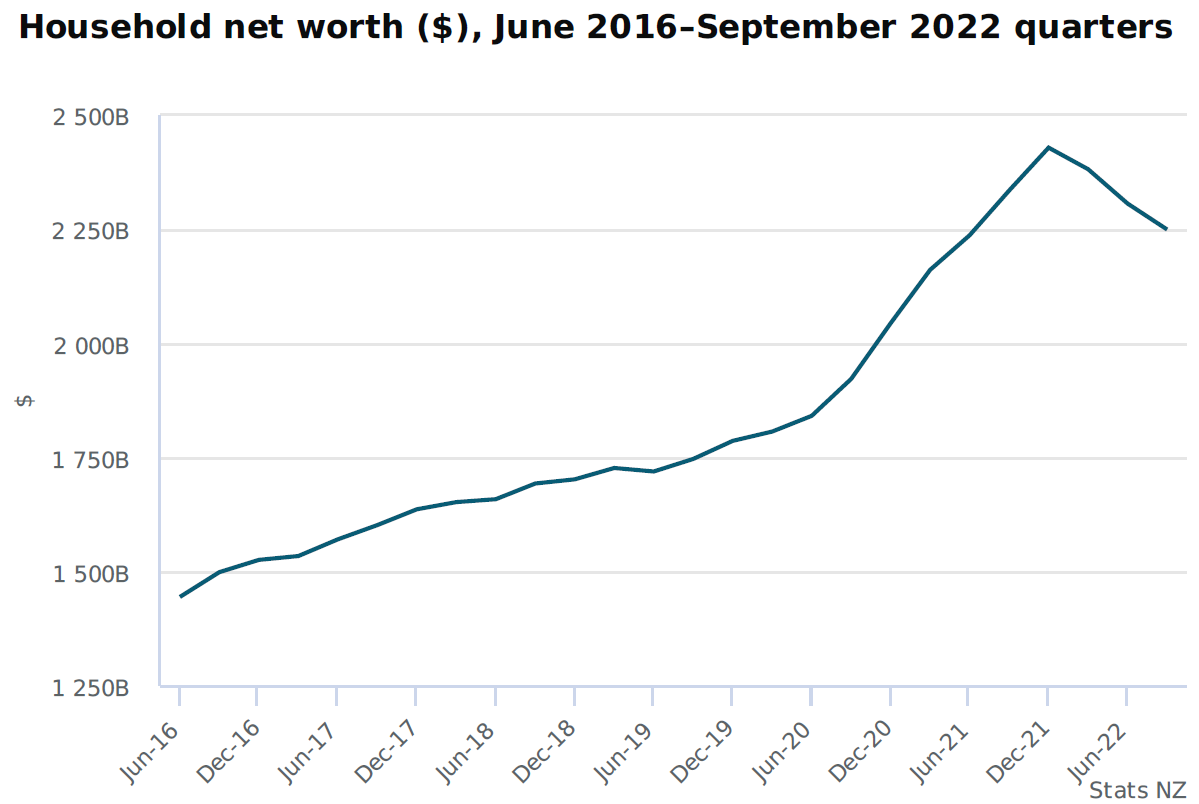

The household net worth of kiwis dropped by some $179.4 billion in the first nine months of 2022, according to new data from Stats NZ.

The fall represented a decline of 7.4% and was driven principally by a $91.1 billion drop in owner-occupied properties and by a $78.6 billion fall in financial assets, including shares and investment funds.

These changes mean that household net worth at September 2022 of $2,250 billion is now just above the value recorded at June 2021, of $2,237 billion.

To give some needed perspective as well, Between the end of 2019 and the end of 2021 household net worth shot up by over $640 billion.

Net worth is the value of all assets owned by households less the value of all their liabilities.

In terms of the September quarter, the latest available, household net worth fell $56.8 billion, or 2.5%, following similar falls in the March and June 2022 quarters.

The fall in the September quarter was also mainly driven by the decrease in residential property valuations, particularly land. The fall in household owner occupied property assets accounted for $41.6 billion (73.2%) of the fall in net worth since the June quarter.

Stats NZ said the falling property values were also the main cause of the $12.7 billion, (1%) fall in household’s financial assets. Rental property owned by households is recorded within equity assets (property valuation less any mortgage held) as a financial asset.

Partly offsetting this fall in equity assets was a continuation of the rise in currency and deposits held by households, up $2.6 billion (1.1%). In addition, households’ insurance and pension assets saw a small increase following decreases in the previous two quarters.

Household loan liabilities continue to increase, up $2.5 billion (0.9%) this quarter. The rate of increase in household debt has been slowing since the December 2021 quarter. Loan liabilities are composed of household mortgages, and consumer and student loans.

Separately Stats NZ said household saving increased 31.1% to $2.2 billion in the September 2022 quarter, Stats NZ said today.

Household saving shows how much households are saving out of their current disposable income. That is, current disposable income less current spending.

One interesting thing to note is that the figures are starting to reflect the higher mortgage rates now applying. The amount paid in interest in the September quarter topped $3.6 billion, which was the highest amount since the early months of 2009. And yet, the quarterly amount of money taken relative to disposable income remained very low at just 6%. In 2009 the last time the amounts of interest paid were this high the amount of disposable income taken was 14%.

Stats NZ's national accounts institutional sector insights senior manager Paul Pascoe said that increases in incomes have meant that household saving increased during the September quarter, despite price rises and higher interest rates contributing to higher household spending,"

Household net disposable income is the amount of money a household has once all income such as wages, interest, and child support, and outgoings such as taxes have been accounted for. It represents the money available for a household to spend, save, or invest.

Household net disposable income increased by 2.5% to $55.9 billion. Salaries and wages (up 2.3%) and interest received (up 34.1%) were the main drivers of the increase in household disposable income. This increase was partly offset by a 6.1% decrease in the income of self-employed business owners and partnerships (entrepreneurial income).

Household spending was up $825 million (1.6%) in the September 2022 quarter. This followed a 2.1% fall in the June quarter. Spending was up across the board, with increased spending on durables (such as clothing and footwear), non-durables (such as food and drinks) and services (such as housing, power, and gas).

19 Comments

I would love to see a graph with average net interest expense for mortage lending next to the OCR. I think we would see interest expense ramping up very soon as majority of fixed rates roll off. A lot of pain to come for greedy speculators :)

Generous speculators, now. Thank you, whoever you are, for holding the bags.

What about owner occupiers? Do their interest rates not rise the same as "speculators" ?

There are only two classes of people in NZ: Investors or aspiring FHBs. If you fall outside of those then you are persona non grata for housing discourse, the up or down is only ever analysed and couched from those perspectives. As soon as a New Zealander buys a house, they functionally cease to exist.

As NZ runs current account deficits and banks can only create money as credit then this only leaves government budget deficits as a source of financial assets for us to increase our savings. This is displayed in the sectoral balance accounting identity (S-I) = (G-T) + (X-M).

Any politician who campaigns to reduce government debt is therefore also campaigning to reduce our household savings,which is all that the governments debt represents.

False equivalence tho, innit. A government can run up a heap of debt and have nothing to show for it, it can spend the same amount of money on productive infrastructure that makes everyone better off over time by unlocking productivity gains that we don't currently have. I'd argue the quality of the spend matters more in the longer run than the amount of overall debt, which is something that our current government seems to refuse to want to accept might even be plausible.

Looking at the relationship between h'hold net worth and sales of a representative basket of nice-to-have FMCG / F&B products would be telling. Considering that the growth rate of the former has been on an upward trajectory because of the property ponzi, the positive correlation should be strong with a have a strong coefficient (association). I'm sure that sales of those nice-to-haves would be an interesting indicator of what's happening in terms of the wealth effect.

The household net worth of kiwis dropped by some $179.4 billion in the first nine months of 2022, according to new data from Stats NZ. The fall represented a decline of 7.4% and was driven principally by a $91.1 billion drop in owner-occupied properties and by a $78.6 billion fall in financial assets, including shares and investment funds.

Market capitalization isn’t “wealth.” It’s the latest price, times shares outstanding. Blotches of ink on paper. Flashing pixels on a screen. If a dentist in Poughkeepsie buys a single share of Apple at a price that’s 10 cents higher than the previous trade, $1.6 billion in market capitalization emerges from thin air. If a single share trades 10 cents lower, $1.6 billion evaporates just as quickly. Whatever happens, every security in existence has to be held by someone until it is retired. Ultimately, the wealth inherent in a security is the future stream of cash flows it will deliver to its holder(s) over time. Price fluctuations don’t change those underlying cash flows. They just provide opportunities for the transfer of savings between investors. High valuations favor the sellers. Low valuations favor the buyers. Investors have never paid higher prices for those future cash flows, or accepted prospective returns so low.

Put simply, the bubble hasn’t changed the wealth, and a collapse won’t change the wealth. What will change is the market cap. I suspect that the erasure of market cap in the coming years, and possibly the coming quarters, may be brutal. Still, no forecasts are required, and our own attention will remain on observable valuations, market internals, and other factors. Meanwhile, even if an investor sells at these extremes, the only thing that will change is who holds the bag. Link

Great Article 👍

Should we really call it a fall? So fall based on one year time frame.

What about we forget the two years of covid and stupid interest rates because of politics and policies of ignorance.

Is there still a fall? +(discounting last two years) and do we seriously believe that the gain was going to last? Who is that naive? Probably only a flightless bird who comes out in the night. No wonder they are on extinct list.

food prices rise because cost rise.

costs like fuel, power, taxes, water, rates, chemicals, WAGES...

ALL THINGS OUR WONDERFULL LEADER, THR MIN OF FINACE, MAYOR'S, AND GOVT CONTROLLED MONOPOLIES HAVE CONTROL OVER.

SO WHO IS TO BLAME?...

OUR KIND LEADER?

OR FISCALLY ASTUTE FINANCE MINISTER

THE guru RB GOVERNOR

THE awesome MAYOR'S

THE generous and benevolent CEO'S OF AIRNZ, POWER COMPANIES....

They have no control over the price of international commodities such as oil, fertiliser and grain nor do they have any control over the weather which has also caused a spike in food prices.

The economy, health, education, crime, debt... In tatters...

.and who shamefully walks away ...

Jacinda Ardern!

Step up Mahuta or Jackson...

Did she jump or was she pushed

Labour supporters will say it's imported inflation but it's not true. There's plenty right here in NZ. Power, water, rates, insurance, mortgage rates and taxes on petrol/diesel.

The good news is that the amenity value this represents never existed anyway due to it being non-value added costs caused by policy monopoly restrictions.

The bad news is that this is the first thing any debt via mortgage you are paying off and the interest there on.

IE the value is not real but any debt against it is.

The good news is that the debt is being eroded at the level of earning increase, which is high.

And the earning increase is being offset by the rise of interest rates and the rise of the cost of living on general.

More of a neutral sum gain.

But the fall in prices and income increases is slightly improving the median multiple ratio but not enough yet to offset the rise in interest rates.

House prices need, and have the potential to fall much more yet.

Normally we could point at active asset allocation and say - wow look what timing markets does for ones portfolio..... but in this case unless you went cash nov 21 against almost all asset types you lost. QE has been a horrible experiment and now the stupid borrowing has to be repaid at a higher interest rate.. It can only end in default for many and pain for all debtors. Creditors who seeked out high rates for seemingly low risk now learn the truth that there is no free lunch. IMHO gold is still cheap here.

Default/jubilee. The damage would be too widespread at this point, it's too far gone. A natural unwinding is no longer a pill that people will swallow after the last few years if it means financial ruin.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.