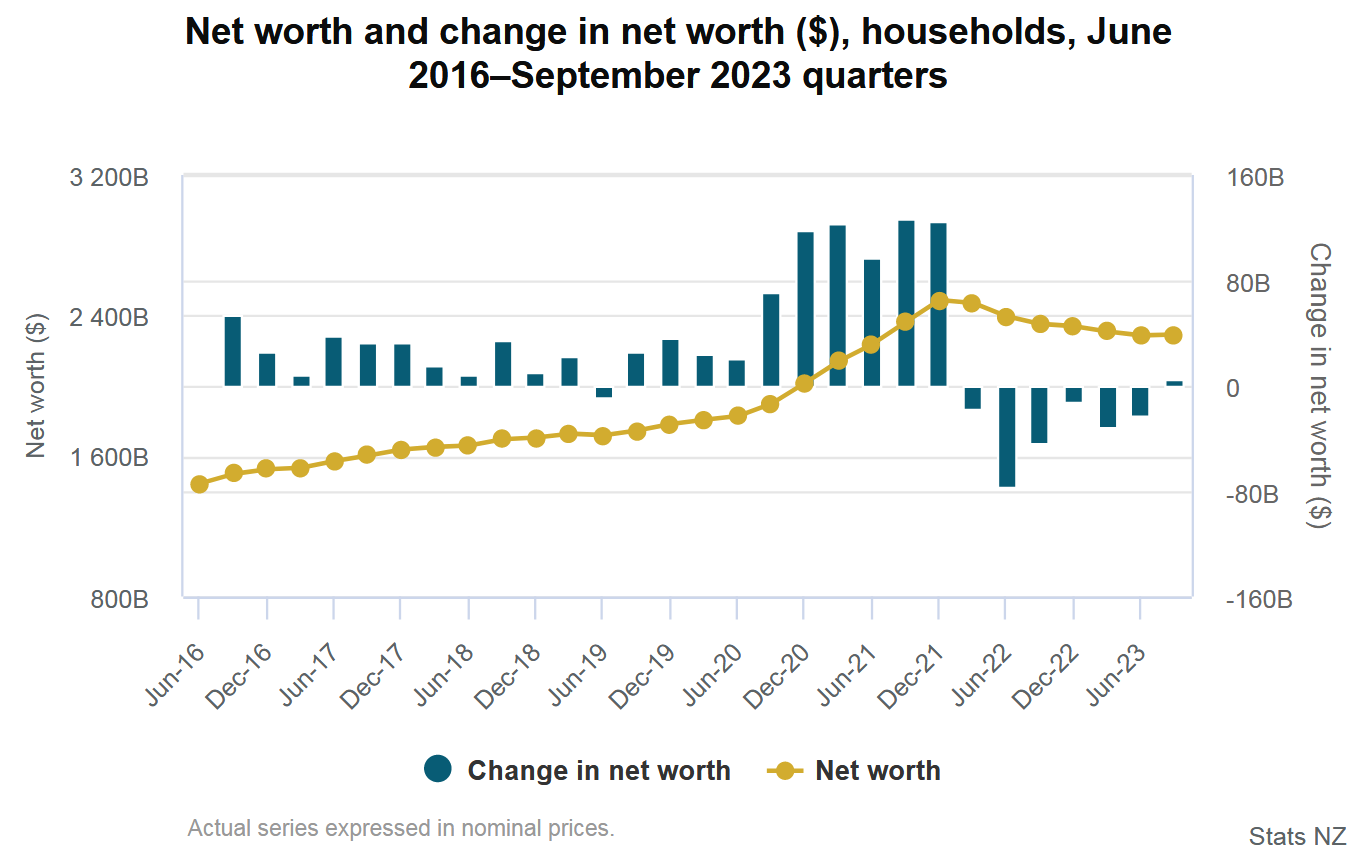

Our net worth has increased for the first time since late 2021, while we are still steadily saving some money even in the face of high inflation.

The latest household net worth figures from Stats NZ show that in the September 2023 quarter we managed to eek out a $5.3 billion increase in net worth - which was the first increase since December 2021.

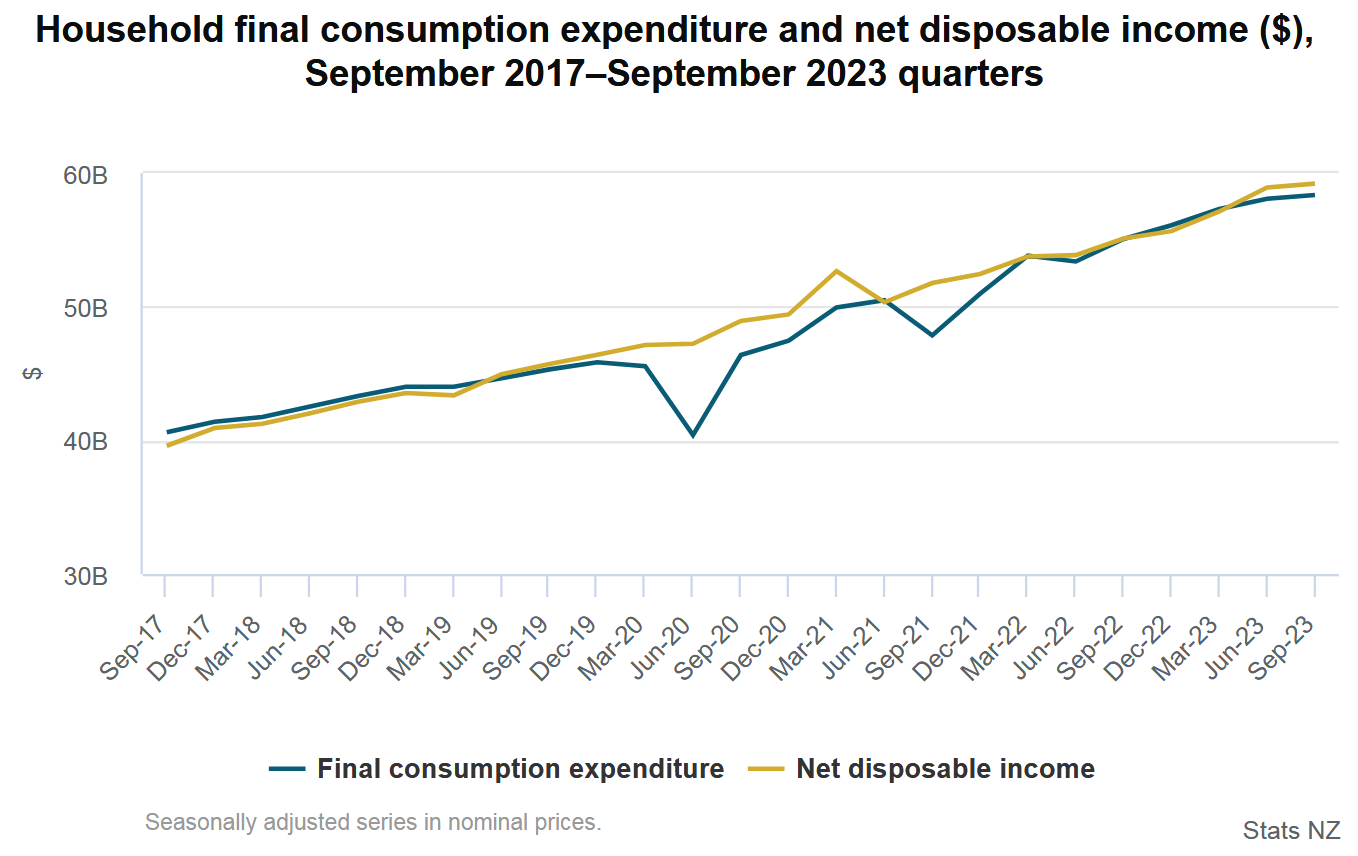

And despite increasing costs, disposable income remained ahead of outgoings, enabling a small amount of savings to be made. After total household expenditure exceeded net disposable income in each of the December 2022 and March 2023 quarters, the last two quarters have now seen disposable income outstripping expenditure - albeit not by much.

Going back to the increase in overall household net worth, this has come as house prices begin to recover.

Prior to the September quarter, the household net worth had fallen by over $200 billion (just over 8%) from the December quarter 2021 onwards - but that of course followed a period of very hefty gains prior to that. In the 2021 calendar year, for example there was a net gain of nearly $472 billion.

In the September quarter housing and land value increased by over $2.3 billion (0.2%) to $1158 billion. Before the latest quarter there had been six consecutive quarters of falls, with the total value having dropped by over $146 billion (11.2%)

Stats NZ's national accounts industry and production senior manager Ruvani Ratnayake said the September 2023 quarter increase in household net worth "reflects a rise in property values for both homeowners and landlords".

"The result compares to an average quarterly decline in household net worth of 1.4%, or $33.6 billion, over the previous six quarters.”

The grand total for net household worth at at September 2023 was $2292.5 billion, which was an increase of 0.2% on the value for the June quarter. The peak level in December 2021 was a worth of $2488.8 billion.

Stats NZ said (as already mentioned higher up the article) that 'household non-financial assets' (which include buildings and land) increased $2.3 billion this quarter, following falls in the previous six quarters.

Household financial assets also grew, up $5.3 billion, after falling in the previous two quarters. The increase was mainly due to currency and deposits, up $4.2 billion, while equity rose $2.7 billion. Household equity includes the value of rental properties less the associated mortgages held against them.

Offsetting these increases in financial assets was a $1.6 billion fall in insurance and pensions this quarter. The last time pensions fell was back in the June 2022 quarter.

In terms of household savings, Stats NZ said Kiwi households saved $856 million in the September 2023 quarter, relatively unchanged from June 2023 quarter levels.

"The household sector maintained its level of saving in the September 2023 quarter, with rising household incomes keeping pace with increased household spending," Ratnayake said.

Household net disposable income increased by 0.5% to $59.2 billion in the September quarter, while household spending increased by 0.5% to $58.3 billion. The increase in household spending was driven by price increases, as the volume of goods and services consumed by households fell 0.6 percent in the September quarter.

The household saving ratio, which compares household saving to net disposable income, remained at 1.4% in the September 2023 quarter.

Household net disposable income is the amount of money a household has once all income receivable (such as wages, interest earned, and child support) and income payable (such as taxes and interest payable) have been accounted for. It represents the money available for a household to save, invest, or spend.

Total income receivable increased by $1.5 billion for the September 2023 quarter. This was driven largely by a 2.2% increase in compensation of employees, consistent with an increase in average weekly earnings and ordinary time hourly earnings.

Household income payable rose by $1.2 billion to $23.9 billion (an increase of 5.1%) driven by income tax and interest payable. Income tax payable increased 5.5% to $14.8 billion, and interest payable rose 8.2% to $3.2 billion. All the percentage increases are compared with the June quarter 2023.

27 Comments

Up, up and away......

Have a glorious day. 🏖

TTP

Don’t think so. No mention in the article of net worth per capita, but without considering this it’s meaningless. Total net worth grew by 0.2% in the quarter. But population grew by more, so average net worth per person has actually fallen.

Spruikers bang on about increasing population creating housing demand (of course it does) but conveniently ignore it when it doesn’t fit the narrative

Very interesting numbers, thank you.

Yes, Very interesting indeed.

Stats NZ says there are 1,943,000 NZ households.

Based on the figures provided in this article-

The average increase in total income for sept quarter is $772 per household

The average disposable income is $30469 per household

The average amount saved in the sept quarter was $440, or $110 per month.

Most interesting of all was average net worth per household is $1,179,876. I find this very hard to believe- anyone elses maths different?

That number would be wrong, certainly for NET wealth anyway. Would probably be about right for face value wealth.

Yes, I also thought $2.3 Trillion in net assets ??? That sounds like too much, that would be $442,000 for each and every person in NZ, including children. Maybe the figure is for "gross" worth, instead of "net" worth ?

The grand total for net household worth at at September 2023 was $2292.5 billion

Based off homes.co.nz

Will the DTI be a party pooper? I think it just might... what will one trick pony kiwi investor do?

Not at the proposed settings.

Just saw that FHBs have become the largest group buying dwellings. A better result.

Woop dee doo.

Can we see the numbers broken down by quintile?

What about those that don't own a house? Versus those that own more than one?

And the top 5%? How did they get on?

And the bottom 5%? How much richer are they?

And people with children?

What about the retired sector?

"Twenty ordinary people are in a room. Prince John walks in. The average wealth in the room triples."

The ol' wealth distribution. Quoting the wonderful Arthur Hayes, the top 10% of US households own ~65% of all the financial assets that the Fed pumps via its various money printing programs. Boomers are the wealthiest generation, and their spending is powering a strong US economy.

The top 10% holds ~65% of all financial assets but only ~8% of the debt. The bottom 90% holds 92% of the debt but only 35% of the assets. This highly unequal distribution of wealth and debt presents a problem for a politician in a democracy. While the politicians endeavour with great resolve to do all in their power to make the rich richer, they need to get elected by garnering support from the hoi polloi. This is why when inflation shows up, it’s a problem.

I think the biggest distortion of investment and wealth in NZ stands from the lack of a capital gains tax..... This should be introduced so that gst and income tax can be reduced.

Absolutely, and CGT should apply to ALL properties!

If a CGT is applied then all expenses, repairs, rates, mortgage interest etc. should be tax deductible. And if losses are incurred, then the IRD will have to cough up. A very tricky business.

In the 1980's a lot of people (like me) made a fortune out of shares. The IRD in its wisdom decided to start taxing capital gains....until the 1987 crash, which cost the NZ Govt. billions. Since then they seem to be not that interested in gouging stock speculators.

Are you sure about this? I find no evidence of a capital gains tax during this time period. There may have been a crackdown on the level of trading leading to profits being taxed.

Buying and selling shares at ever inflating prices is no different to the property market. It has no effect on dividend income and is of no real benefit to the company as it doesn't put any money into their hands. The real damage is done by the central banks and their efforts to prop up stockmarkets and the illusion.

The IRD taxed capital gains on share trading because people were making fortunes. But it all came to a halt in October 1987 when the crash happened.

You're virtually a lone voice crying in the wilderness. The family home is sacrosanct, which is why its exempt under the brightline test

And so it should be. Why should it cost you a fortune to sell your house, move across the street and buy one of equal value?

Speculators have always been liable for capital gain.

Speculators have always been liable for capital gain.

That is the most heavily quoted yet least applied tax rule

What happens if there's a sudden plunge in property prices and lots of people are making losses?

And that includes rates, insurance, repairs and other maintenance. Da gubbermint has to cough up...big time.

Not really. It would depend how the law is written. Write it as a capital gains tax not a capital loss refund.

Two intended consequences - broaden the tax base so other taxes can be reduced and encourage the masses to move away from chasing capital gains. Ideally a capital gain is a bonus not the purpose. To bitch about paying tax and not seeing the gain in one's hand is obviously the other flaw in one's mindset. The capital gains model/speculation (and central banks reactions), especially since the dotcom bubble is literally the cause of our economic and financial imbalances.

Wouldn't need a sudden plunge. I could just sell my house to my sibling/spouse/close friend for a "huge loss". Claim the tax refund. Then "buy it back" off them at the "pre-loss value" in a private sale. No money would need to change hands unless the lawyer needs to see in trust account.

Sibling has $2m in bank. I have $800k house. They buy for $400k. I claim loss. They gift me $800k. I buy house back at $1.2m ($800k + $400k).

I have my house back, they have their cash back. I've not made a profit yet, so in theory I could sell my $1.2m house to another sibling for a loss. Rinse and repeat.

And that's how you got in debt to IRD with multiple punitive penalties

Not see a decent article on this for over 5 years now. I suspect the percentages of people in each "category" have not changed much, the bottom 10% actually owe more money than they are worth so they have a negative net wealth. No doubt you need a whole lot more now to make the top 5%, probably in excess of $3million individually.

+3m individually is not much if you are talking top 5 percent

Not much has changed. We are still going backwards socially, psychologically, relationally & morally - to name a few.

PAYE, the low hanging fruit. I am in the top 1% of income earners but I’m far from wealthy - I’m lucky to own my own home (albeit with a mortgage). While I understand and accept there is a need for a 39% tax rate, it disproportionately captures skilled salaried professionals, while the real wealth goes relatively untaxed. Top 1% income is not in the same universe as top 1% wealth.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.