Our net worth is still falling - but we are saving more than we spend, according to the latest household net worth figures from Stats NZ.

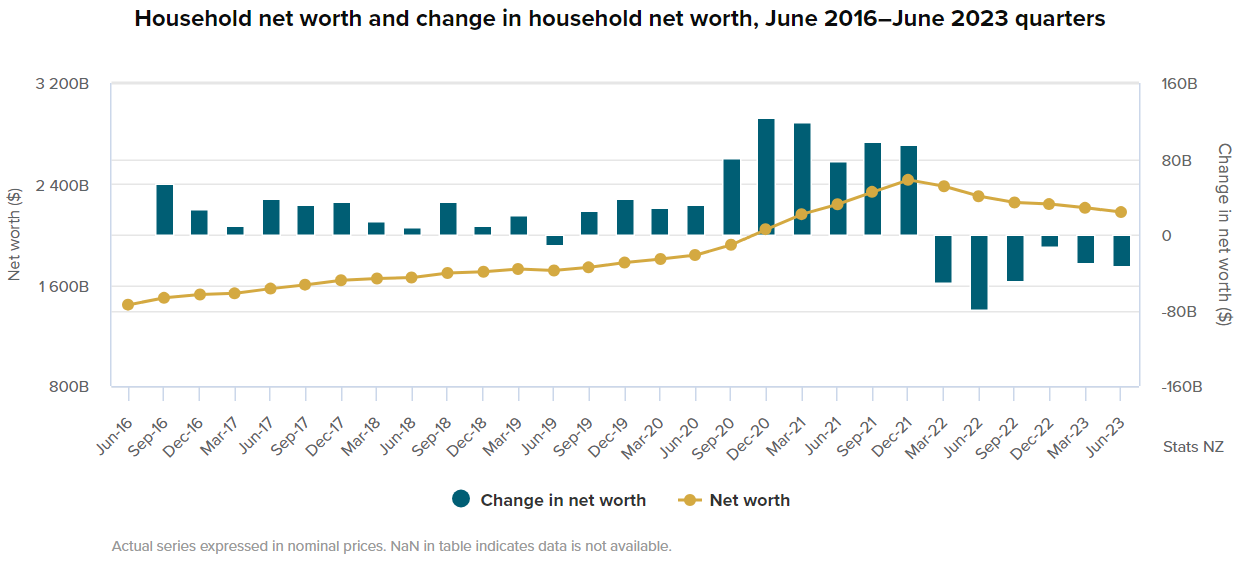

The figures for the June quarter show that the total household net worth of Kiwis dropped another $33.5 billion (1.5%) in the quarter.

Since peaking in total value at 2,433 billion in December 2021, Kiwi households have seen their net worth falling by some $255.2 billion - nearly 10.5%.

However, the drop has followed on from periods of massive gains, including a $390 billion rise in net worth in just 2021 alone.

As you might imagine, much of this has been about house and land values.

And indeed, over half the decline in the June quarter - some $17.158 billion - was due to continuing falls in property values.

"This quarter’s decrease in household net worth was mainly due to the continuing fall in equity and investment fund shares and value of owner-occupied property," Stats NZ's national accounts institutional sectors senior manager Paul Pascoe said.

But it wasn't all about property.

Pascoe said equity and investment fund shares fell by $19.9 billion, or 2.2%, in the June quarter. Equity includes the ownership of rental properties, which has also been impacted by falling property values.

The fall in equity and investment fund shares was partly offset by a $3.3 billion rise in currency and deposits, and a $2.6 billion increase in insurance and pensions. Insurance and pensions increased due to higher pension entitlements and decreasing outstanding insurance claims, mainly from Cyclone Gabrielle and Auckland Anniversary flood payouts.

A rise in household loans of $2.5 billion also contributed to the decline in household net worth.

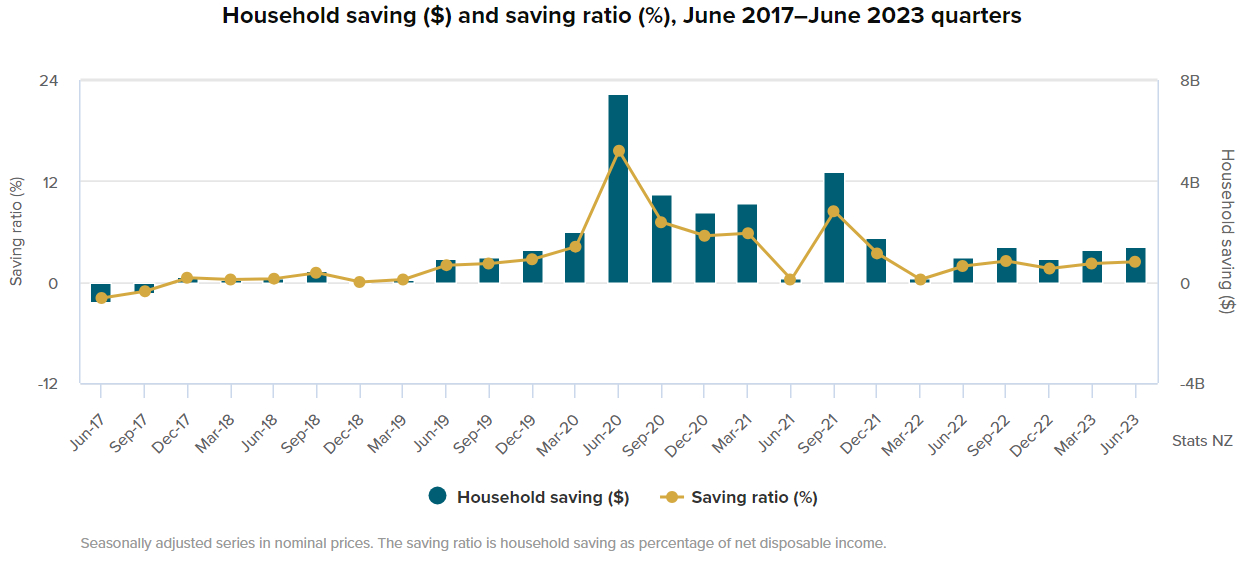

Meanwhile, though, we are continuing to save more than we spend, despite high interest rates and the general high cost of living.

Stats NZ said household saving rose $122 million to $1.4 billion in the June 2023 quarter. The saving ratio, which compares household saving to net disposable income, is at 2.4%, up from 2.2% in the March 2023 quarter. An increase in the saving ratio means that households are saving relatively more of their disposable income.

Household net disposable income increased by $952 million (1.6%) to $59.6 billion during the quarter, while household spending rose by $830 million (1.4%) to $58.2 billion. The increase in household spending was led by increased spending on services and durable goods, such as motor cars and audio-visual equipment.

The increase in net disposable income was driven by increases in interest earned by households from their investments (up $551 million), compensation of employees (up $440 million), and social assistance benefits in cash (up $251 million). Offsetting these increases was a fall in dividends received during the quarter.

50 Comments

Equity can be vapourised.

B b b b b b b b b b ut, but, but, b -

MONEY IS A STORE OF WEALTH

Or so folk were told.....

Money is, currency is not.

There are few places to hide from loss. A Rabobank TD for 1-year @ 6.3% is one example of money working hard for you. If one is fortunate to be cashed up ready to purchase depreciating assets trending towards real value, why would one not do this in such uncertain times?

Yip, with the risk of being abused as a DGM (but who really cares to be judged by vested interests? who only desire and promote one outcome - that is the one that suits their own personal finances while ignoring any information that opposes that view - but who could still be right!), there are end of empire vibes going on in the world.

Confirmation and recency bias could be very dangerous heuristics to have in this environment (i.e. assuming recent decades are going to be representative of what is ahead of us).

Recommend book on topic = 'Thinking Fast and Slow' by Kahneman.

Rents are still pushing up. Hopefully the tide of rentals going into social housing turns now, which should ease the supply crunch. I really like National's policy that certified products from outside NZ will be certified here automatically.

The only thing that will help rents now is to slash immigration numbers. Maybe NZF will be good after all with the return of the 20,000 P/A spiel.

I didn’t know about that policy, yes it’s interesting / potentially good. Perhaps a surprising policy as National buddies such as Fletchers mightn’t like it. Although maybe they could also benefit from it

Graeme Hart aka Carters donated 250k to the cause...

Wasn't the monolithic cladding product they had issues with certified in Australia and still is, cos its fine in their environment?

Smells slightly dangerous to me...

those cladding are still in use today, but how to be used has been updated since beginning, and maintenence requirements too.

Like Iplex piping perhaps?

Interesting about the building materials certification.

Rental experience - Im hunting for a larger rental now in the hutt valley. First one was from around 1905 and around $700 no heatpump, 3 bedroom, high ceilings, gigantic lounge, damp smelling kitchen, ancient bathroom, leaky vertical windows,3 sheds full of landlord stuff and 'landlord organizes mowing'.Why bother with todays mowing rates its about 12 sq m a push mower could do it? There was an old wood burner in the kitchen that is disconnected from the bedroom radiators, why not just pull the radiators out theyl never be used again.

Second one around $800 more desireable area close to train station, nicely renovated but small,again the landlord is using HALF of the double garage, absolutely ludicrous. Use a storage centre at $70 a month like the rest of us plebs.

Im not looking forward to looking at more.

The retreat of artificial price inflated by the lowest cost of debt ever. Debt that is no longer cheap.

B-b-b-b-but houses are so expensive to build just because that's how much it costs. The lowering of debt over the last 20 - 30 years has nothing to do with house prices, correlation does not equal causation etc....

/sarc.

Would we get a refund for having overpaid a wealth tax in this situation? This is the problem with taxing people on phantom money.

Councils are doing it with current rating valuations. Complete rip.

No they aren't. The rating valuation just determines how much you pay compared to other ratepayers. The total amount of rates payable remains the same. You only lose if your property dropped in value more than someone else's.

Would be good to have figures for this years “economic income” using the same metrics they used last year, so that we can show an average and then scrap the measure and the associated costs to produce it.

NZ runs current account deficits and which are a loss of potential savings and bank lending creates assets and liabilities in equal measure and so this only leaves government budget deficits as a source of net savings for households. This is something that people should be aware of when promoting government surpluses as these destroy household savings. https://theconversation.com/how-government-deficits-fund-private-saving…

Imagine how much crowing you'd get from proponents of Governments running surpluses if successive Governments continued to run surpluses for an extended period of time.

"When we said we wanted you to keep running surpluses, that didn't mean we wanted austerity!!!".

How much NZ$ max govt can 'borrow?' From RBNZ money creation documents, it is limited by how much it has spent into banking so far.

Do you know how much was this before COVID spending? Thanks

As borrowing is removing currency reserves from bank exchange settlement accounts it must have been spent first at some point in time. Borrowing has much to do with the central banks interest rate target as described here. https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/programs/…

I don't have any details on amounts but you might find something on the Reserve Bank or Treasury's websites.

Pre-Covid, Govt typically kept the Crown Settlement Account at around $8bn and had about $12bn in Ministry bank accounts. When Govt topup Ministry bank accounts they credit the institutional settlement account of a commercial bank - marking down the balance of the Crown Settlement Account.

When Govt sell bonds, they issue a bond to a bank, mark down that bank's settlement account, and mark up the Crown Settlement Account.

Thus, the only real limit to Govt spending under the current rules and policy framework is the speed at which they can spend money and sell bonds to take that money back out again. Currently the Crown Settlement Account is at $25bn and Ministry bank accounts have about $15bn of credit. So govt has a massive buffer.

Fletchers shares tanking. Article on its way?

Or is this a shares-free financial website?

I think that's more to do with their pipes problem

I think I'm down around 4.5 million or so since top (I can joke about it now, not so much at the time). But a chunk of that is taxes. Fun times on both accounts

One lesson to be learned is that your wealth on paper is just numbers on a screen until it can be realised (and even then its a case of where does it go)

A VERY good lesson on why a wealth tax on unreleased gains is often a bad idea

Spot on. Most of it's just paper or extent to which the money supply has been corrupted.

Value today of $10,000 invested a decade ago:

BTC: $2,120,615

Nvidia: $1,190,079

AMD: $274,386

Tesla: $210,848

Broadcom: $204,015

Eli Lilly: $124,632

Adobe: $105,147

Apple: $101,619

Microsoft: $96,021

Netflix: $82,755

Amazon: $83,520

Alphabet: $62,951

Meta: $64,079

It would seem like a very good idea of the goal was to disincentivise speculation on those unrealised gains though would it not..?

Just tax realized gains like sensible economies do

This is great news right?

Probably for most households their assets haven’t changed - one house perhaps with a mortgage, a couple of cars and a bit of KiwiSaver. It’s just that one of those assets is worth a lot less.

Don,t worry we are about to restart the Ponzi

Bad , bad move

Don,t worry we are about to restart the Ponzi

The Ponzi never stopped. In the U.S. unaffordable housing hits a record high. It's worse than in 2006 — just before the GFC. In U.S. cities, it now takes between 50-66% half of median h'hold income to own the median house. In San Francisco it’s 84%.

It's anyone's guess what's going to happen there or here.

Incorrect, there's been some very serious downturns in the US property market.

Lots of interesting stuff in the data released today...

Households are now earning nearly $1 billion per quarter more in interest than they are paying out - of course that masks the winning households (wealthy savers) and the losers (mortgagors). Banks are coining it in making net $3.5 billion per quarter. Govt is paying out $1 billion net in interest per quarter.

Non-financial businesses are the big losers - they are now paying an eye-watering $5.5 billion in interest (net) per quarter - nearly double pre-COVID levels. Businesses will pay over $22 billion in interest this year - that's the same as their company tax bill, or equivalent to 1/6th of total wages paid. Now tell me, how will loading that much cost onto businesses lead to slower inflation?!?

Overseas ownership of NZ currency and bonds went up by just over $30 billion in the year to June 2023 as a result of our widening trade deficit. This increase in overseas ownership of dollars and bonds requires a reduction in domestic wealth and / or an increase in domestic debt and sure enough Govts, households, and businesses all went further into debt by around the same amount.

Lots of talk about spiraling Govt spending in recent weeks(!) Interesting to see that Govt share of consumption expenditure is running steady at 25% - back to the average during the Clark / Key / English Govts (it got as low as 23% under Ardern).

Great post, thank you.

Although I suspect some are too sugar-rushed to read it, at the moment....

The saddest part of it all is on one hand that extra equity is mainly in housing and on the way up is comprised of non-value added costs that we would otherwise call waste and only exists because of speculative pressure, ie with better policy the same house could have been build for at least that much less.

But it is the 'equity' part you bet your deposit on, so when prices fall as they do, on the way down, then it is your money that goes first not the banks.

In summary, you spend your tangible savings on the intangible value part of your house.

Double Ouch!!!

It also works the other way. If you've borrowed to build or buy a house and the value goes up, you've used leverage and it magnifies the returns. That's how people get rich.

In a nutshell : Boomers are buying new cars with their rising term deposit income.

And overseas holidays and campervans.

Worked for me as a Gen X. The interest rate has gone up 0.7% in 9 months so buy a car and still get paid the same on the balance. Don't worry wont be any different for the next generation.

That build up in savings over covid is crystal clear in the graph. IMO, this explains why the RBNZ OCR rises have been slow to take effect this time around. But 'rainy day' funds don't last forever. Crunch coming and with it more mortgagee sales. The NACT 'tax cuts' and 'interest deductibility' (staged!) won't come in time to save many.

Disagree on the latter.

Loads of posters here bang on about property, its gains, and how unfair it all is.

I would say if it's such a terrific, one way, 'can't miss' bet, and it's so easy, go to the bank, borrow a million or two and have a go.

Yeah folks, paying out 8% net, plus rates insurance and maintenance is way better than receiving 6.3% before tax hassle free. Its no wonder you're on here doing what you do best - Spruik.

Thanks. Your post is priceless and should be framed :)

I've never met anyone who got rich putting their money in the bank, but I've met a lot of people who got very rich buying property. I've owned about 15 properties.

The socialists have been relegated to the political wilderness, long may it last. There'll be posts on here a year from now lamenting the fact that they've missed the property boat. The time to get on board was a few months ago.

There's also an article in the Herald today that reckons kiwis buy more houses when National win at the polls.

"I've met a lot of people who got very rich buying property."

People who get rich in property are frequently reported and reported repeatedly. In contrast, people who lost their entire wealth in property generally don't go telling people openly - that is the reason that most of these stories get overlooked / under reported.

An investment in residential real estate is not a one way bet as some buyers of 2020-2021 will soon find out. Property promoters with their financial self interests conveniently forget or fail to mention that there have been a lot of people who lost everything buying property also. There will be more coming.

A friend purchased a property in 2005 in central Auckland. The current property price is still below their original purchase price (and remember that they have been paying interest for the last 18 years). I estimate that they have made total payments of about $878,000 over 18 years - and their current net equity after outstanding mortgage is about $287,000. Paying $878,000 for a net asset now worth $287,000 doesn't seem like a property investment that worked out.

Close relatives lost all their property previously. They lost all their wealth, and ended up living in social housing until they died - they didn't even have sufficient funds to pay for their own funeral - their children ending up paying for their funerals.

A reminder of property promoters who went bankrupt in the last cycle:

1) Phil Jones - https://www.stuff.co.nz/business/8972263/Bankrupt-called-before-Assignee

2) Dean Letfus - https://www.stuff.co.nz/business/money/6051241/Property-Guru-declares-h…

3) Don Ha - https://www.stuff.co.nz/business/7580992/Property-high-flier-bankrupted

There have been many instances in other countries:

1) residential real estate buyers in Japan early 1990's

2) residential real estate buyers in US in 2005 - 2006

3) residential real estate buyers in Ireland in 2005 - 2006 period

FYI, here are examples of owner occupier collateral damage from falling house prices elsewhere around the world:

1) https://www.investorschronicle.co.uk/.../aft.../article.html

2) https://youtu.be/iKPG_l1P7lk

3) https://youtu.be/ugBKnP2FKDM

4) https://youtu.be/fiCXsu_4BoA

I guess you'd better stick to renting and term deposits then.

Previously was in the long term rental accommodation business and owned residential real estate in Auckland for over 20 years.

Exited that business when price risks became extremely elevated and returns seemed unattractive. Reinvested the sales proceeds elsewhere where returns were more attractive.

If returns become attractive relative to other opportunities, then an investment in NZ real estate may be warranted.

Most New Zealanders forget that NZ real estate is only one of many asset classes available for investment.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.