but anyone who is not a New Zealand resident, even if they hold New Zealand citizenship, cannot invest in Kiwi Bonds. The definition of a New Zealand resident is that used by the IRD.

Kiwi Bonds are a simple form of investment, similar to a term deposit in that they offer a fixed rate of interest for a given term. Kiwi Bonds are denominated in New Zealand dollars with a fixed interest rate paid quarterly in arrears.

The minimum amount that can be invested is $1,000 with a maximum of $500,000 in any one issue. The maximum limit is probably there to discourage wholesale investors loading up on this retail offer because it pays more than the tender market.

The interest rates offered are generally lower than those offered by banks, reflecting the greater level of security associated with a government investment.

If you are a New Zealand resident and would like to know more about Kiwi Bonds, further information is available in the Product Disclosure Statement and the current application form.

And Treasury no longer uses Kiwi Bonds agents to facilitate the issuance of Kiwi Bonds. That means it has cut out banks, NZX brokers, chartered accountants, solicitors, investment advisers or investment brokers being able to offer them. You can only invest directly now.

This is the official announcement from the Debt Management Office of Treasury.

The Treasury today announced changes to the interest rates available on Kiwi Bonds, effective from 12 October 2020. The interest rates for the six-month and 12-month Kiwi Bonds have decreased from 0.25% to 0.10%. The interest rates for two-year and four-year Kiwi Bonds have decreased from 0.50% to 0.20%.

Kiwi Bond interest rates are set periodically from moving averages of domestic wholesale interest rates. The new Kiwi Bond interest rates have been set to better align to those available in wholesale markets.

The Kiwi Bonds rates are as follows:

For subscriptions of $1,000 - $500,000

Maturity Rate 6 months 0.10 percent per annum 12 months 0.10 percent per annum 2 years 0.20 percent per annum 4 years 0.20 percent per annum The Treasury also announces the cessation of Kiwi Bonds agents in facilitating the issuance of Kiwi Bonds. If you are an individual investor and would like to invest in Kiwi Bonds, please contact Computershare Investor Services Limited, New Zealand Debt Management's registrar for Kiwi Bonds.

10 Comments

What a messed up environment we've created for ourselves. These are now negative real return.

Interest - how often in their history have Kiwibonds provided a negative real return? (honest question as I don't know..)

In 2018 they were paying 2.25%. So that would have been about what inflation was back then. Prior to that, Kiwibonds would have paid out more than inflation.

Yes just wondering if there has ever been a point when you lost money in real terms by buying government bonds in this country?

Have had a lot of people recently asking about where to invest their money in this low interest rate environment and many are completely outraged (mostly boomers) when you explain the difference between nominal and real returns. They go from being disappointed by the low interest rates offered by bank TDs and kiwibonds, to being completely pissed off! 'Well at least I'll get some return on my money', 'yes but the purchasing power of your savings is reducing by buying that bond'.

"to infinitesmal and beyond' is the new catchcry for RBNZ.tough if you are in the 40% that cant afford to buy a house now.

DP

"..a maximum of $500,000 in any one issue. The maximum limit is probably there to discourage wholesale investors loading up on this retail offer because it pays more than the tender market."

I've told this story before; because it was done years back, re the answer.

"ANZ" lends all 20,000 of their staff $500k each to be exclusively applied to the purchase of KiwiBonds The funding comes from their Interbank Desk; the collateral is the Bonds, and the difference in %rates is shared between the staff member and the Desk. Easy way to pay the bonus' this year!

Pure fantasy. Besides ANZ has nowhere near 20,000 staff in New Zealand. More like 9000 I think. But you are right - it is just a made-up story, no basis behind it.

You can also have the interest compounded quarterly.

But..... at 0.2% it's now pretty much academic. Which also applies to what tax rate you tell them that you are on.

Well I hope the reserve bank has ordered plenty of banknotes because I think a fair proportion of maturing bonds may go under the mattress. And a fair proportion of that into the black economy eventually. A ten percent discount for cash is effectively a ten percent instant return.

March on, next experiment is on the table Q1 - 2021 let's move the OCR to -5.00 basis points. Then FLP 2.0 then 450billions further QE. Let's do this, let's keep on moving - By most of MMT economist guidelines, The higher we can push the RE valuation that matches real pricing, then the sooner we can feel the economic wealth trickle effect taking place - Guaranteed. For this we must ensure the ideal DTI must be achieved first at the ratio of 1:24 (of combine couple incomes), this is the magic numbers for most of NZ average income earners.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.